Any views on the open offer?

This open offer at 847/share by Shiva performance materials pvt ltd is believed to be linked to the current leadership team at INEOS. This open offer gives more confidence of underlying strength of the business.

It bodes well for the stock price which can rise further from current levels. Q2FY23 results will be declared on 11-Nov-2022 and are expected to be decent. Over all, stock is available at 4X which is very cheap at current price. Downside is limited with potential for re-rating.

4 Likes

Styrenix ( previous Ineos) declared Rs 80 dividend today on CMP 840

1 Like

Us Indian investors are ready to pay high PE just to get a tag of MNC player in our investments but many incidents such as Ricoh India and INEOS suggest that we must be as diligent with these players as we are with Indian companies. MNCs are no saints.

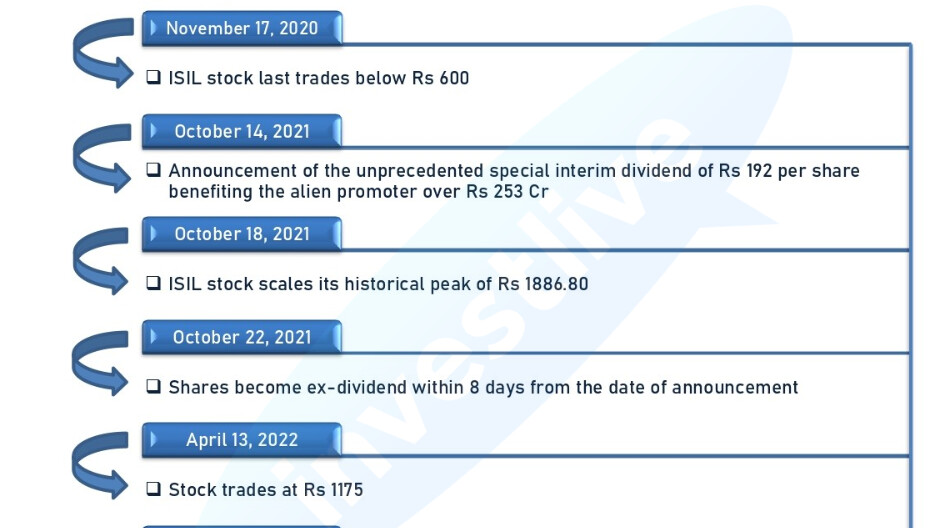

Incidents related to INEOS in last two years are quite interesting.

-

From 2011 to 2018 company never reported a PAT higher than 70cr. In 2019 they report losses. In 2020 also they report loss (which is understandable). But in next two years company reports annual PAT of 280cr and 383cr!

-

Company then suddenly becomes very liberal in their dividend policy and declares huge unprecedented dividends by which the MNC promoter essentially sucks out 253cr and ~111cr in two big dividend payouts.

-

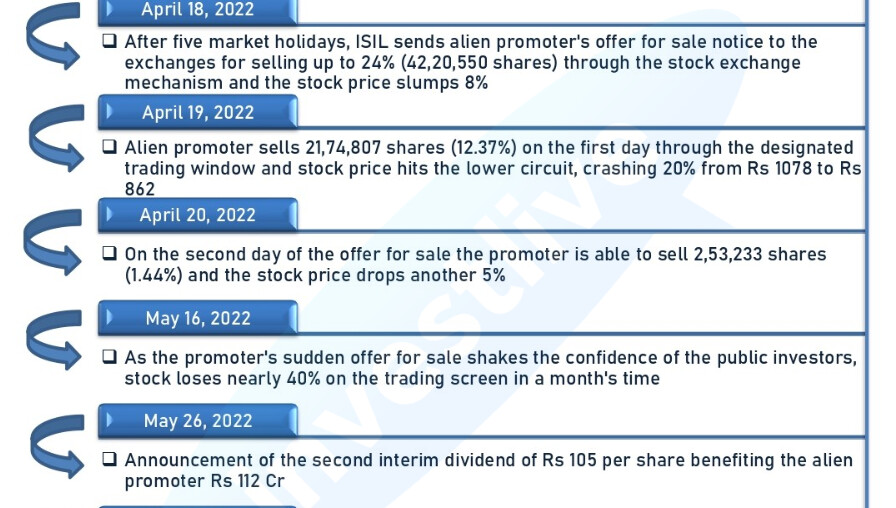

Then delisting drama starts. Company applies for delisting and wants to purchase public shares at throw away price of ~400Rs per share. The share price at the time in exchanges was multiple times that. Obviously, the delisting fails @ discovered price of 1100. Company now offloads 12% shares and stock goes into lower circuit and price corrects significantly.

-

After stock price corrects significantly, Mr. Rakesh Agarwal of Shiva Performance Ltd. comes into the picture and purchases the 61% stake of INEOS at a meager price of ~600Rs per share. An open offer is made for public shares at ~850Rs per share.

Interestingly, this is the guy who founded the company and ran it for years. Since the stock price had corrected significantly, the deal does not look too far away from value but if we connect the dots of events in last two years it appears that all of that was done to be able to do this purchase agreement at a lower price of 600Rs per share.

Essentially, the promoters sucked out a lot of juice through extremely high dividends and then sold the company at cheaper valuation. This is beneficial to both parties from tax perspectives.

It is not clear why INEOS would want to exit India.

Following is the detailed analysis of these events.

These events does not bode well for quality of pervious and new managements.

Positives:

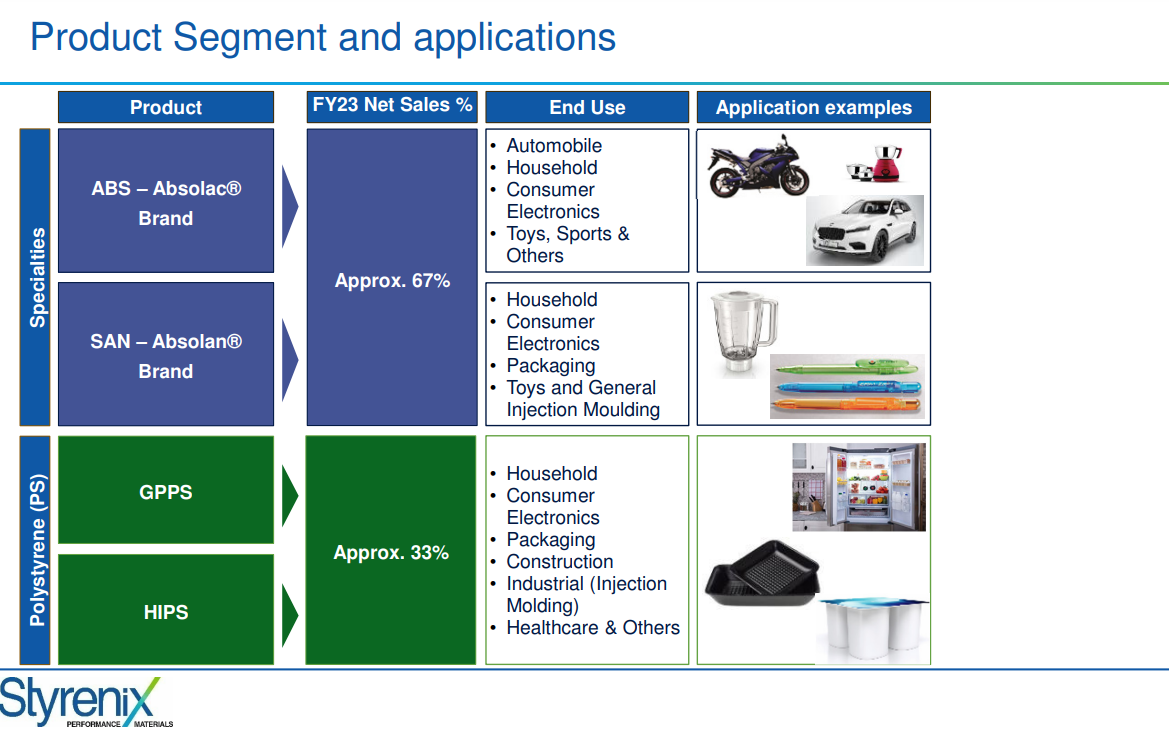

- Company is leading player in ABS and SAN.

- Products of the company finds applications in Automotive, electronics, household, construction, healthcare, packaging many of which are seeing good growth owing to the capex cycle ongoing in India.

- It trades at cheaper multiples compared to peers.

- Although the transaction looks shady, the new management is not new to the business and they know the business and the industry inside out because they essentially founded the business and ran it for years.

- New management acquired 61% stake at 600Rs per share which is about 644cr. If we assume that roughly 350cr that were sucked out through dividends earlier were with silent understanding of new acquirer then essentially they would have paid 650+350 = 1000cr for the business. This is the value at which industry expert, insider entity is ready to buy this business. Current market cap is ~1800cr. Since the company is almost debt free with net current assets of 569cr. We get the price of 1231cr. Which is not too far from 1000cr.

- The industries in which products of Styrenix are used are facing tailwinds in India. At the same time gas which is key raw material has become very expensive in Europe due to Russia-Ukraine conflicts.

I have not looked into the demand-supply situation of ABS, SAN and Styrene yet though which I intend to do next.

7. In the very recent announcement, company is meeting with Lucky Investments of Mr. Ashish Kacholia a celebrated investor. That boosts the confidence a bit.

8. New management, Mr. Rakesh Agarwal is a technocrat who did pioneering work in this industry from 70s. His sons are also well educated from reputed American Universities.

9. Current capacity utilization has enough room for growth so company will not need capex in recent times to grow if the demand improves.

10. INEOS is a global leader in this industry

There are many more questions to be answered such as demand-supply scenario, competitive strengths of the company, product portfolio and its position in the supply chain of various applications etc.

Relevant articles and links:

Disclosure

Invested recently at about 1000 and still evaluating very cautiously

7 Likes

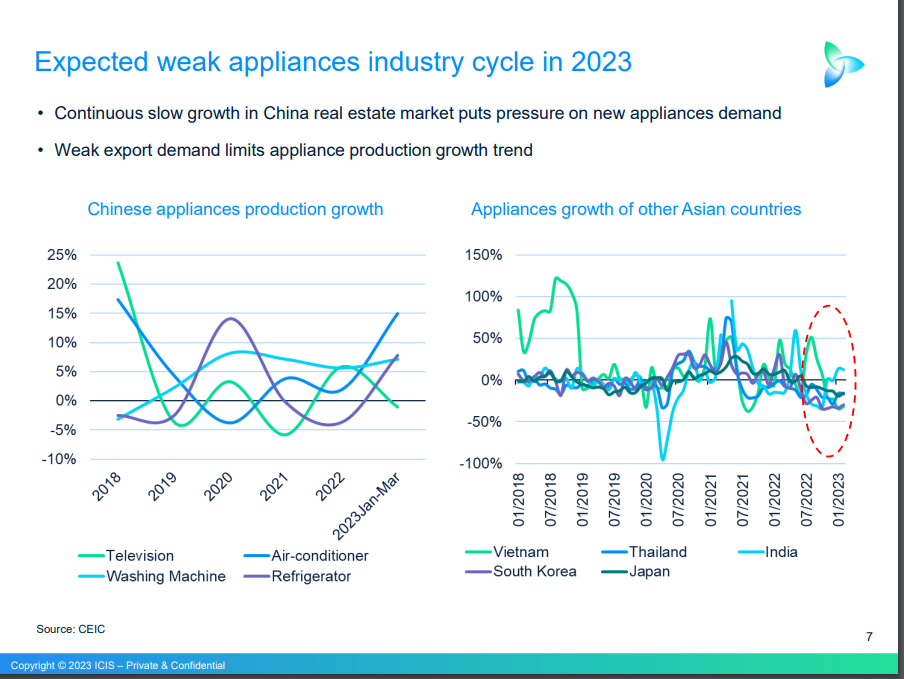

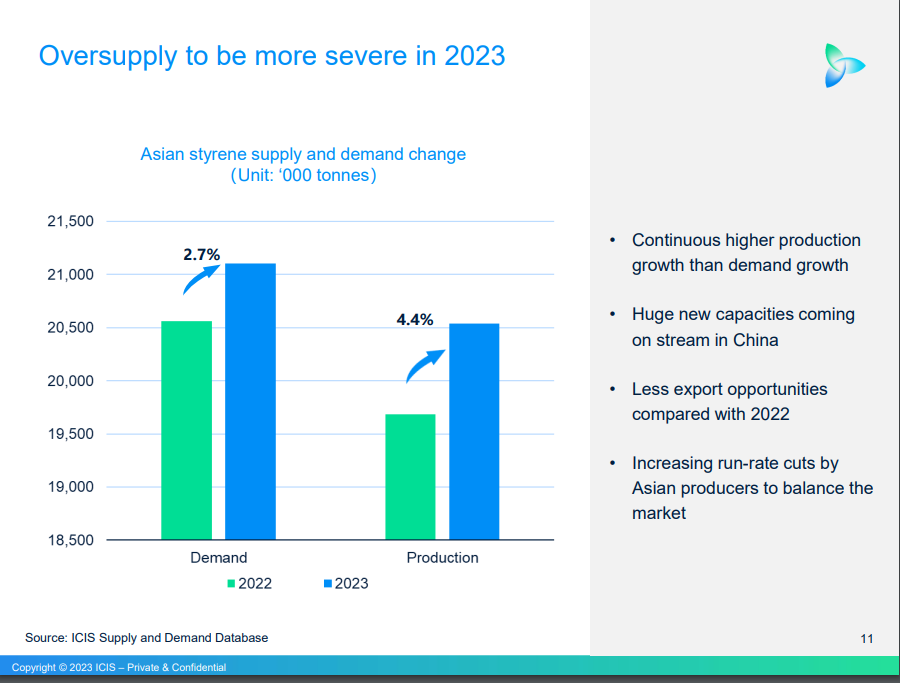

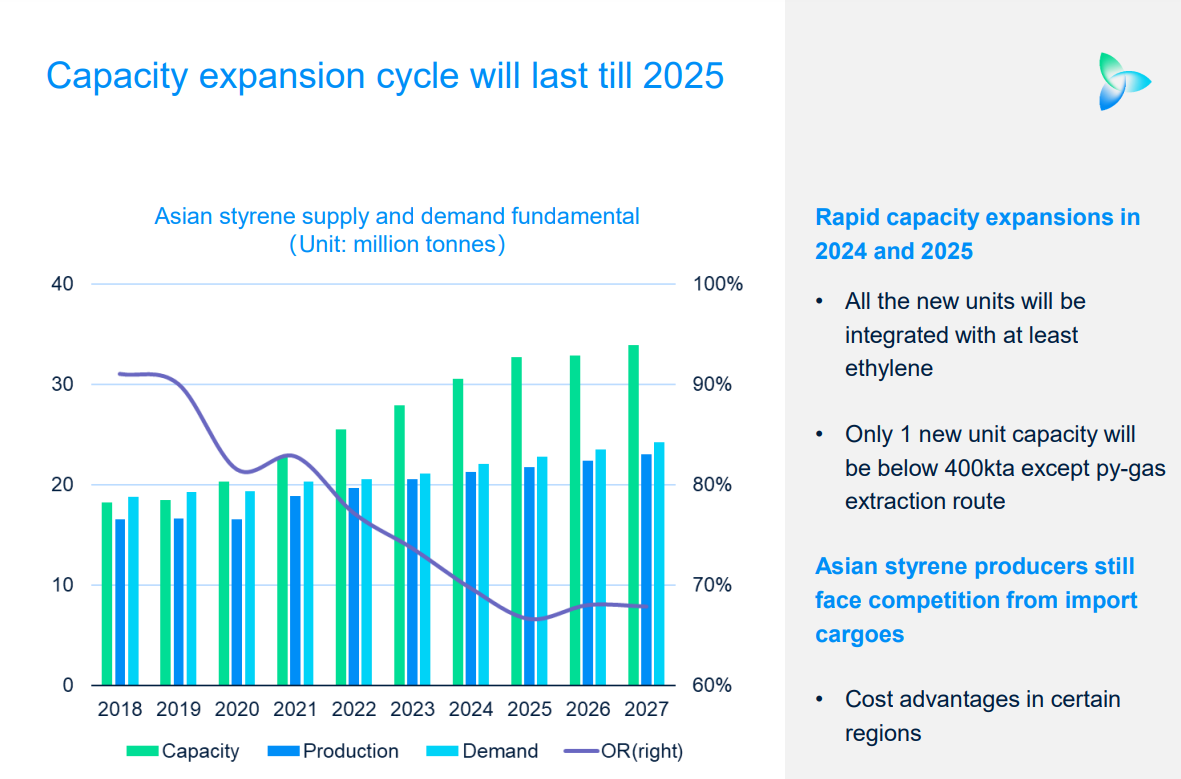

some information on demand and supply.

slowdown in growth in China but not so much in India. Need to see if there’s any Anti Dumping Duty in place for chinese import into India. If not then it may be a red flag.

supply is higher than demand in Asia.

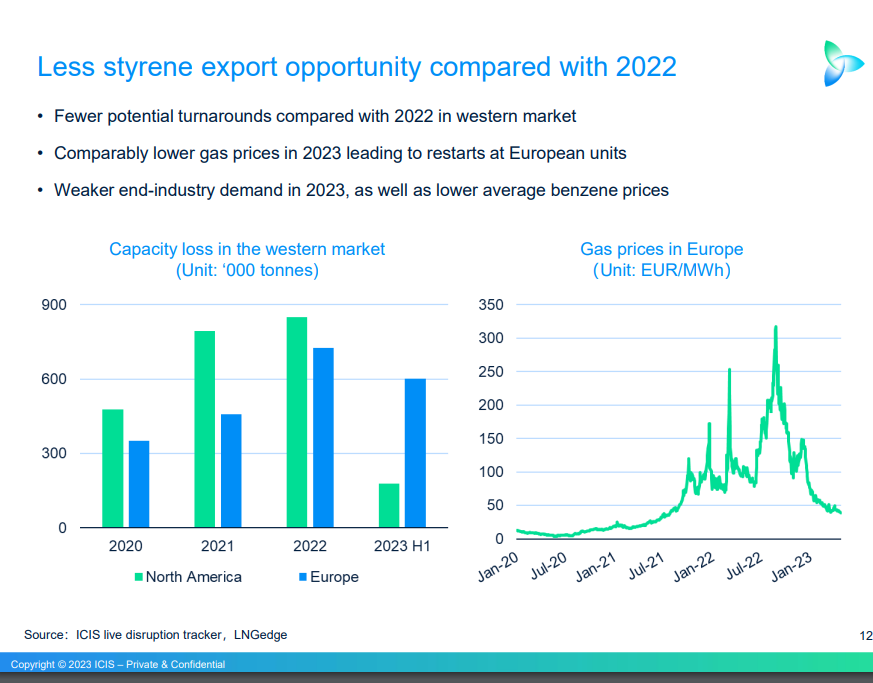

this was something new for me. European Gas prices have actually come down significantly!

1 Like

Styrenix performance materials Limited.( earstwhile ineos styrolution )

CMP 1020, Mcap 1785 cr, Debt:0

This company is mainly into manufacturing of ABS and PS .

In ABS almost 70% is speciality and 30% is commoditty and in PS almost 40% speciality and 60% is commoditty and they are working to increase the specialty part here.

In ABS currently there are two big players in India, Styrenix and Bhansali. Total consumption for the year 22-23 was almost 3 lakh tons and imports were almost 140,000 tons. There is one new player Supreme petrochemical who entering with 140,000 capacity in phased manner 70,000 each and first being commercialized in second half of 2024 calender. The technology with which they will manufacture ABS is mass while the other two players are manufacturing through emulsion process the difference between the two process is that in mass the production is a continuous process where as in emulsion there is batch processing and its combination of SANS with other products to arrive at ABS . Globally ABS is manufactured 90 % through emulsion and 10 percent mass, all imports in India are from emulsion processed ABS.While the end application of both the process might be same in emulsion process there is a possibility of customization which according to styrenix is an edge over the other process.

It seems that the market for ABS shall continue to grow at around 7% per year and so by the time capacities of supreme petro are on stream, requirement would possibly go to 370,000 ton p.a. After the company being taken over by the Indian managers there has been some margin improvement and there seems to be much more scope for improvement. While the management is not providing any guidance it seems that 13 to 14% ebidta margin is achieveable.

The capacity utilization in ABS currently stands at closer to 60 to 65% and in PS it seems that it stands at 80%. Management is guiding that they can easily go to hundred percent and by bottlenecking here and there they can grow more without committing to any CAPEX.

One negative thing which I have gathered is that th management has placed all their shares in pledge for the acquisition and that might be the reason for declaring handsome dividend.One of the analyst on the call did try to get some hint on whether the management will reduce the pledge from the money which they have received through dividend but the management has not committed anything.

Mr Rakesh agarwal was MD of the company untill 2012 and post that the company MNC was not able to grow it and no capacity increase was done in last decade.The company used to be his baby and than there has been change in hands many times in last 20 yrs.I gathered that in the past there was some insider trading case against him, since he was priviy to information of take over….and some trade happened in one of his relative accounts.This is many years back I think before 2005. Open offer to shareholders was at 848.5rs. Management took over operations from November 2022.

Just to add to your work, Mr Pratik.

Disclosure: Invested

10 Likes

Can a moderator change the title of the thread to Styrenix Performance Materials ?

Styrenix’s latest results look good -

The new management is more investor friendly and seems to be more willing and capable in utilizing existing assets. The previous MNC management never gave me good vibes in their earnings call.

The investor call is scheduled for Oct 23rd.

Link to last quarter’s earnings call transcript -

Link to updated presentation -

1 Like