I started my investment journey around 2017 July ( summit of a bull market ). Started with a capital allocation strategy of 40% debt and 60% equity. Out of 60% equity, I have mix of mutual funds (60%) and direct shares (40%).

As a starter, searched for the shares with lowest price point Started investing in duds like future consumer, pcj etc. Then I started reading books like Once upon a wall street, Buffets letters, valuepickr posts etc and realised my errors. I was lucky to get rid of all those duds before the meltdown in January 2018. Even though I didn’t gain anything, protecting the capital itself was a big achievement in hindsight now. Then I started analysing individual companies in detail. It included reading quartely results, concalls, annual reports, valuepickr posts etc. Still learning, and here is my portfolio.

Mutual fund(SIP) breakup:

Large Cap ( SBI and BSL Frontline)

60%

Mid & Small ( Franklin smaller, Axis midcap, LT emerging)

40%

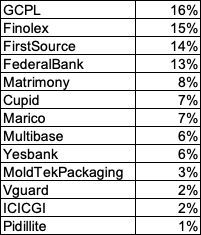

Direct shares ( mostly small/mid cap as mutual funds take care of large cap)

Godgej Consumer

15%

Strong brand and products.Very transparent and strong management. Betting on sales from Africa and other South Asian countries

Finolex Cables

12%

Strong brand and distribution network.Management is good. Betting on real estate revival.

Matrimony

10%

Strong brand. Big moat of million profiles. Very good first gen management. Betting on growth in North India ( comparatively young population compared to South)

Federal bank

10%

Very good and conservative management. May not be next HDFC, but still a lot of room to grow.

Cupid

10%

Moat is FC and WHO approvals.Good management( risk of ceo replacement).betting in growth in US and increased gov spending across worl on condoms).

Multibase

8%

Started investing after checking the products and parent company. But parent merging caused a lot of issues. Biggest wealth destroyer in my portfolio till now. But I will still wait for one or two quarters before declaring it as NPA.

Yesbank

7%

It was a trading bet, but forgot SL . Still hoping for revival.

First SourceL

7%

Strong IT, BPO company available very cheap ( because of brexit uncertainty). Management is very good.Reduced a lot of debt.

Eris

6%

Domestic pharma with no noise of USFDA. Primarily a sales company I would say, not pharma as they don’t have string R&D capabilities. But will keep in portfolio as long as they report good numbers.

Advanced Enzymes

6%

Here the moat if strong R&D skills and only a limited companies are there in this space.

Vguard

3%

Very strong brand around stabilisers. And these are a must for new TVs and AC ( people wont mind spending 1500 for protecting a 50K tv ). Betting on growth across other products and pan India.

ICICGI

2%

Got from IPO.

Trident

2%

Reporting very good numbers every quarter and strong presence in US market. But I wont be committing more into it as I don’t see any moat.

NB : I still have 40% networth in debt. I will move it to equity if I find good companies cheap. But all good companies are still expensive compared with historical averages.

Thanks @sainkar for the feedback. My SIPS are spanned over entire month. And regarding exposure to small/mid caps,it is deliberate. 50% of my entire portfolio is in large cap funds. It includes a large exposure to HDFC, ICICI, ITC, Kotak, Reliance, Unilever etc. And for direct equity, I don’t find any of these companies cheap. I will buy more of these if valuations come down.Lets wait and see.

While I don’t think there is anything wrong with most companies you’ve invested in, I would like to draw attention to your investment thesis for some of them.

GCPL is not doing very well in Africa. I’m personally tracking this company too. My idea is that men’s grooming will form a considerable part of the company’s journey in the next decade. They’re also very good at acquiring companies, so I would expect a good amount of inorganic growth too.

From my limited understanding of the online matrimony market, this is not a moat. The market is highly fragmented. Whenever I’ve heard about people using online tools to search for a groom/bride, they have used websites that cater to a very specific religion/caste/sub-caste. I have not done extensive studies on this, so you may very well be right.

I have Cupid in my PF. I don’t think the company’s moat is in their Female Condoms. The moat is in the fact that condom manufacturing is a business with terrible economics and Cupid, with its cost-effective manufacturing process remains one of the very few profitable condom companies in India (And indeed perhaps the only profitable one in the B2C/B2G2C space).

An equally important moat is in the fact that it takes at least 5 years of trails and approvals to even enter the B2G condom market. That’s a massive entry barrier. The fact that there are only 3 competitors to Cupid in this space and only 1 of them considerably large (Veru-FC) simply verifies this for us.

They say ‘Hoping is not a strategy’.

You either know why you are holding a company or you don’t. If you don’t, sell it. The fact that it forms 7% of your portfolio only makes it worse. You seem to be confident about Federal Bank already, so why not pile on to that instead?

I hope this helps. All the best for your investment journey.

GCPL

Agree that they are not doing good in Africa currently. But they have a very good presence there in hair dye/ personal care segments. From AR : ‘In fact, our largest investment as a company, of ₹4,000 crore, is in Africa. Our Indonesia business has picked up its growth momentum and is outperforming the industry in a tough macroeconomic environment.’ They are headwinds in short term due to overall global slowdown, but eventually demand should revive. For men’s grooming, Marico is also interesting. Its in my watchlist and seems very expensive.

Matrimony

Agree that the market is highly fragmented. But don’t you think that itself is the biggest opportunity for organised players like matrimony?

And religion/caste/subcaste level searches, matrimony owns a variety of portals like BharatMatrimony.com, CommunityMatrimony.com, AssistedMatrimony.com, EliteMatrimony.com and a lot of regional portals which caters to these specific groups. From my understanding, their biggest moat is the huge number of profiles. Nobody will go to a service with less number as choices are limited and it will create a feedback loop. Once a leader, it is difficult to dislodge because of network effects. In north/west, biggest player is shadii.com . Matrimony.com is focussing a lot on North market now and growth should come from north west as the population is young there. With the growth of internet and mobile app, a lot of people will be using these services. And they have now introduced photography and other marriage related services. If they can crack north/west market, it would create a lot of opportunities for wedding related services as well ( people spend a lot of money on wedding compared with south).

Cupid

Completely agree to your point on moat. When I said approvals, I meant the same time period required for trials and approvals. Would like to know about your thoughts on US market FC? Won’t that be a big boost considering the margins on FC ? I would not like to bet a lot on B2B orders. I will wait for some more quarters to see the development on B2C space before taking a decision on it.

Yes Bank

Remember, Hope is a good thing, maybe the best of things, and no good thing ever dies

Not in share market I guess avneet Gill is cleaning the books as he has been doing for last few quarters. So I don’t see it going down entirely. I won’t be putting more money into it as long as no good news comes. But as my allocation increases across other stocks, this 7% will come down and I am fine with that risk.

Advanced Enzymes - Nothing specific to point to but it could have corporate governance issues, better get out. Also I would get out of Cupid similarly.

Matrimony looks interesting and i will read up on it. Recently created profile for a relative and they seem very aggresive in calling us to purchase the premium plan. We did end up buying and got a good match. Experience of one matrimony agency was very bad. They promised to give 3 matches per week but took profiles from online sites only. Complete waste of 14-15k money. I think if matrimony sites give option to pay some small amount to unlock a single profile vs buying full membership for few months, that would increase the number of transaction volume.

Thanks @bhaskarjain for the feedback

Could you please highlight the corporate governance issues with AEL/Cupid? I couldn’t find red flags to be honest.

It’s more of a perception of people who follow them regarding the promoter quality in those two companies. Not to scare you out of your position but you can be more careful regarding them. All the best.

The opening batsmen seem the best of the team. Godrej consumer and finolex cables are decent companies. Matrimony I feel is not as strong a moat as people make it out to be.

Among banks and private sector banks, my preference is for solid banks like hdfc bk or kotak bk or if one wants to go into smaller banks, dcb bank. These have very little worries on the npa front. (unless something crops up there too.)

I myself was sucked into multibase looking at the previous numbers and growth potential but the last couple of quarters and loss of a part of the business has been a shocker.

Yes bank has been very well discussed on VP thread on the company. You will find both sides of the views but as of now the guys with negative views are having a laugh and those invested have borne a lot of pain. How it plays out is anybody’s guess.

First source and Eris are okayish type of companies. Nothing great but not too bad.

Vguard is a solid company with good management and track record.

Advanced enzymes has failed to live up to its billing and has been accordingly punished. Trident is a cyclical and could suffer the risk of trade sanctions. Cupid remains a one trick pony and has disappointed till now with the odd quarter of good growth. What it needs is consistency but looking at its business model its unlikely to be consistent and hence markets are not likely to give it high valuations.

The really interesting part of the portfolio is the watchlist you have put up. All of them are dominant players in their own niches or segments. I would prefer to add more of them and get rid of the poor quality companies in the PF even if it means booking losses.

@hitesh2710 Thanks a lot for your review. Could you please share your thoughts on below queries?

why do you feel that matrimony moat is not that strong?

How do you deal with a situation like Multibase when there was not even a hint of what was going to happen? Should we immediately get out of the script or wait for clarity to emerge?

The problem with watchlist is none of them are available at a cheaper price. All and expensive compared with historical valuations.Still sitting tight on cash for some opportunities.

For a company like matrimony’s moat to be successful, the network effect has to come into play very strongly. But in the Indian context, besides the other online matrimony sites, there are a lot of other offline matrimony institutions, caste based matrimony organisations, private players, newspaper based matrimony ads etc. So the moat is not as strong as believed to be. Those interested in finding spouses register in multiple online sites, or are registered with various other options and hence the true network effect never kicks in.

In a multibase like situation, its better to get out as early as you can.

Try looking out for companies which have delivered good results and whose stock prices after initial kneejerk upmove have settled in a tight consolidation range (now dont ask me which ones )

This atleast tells you that markets have received the results positively but upmove remains pending till market situation improves. . These, if the results will be consistent would be the first to move up once market sentiments improve.

Problem with sitting on too much cash is often one tends to get paralysed and keeps praying for lower prices. Ideal scenario would be to zero in on companies which we want to invest and buy in small lots with SIP kind of mode for next few months.

Thanks @hitesh2710

Matrimony has a lot of regional/caste/age based domains which are catering to different segments of society. One more factor I consider is the wide spread mobile phone app usage. I am expecting this might result in more people moving to organised players like matrimony.

Absolutely agree with your comment on multibase. And I wont be asking you stock tips

Regarding cash position, I do have certain range of values in mind. If any of the stock in my watchlist is correcting to those levels, I will certainly deploy it.

And regarding the valuation, eventhough small/midcap correction is very severe, large cap stocks are not at all impacted.All of them trade at historically high PE values. Examples are HDFC,Asian paints,pidillite,hul, Nestle,TCS,dmart and most other fmcg stocks. If economy picks up again, do you think these stocks will again go up breaching all historical valuations. May be earnings might catch up, but if the earnings increase, won’t more money again flow into these stocks keeping its valuation high? As I started investing recently, I am not aware of the mood and sentiments during 2008 melt down. Was it similar to current economic scene where some stocks(best ones) are resilient to these macro events? Could you please share your thoughts around it?

Pidilite is for tracking, will add more if price matches with value in my calculations

Entered moldtek packaging recently as I see they are supplying lot of packaging for big giants like cadbury, amul, heinz etc ( checked in supermarkets nearby).

From a packaging industry perspective, they are performing well ( good sales growth, less debt, good ROCE and a fair OPM). And with governments banning single use thin plastics across country, I see that as a good opportunity for players like MoldTek.

But same promotors are running Mold-Tek Technologies ( engineering and IT services) as well. I really want to understand where their priorities are before committing a big capital into it ( seeing all the frauds happening with small cap cos).

Until I am convinced, I wont be increasing my allocation.

Completely liquidated ITC, GodrejConsumer,Vguard,Havells,Cuoid and Matrimony. Less than 5% gain . Liquidated some mutuals funds as they were still in Green.

Sitting on 80% cash now.

The situation is very gloom and whole world is coming to a stand still. Next two weeks, we might see US , EU and probably India as well, introducing more and more lockdowns.

I am planning to deploy cash in coming 6-8 weeks very slowly, but again depends on the situation.

Good, as long as you have a strategy. Only question is - Markets run much ahead of times, specially in such situations. What if market at current levels has already factored in the shutdowns and spread and eventual control in 3 months. Very hard to tell…I wish the control in India happens this month itself…not for sake of Markets anymore…Thanks

Agree. But even with recent selloff, most of the quality bluechips are still at frothy valuations. And they are the last pillers to hold when entire castle is coming down. I still feel that market has not captured all the ground reality. It’s totally different from 2008, a true black swan event.I am sure we will come out of it, but I will wait a little more to see at what cost…I don’t understand technicals, so not sure of bottom or reversal…I am closing observing situation in Eu and US, will take a SIP approach based on what happens in next two weeks

). Started with a capital allocation strategy of 40% debt and 60% equity. Out of 60% equity, I have mix of mutual funds (60%) and direct shares (40%).

). Started with a capital allocation strategy of 40% debt and 60% equity. Out of 60% equity, I have mix of mutual funds (60%) and direct shares (40%). . Still hoping for revival.

. Still hoping for revival. )

)