Infibeam Avenues is India’s first listed Fintech company and it’s leading product is CCAvenue payments gateway. It is amongst the top 5 payment aggregators in India and runs a profitable operation. It’s business is divided into two major parts - Payments and Platforms.

In the platform part of business, it provides E-commerce marketplace solution as well as other solutions. Notable deployment and crowning glory of this business is the Government of India’s E Marketplace more commonly known as GEM platform (https://gem.gov.in/) which is growing at 100% YoY as of Aug 22. Besides this Jio-Mart also uses their platform. Besides the marketplace solution, they have a few other platforms addressing bill payments (based on BBPS), Hotel booking (ResAvenue) etc.

On the payment side, Infibeam is the pioneer in the industry with a lot of industry first in India. Over last few years it has lost in market share to better funded fintech(s), but since 2021 it has started pulling itself back. It has stayed out by and large from the gig-economy and focused on payment segments where credit card / debit card is dominant. Its net take rate (NTR) had plummeted as it started getting aggressive and more competitive. However, over last 2-3 quarters, the NTR has started showing improvement as some of the more lucrative sectors including travel and hospitality return to full working post covid and other reasons.

Both GEM and payment gateway business are clocking heavy duty growth on GMV basis. Margins have not kept pace as gross margins in payment gateway business have halved in FY22 compared to FY21 - thereby cancelling out the margin addition from top line growth. FY23 is likely to see some improvement in the NTR and thereby margins too.

While the business is 90%+ India based, they do have an international presence and want to roll out more aggressively internationally. Please refer to their Annual Report of FY22 to understand the business in depth. They have done a commendable job to try and explain the business and its components in there. There are simply too many components to try and explain here in this note.

Besides the existing business, 2 new areas catch attention :

TapPay - is a soft POS solution, converting any mobile with NFC into a potential POS machine. It acquired this technology from an acquisition (UVIK) and is in process of rolling out. This solution has the promise of addressing the acquiring side of payment business in a cost efficient manner. Company expects a large part of volume growth to come from this in the next couple of years. This solution, if it succeeds in India, can be taken to other Asian countries rapidly.

TrustAvenue (https://trustavenue.com/) - is an intermediation play between bank’s/NBFC’s and loan-seekers (typically targeted to MSME’s). This business is likely to leverage (a) Infibeam’s existing relationships with large Indian Private sector banks for the supply side and (b) it’s merchant base on the payments gateway business and most likely the supplier base on GEM platform also as the demand side. They are in the process of doing integration work with banks.

Overall Infibeam is operating in high growth businesses. The challenge is to keep margins growing at similar rate / higher rate than growth in GMV and competing with VC funded fintech’s which have the capability of disrupting the unit economics and even working at -ve margins. Besides other risks, one key risk is on GEM business. Their contract ends somewhere in mid-2023. Whether it gets renewed (and for how long and at what economics) or will go on tender mode needs to be seen. This is perhaps the biggest risk for Infibeam today and an overhang. There have been mentions of corporate governance issues in the past and that also is an overhang perhaps.

Key to valuation besides addressing the risks above, is how they are able to improve on the margin profile and create some semblance of a moat (entry barrier to payments business is very low). They are in process of preferential issue of capital to fund international growth and investments/acquisitions. Management has started providing guidance at annual level (Q4 investor presentation and Annual Report).

Overall, a high risk, but interesting proposition in a very high growth, highly competitive, dynamic and regulatory heavy industry.

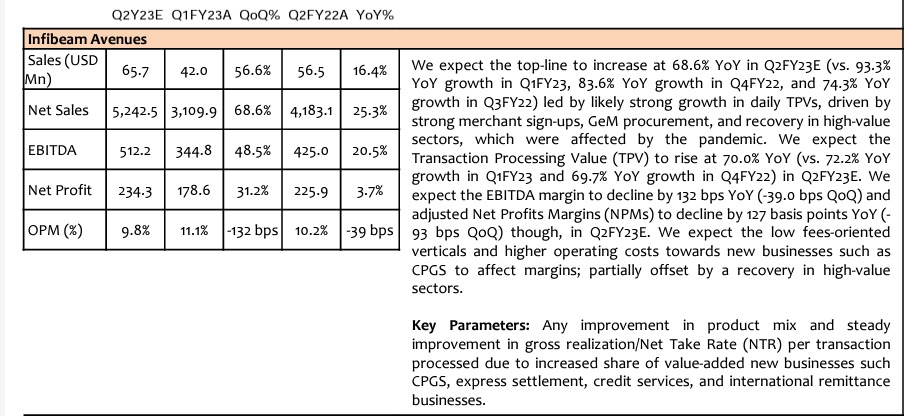

Numbers are wrongly put. What is given as Q1FY23A are actually number of Q2FY22A and vice versa.

Q2FY23E give by them - dont seem to have any basis.

My Estimate for Q2 would be more like a EBITDA of 480mn INR and around 10% qoq topline growth. There is simply no basis to think of a 25% qoq growth in topline.

PAT of Infibeam is always tricky to predict as their allocation for taxes swing widely over the year. However, if we were to assume a normal kind of tax allocation - then PAT should end up in 260mn range.

The license will give more power and legitimacy to grow the acceptance base

Take rate is increasing QoQ - right now it is at 6.9 bps and it will grow from here

Guidance of 100 bn dollars of processing volume across our payment and platforms business

It will keep increasing more and more as we move away from this covid period

Take rates and volumes will go on increasing as we add more and more merchants, as we keep building more and more innovative solutions to go across

License is constraining the players - that anybody can’t just come to the country and start operating without this nod - so this gives us the additional power, the empowerment from the RBI to actually go out and mass deploy in a safe and growth-oriented manner

Float Business - we don’t look at that as an income. We keep it with the RBI. It is an RBI-monitored nodal account. We don’t make money on the float. And that is not a core focus area of the company to make interest out of that. Credit is the major focus now.

I don’t look at the share market. We’re here to perform, to build a large, profitable company - that’s always been the focus of us.

Even I personally am putting in my personal money subscribing into the warrants of the company, because we are positive about the company

Past being the past, right now if you see, for people who understand this business, it is all bank-to-bank-to-bank, the GeM numbers we process is visible on the GeM website, we’ve been doing profitable business since the last 20 years, for me in the CCAvenue Payment gateway space, never had any complaints from any card companies, the growth prospects that we have and what we do is very visible to all the investing audience there.

When looking at Infibeam Promoter shareholding I add shareholding of Vishwas Patel & his relatives to the official promoter shareholding. For whatever reasons Vishwas Patel is not categorized as promoter (possibly because his company was acquired by Infibeam and merged into it and hence they have retained the original promoters as only promoters).

There were rumours doing the rounds that the company had advanced an interest-free loan to a subsidiary, which has negative net assets. In recent times, it also allegedly classified a co-founder as non-promoter.

Annual report of 2016 quotes about this subsidiary as follows:

“Under the business model of e-commerce, the role of payment processor is very crucial in completing the financial transactions after the purchase is made by the customer. Infibeam has taken a strategic step by investing ₹600 million through its fully owned subsidiary NSI Infinium Global Pvt Ltd in leading payment solution provider company CC Avenue, to gain an advantage of incremental revenue by way of deep integration for customers shopping on BuildaBazaar merchant store and also on Infibeam.com. The payment integration is a very critical/equally important for the merchant in expanding his merchandise which on the other hand results into higher sales. CC Avenue is a leading payment processing solution provider for thousands of merchants across business verticals in expanding his merchandise which on the other hand results into higher sales.”

This doesn’t seem material for a 70% fall. Regarding the promoter holding, Mr. Vishwas Patel, who is a founder and has 11.45% holding is still being shown as public shareholder. He is executive director also. Is there any purpose for this shareholding?

There was probably another reason. It’s IPO came at huge valuation and from the listing price it because a 5 bagger during 2017 bull run in 2 years. Afterall it was the first eCom player to get listed. I am not sure, but probably that time it became clear that Infibeam won’t be able to compete with the likes of Flipkart, Amazon & Snapdeal and thus investing more in the adjacencies, and the eCom premium was stripped off.

NTR of India Payments on the rise (7.2 vs 6.9). The bad days of sub 6 NTR are gone. Mangement expects further improvement which should aid margins.

GEM volume growth continues (39,840 vs 36,300 Cr). See further rampup in next 2 quarters to hit 180-200K Cr for the FY.

Tappay launched (no revenue/NTR shared) and active on 15K terminals. To be ramped to 100K by year end (or is it Q3 end?). Management maintain significant volume addition from this over next 2 years (~20% of TPV).

Clearer commentary for international expansion provided. Money raise from preferential warrant allotment and sale of investment would provide necessary support for such growth. Take rates are higher in international markets.

In principal license/approval for payment aggregation is welcome and removes risk from mind for some investors (I never thought it to be a risk though). Conversely, not anything great either as RBI is likely to give such approval to all existing significant players.

Negatives

Sequential India Payment Volume growth is muted not keeping with industry growth (45,364 Cr vs 43,736) - indicates minor market share loss, given higher overall market growth.

Platform revenues and profit not keeping pace with GEM growth, basically indicating some other platform revenues (and margins) are getting lost. Segment profit are flat YOY despite GEM nearly doubling in volume. Entire gains from GEM volumes ceeded, due to loss in other parts of platform. This is continuously impacting bottom line over last 3 quarters.

No commentary on loan intermediation (Trust Avenue). In investor presentation - no news is bad news. Hence, I assume, no further progress worthy of getting mentioned in the presentation or concall has happened during the quarter.

If Onetime profit is excluded - then PBT(and PAT) would be sequentially lower.

Industry wide -ve - UPI has literally eaten away debit card spend (online and POS). YoY debit card spend values have declined !!!. This has taken out a large chunk of revenue accretive business of payment aggregators and replaced it with zero revenue business. This reflects in overall sluggishness of payments growth for Infibeam as well.

Overall a mixed bag. For next couple of quarters, while topline growth will continue at some level, I expect bottomline growth to be muted/-ve, given investments in launching and scaling up Tappay in India and payment business in International markets. Eagerly await some numbers of Tappay in Q3 investor presentation - this is possibly the most exciting thing/value driver at Infibeam right now.

And I think this is just one of the many. A simple google news search should come up with a few adverse news items. If I remember correctly, there was a detailed article some 3-4 years back on the challenges being faced.

I found these incidents of importance while digging for red flags…

There was a spat between the management and auditor when the auditor had asked for an investigation over the firm’s merger with CCAvenue and an investigation over a statement on the same.

The firm sacked the auditor with allegations of sharing price sensitive information.

The auditor said the firm did not maintain proper records of assets.

There was a case of insider trading for which Sebi barred three entities from the capital markets for one year.

Does anyone knows anyone who is using TapPay to receive payments? Has someone seen it in action in real world conditions? This could be a game changer for Infibeam, but what is the reality on ground today?

Meanwhile, GEM apprears marching ahead confidently and seems likely to hit 2LCrore volume in FY23. UPI continues cannabalizing Debit card volumes (and to some extent credit card vol too) leading to degrowth in Debit card and somewhat muted growth in Credit card overall volumes. Unlike some other VC fund led sectors, this sector is not facing fund glut as some of the large competitors are extremely well capitalized and continue to attract funds. Hence, competitive intensity remains high, though clearly the crazy days are over for the time being.