Insightful analysis. I highlighted the cash flow difference in FCFF for a comparable period for 2020 onwards. Nevertheless, the FCFF cash flow difference is less than 1% of total FCFF cash flows across all projects, so I agree that this is not a significant point.

I think this SPV has to choose a starting date for the 10 consecutive years. Maybe the management has decided not to use this option right now.

Possible but very unlikely because the COD date for BDTCL was in 2014. They would have to choose a period starting 2019, latest. I will get clarity on this in the next concall.

1 Like

Yes, that would be great!

In any case MAT is payable if there is book profit even during the tax holiday period. At best the MAT credit can be carried forward and adjusted in future years when they are out of the tax holiday.

1 Like

I just went through the section 80IA of Income Tax Act, on the Income Tax Department website - Insertion of new section 80-IA.

After going through this section, my understanding is that the SPVs are allowed a deduction of 30% of their profits. So the balance 70% of the profits will be taxed. It is not a 100% tax holiday.

However on another website - India Filings - Section 80IA Deduction it says:

Deduction Amount

100% profits form the first 5 assessment years is permitted as a deduction and 30% for the next 5 assessment years for a total of 15 years from the year of its commencement.

1 Like

This is with reference irbinvit…nothing to do with indigrid.

As rightly pointed out by @narenarora this article is related to IRB InvIT. Also the article is dated MAY 29 , 2017. At that time there may have been many unanswered questions. You can refer to this topic for discussion on IRB InvIT:

Good update

3 Likes

Indigrid has informed exchanges that Sterlite Power Grid Ventured Limited (the sponsor) has pledged 100% of its holding (15% of total units) towards a loan taken from L&T Financial Services.

The pledge happened on 25th September, whereas the trust informed it to the exchanges on 11th October. The delay reflects poorly on Indigrid’s disclosures and corporate governance. To be honest, I did not expect it to be better, given that the parent is Sterlite.

NSE-11102019-19.pdf (686.4 KB)

According to the previous conference call KKR was supposed to buy out this 15%. Looks like there are some road blocks in this - maybe SEBI approval has not come through yet? Or maybe Sterlite and KKR have developed differences over the valuation? I am just speculating. I really don’t understand why Sterlite had to create this pledge when they agreed to sell it to KKR.

1 Like

Power Grid looking to launch its own InvIT by March 2020.

The filing says that the aggregate value of the pledged units is Rs 750 crores. This comes to Rs 85.7 per unit. KKR investment happened at Rs 83.89. Not a very big difference. So it does not seem like Sterlite and KKR have differences over valuation.

I am curious - what happens if Sterlite defaults on this loan? The trustee will liquidate the pledged shares. The sponsor holding would go down to zero. However as per SEBI InvIT guidelines, the sponsor needs to maintain a minimum of 15% holding.

1 Like

In my limited understanding, it would depend on structure of transaction, specifically about who has right on distrubtion of cashflow. In case of pledge of shares, generally, owner (pledgor) has right to receive dividend. However, typical dividend yield is around 1-3% for most of listed shares and hence not very material.

In this case, since the distribution is around Rs 12 per unit (vis current price of Rs 93). So, current cash distribution yield is around 13%. Since Vedanta Group credit rating is AA (by Crisil https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Vedanta_Limited_July_02_2018_RR.html), the likely borrowing cost in INR terms would be in range of 9.5-11% p.a. in my opinion. Given the moderately certain cashflow of Rs 12 as distrubution (net of TDS also around 11), with Post tax cost of borrowing at around 7.12-8.25 %(Post tax shield of around 25% of income tax), in case the lender maintain right on distrubtion on cashflow (or have strcuture where distribution is escrowed in Bank account for servicing of interest on loan), I see very limited chance of pledge being invoked. This is my understanding and I am not expert of subject. Hence, what I wrote may be completely different from reality. Reader shall read this message with clear understanding of that fact.

Discloure: My view may be biased due to my investment holding in IndiGrid InvIT. Not a SEBI registered Financial advisor. Investor shall do his/her own due diligence before making any investment decision.

7 Likes

One more point I would like to add, loans such as the one taken by Sterlite Group would be at 2x security cover (loan should be around Rs.375 Cr.) and the cash flow cover due to difference in interest rate and InvIT distribution would be 2.25 to 2.5x. (loan at sub 11% interest rate and distribution yield of 13%)

But SEBI should clarify about sponsor pledging there shares when as per rules they are suppose to maintain a minimum % of shareholding (isn’t it indirectly breaching the rules) and can L&T Financial Services in event of default sell these shares in market as Sterlite is suppose to maintain minimum shareholding (won’t that be running contrary to SEBI guidelines).

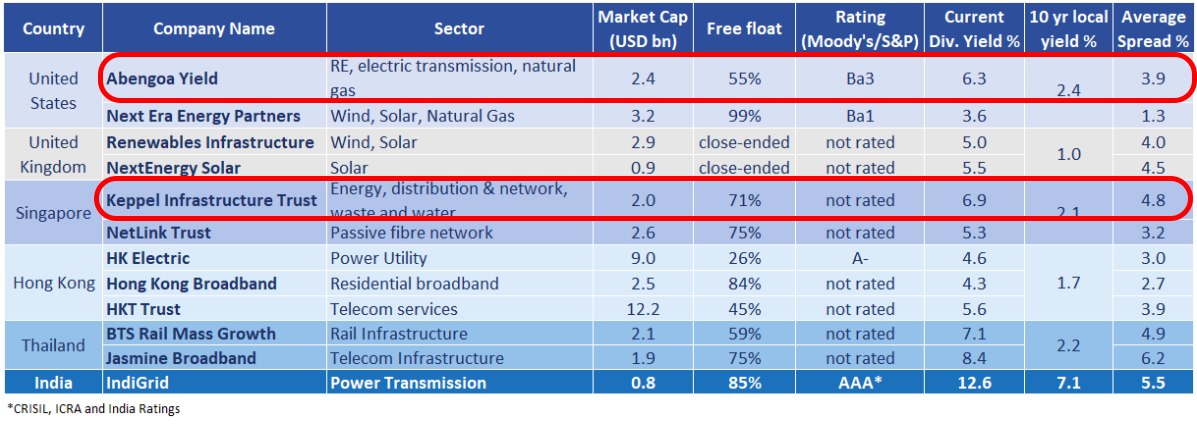

Today I decided to look at a few foreign InvITs in the energy infrastructure space, to see how they have fared over the last 10 years or so. I chose 2 of them, both mentioned in Indigrid’s quarterly presentations (refer to the slides titled ‘Overview of yield platforms across geographies’). My objective was to look at the history of InvIT products in more mature markets and figure out things that can go wrong.

Coincidentally, in both cases, I found things that had gone wrong.

1. Abengoa Yield (Now known as Atlantic Yield)

- Listed as Abengoa Yield, sponsor was Spanish conglomerate Abengoa SA

- The sponsor held about 41% in the InvIT

- It owns more than 1,400 MW of renewable energy assets, about 300 MW of conventional power and nearly 1,100 miles of electricity lines.

- Listed in 2014, at around $40 per unit. The price collapsed to $13 in early 2016. Currently trades at about $25 per unit.

- Its sponsor, Abengoa SA, went through financial turbulence in 2015-16, that pushed it to the brink of bankruptcy. After years of expansion, the group had built up an €8.9bn debt load, which it was no longer able to service. Source: Financial Times

- Name was changed to Atlantic Yield Plc to distant itself from the troubled sponsor. Source: S&P Global

- There seem to have been concerns that cash flows from the InvIT would be used to support the sponsor, which apparently led to the price collapse (to $13/unit in Feb 2016)

- The sponsor eventually went through a round of debt restructuring and survived to tell the tale. In 2018, the sponsor sold down all its stake in the InvIT to a Canadian power utility at $20.9 per unit. Source: Renewables Now

Distribution History

Per unit per year

2019 - $1.57

2018 - $1.33

2017 - $1.04

2016 - $0.45

2015 - $1.43

Source: Company website dividends

It is not clear (or rather I did not bother to dig more) what led to the drop in dividends in 2016. It does coincide with the financial troubles at the sponsor. This shows that it is possible that the unit price or distribution of the InvIT won’t be insulated from the troubles at its sponsor, even if it does not have a direct impact on its assets and operations.

2. Keppel Infrastructure Trust

- Singapore based. Has an older track record, since 2007.

- Owns and operates infrastructure assets in energy, distribution & network, and waste & water management. As at 31 December 2018, KIT has S$ 3.8 billion in assets under management (AUM).

- Listed at about 90 cents per unit and now trades at about 53 cents.

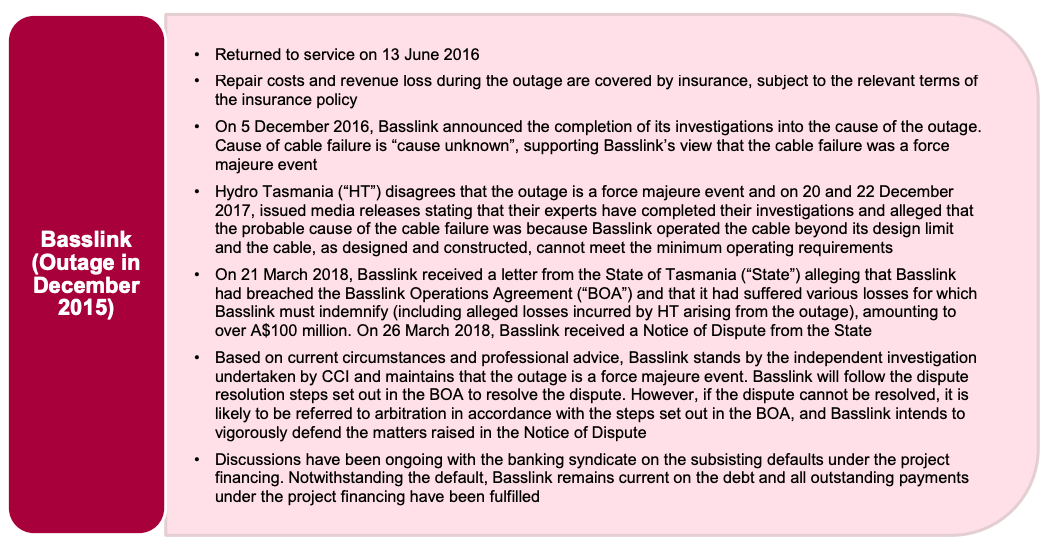

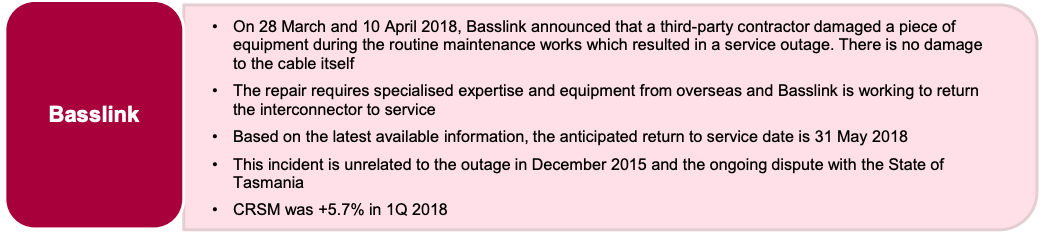

Its subsidiary Basslink, owns and operates an undersea electricity cable. The cable connects electricity grids of Victoria and Tasmania in Australia. It faced 2 outages - one is 2015-16 for about 6 months and one in 2018 for about 2 months.

-

2015 outage

Basslink is in dispute with both the state of Tasmania and Hydro Tasmania over a six-month outage of the cable in 2015. Tasmania last year claimed some A$100 million (S$ 92.6 million) over the cable failure. The clients refused to accept this as a force majeure event (unforeseeable) and did not make payments to Basslink for the duration of the outage.

-

2018 Outage

-

Hydro Tasmania had in October 2019 restricted Basslink from operating at full capacity except during critical periods.

-

Basslink had a term loan of S$ 700 million, due for refinancing in November 2019. The CEO said that they were confident of refinancing this loan (Source: 8 things I learned from the 2019 Keppel Infrastructure Trust AGM).

-

It got a 1 year extension for the repayment (Source: this article)

Distribution History

Per unit per year

2019 - 3.72 cents

2018 - 3.72 cents

2017 - 3.72 cents

2016 - 2.8 cents

2015 - 6.5 cents (had some special distributions)

2014 - 3.28 cents

2013 - 3.28 cents

2012 - 3.28 cents

2011 - 3.74

2010 - 4.2 cents

2009 - 5.6 cents

2008 - 6.85 cents

2007 - 4.7 cents

Source: Company website dividends

This shows that things can go wrong in complicated assets. If not found to be “force majeure” event, the cashflows could suffer.

13 Likes

yes, these are equity like instruments sold with promise of Debt like return, it’s actually worst of both the worlds.

5 Likes

There are many factors which could impact underlying asset when earnings are not stable enough. Specifically any European utility is also impacted by Carbon credits etc which has been swinging wildly so I don’t think you are comparing rightly with IndiGrid trust. In fact most of these trusts are not strictly comparable. I think apart from natural disasters the only risk here is govt. not honoring its side of commitment like what happened in Andra P recently.

@AmitContrarian these are debt securities but trade like equity only because these instruments have good liquidity in the market. Anybody investing here assuming it to be equity instrument will get schooled in due course.

My purpose was not to compare, but just figure out how these have fared over the last 10 years. Co-incidentally in both cases there were things which had gone wrong. This led me

to think about things that can go wrong with Indigrid.

Example

It is not too difficult to imagine that such an incident could happen with Indigrid. Construction & maintenance of transmission lines is sometimes carried out using precision helicopters. Just like in the image below.

If an accident happens due to a pilot error (eg. helicopter crashes into the transmission line or tower), then that would not be considered as a “force majeure” event i.e.

Here is the definition of ‘Force Majeure’

Force majeure refers to a clause that is included in contracts to remove liability for natural and unavoidable catastrophes that interrupt the expected course of events and restrict participants from fulfilling obligations.

An accident due to pilot error would be considered an avoidable human error. In that case, cash flows would suffer for the duration of the outage.

My purpose is not to discourage you from owning or buying into Indigrid. Indigrid forms >5% of my portfolio. My only intention is to remind myself and others, that this is not as safe an investment as we consider it to be.

I think damages due to natural disasters are covered by insurance. This year, due to the storm in Orissa/WB a transmission tower was damaged, resulting in an outage. However, Indigrid’s MD mentioned that their revenue would not be affected because this would be considered as a “force majeure” event. Insurance company would compensate for the repair and revenues would come as if no outage happened.

@sumi00 Can you elaborate on what happened in Andhra recently? I am not aware of the issue.

1 Like

I think at a certain price, investment in InvITs would make sense. Right now I think Indigrid’s unit price factors in all the positives. It is fairly valued, with no margin of safety. I say that because an accident caused due to human error, as I pointed out in my earlier post, could affect cashflows.

Disclosure: Indigrid forms > 5% of my portfolio. No transactions in the last 2 months.

2 Likes

Andhra Govt has been reneging on infra contracts and power purchase agreements signed by the previous government. Since there is no second customer, it would be forced to accept any terms given by the govt. diktat. Court cases etc have hardly been useful in this country.

2 Likes