Infollion Research Services Ltd

The company was formed under the name “Infollion Research Services Private Limited” on September 9, 2009

Infollion research services is in the business of providing platform for contingent staffing.

What is contingent staffing? → Contingent staffing or Gig work is basically hiring the employees on temporary basis for which the work required

for the organisation is temporary in nature. The hiring is done on the contractual basis for a pre-determined amount of time.

Some of the examples which we see in daily life may be in Consultancy, Independent Contractors and freelancers in marketing, Hiring a project

based team, Hiring in hospitality (IRCTC ka Staff isn’t employed by IRCTC), Finance and accounting, Education, etc.

The amount of contract per project depends on the → 1. Remote or Hybrid work 2. Duration of the project (See the below Picture)

Understanding Gig economy

What is Gig Economy → in era of fast hiring (2021) to fast firing (2023) the company incurs cost to onboard employees such as signing bonus,

training cost, etc. and for firing giving severance getting Bad PR Etc.

Gig Economy comes to a save by providing contract-based solutions hiring only for temporary pre decided time period

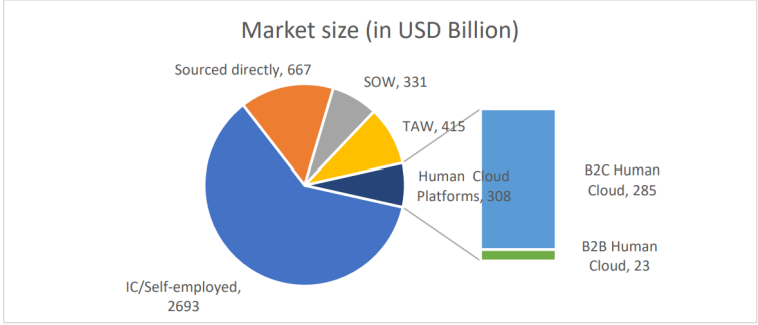

Business Spent almost $4.4 Dollar on contingent labour and only 9% was through platform and majorly was through independent contractors

Now where does the platform come?

So platform enables the independent contractors as well as the company hiring the contractors to meet. It’s like fiverr. This part is termed as

human cloud

Human cloud Is one of the emerging part of the Gig economy. It has 2 Sub-Segments – B2B and B2C

- B2B - let’s say a big company needs help designing a new logo. They can go to a B2B Human Cloud platform and find a graphic design

company or a freelance designer who can create the logo for them. It’s all about businesses helping each other out and getting work done

efficiently. - B2C - let’s say you need someone to help you clean your house or fix your bike. You can go to a B2C Human Cloud platform and find a

cleaning service or a handyman who can help you out. It’s all about regular people finding help with everyday tasks or services they need.

- The company is Into B2B Platform provider

The market for B2B Gig economy is very tiny in comparison to B2C, Reasons for the same are → B2C hiring is mostly for the unskilled work such

as fixing the rough, editing a video but B2B is for very Skilled work required in corporate

If I were to dissect the market for B2B gig Economy in Human Cloud major of the hiring is done through the online platform rather than through

independent contractor (80% Source → RHP), reason is the credibility of the hire

India is the Hub of “Gig – Economy” India’s Gig Sector is expected to expand up to 455 Billion almost 10% of the World market and is expected

to grow at CAGR of 17% - Niti Ayog June 22, 2022.

So Summarizing above → B2C Platform like Fiverr are the one who are facing stiff competition from Individual contractors reasoning → they are less specialised and hence the hiring for the same can be done through offline mode

now for B2B and that too for expert field requirements the hiring is done through platform (80%) i.e. 80 B2B hire is through online out of every 100 hire making platform the king in B2B Space in Gig Economy

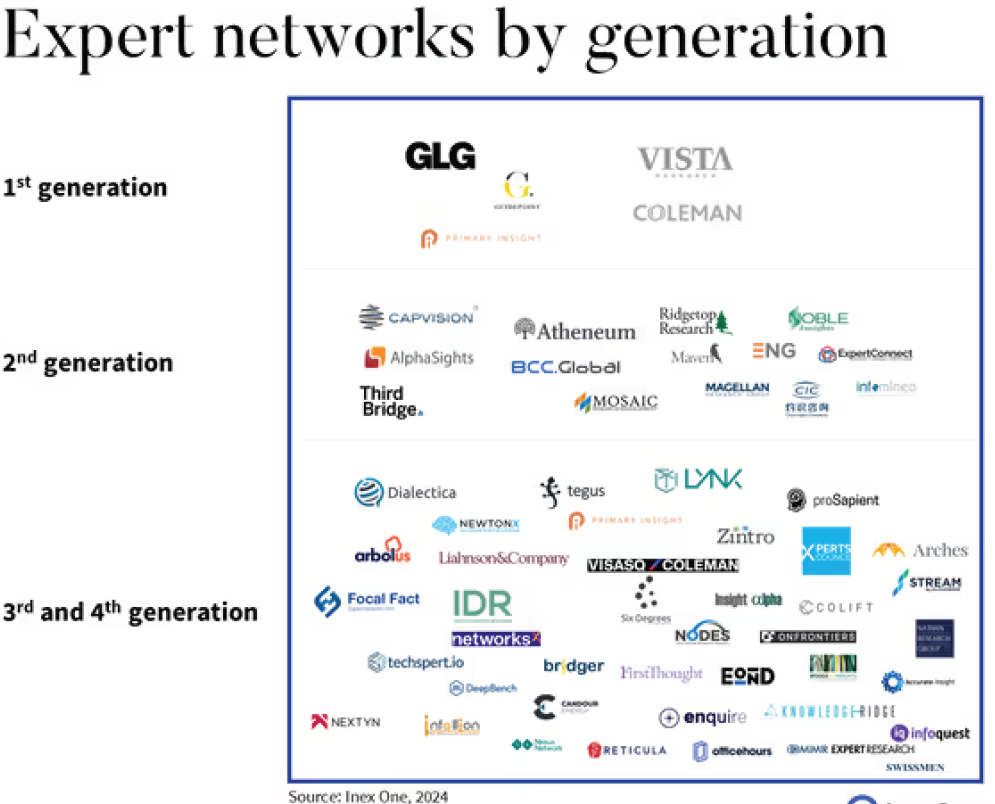

But major of the above is due to IT outsourcing in India, but what makes company interesting is that the company is into Niche space “Expert

Network

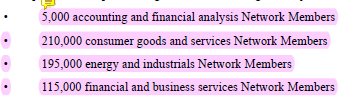

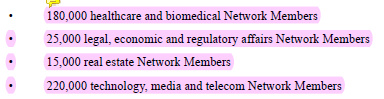

Expert Network industry –

In simple terms, the expert network industry is like a special club where companies can find experts with specific knowledge or skills to help them

with important decisions or projects

Some of the industry using the Expert network are Consultancy in Deal due diligence, Pharma in Specific drug discovery, Investment companies

issuing buy and sale report (Company’s website) etc.

So what does the company do?

The company arranges contractual work arrangements for clients by identifying, screening, vetting, and matching work requirements based on

various parameters such as the nature, duration, objective, location, and pricing.

Just like we have delivery partners for Zomato and swiggy there’s Network partner here which will be getting paid on the basis of the

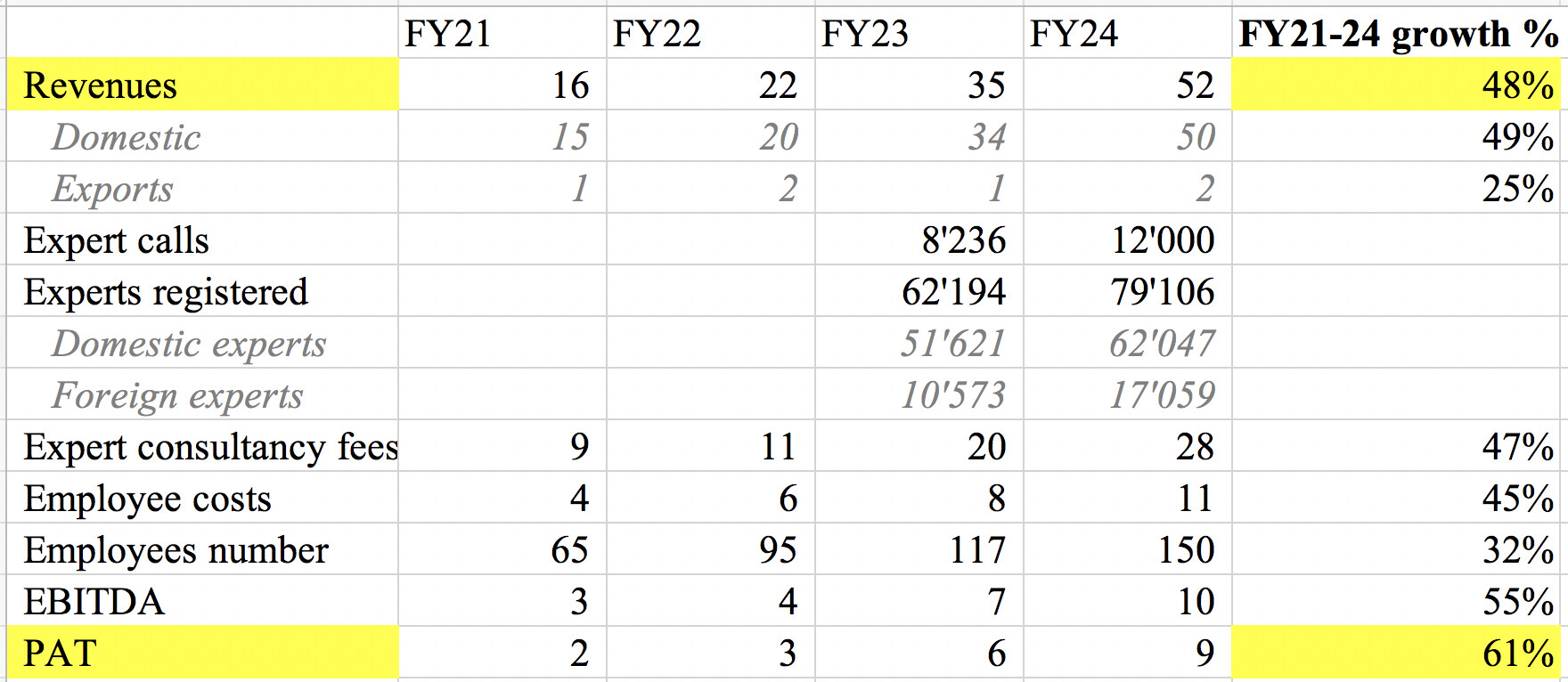

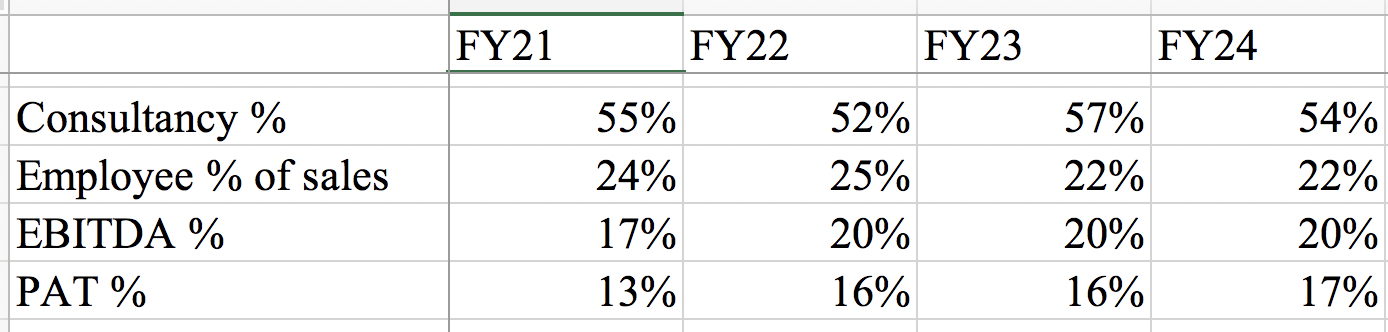

engagement which will be employed by the company the 52% of the revenue is the cost for the network partner considering that the company’s

main asset is human itself. They are paid fixed hourly rate for the engagements. This results in more engagement over the platform for new

requests. Meaning if there’s no work then there will be no payments too.

So this also becomes a risk on other hand → Rajasthan recently classified as the member of platform to be the employee of the company meaning

giving them all the benefits of the employee there are total 57k+ contractors whose cost could become fix for the company out of no where

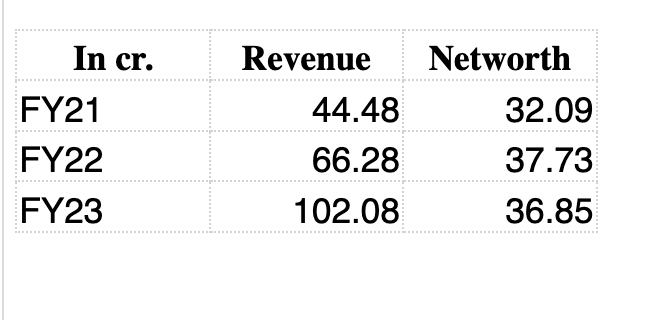

The IPO of the company was for the purpose of Fresh Investment in US Geography and OFS was very minute part of the IPO may be 10%

The established market of US is very tough to crack as they (US and Europe Regions and even India) already has such kind of business there, but if they do the company is sitting on the

huge amount of opportunity this reminds me of the post 2000 IT Outsourcing era and what did the same for Indian IT Companies

Certainly the same is very dreamy statement but that is the power of mega trend too

The company is trading at 24 -25x Annualised earnings

Views are more than welcomed

Not invested, Stuyding

")