What can be the potential risks here apart from equity dilution? Is it possible that they might pump in more money to get into the US market and it could be not the right move?

Damned if you do, and damned if you don’t

That captures the general issue with any business. If all that is measured is the short term monetary outcome of a business success, then management would be caught in the wrong foot pretty much sometime in a life span of 5~10 years (for any company).

I would look out for

- What are their own yardstick against which they would measure themselves.

- How cautious are they to go through the iteration of learn, correct and invest further than going all out - to protect the capital.

So in general, it is process, prudence and common sense which I would generally look out for in any business.

If you check out their presentation, con-call and etc; they do provide some pointers about the same & management thought process on how they would like to go about.

2 Likes

Here are my notes on the company based on VP thread, Concalls, DRHP, Annual reports:

Business

It operates as a tech oriented marketplace within B2B cloud segment specializing in on-demand contingent hiring and work arrangements. They are catering the premium segment of the gig workforce. It’s an asset light business with zero debt, high ROE and ROCE.

It generates revenue by

- Client approaches them for an expert

- They find the right match for the client from their pool of experts

- Expert helps the client

- They pay the expert on a pre agreed rate

- They invoice the client and later on get paid by the client

They have a post paid business model and since they are supposed to pay the experts before the client, it leads to the working capital days.

Range of services

- On demand experts: contributes major revenue

- Knowledge Tours: organizes research tours, meeting key stakeholders, as per the client’s requirement

- Webinars: to keep clients updated on the latest developments in the industry

- Pex-Panel: offering businesses access to temporary talent pools of former CXOs, subject matter experts, top professionals.

- Flexi-staffing: temporary force management to meet flexible work needs.

Main Customers

- Consulting firms

- PE funds

- Hedge Funds

- Corporates

Major revenue from India, expanding in US. Contribution majorly from IT service, BFSI, Healthcare and Life science, CPG and retail, together represent about 60% of

their business.

Competitors

GLG Network, Alpha Sights, Insight Alpha, Guidepoint in B2B human cloud segment.

In flexi-staffing, we compete with staffing platforms like Randstad, Adecco, Teamlease, and QuessCorp.

Vedak is the local competitor who has clients like Bain & Company however they work in the lower cost structure.

Growth Strategies

- Increase US market penetration: Adding more US experts which can connect to Indian client base and then add more clients from US. Established a US subsidiary and built a dedicated team working US hours.

- Expanding into new geographies like South East Asia, Australia, New Zealand, western Europe, etc. Establishing 24/7 operations to facilitate cross-border projects, in these regions

- Huksa Learning & Development: Targeting Indian businesses including family businesses, mid-tier corporations, and top-tier corporations, creating deep domain modules/courses designed to be 90-120 mins sessions with focus on Auto, manufacturing, BFSI, pharma. They are leveraging the pool of experts that they have to venture into long-term projects.

Also, will offer Learning Management Solutions which is based on top of the open source Moodle to standardize and automate their training programs for employees. - Also, looking into peripheral market place including areas like HR, finance, digital and tech. which may lead to lower margins.

- Providing Value Chain Maps as a SaaS offering: A proprietary data visualization platform by Infollion that allows clients to browse and discover experts across various industries. This helps in visual representation of industry value chains, enhanced expert discovery, improved talent management and potential for self service functionality.

Some more points:

- Primary client base consists of consulting firms, particularly the Big 3 (MBB) and tier-2 consulting firms. 70-80% of business comes from the consulting space for them.

- Aim to keep growth margins stable while focusing on volume growth

- Exploring opportunities in the freelance segment (through it’s Huksa service line)

- 90k expert with 6.3k US experts. International experts contribute 27% of the revenue as per H1 FY25. Adding 1000-1500 experts on a monthly basis.

- The market is not price sensitive and they are seeing healthy demand due to rise in gig economy, and a shift from traditional staffing models to marketplace.

- Huksa creates long term business with clients however can lead to margin erosion, Value chain mapping as SaaS can give opportunity of cross selling.

Strengths

- Well established in India, 50% gross margin and EBIDTA of around 20%.

- New product offerings, expanding into new geographies with focus on operational efficiency and technology

Weakness

- Concentration risk, 80% of revenue from top 5 customers.

- Most experts are non exclusive, meaning experts can work with other expert networks or independently.

Opportunities

- Growth of gig economy, expert network industry

- Expansion, operational efficiency, new service offerings

Threats

- Intense competition, economic slowdown which could lead to lower consult spending

- Regulatory changes which could lead to changes in the gig economy. Experts are contractual in nature, with re-classification of contractual class by the government, it could lead to added expenses.

- Data privacy related compliance challenges as it stores private information of clients and experts.

Let me know if something is missing or could be further improved. I’ve taken assistance of AI tools to help me in my analysis

Disclaimer: Studying the business, not invested.

1 Like

Their revenue is approx/mostly = Fee collected from clients - fee paid to the experts

Is this actually a good things, coz the cost arbitrage is not gonna be there, the fixed fee that they pay for the indian experts should be lesser than the American experts, or

is this transient in nature, like until they have enough number of US clients or any other arbitrage clients (i.e: Clients who can pay more compared to what to what they pay for experts) , once there is enough trust on the platform(s) ability to match the experts as per needs, then they slowly introduces the experts who charges less for the same service expected from the client ??

2 Likes

How strong is this business model against LLMs like chatgpt. Can it hurt them in next 5 years?

2 Likes

From my limited knowledge;

My take is bit different here. LLM’s are in-fact good; it would help may be some of the clients and thus weed out so low quality expert-client engagement calls. What would it then lead to is a very high quality client - expert engagement business (which indeed cannot be replaced by LLM’s).

The other way to look at this business - as the product lines (subsequently service lines ) gets more and more complicated for a business, the “support” required to complete product lifecycle gets complicated and thus pushes the need for such cloud human companies such as Infollion.

So in general; complexities of a product and service is more to look out for ; than LLM’s (this is true for all companies in this space - I am not speaking only for this company).

My personal apprehension is from challenges arising from fellow competitors; which is to be seen - how it plays out.

2 Likes

A very interesting question in my opinion.

So from what I can understand:

- Most of these models have a cutoff knowledge. Llama 3.3 has a cutoff knowledge of December 2023. These can not be up to date atleast as far their core knowledge is concerned. While Retrieval-Augmented Generation (RAG) systems can supplement these models with the latest data, they cannot achieve the same level of contextual, nuanced understanding as human expert.

- Experts often bring diverse backgrounds and cultural understanding, making them more suitable for clients with specific cultural or subjective requirements. Also, they provide accurate and real time information of what’s happening in the industry which is tailored to each client’s requirement.

- Experts often leverage proprietary data and insights gathered through methods like scuttlebutt which LLMs cannot access or synthesize as they are typically trained on publicly available data. RAG is one way to improve it but information evolves real time and hence it will remain a challenge.

- Experts consider both material and non-material factors which LLMs may lack the ability to fully grasp or understand.

- I feel like this will become an enabler for them to further improve their client expert matchmaking. AI adoption takes time and mostly it is going to improve efficiency via task automation [Agentic behavior is what the recent research is on].

- Also, I do believe if they go into areas of expertise which have very subjective requirements like HR, etc. which require more nuanced approach of human behavior the risk of what you are thinking can be reduced.

- There’s a brand value which might be associated with a company’s research experts which may not be easily replicated/contested by AI agents. In fact, it is possible that Infollion themselves provide AI as a research tool going forward.

As mentioned above, the lower quality of work will be gone however since these guys are in the premium segment, they shall not see a huge issue. I believe they will have to innovate just like any other IT business to survive and it’s definitely not something they need to worry about in the near future. However, we must be on a lookout for any startups which might leverage something in this direction.

However, lets see how things pan out in 5 years, as the AI industry is evolving exponentially.

2 Likes

Nothing on this is mentioned but from what I can infer:

- The market is price insensitive so I assume they will be able to maintain gross margins in case they onboard more US experts. Also, I believe, the client payment must also be higher for US experts than Indian ones.

- As they build in more regions, they might offer multiple experts with different pricing and might manage margins by having more gross margins for Indian experts vs US experts.

3 Likes

Stock is on lower circuits for last couple of days and on downward trajectory for last 3 weeks. Is it due to upcoming Trump Presidency effect on this company? Interestingly, few fund houses met on 16th Dec and 17th Dec but stock continued downwards thereafter.

1 Like

I agree. In fact, a human expert who has practical experience in that field can provide insights like no LLMs trained on data can. Also, cultural context, insights and nuances pertaining to that industry in that country/region can only be provided by someone who has actually worked there.

In general, I don’t think AI can totally replace “NI” ![]()

2 Likes

Can anyone tell what is the minimum lot size for buying the stock of this company?

Thanks in advance

dr.vikas

400, unless it has got reduced.

1 Like

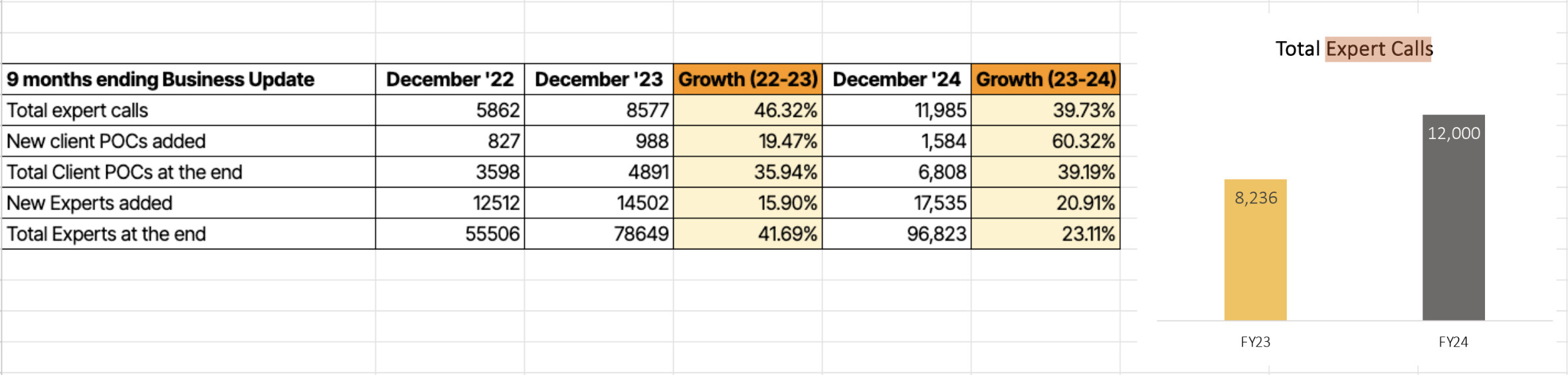

The way I read this is that the first metric - total expert calls - should directly correspond to increase in revenues, while the other two - number of client POCs and experts - would potentially impact future revenues.

Am I reading this right?

1 Like

Yes. Total Expert call looks like the top-line but need to wait for the results to see how much of it is converted to the bottom-line.

Just Tracking. Not invested.

dr.vikas

2 Likes

Good to see additional fund/PMS interest in this micro-cap.

I see Dhyana capital ( About – Dhyana Capital) and Tunga Investments ( About Us - Tunga Investments) with a little over 1% each in the Sep quarter. India Equity Fund is already there with ~ 3.78%.

Discl: Invested

Both equity capital funds hold only one share- Infollion. (Dhyana Capital and Tunga India Long Term Equity fund)

3 Likes

What are your thoughts on the longevity of growth of this business? Till when will the 40%+ growth last? Has the management ever given their 3/5 year vision/ guidance?

1 Like

Presenting a comparative overview of the Business Update for the 9-month period ending in 2023 and 2024.

+FY updates

6 Likes

Hi guys,I recently completed a research report on Infollion. I’d appreciate any feedback you have. Thanks!

Research Report_Infollion Research Services Limited.pdf (2.1 MB)

5 Likes