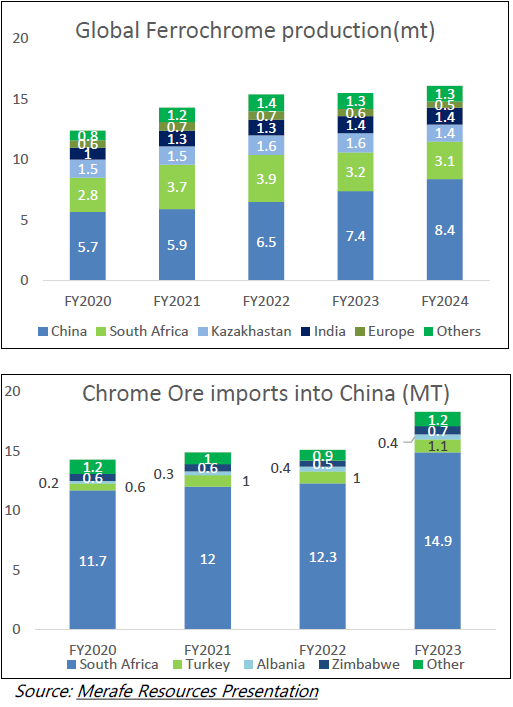

Global FeCr supply cuts: South Africa accounts for ~20% of global FeCr production. Three players account for the majority of the supply: Samancor (1.5 MT), Glencore, and the Glencore-Merafe JV (1.5 MT). Over the last two months, Glencore has shut down all of its furnaces and ceased production of FeCr (earlier 8 lac MT and now 7 lac MT). This reduces ~10% of the global supply for FeCr! Such supply cuts mark the bottom of a commodity realisation as these capacities are relatively efficient because of captive chrome ore.

IMFA could be a direct beneficiary of an increase in FeCr realisation, as it is completely backwards integrated in Chrome ore and Electricity, the two most important costs for manufacturing FeCr. The ongoing greenfield capex of 1 Lac MT will provide 40% volume growth. Its balance-sheet has transformed from INR 700 Cr net debt to INR 800 Cr net cash over the last four years, which would help in funding the expansion from internal accruals. It currently trades at 10 year median EV/EBITDA valuations of ~5x and cashflow yield of 15%.

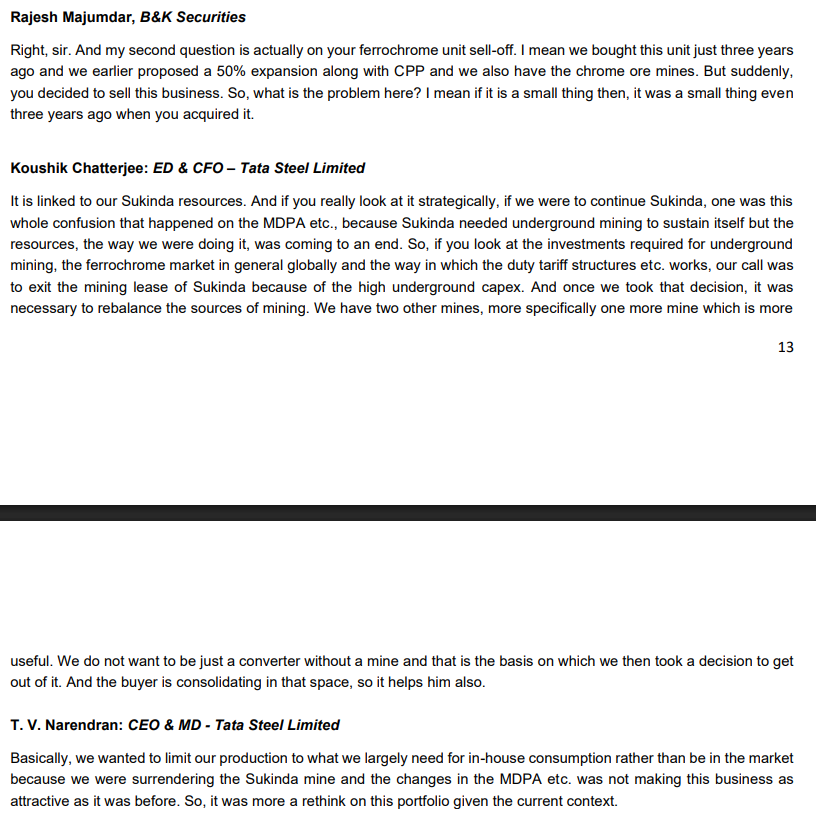

Followed by the shutdowns mentioned earlier in the thread, ferrochrome realizations have now reached at the yearly high levels. Given that the RM costs have not increased in this timeframe, next few quarters should see significant better profitability.

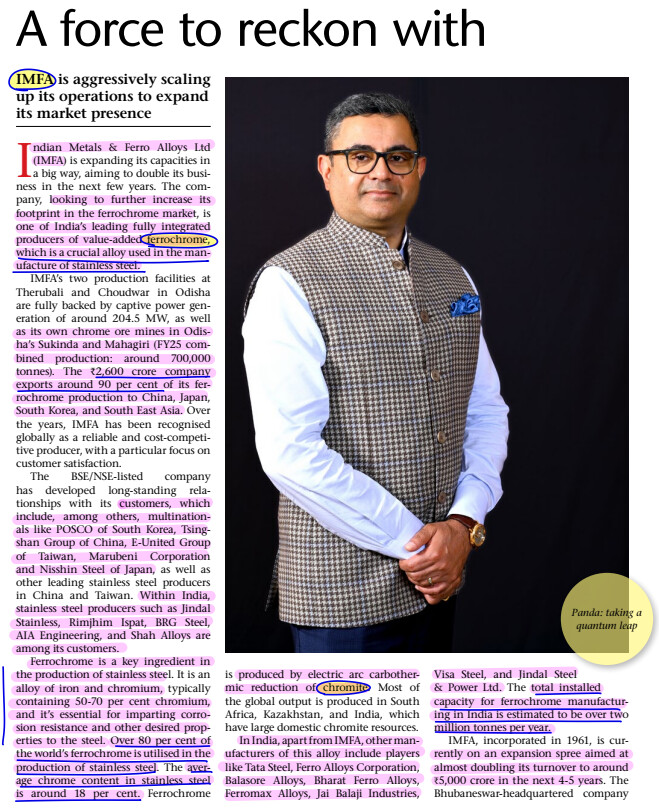

If this gets imposed, South African ore prices will move upwards, which will further elevate the cost of RM for China- the largest manufacturer of FeCr as they import 80% of their RM- ore, from South Africa.

This in turn will increase the Ferro chrome prices for the industry due to this cost push.

IMFA gets benefitted as its FeCr prices are globally derived while its RM is procured captively- so leads to further margin increase.

IMFA completes acquisition of long awaited Tata furnace. Post this, their sales volume will be doubled to 0.5 Million MT over the next two years! Management targeting 4L MT volume next year itself- volume growth of ~50%. With the current spreads, the inorganic capacities payback is <2 years!

Company looks to be at a very interesting juncture. Back of the hand very rough calculations at 4 Lakh tons volume in FY27 and 4.75-4.8 Lakh tons volume in FY28 at an EBITDA per tonne range of 20k-22k brings out an EBITDA of 950-1050 Crores in FY28 if the Ferro Chrome prices stay stable. Any uptick in the global ferrochrome prices as the situations is turning out to be, can be a cherry on top.

A very interesting indication to the acquisition was them suddenly raising the inventory few quarters ago to record high and now they’ve clarified that the chrome ore requirements will also be captively catered. The Ethanol project wasn’t a very interesting part to me personally but overall things seem to be working out quite well with favorable demand supply scenarios globally.

Interesting insights from Tata Steel Q2 Concall- explains why IMFA is at a structural advantage to even the larger companies because of its captive chrome ore mine under the old regime. Also revalidates the higher CAPEX IMFA has budgeted for going underground.

Management has tweeted about the current situation:

South African Ferro Chrome Situation - Interesting article to go through- Samancor and Merafe could get better negotiated terms for Electricity and Ferrochrome output can face some revival in SA.

But, secondary effect could be potentially higher Chrome Ore costs to the largest Ferrochrome Producer- China if that happens which could increase their FerroChrome production prices. If things go this way- South African smelters may increase the production with Chinese Ferrochrome production taking a cost hit. Also, Mr Panda rightly mentions that it’s not a sustainable way to produce Ferrochrome- You can only give preferential electricity costs for so long.

The focus to revive Ferrochrome Smelters is obvious for South Africa given Ferrochrome is a five-times multiplier of raw chrome ore (https://x.com/fyiitsdeepak/status/1963866910157844482) value but South Africa is increasingly switching to the exportation of much lower valued raw chrome ore, which provides its global ferrochrome competitors with increasingly greater opportunity to benefit from the fivefold value-add that it is pivoting away from.

Link to the management tweet: https://x.com/subhrakantpanda/status/2008756835394920935

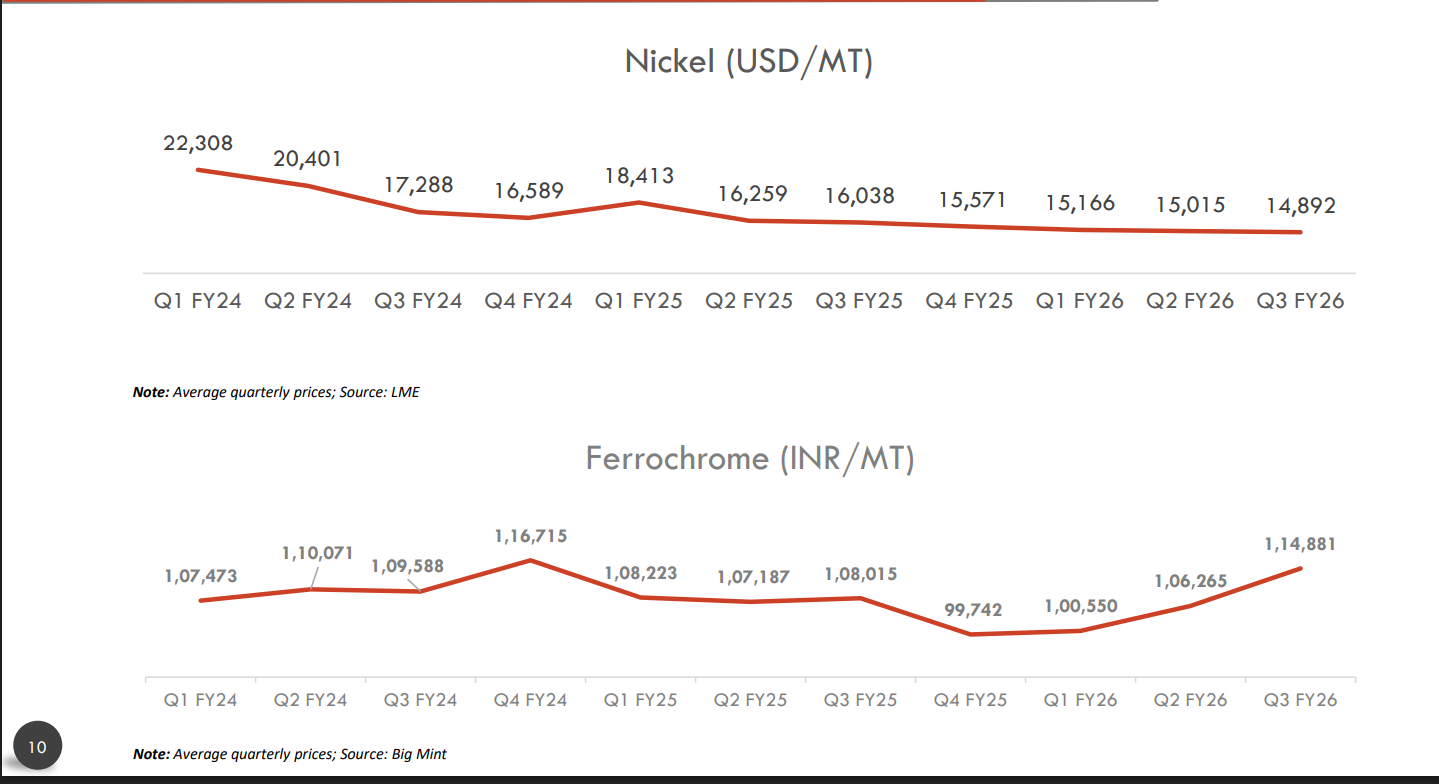

Ferrochrome maintained its upward trajectory till December (Source: Jindal Stainless Q3FY26 investor deck). January has been especially volatile for most metals. Any one has access to Jan’26 trend?

Still the trend is up even in Jan 26:

Below are some notes from AI 2026 predictions:

Ferrochrome Price Trends in India

The market outlook for ferrochrome in India throughout 2026 remains cautiously optimistic, primarily driven by domestic infrastructure development and consistent export demand to markets like China and South Korea.

-

High Carbon Ferrochrome: Prices for HCFeCr typically range from 68,000 to 120,000 INR/metric ton (or 100 to 138 INR/kg) depending on purity and location (e.g., ex-works Jajpur/Bhubaneswar).

-

Low Carbon Ferrochrome: LCFeCr commands premium pricing, generally between 160 to 275 INR/kilogram.

-

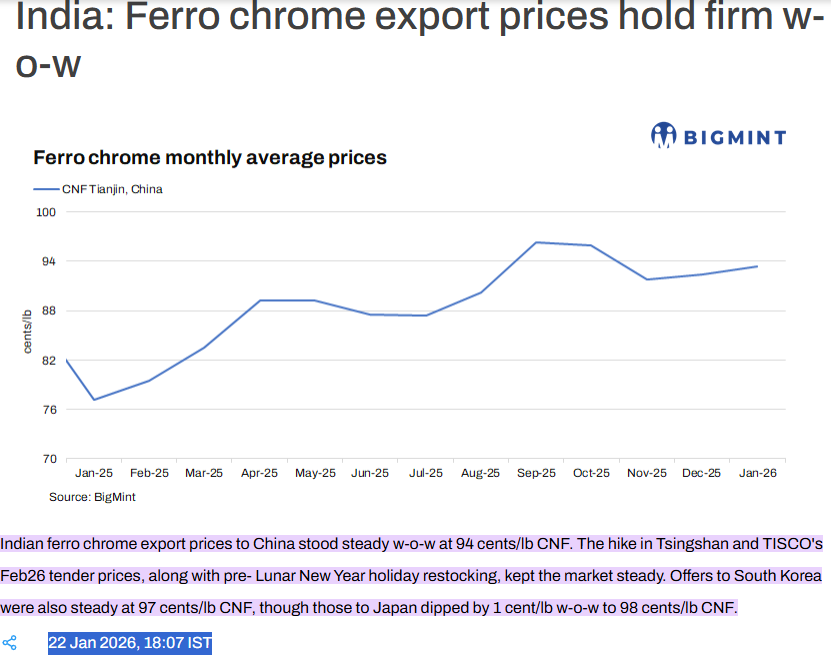

Export Prices: Indian export prices for HCFeCr (58% min Cr) to China have remained steady at approximately 94 cents/lb CNF in early January 2026, with offers to South Korea at 97 cents/lb CNF.

Key Insights

-

Supply Dynamics: The market is tight due to logistical challenges in major producing regions like South Africa and increased raw material (chrome ore) costs, which are keeping prices elevated.

-

Demand Drivers: Expanding stainless steel production for construction, automotive, and general infrastructure projects in India and the wider Asia-Pacific region is the key driver of sustained demand.

-

Market Growth: The global ferrochrome market size is projected to grow to $9.19 billion in 2026 at a CAGR of 5.9%, indicating overall strong market health that supports Indian prices.

-

Producers’ Sentiment: Producers with captive chrome ore mines, such as Indian Metals & Ferro Alloys Ltd. (IMFA) and Tata Steel Mining Ltd., are in a better position to manage production costs and navigate margin pressures.

Hope this is helpful.

Happy Investing,

Karthik

Disclosure: I am having exposure to this counter from last year lows. My views can be biased.