Indigrid is looking to acquire 1 more asset from Sterlite for Rs 1,020 crore. The name is East North Interconnection Company Ltd Transmission Company Limited (ENICL). It has two 400 KV transmission lines with a total roughly 900 circuit km across Assam, Bihar and West Bengal This will increase Indigrid’s AUM by 10% to roughly 12k Cr. This acquisition is subject to unitholder approval (mere formality) and the EGM has been called on 24th Feb.

This acquisition will be funded by internal accruals, proceeds from the preference issue done in May 2019 and new debt - Harsh Shah, CEO

If anyone attended the Q3 concall can you answer these question?:

Any idea as to how much additional debt will be taken up to fund this acquisition?

Did the management specify whether DPU would increase in the near future due to:

No mention of increase in DPU on the call. If no acquisitions, current DPU should be maintained for 10 odd years, it was mentioned. Don’t think there was any specific question on reduction in corporate tax.

@fabregas, @sumi00

Could you please help with your thoughts on impact of lockdown/covid disruption on indigrid’s earnings and it’s ability to distribute (interest, capital).

Thanks

Disc. Invested in indigrid invit since more than a year.

The shutdown due to COVID will only marginally affect Indigrid earnings if at all according to the company. See below extract from the latest investor presentation:

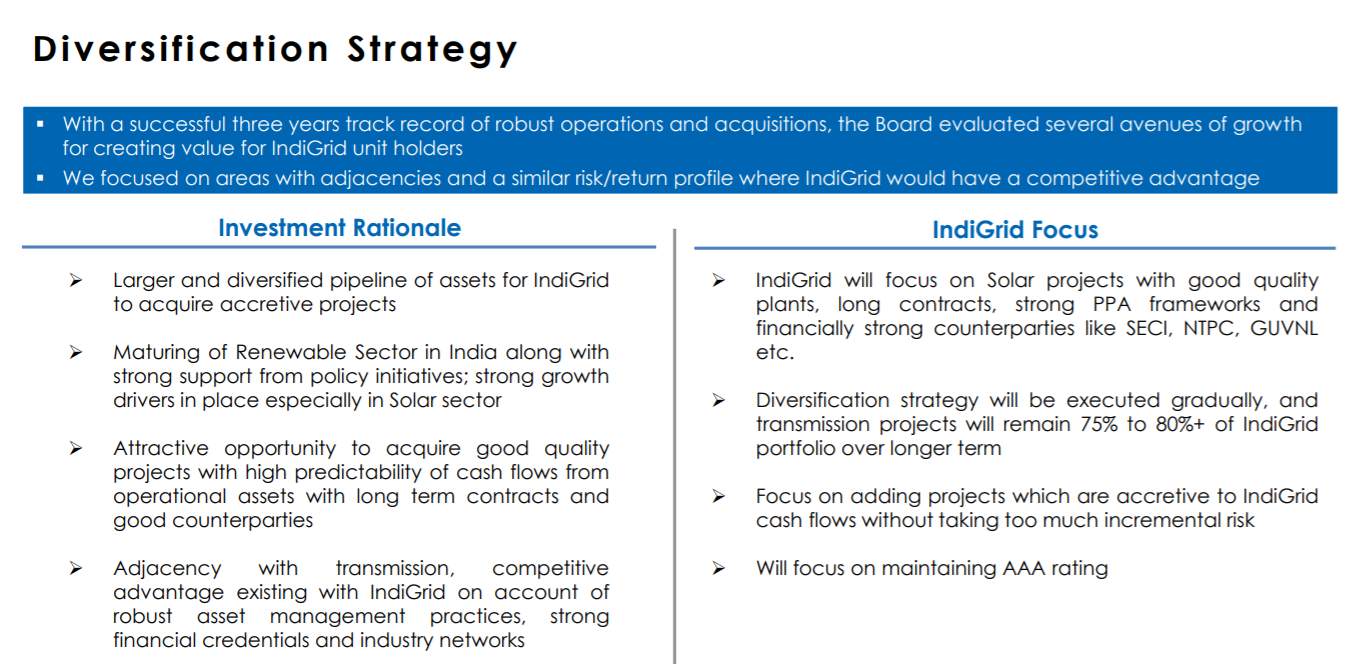

What is more troubling is their decision to diversify into Solar power yield assets now. They want to bring down the share of transmission assets down to 75-80% over time. Not sure of the rationale to expand into solar projects, where availability based revenue wont exist and counterparties will necessarily be weaker than through the pooled collection mechanism for interstate transmission projects.

Not a bad strategy if executed well since many Solar assets are having costs comparable or lower than thermal power. Grid storage sector is also getting viable now so there could be good biz viability over the longer term. I agree this will bring volatility in cash flows but I would hardly care at this price if yield varies between 10-14% over the longer term as long as cash flows remain intact. Many solar assets are indeed going cheap due to liquidity squeeze etc. It is not without reason that investors were falling over each other to get slice of Adani Green not long ago which had been aggregating these stranded assets.

The distribution % of 11-12% for Indigrid’s assets makes sense given that that the cash flows are annuity in nature and the underlying assets are ‘AAA’. Renewables sector is going through a tough phase with errant discoms delaying dues and asking for tariff reductions. If Indigird wants its investors to take on renewables risk, then investors need to get at least 14-15% return, lower returns would not work. There is a high risk of NPAs in power generation as compared to transmission and investors should get higher return for taking this risk. Unit-holders should oppose this sudden change in Indigrid’s investment philosophy till the management gives more clarity on this.

I was on recent conference call conducted by the managment. They give update on business which is generally business as usual and they do not see any destruption in their operations. However, most of investors were concerned about their intention to acquire renewal assets. The management did clarify that it is enabling resolution and they would ensure that all essantials are in place before they acquire any assets. However, given the kind of experience with State which are not even honouring commitment signed on dotted lines, it would be more of wishful thinking in my limited understanding. I have personally voted against the resolution which change constitution of trust to enable acquisition in renewal energy as I see personally negative and need pure transmission business. As an investor, I have option to invest in renewal energy (if I wish) through various other modes (including equity of some listed players). For me, IndiGrid is more part of debt allocation than hybrid. In case I find this resolution is approved and management initiatiate action to acquire renewal assets, my hypothesis for investment in IndiGrid undergo complete change. Hence, I may exit from investment subject to valuation and other market opporutnity. While management did gave ensurance of no point of time more than 25-30% exposure would be to renewal, I fail to understand why they shall be considering business which is not core?

Disclosure: My view may be biased and my understanding is limited on the sector. I have investment in IndiGrid. Investor shall do his/her own due diligence/ consult financial advisor before making any decision. I am not SEBI registered financial advisor.

Thanks. I wonder if the venture into solar energy is as bad as we consider it to be.

From my limited understanding, renewable energy projects sponsored through SECI (Solar Energy Corp of India) come with a 25 year PPA with SECI at a fixed tariff, where SECI procures power from the renewable energy players and then sells it to state governments. In this manner, payment to the renewable energy players is made by SECI irrespective of whether state govt owned utilities pay up or not. My cursory look at SECI annual report for FY19 revealed a very healthy balance sheet (debt free + cash rich) with low outstanding receivables. I believe that a similar arrangement is also applicable for projects sponsored by NTPC. Would be good if any of you can explain this in greater detail

cc: @fabregas@sumi00

India Grid Trust, an infrastructure investment trust backed by private equity fund KKR & Co. and Singapore’s GIC Pte, is looking to add as much as 60 billion rupees ($786 million) of solar power projects to its portfolio and expects some financially stressed assets to become available in the wake of the coronavirus pandemic.

The move is part of the firm’s plan to more than double its portfolio to 300 billion rupees over the next two years, with solar accounting for as much as one-fifth, Chief Executive Officer Harsh Shah said in a telephone interview.

“We see that there will be consolidation in the solar industry,” Shah said. “It’s a good time for both sellers and buyers to complete the transactions.”

IndiGrid, as the company is known, is seeking solar assets with government-backed counterparties, such as NTPC Ltd. and Solar Energy Corp. of India Ltd., bearing the payment risk, Shah said.

Distressed asset sales in the renewable energy space has gathered pace. KKR is buying 317 MW of solar assets in MH & TN from Shapoorji Pallonji group for 1554 Cr. This works out to approx 4.9 Cr per MW. Not sure if these assets are under a PPA with SECI/NTPC or with the state electricity boards. Interesting to see KKR buying these solar assets themselves rather than routing them through IndiGrid.

Renewable assets (with SECI / NTPC) as counter-party are not fully insulated from payment risks as contractually, SECI / NTPC only act as intermediaries. They cannot pay unless the back-to-back offtakers (in this case, state discoms) pay them. Further, Tamil Nadu is one such discom which had average outstandings of more than 2 years. I wonder if Indigrid would have the capability to deal with such discoms. Don’t see why Indigrid should to dilute its asset quality (which is currently ‘AAA rated’), just for seeking growth.

I believe any change in investment strategy requires special majority by non-interested shareholders, this has now been put up for e-voting. Unit-holders have an opportunity to voice their views against this change.

Q4FY20 Results released by Indigrid. Here is the presentation. DPU of Rs 3 in the form of interest.

Other Development:

Signed definitive agreement for the acquisition of Jhajjar KT Transco Private Limited (“JKTPL”) for ~INR 310 Cr from Kalpataru Power Transmission Limited (“KPTL”) and Techno Electric & Engineering Company Limited (“TEECL”). Will add Rs 15 Crore to NDCF per year (approx. 25 paise per unit). Press Release.

If anyone attended the recent concall, please post your findings.

They refrained from giving any DPU guidance for FY21 but gave enough hints that it would be higher than 12/unit. May be we might get clarity by the end of Q1 when all working capital related issues are resolved by then. I think more upside to the DPU will come from refinancing at lower rates or more acquisitions at higher IRR.

I was shocked to see foreign holding of 55% in IndiGrid. More than 50% of quarterly distribution will flow out of the country while domestic guys will struggle to generate 6-7%.This was a great asset from the word go despite some hiccups regarding the promoter. It gave ample opportunity to add even after entry of KKR. I also added after KKR entry. It is more shocking to find small holding by insurance companies who have long duration funds.

This has done really well and might be reaching a fair value sooner than later. Management has started selling which they acquired in the 85-90 range. If they raise DPU this quarter, more upside is clearly visible. I don’t know if folks will start justifying even 125+ levels given the state of yield scenario in India.

Two implications for sure… the price run up has kind of ensured that old agreements become untenable. I don’t think anyone estimated the speed of decline in interest rates. Or there could be serious disagreements the way they are looking at acquiring assets. This is clearly sentiment negative when a PE is not going to be sponsor but they do hold majority stake along with GIC. Now it is very clear that KKR can sell its stake which will hurt sentiment whether they actually sell is a different matter. Selling by Deutche bank had caused it to fall to low 80s. It will be an opportunity to add in case any deep correction happens this time. There are not many opportunities to make 12% pre tax from a AAA asset.

Please split India Grid into investment manager and shareholders. KKR controls 75% of first entity, so they are the fund manager. Yes negative that either of Sterlite or KKR did not honour shareholders agreement or could not enter into a new agreement or it is possible it is win-win new arrangement. Enough and more demand for invit by debt mutual funds.