Hi Dj,

Thank you for the analysis. Can you pls. explain this: Anything below 180 increases risk reward ratio? any reason why? Is the analysis done on technical parameters?

Hi Dj,

Thank you for the analysis. Can you pls. explain this: Anything below 180 increases risk reward ratio? any reason why? Is the analysis done on technical parameters?

Hi Akshay

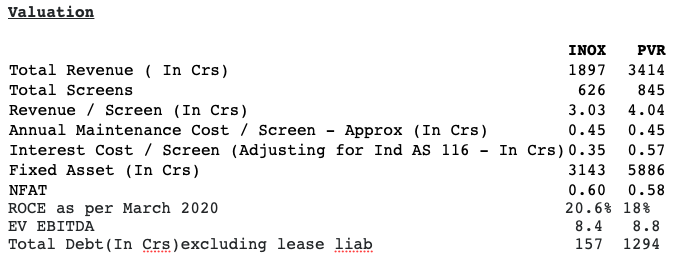

As I have covered in the template.i am expecting them to do sales of around 2500 crore in two years from now and a net profit of around 200 crores … So that gives a mcap with a avg pe of last few years ( 25) around 5000 crores. Since the current price is around 200 rs and mcap 2000 crores … so a horizon of 2-3 years can result Into above average market returns if the above scenario plays out … now if the price keeps on correcting the expected returns will increase accordingly. 180 is just a price anchor …nothing more…

Big if in all this is how virus situation evolves and how does inox contain there fixed costs during the lockdown. q1 results and concall can address few issues

Regards

Divyansh

Regards

ATP is pre tax or post tax?

30th April Concall transripts https://www.bseindia.com/xml-data/corpfiling/AttachLive/49425061-76d5-49a1-b9ca-fd7a62fd55b9.pdf

As the stock is trading at a 52W Low also at aprox 5YR low, with positive cash flows and excellent management, I believe the company is in a temporary trouble.

The reasons I believe the stock will rebounce is:

Should we catch the falling Knife?

One of the factor we should estimate is, if everything does bad for the company, how much time can it survive with its present cashflows and reserves. If the company can survive from bankruptcy, then its a catch. Eventually when things get on track like may be in a year or so, the stock will perform.

I will share my analysis of the above. If anybody from the community can do the analysis, we can compare it.

Do correct me, if there is anything wrong in my analysis!

Disc: Tracking. Will consider if PE<10.

I read their con-call of a few days back.

The company is (almost) debt free.

They have about Rs100 crore cash and a few monetizable assets. This should last them for 6 months at the minimum.

They were extremely confident in saying that they won’t be paying rents (Force Majeure).

The CEO, Alok, literally gave a threat to the producers that if they go the OTT route, then there will be trouble for them. So, a few small producers can take the route of OTT, but big budget movies with established studios cannot. Also, movies of superstars needs theatrical release to recover the money.

From concall transcript -

I mentioned earlier our monthly cash burn is about Rs.15 to Rs.18 Crores so with our current funding that we have Rs.100 Crores we can withstand another six months of the shutdown,I donot think it will come to that, but we could if required

Above is funding line from bank

Siddharth Jain:I think debt net of cashwas aroundRs.110 Crores.

Deepak Gupta:The cash on the books is about Rs.100 Croreswith treasury?

Siddharth Jain:With the treasury and the cash it is north of that

Key risks:

Once they start operation there could be single shift of operation

Due to physical distancing less occupancy and less F&B sales

Discounts to attract customers

These may lead to OPM impact and could be loss ?

Increased debt level so it will no longer a net debt free company after 6 months

Also who is to confirm this will last for 6 months and not longer?

So what is the margin of safety as a investor for us? This is as good as company whose plant is shutdown indefinitely.

I would wait for bottom confirmation using technicals

Check for Q1 & Q2 results before taking portfolio position.

It would be great if someone can share their view basis similar situation in past.

This template was shared by me on apr 30 when the price was hovering around 200 odd levels. few developments since then :-1

Cinema Halls to remain closed till July 31 as per Unlock 2 guidelines.

OTT platform Disney+ Hotstar to release 7 big-ticket movies in next two month starting July 24.

A setback to PVR and Inox Leisure in mid-term.

I don’t see them opening even after July 31st anytime soon. There are simply too many cases to justify it.

PVR and INOX are still trading at rich valuation of 30x and 20x PE based on peak cycle earning. Both will not be able to do a single penny of business in rest of 2020. There is long way to fall for both stocks.

Yeah. Curious how market will react to a near zero revenue Q1FY21 result.

What levels would you be comfortable jumping back in ?

We know Q1FY21(maybe even Q2) is zero revenue.

Hello

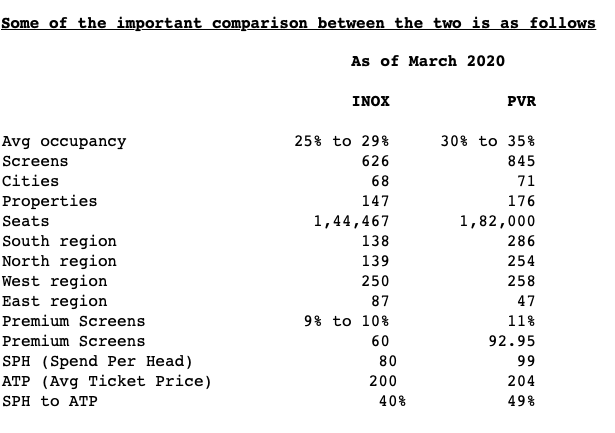

Price is not the only Variable which one should track for a business going under a period of high uncertainty and high risk…

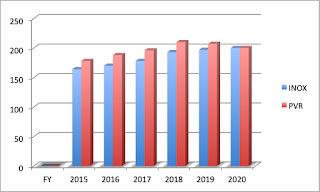

Avg Ticket Prices btw 2015 to 2020 of INOX & PVR

CAGR - INOX 3.36%

CAGR - PVR 2%

As per both the managements going forward ATP shall rise at 4% to 5% which should be annual inflation rate

This generally depends upon the footfall in the multiplex

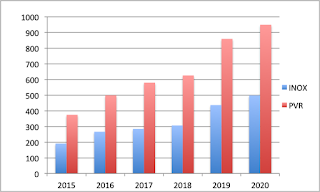

Food & Beverages

Amount in Crs

CAGR - INOX 17.28%

CAGR - PVR 16.72%

This is high margin business as gross margins are close to 75%. As per management improvement in margins not possible

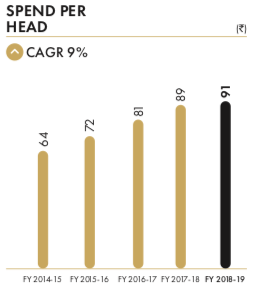

Spend Per Head

PVR

For FY 2020 SPH is 99 INR which gives CAGR of 7.54%

As per Annual report of PVR 2018/19

INOX

CAGR - 6.44% (SPH) FY 2020 SPH is INR 80

Advertisement Revenue

PVR & INOX both do not want to increase the number of minutes of advertisement on screen.

Currently INOX caps it at 19 odd minutes and PVR caps it at around 22 mins per show per screen of advertisement.

Both chains looking to increase yields by increasing the rates of advertisement

It is still the cheapest medium of advertising and has a lot of headroom for improvement as per both the chains

Also they aiming to increase offline advertisements as the proportion of it is just 10 cent to the overall advertisements. They see a lot of scope to increase the revenue from offline advertisements.

Advertisement expenses have started to fall since the start of FY 2020. As the economy slows advertisement spends are cut by the corporates

OTT Vs Theatrical Release

Concalls Of PVR over different quarters

Talking about the gap between movie release on OTT and Theatrical release

Concalls of INOX over different quarters

Talking about direct release on OTT platform

I think this move is a validation of the fact that OTT on television is a failure in this market and if people are going to watch OTT on phone that experience is really substandard as compared to cinemas.

Globally if we see the producers they have released some movies but at the same time they have also delayed the releases of some movies.

For another argument regarding simultaneous movie release on all platforms

OTT doesn’t give amount of revenue needed for big box office collections

OTT doesn’t give clarity as in the total collection in numbers whereas box offcie collection was known to everyone from theatrical release of the movie

Last but not the least the movie watching experience.

AMC updates - Amazon thinking of investing in AMC cinemas - Rationale

A distribution channel for Amazon content being produced, a guaranteed outlet for its own production

Get more people subscribing for amazon prime

Can get easy recognition for awards

Can create additional revenue stream for the contents

Well, there is no word on the investment as yet so we ll have to wait & watch for the further action in that direction.

Other Updates

PVR

They have opened one property with multiple screens in Colombo Srilanka. They see a lot of traction in that market

They cancelled the plan to set up screens in Saudi - middle east

Focus is to open more screens at tier II , III & IV cities in India to increase the reach.

VR technology is still in its nascent stage so difficult to commercialise the same as of now.

Trying to develop the popcorn brand by increasing retail sales outside of multiplex. They hold close to 70% stake in Zea Maze (developing Popcorn brand - still making losses)

As per one of the concalls of PVR in quarter 3 of FY 2020 - You will not see very high growth rates at least in the near term, but we still expect to deliver growth, maybe single digits in the ad revenue in the near term and as and when I think the box office outlook improves and we see some bit of improvement in the economy this will also move up.

SPI chains of cinema taken over by PVR operates in southern region of India at 50% to 51% of occupancy which is considerably high looking at the national avg of 30% to 35%. EBITDA around 20% to 25% which is good and it can capture some local content easily.

INOX

They have started taking group bookings for sports / concerts. Generally for the weekdays. They had the rights to telecast world cup cricket matches

Looking to increase yields in advertisement segment.

Trying to increase the occupancy from 28% to above 30%

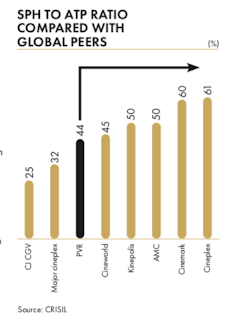

Making lot of efforts to increase the SPH to ATP ratio.

FY 21 will be EBITDA negative

Looks very difficult to even be able to work at 50 cent of capacity post Covid.

Some Common Points

Have partnered with swiggy & zomato for online delivery of their signature products directly at home

Both PVR & INOX chains focusing to increase the premium screens. Trying to increase the proportion of premium screens to total screens

Premium screens have almost double ATP and higher SPH to ATP ratio. Also it attracts better rates for advertisements.

All the new properties which come up takes about 4 to 5 years time to reach break even

On an average setting up cost of a screen is 2.5 Crore to 3 Crore

After every 6 to 7 years renovation is carried on to the screen which usually comes to 30 cent of total set up cost of screen

Other overheads are around 40 lacs per screen per annum.

Ultimately number of people walk-in into a cinema has a direct impact on our EBITDA.

Only and only good content can increase the footfall in multiplexes.

As per one concall of PVR , they make operational losses if it is only one segment of movie exhibition which is their core segment to get revenue. All other segments are directly or indirectly depended on movie exhibition

Key Risks ( From Annual Reports)

1 OTT direct first day releases

2 Piracy

3 Ticketprice regulation in some of the states

4 Restrictions on number of shows

5 Regulating the food & beverages prices inside of multiplex

6 Development of real estate slowing down

7 License requirements to start operating

Excellent compilation. Do you have the details about the rent they pay per square foot?

Thank you!! No they don’t disclose rent paid for an individual property, so that is not possible to identify… But they choose all the properties on the basis of ROCE. Generally a new screen gets to BEP in 4 to 5 years time as per one of the concalls of INOX.