I think thats the fair point…Lodha tower only contribute more than 100cr in revenue and today the whole company stands at 25cr mcap.

And if things turn positive than it will become multibagger…

Some risks which i consider is corporate governance issues…

And why innovators facade not declared last qtr results ?

Of course. This is a risky investment as are many microcaps. I have currently allocated really low percentage of my portfolio to it. Famous investors have their allocation low too when seen by the size of their entire holdings. I see it as an optionality with asymmetric returns. I can be dead wrong here, that is why I am waiting for more information here to act more decisively.

I think market cap is the wrong metric to judge here. They have around 150 Cr of sales and market cap of 25 Cr. Moreover, the façade industry can grow exponentially in India.

Yes, it may take long time to deliver returns as they have limited capacity. But with current capacity also, it seems vastly undervalued.

But I think tracking such microcaps from a long term perspective and lapping them up when conditions seem right is the correct strategy.

If anyone can go and check ground level situation like go to LODHAs site and trying to gather some primary information about the companies image with lodha.

That could clear many doubts…

If lodhas are satisfied with innovators than they will defenately going to big !!

See the current valuations are really mouth watering and if mr.kedia and mr.sekhar is not completely wrong than it could be MB.

Personally i am not so impressed with mr.radheshyam sharma and his son but thats could be wrong…

Sir,

I think both are different towers in a big project.

One is World View and other is World One.

But i wonder why Lodha choose different partner for the towers located in same premises

I had a talk with a person who previously worked with the company.

All I can say that tbe company is legit and had completed good projects.

He had huge respect for the promoter

There are three brothers, 2 of them are involved in this business.

They had more than 25 years of experience and have acquired some kind of technology which make their process easier.

Now

Will the company survive or do well in future is something cant be surely said.

But I think if the company has survived for 25 years is something we have to appreciate as there were multiple economic issues in the years in between.

If somebody has any other insight, request you to please share.

@preetkaran - i would second that. I have met the promoters around the IPO time and also visited their factory. They have experience and infrastructure. With IPO proceeds they seemed to be making investments in automation and better capabilities. Good thing was that next generation has joined and seems competent and trying to grow the business. The last big project they bagged was quite prestigious as the facade was for very high rise building which is not easy to do.

Negatives - very working capital intensive business. They had issues of bad debt (or issues) from past projects, which came to light after IPO. Given Covid, real estate would be badly affected for sometime and it would impact the company.

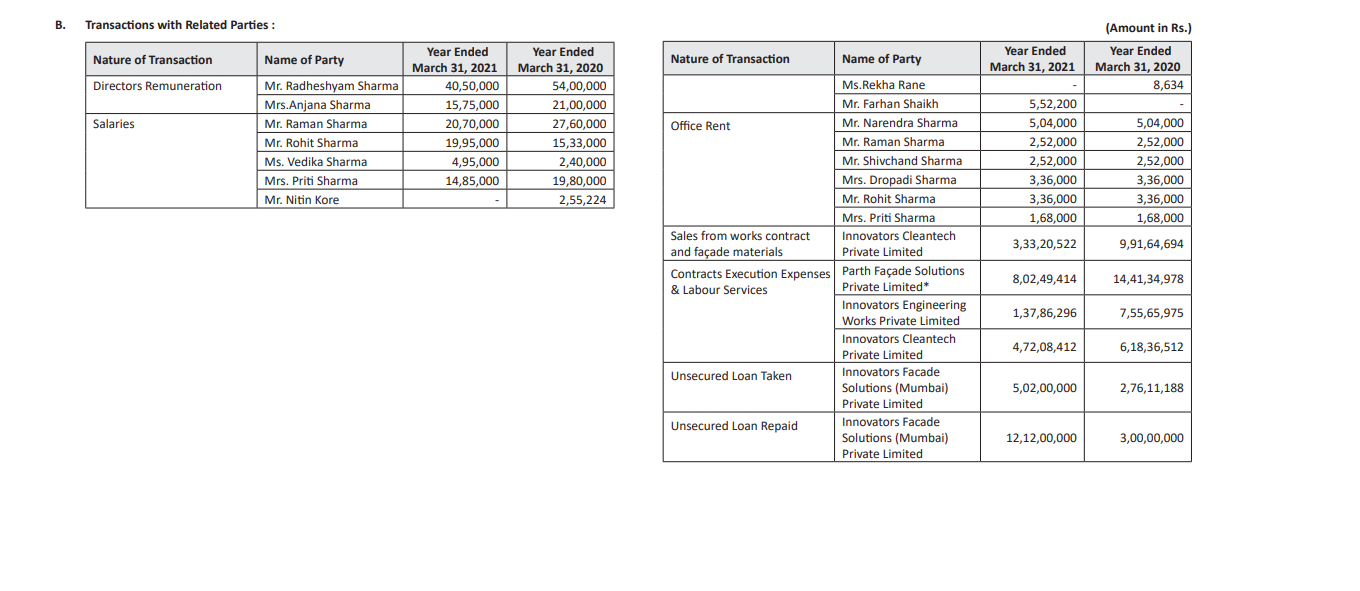

Can someone explain remuneration of directors. As per the annual report 2019 remuneration of directors is 75 Lacs but as per the companies act,2013 it should have not exceeded 11% of the net profit (4.65 Crores) of FY 2019 i.e. approx 51 Lacs.

I was trying to initiate a tracking position with IFSL. But upon checking found that the share can be purchase in bundles of 1600qty only. I am novice in equity and this was something new for me. Can anyone explain the reason for this.

I am also facing same problem. Wanted to buy small quantity for but minimum 1600 shares need to be bought.

People who have invested small amount for tracking, can you please explain how did you do that.

IFSL is a SME offer (Listed in BSE in M catagory) whose minimum Trading lot is 1600 meaning you can trade only in lots of 1600. Many of the SME offers are in multiples of 100 only Another SME offer Valiant Organics (CMP Rs1300) in 150 lot. When the scrip migrates to main board then the trading lot will change to 1. Hope this answers your query.

Had a talk with current employee

Some points noted

Current Projects

a. Lodha Tower 76 floor building

per floor costings 2 cr approx

total billing 136 crores

Its the most expensive project taken by this company till date

b. Raheja Buildings (Mumbai)

Project cost 20 cr

c. Bandra Hotels (Mumbai)

d. Galaxy buildings (Hyderabad) (35 crores)

e. other projects in chennai, goa , delhi

Do these guys have some technologies which they can differentiate

ANS: Not as such

competitors

a. glasswall

b. Amco

c. Shreeji Facade

was optimistic about facade industry

the real estate companies are currently facing problems (labor issues, supply side issues etc) may take 1.5-2 years to get in track

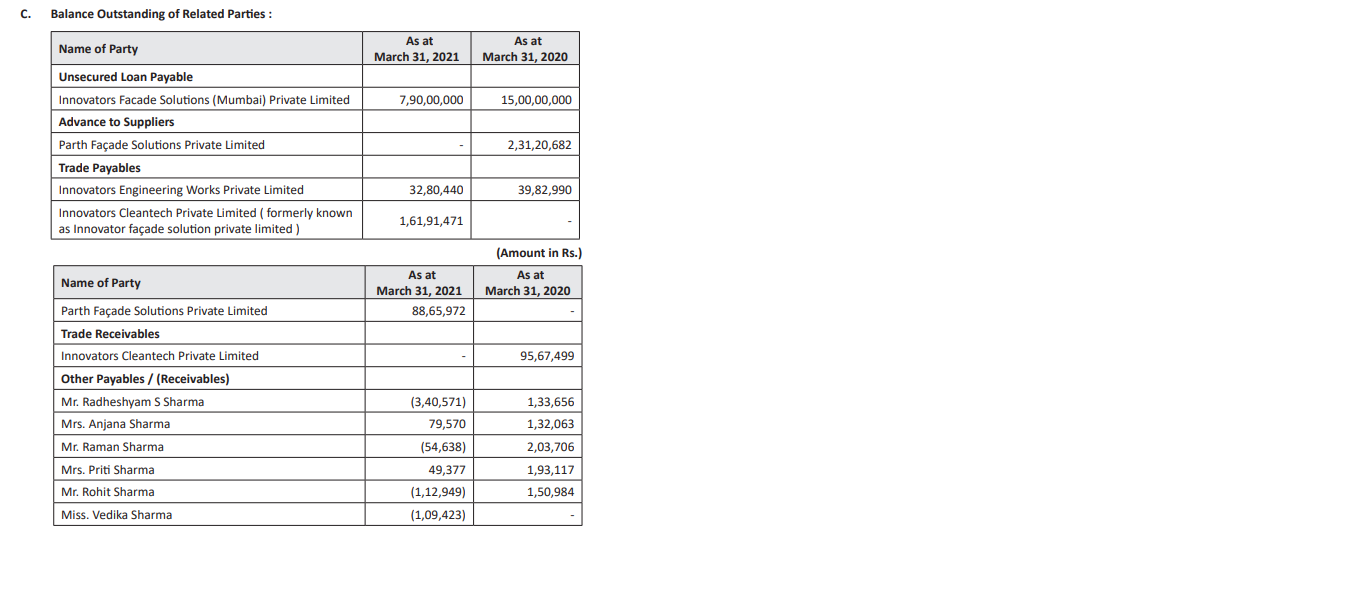

Like I mentioned about stuck money in past projects, it seems that the company has provided for the same along with some more write-offs. Overall, its poor to see companies hiding these things before the IPO and cleaning up the books when things are bad.

I hope the management gives explanation around this and about things going forward.

@ayushmit sir if they r hiding such things before IPO than how investors like mr.vijay kedia bought 10% stake!

Sir just try to understand from u what i was missing ?

Hi Kuldeep, I don’t think it’s easy to figure out the negatives from before even for big investors. I have interacted with management and seen their factory and from that perspective things seem to be all right. Couple of years back there was frenzy in the SME space and people were lining up to be anchor investors today the sentiment is opposite.

If operational order book is good and cleansing of books are done with then there could be possiblity of better days ahead.

BS is improved as there is no increase in borrowings and good decline in inventory and receivables.

So post covid19 crisis era, this could be good bet.

Disclosure - Not invested yet, but may enter at lower levels…