The obejctive of this thread to understand what would drive valuation of cases referred to NCLT/IBC in the listed place.

I am enclosing my presentation about primer to this subject which can be find on enclosed thread

Further to this presenation and also discussion with certain friends, find enclosed my understanding on the subject.NCLT Cases Valuation Jan 2018.pptx (68.0 KB)

Please note that there are simplication of assumptions in order to explain the situation. Two major assumption from my side, that under SEBI guideline last six months market capitalisation of the company share be mimnium maintained under the restructuring and also at least 25% stakeholder shall remain with Bankers/Minority shareholder so that the company may be listed.

The new preseantaion about propsective approach for valuation of listed company now available. I was writing the thread and it was saved draft when you seen visited previously. My apology.

@dd1474 It will be great help if you could explain your presentation using some example. For example

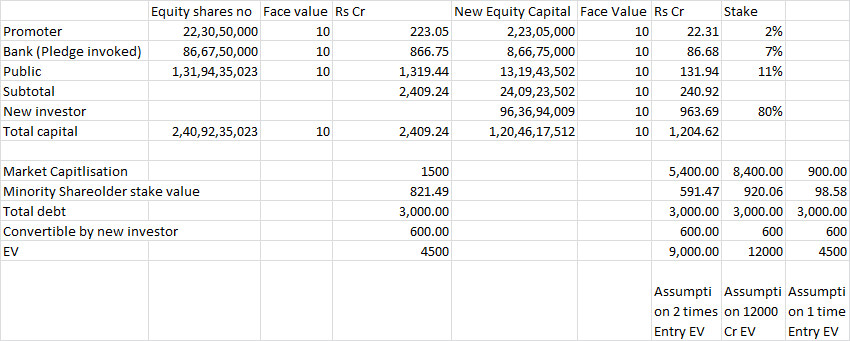

Today Electrosteel Steel is in news, Vedanta has submitted a bid of 4500 crore. The total debt is 13,000 crore including 3000 cr interest on debt. Company has capacity of 2.5 MT. Rough estimate is cost of setting-up 1 MT plant via ballast furnace cost approx $1b = 6500 crores. Therefore apporx cost of asset could be 16,250 crore.

How do you imagine IBC process for Electrosteel Steel will work out?

Thanks for your revert. First part if the value of assets of worth Rs 16250 Cr then why the company in insolvency? The company with able management would definintely get 16250 Cr EV but as per current managment, it is debt of Rs 10,000 cr as on March 31, 2017+ 1450 Cr latest Market cap, giving total value of Rs 11450.

Now if we look at Vedanata bid for the case, it is around Rs 4500 Cr

I am Assuming last 6 months market capitalisation is around 1000 Cr (share price of Rs 2, market cap Rs 500 Cr in June 2017 reached Rs 6 in December 2017, market cap Rs 1500 Cr) and 55% stake of public Shareholder. I also assume that Vedanta offer of Rs 4500 Cr is final and accepted by COC and NCLT.

Now, we need to break link EV and Marker cap as same are interdepedent to arrive at some capital structure. Let us assume again that nearly 400 Cr are infused as Equity be Vednata (after equity write down by say 90%) and balance 600 Cr as OCD in the company. Vednata would offer lenders around Rs 3500 for settlement of 10,000 Cr principal (Rs 13000 Cr total due including interest). So lender took hair cut of Rs 6500 CR of principal and Rs 9500 on Total exposure. In order to sweet the deal for lenders, Vedanata may ask lender to enforce pledge of promoter stake of 45% stake. Subsequently, may write down equity by 90% (my assumption and only ratioanle being past BIFR restructuring where generally such equity writedown were approved).

So revised market cap decline to 100. With Vedanata Equity infusion at 400 Cr, total market cap would be around Rs 500 Cr (of which 80% is Vedanta, It may give some more stake to lenders against debt waiver to make non-Vedanta Stake to 25%).

I know there are limitation, as Enterprise value, Market Capitlisation and Stake of various class equity shareholders are interlinked and moving. We also do not know what kind of new investment/working capital may require to restart of plan.

However, if this assumption is correct, and market capitilsation shall be around 1500 Cr, then existing sharheolder would get Rs 100Cr-900 Cr market cap as against current market capitalisation of around Rs 825 Cr. So the adjusted post restructuring, subject to my “BIG” assumptions, shall range in decline of 88%. to gain of 12%.

Thanks for quick reply @dd1474. What I have understood is

Whether company holds any value of minority investors present or future depends on the terms/condition of Resolution plan and its acceptance by NCLT.

We need to evaluate each company once resolution plan is known and accepted by NCLT and then only we would be able to know if the company is value trap of value investment.

Original promoter will most likely go to Honble Supreme Court after NCLT process and that will add more time in resolution.

Agree on First 2 points. See low probability of point 3 in view of Clarity emerg from Innoventive Industries and Essar Steel cases.

However, even though lower proabble even, it is a probable outcome.

Thanks for provoking my thought process of Electrosteel. While replying your questions, I got many of my queries answered !!!

Do you agree with the valuation of assets of the company?

FY18 Company may do revenue of approx 3000 crore. Do we have a comparable company in same/similar product which can give estimation of asset value of company?

Also as you mentioned

Why do you think present management could not sell out the assets and repay the loan instead of going into IBC?

It is open market and all propsective bidder would have jumped had there been substantial discount on value at 4500 Cr. Since there are no prospective buyer at >4500 Cr, I do believe that being price for assets as is where is basis. If Vednata improve on working and market change perception about company, that would be different perspective.

Further, if value would be say even 6,000; why would lender sell assets at lower price? While IBC provide limited time, Electsteel has already undergone SDR 18 months back and lenders attempted to sell the assets for 18 months which did not resulted in any success.

Hope this answer your queries.

so dhiraj, if there’s a 90% writedown on equity value of the company, the no. of shares held by minority shareholders also dip by 90% and therefore, if one had 100 shares he would hold 10 shares only, right?

Yes, It may be reduction in face value to Rs 1 or reduction in number of shares. also I assume equity writedown of 90%. It may not even be there in some case.

I assume, equity will be diluted not destroyed. So, current market cap is 1500, and Vedanta brings in say 4500 equity, the equity value may be diluted by 75%. That means the debt free residue entity will have assets worth 16000+ crore. What happens to market cap, 6000 crore?

The shareholder value created here is nothing but the amount of loan haircut accepted by the lenders… I am Just thinking intuitively and independently… Lets see how things pan out in the next few months… Fear of value traps is too common among value pickers here…

This would be very optimistic assumption, particularly, if lenders are taking haircut. But for SEBI regulation, in such scenarion, equity value would nil. This is completely against priority in liquidation, where lenders take hit and equity investor are proected in my opinion.

Also Vednata is not brining 4500 Cr as equity. It is giving EV of Rs 4500 cr for total company. Significant portion would be utilised to settle the debt.

Lenders need not accept the 4500 cr plan. They can wait for the 13500 cr resolution plan.

Equity is getting diluted. Shareholders are indeed impacted, the more the lenders are ready to forego, the better the chances for shareholders. I think, That’s why Electrosteel is on continuous upper circuits.

And it is precisely why, the Govt put a rule to disallow the same promoters to bid for the assets again… So that they can’t buy back their pledged assets at a much cheaper price, having been unable to pay off their loans…

If 4500 cr includes 3000 cr to write off the debt and 1500 cr as fresh equity infusion, then with current market cap of 1500 cr, equity dilution should be only 50%. A much better scenario for minority shareholders…

If banks retain a portion of the pledged shares, they will make big money in return for taking the hair cut on the loan…

Please read the first presentation. After entering into NCLT under insolvency, all stakeholders have only 180+90 (with approval of NCLT) total 270 days to approve a resolution plan. In case resolution plan is not approved within the stipulated period, the comapny automatically moves in liquidation. Value realisation on liquidation would not even in double digit cents for lenders and nil for equity holders in almost 99% of cases in my opinion.