Why talk about Non Performing Assets (NPAs)?

I have been wanting to write a post on this problem for a long time now. I am not an investor in any of the banks affected by the NPA crisis or banking frauds. However I do know that if one big bank fails, there could be contagion and this would affect all sectors of the economy. This means even if you don’t own stocks of anyone of the problematic banks, you could see an erosion in your investment value. As an investor I am worried about this ![]() I am not sure how serious the problem is

I am not sure how serious the problem is ![]() Every quarter I read about NPAs rising and the management saying “the worst is behind us.”

Every quarter I read about NPAs rising and the management saying “the worst is behind us.”

Quantum of the problem

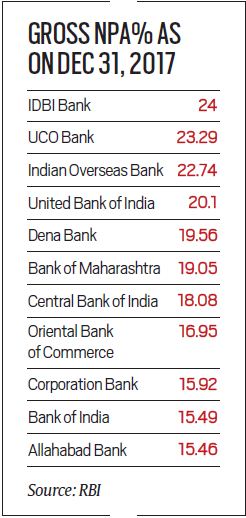

At the end of December 2017, the gross NPAs for all banks were at Rs 8.4 lakh crore. The highest amount of gross NPAs was for country’s largest lender SBI at Rs 2 lakh crore. Among others, Punjab National Bank (PNB) was at Rs 55k crore; IDBI Bank - Rs 45k crore; Bank of India - Rs 43k crore; Bank of Baroda - Rs 42k crore; Union Bank of India - Rs 38k crore; Canara Bank - Rs 38k crore and ICICI Bank - Rs 34k crore.

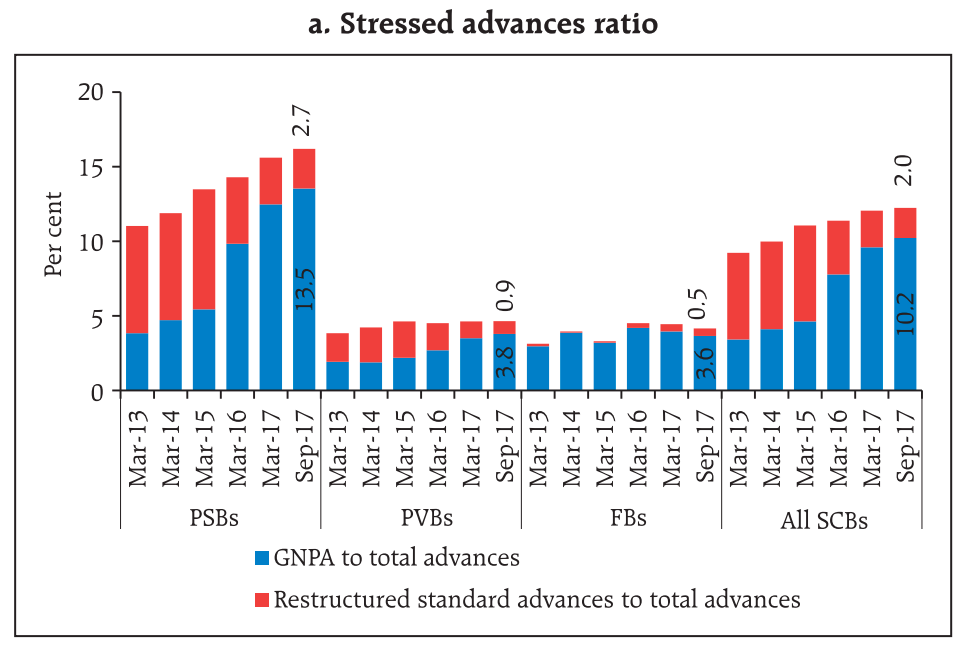

The Financial Stability Report, 2017, released by the RBI, states that India’s gross NPAs stands at 10.2% at the end of Sep 2017. The report says the GNPA ratio may increase to 10.8 per cent by March 2018 and further to 11.1 per cent by September 2018.

PSBs have a huge problem

So far, PSU banks wrote off loans worth Rs 2.42 lakh cr in 3 years. Gross NPA levels have reached 13.5% at the end of September 2017 and show no signs of going down.

Source: The Financial Stability Report, December 2017, RBI

PSBs: Public Sector Banks, PVBs: Private Sector Banks, FBs: Foreign Banks, SCBs: Scheduled Commercial Banks

Prompt Corrective Action

RBI’s Prompt Corrective Action (PCA) framework, which restricts lending activities of the banks. At present, 11 weak PSBs out of the 21 State-owned banks are under the PCA, which kicks in when banks breach regulatory norms on issues such as minimum capital, amount of non-performing assets and return on assets. The RBI enforces these guidelines to ensure banks do not go bust and follow prompt measures to put their house in order.

Government sources also confirmed that at least three-four more banks are expected to be brought under the PCA framework because of deteriorating performance.

Source: Indian Express

In a report in March 2018, rating agency ICRA said that five more banks could be brought under the PCA. These include Canara Bank, Union Bank, Andhra Bank, Punjab National Bank, and Punjab & Sind Bank.

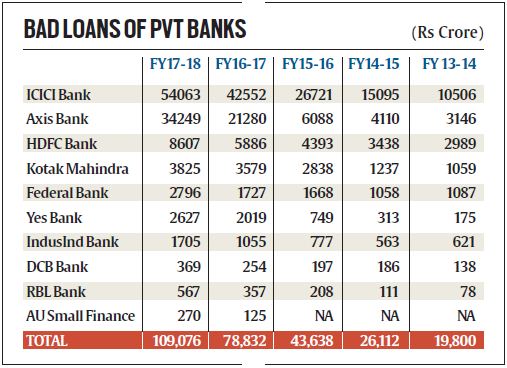

Private banks facing the heat as well

It seems like even private banks are not un-affected by the problem - 21st May 2018: Private banks record 450 per cent jump in NPAs, ICICI Bank tops the list.

Silver lining?

Insolvency and Bankruptcy Code (IBC)

Insolvency and Bankruptcy Code, 2016 was enacted, which provides for timebound resolution of stressed assets. Banks are now banking on insolvency proceedings for a substantial recovery in toxic assets. With some of the high-profile cases entering the final stage of resolution and loan slippages coming down, bankers are hopeful that the NPA situation will get better in the coming months.

NCLT clears Tata Steel’s ₹32,500-crore resolution plan for Bhushan Steel

Bhushan Steel resolution could be more of an exception than the norm’

Change in RBI guidelines

The spike in Mar 2018 NPAs has more to do with RBI’s guidelines change. On February 12, 2018, the RBI withdrew all existing restructuring mechanisms such as Corporate Debt Restructuring and Strategic Debt Restructuring (SDR) and said that if a borrower company defaults even by a day, lenders must consider it a defaulter and start working on a resolution plan. Until then, bad loans were classified as such only after 90 days of default. The central bank also said the company’s failure to come up with a resolution plan in 180 days would lead to the account being referred for insolvency proceedings. Both the government and the bankers had opposed the new framework.

Although this has increased the NPA %, there is no actual cash outflow. Its just accelerated recognition of NPAs. Which also means there will be acceleration in provisions and/or recovery process. Which means the problems will be recognised sooner and solutions will be implemented faster.

SBI reported a mammoth net loss of Rs 7,718cr in Q4 March 2018 due to these change in guidelines. Apparently the worst is behind it. For FY18, SBI’s slippages were less than the previous year, which means the balance sheet is healing. More on this - What SBI Q4 results say about the Indian economy and the bank

The purpose of this post is to instigate a discussion in this community on the topic of NPAs.

1. Do you think this pain will continue?

2. What are the risks of contagion?

3. Will we see a big PSB go bankrupt?

4. Do the balance sheets have enough strength to absorb the bad loans?

5. How will other industries and banks/NBFCs be affected if one of the PSBs goes down?