source of Utkal C coal block allotted to NALCO?

Apologies. It is Block D & E not C. My bad.

Company stand alone EPS in FY 21 was ₹ 61.81 per share.

Company stand alone EPS in Q-1 FY 2021-22 was ₹ 36.54 per share.

Company had unencumbered cash and liquid investment portfolio of ₹132 crore as on Mar-21.

Triggers

Company can benefit from deleveraging impacting the interest cost and growth in EPS.

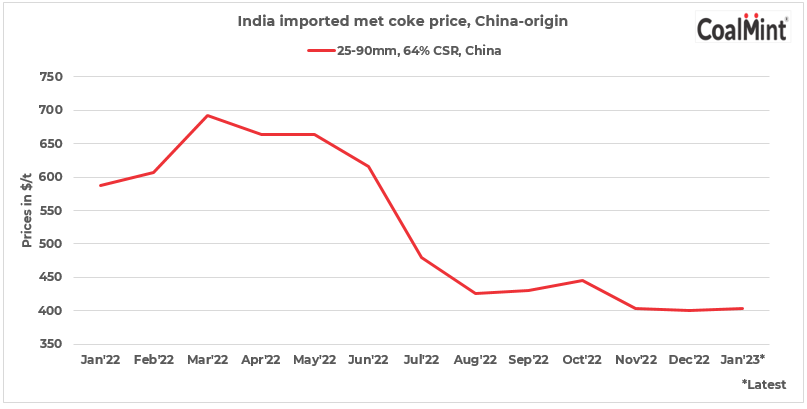

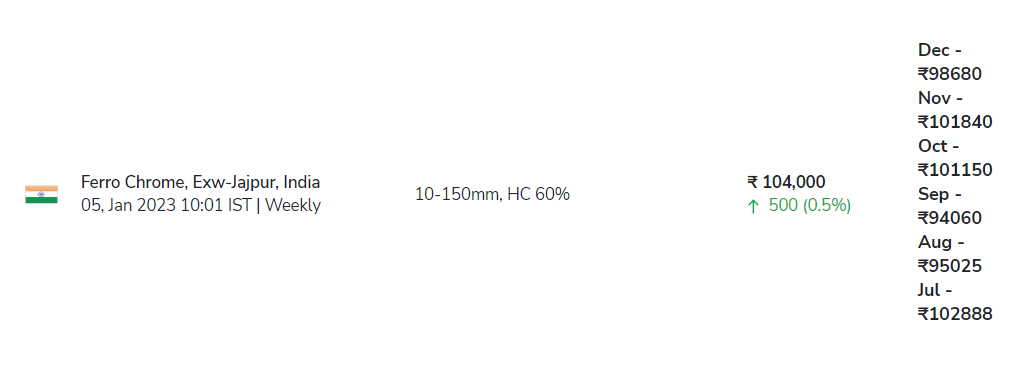

Ferro Chrome price ranges from ₹ 115000/T to 125000/T during Q-2 can result in sustainable improved margins.

Disclosure : Invested. No Reg. Advisor. Do your own diligence.

1 Like

Oct-Dec Qtr rate has been fixed at $1.8/pound. This is higher than $1.56/pound in the last quarter. This translated in to realisation of 1.22L/tonne for the company from last qtrs 1.04L/tonne.

Most of this incremental realisation will go towards coking coal input cost. While company should make 5-6k/tonne extra in the next qtr.

as per my estimates the Sales will be upwards of 620crs with an ebitda of 220-240crs in Q2. assuming a volume of 60-62kT.

in the next qtr the ebitda should be 300-330crs on volumes of 65-67kT and sales of 800crs+

5 Likes

Superb set of Numbers. EPS of 53.72 in Q-2. It was 36.54 in Q-1.

Disc. Invested, No Advisor, Do your own diligence.

1 Like

Company has prepaid the term debt of Rs 181 Crores as on date and after payment of normal installments for the quarter ending 31st December 2021

the Company’s Long term debt will reduce to Rs 143.94 Crores

and it will become net debt free.

Disc:- No Advise. Invested.

2 Likes

Land Allotment Details at Kalinga Nagar Industrial Complex (KNIC), Jajpur for

ferro chrome expansion project.

Disc:- No Advise. Invested.

Company has further prepaid the long term debt of Rs 127 .65 Crores thereby making the total prepayment of Rs 308.65 Crore till date. After payment of normal installments for the quarter ending 31st March 2022, the Company will have miscellaneous loans of Rs 14.28 Crore.

Disc. Invested.

My search for players in the metals space with captive mines lead me to IMFA.

Seems like there may be potentially significant one-offs playing out here over the next few months.

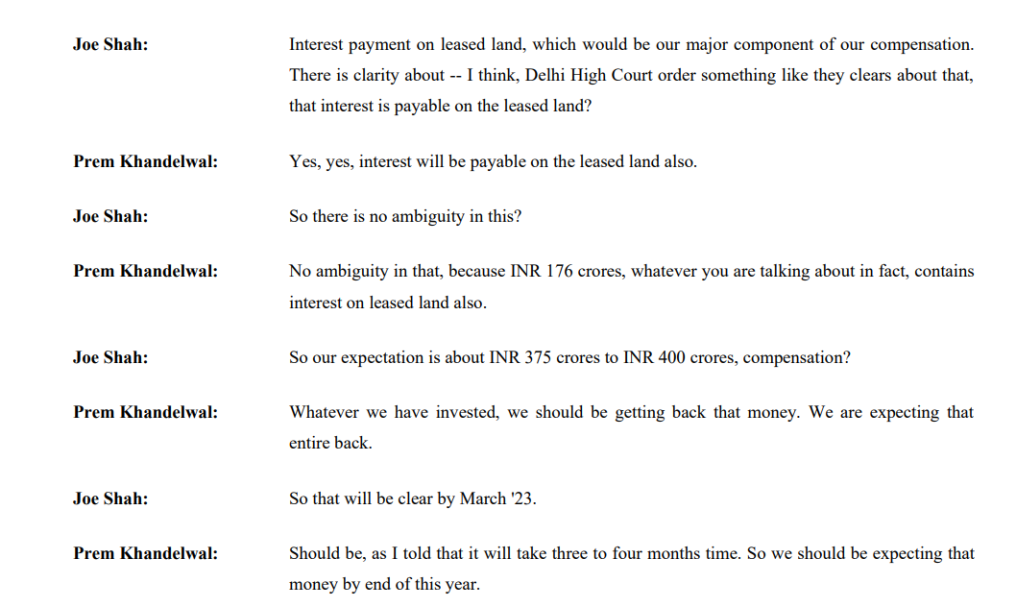

1. Receipt of 370-400 crores from resolution of UCL matter

Screenshot from Q2FY23 concall:

They posted this to the exchanges a few days back:

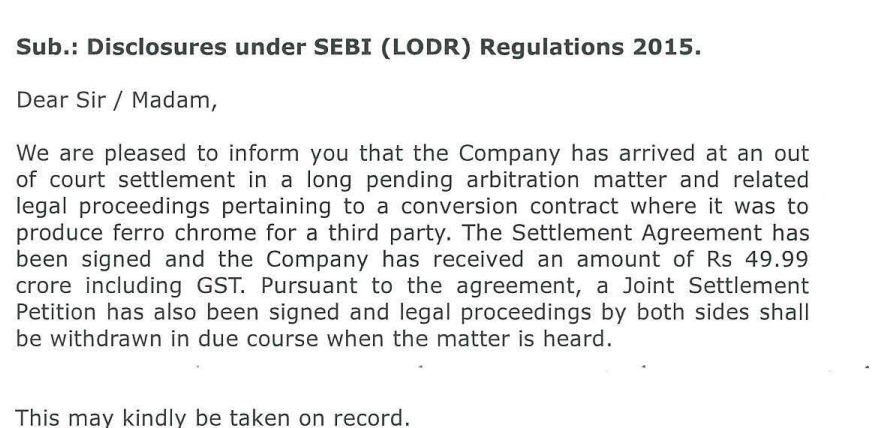

2. Receipt of ~50 crores in another matter

The above is taken from an exchange notification in October and should reflect in Q3.

Disc: Invested with a tracking position and studying further

3 Likes

If they use the 400+ crores cash coming in to clear short term borrowings, they are essentially debt free and will save on interest costs as well. Apart from this they have ~180cr in mutual funds and some cash as well bringing EV closer around the 1000cr mark. Management has guided that Q2 will be the bottom in terms of margins and passing of high-cost inventory.

If I take an average of the EBITDA of the last 5 years - something I’ve seen one of my favourite analysts in the metals space @Rakesh_Arora do - then I get sustainable EBITDA of around 390-400 crs.

So by my rough calculations, the stock is currently available at an EV/EBITDA of 2.5-3 at max. Am I missing something here? Would appreciate your thoughts.

Disc: Invested with a tracking position and studying further

3 Likes

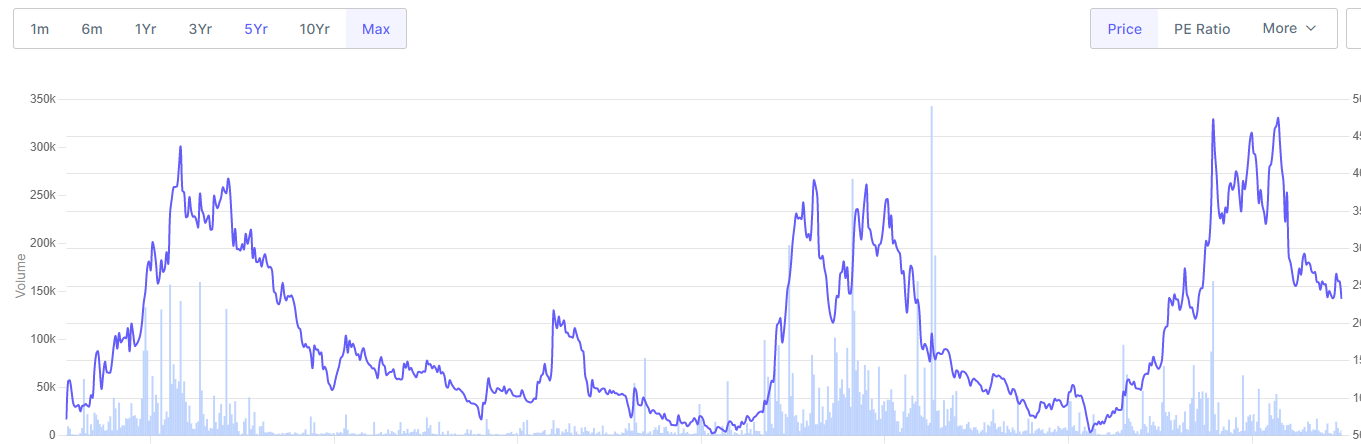

All the calculations appear very good on the paper and have always been in the case of IMFA . I am following this counter from a decade . It is pure cyclical whereby before 2015-16 it’s high low were 180-550 and the cycle of it gyrating between this two points would usually be 2.5 to 3 years . Same has been repeating i think during COVID it touched 180 levels and a high of around 980-1050 . Last year in August it went ex bonus again than a fall than again a good qtr and a high of 550 and than a cruel dumping ( in hindsight you feel bonus was used for this dump) . You will only make money when you enter at right time and can time a perfect exit , because the picture would appear most rodiest and yet the price decline will be like 30-40% within a cpl of weeks where you won’t be able to react .

Yes at this juncture it’s at a good entry point and can give 40/50 % return if you have 3 to 4 qtrs time frame provided metal cycle shows an upswing .

4 Likes

Agreed, the peaks and troughs over time window from screener, proves Shri Deepen’s point.

Have taken a tracking position on this share

Q2 had 30cr of one-offs - 20cr of forex impact and 10cr of CSR. Were it not for these, EBITDA would have been 100cr so I think Q3 should safely be 100cr + benefit from drop in costs. And there’s the 70cr inflow - 20cr for UCL and 50cr from the arbitration matter.

Meanwhile prices have held up fairly well and near-term outlook looks promising with China reopening.

Disc: Invested

1 Like

Highlights of concall:-

Cost of production has gone up from INR 65,700 to INR 79,900 in the third quarter comparedto the corresponding quarter in the previous year. Production figure for the third quarter was 58,000 tons compared 61,000 tons in the corresponding quarter of previous year.

Chrome ore-production was more in the current quarter at 134,600 tons compared to 107,900 tons in the previous quarter. Ferro-chrome sales quantity was 65,773 tons in the current quarter compared to 55,400 tons in the previous quarter. And average realization price, as I have already told you, it has come down to INR 93,000 per ton compared to INR 1,16,000 per ton in the previous quarter.

Our normal EBITDA should be INR 15,000 to INR 20,000 per ton. But as you know, we are into cyclical industry, so it keeps on fluctuating every quarter… But on an average, if you take long-term projects, it is maybe around INR 15,000 to INR 20,000 per ton. Chrome ore cost, all blended together and landed at Choudwar, it is around INR 8,500 per ton as compared to market price of around INR 15,000, INR 16,000 (Company has advantage of 6-8K /ton). Next year also volume will be around the same level of 2,50,000 tons. Because the capacity expansion will come into picture in FY ’26 only, not before that.

South Africa, it has been already declared from the month of April power tariffs will be increased by 18.65%. Further, winter tariff will be applicable during June to August, which is additional. The power situation is critical now reaching stage 6 and 7. Considering all

these factors, we are expecting further increase in Ferro chrome price in the first quarter of FY24.

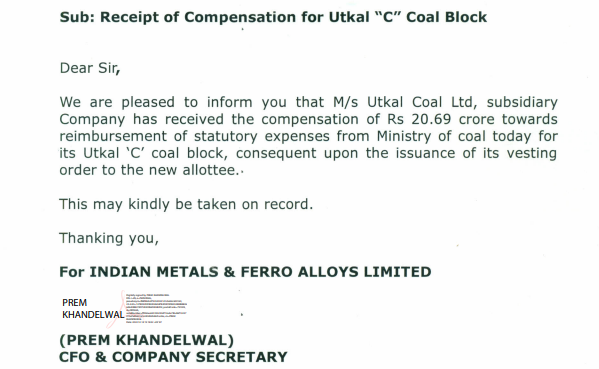

Other positive factors:- One time settlement with ED, POSCO issue resolved. Expecting recovery of amount invested in Utkal coal block (350 crore).

4 Likes

IMFA gets the part of long pending settlement amount of 131.5Cr which was held with Ministry of Coal as JSPL filed stay application on the final compensation order. Remaining additional compensation of Rs.221 Cr is also expected to come subsequently as per this notice. These funds will help the company to fund next phase of growth in mining and ferrochrome completely from internal accruals.

29-02-2024 Utkal C.pdf (3.0 MB)

5 Likes

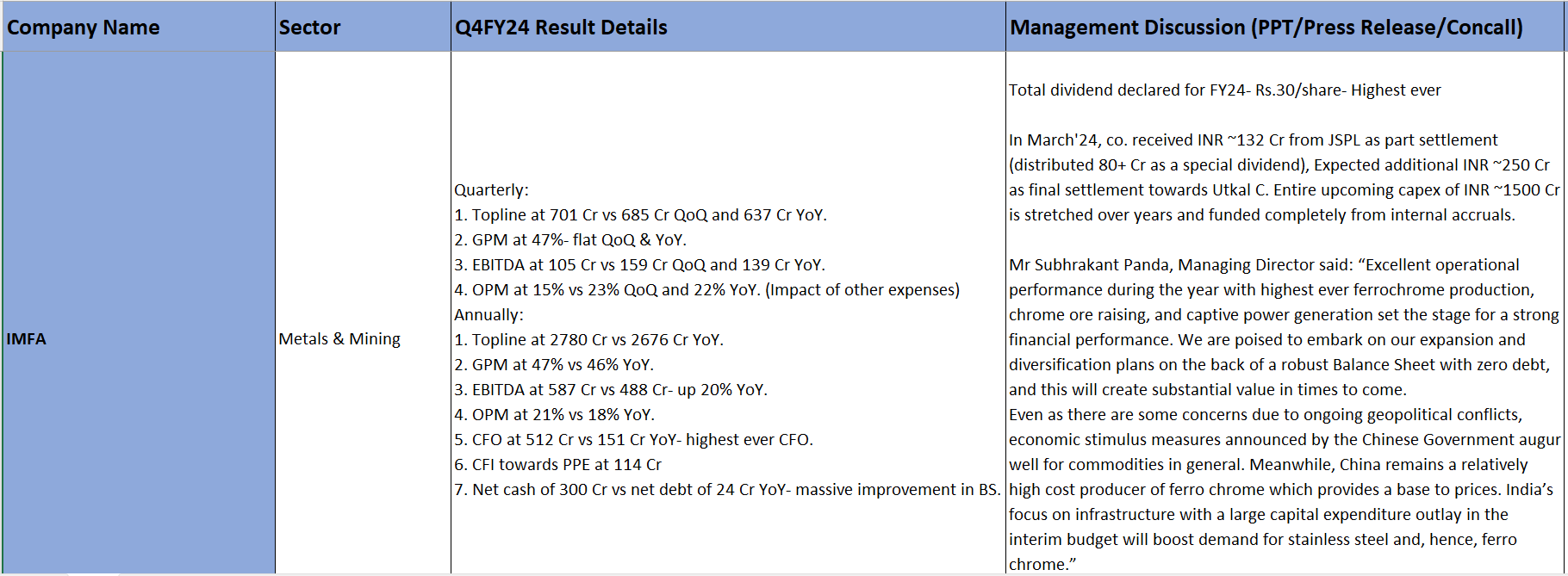

IMFA posted a weak Q4 nos, largely due to increase in other expenses- gross margins remains healthy. Few interesting points:

- Co. declared total dividend of Rs.30/share in FY24- highest ever.

- Net cash on book currently at 300 Cr- strongest Balance Sheet in company’s history.

- Valuations are still around 5x EV/EBITDA- same as 10 years of median multiple despite the balance sheet turnaround.

- Fox Consultancy- public shareholder sold almost entire holding of 5% in last 1 year- pressure on the stock price is expected to ease out.

- Co. is generating 500 Cr CFO in a year where all other global players are suffering big time- South Africa due to Power issues and China due to rising chrome ore prices. IMFA made consistent 20% margins because of its backward integration.

- Upcoming capex of 1500 Cr will help to increase volumes meaningfully- entirely funded from internal accruals.

- Management expects additional INR ~250 Cr as final settlement on account of Utkal C ongoing litigation from JSPL.

6 Likes

Not sure why the management has decided to foray into Ethanol esp. with policy uncertainty and non-core biz.

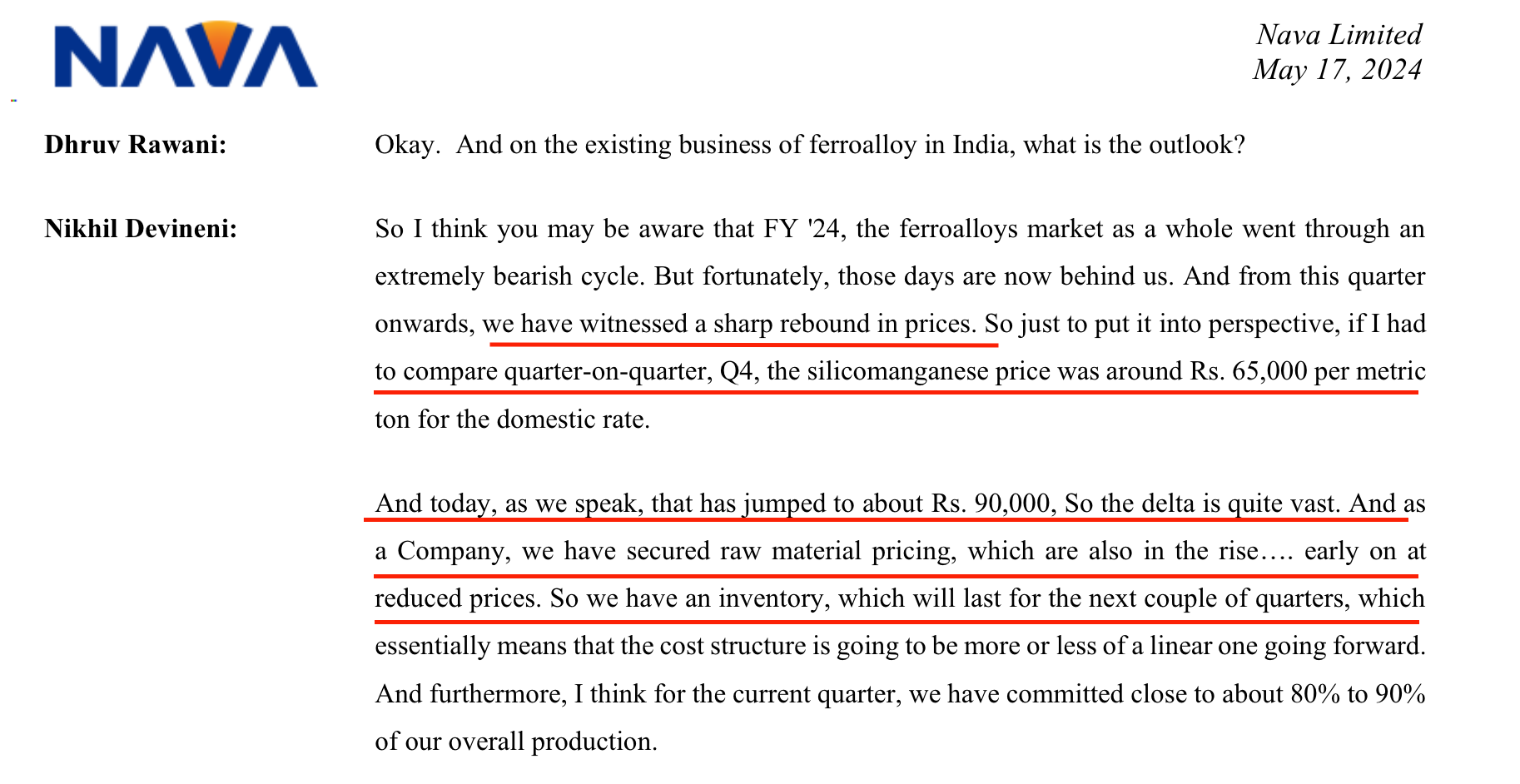

While concall is scheduled for Fri post market hours, based on NAVA and GPIL concall, it seems that there has been a sharp uptick in ferroalloys prices with likely reason being disruption in Australia which may last for few quarters.

5 Likes

IMFA receives INR 221 Crores as final compensation on account of Utkal C. Expecting special dividend.

In April they received part compensation of INR 132 Crores and they distributed INR ~80 Crores as special dividend- Rs.15/share.

2 Likes

IMFA | Financial Results

IMFA | Management Interview

- We are focusing on organic growth and expect to start the expansion of our phase 1 construction next month

- Post weak Q3 results, by the end of next year he expects their capacity to be 40% higher.

Watch here - https://youtu.be/tXipPR357xo

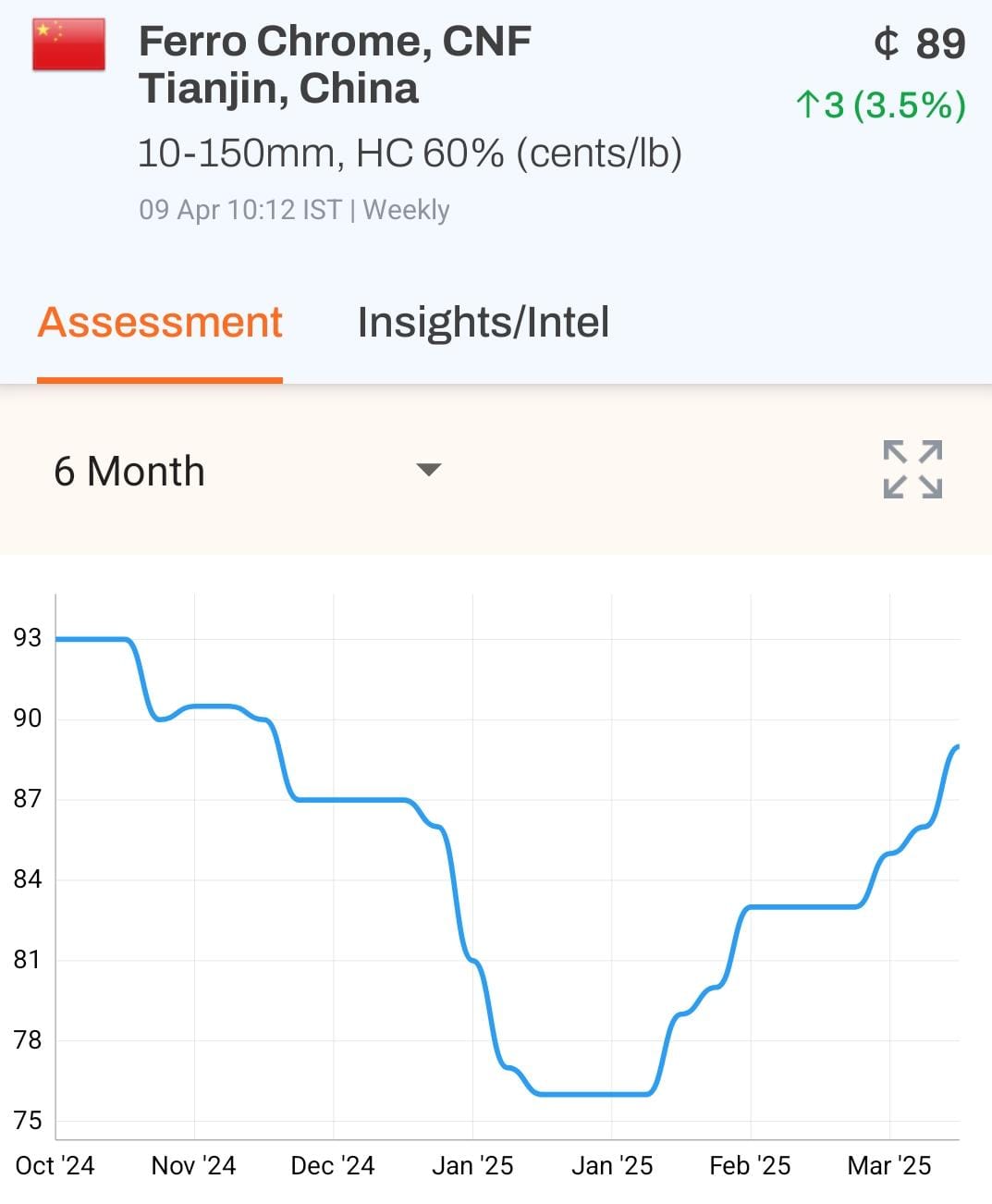

Over the last couple of months, given the lower FeCr realizations, global leaders like Glencore, Merafe etc. are also shutting down their furnace capacities as the production is not viable at current levels of FeCr. This reflects the pain point for South African smelters- it’s not currently viable for cos even 10x scale of IMFA to manufacture FeCr.

IMFA is making decent margins (~20%) because of its backward integration while global leaders are suffering- South Africa due to power costs and China due to increasing chrome ore prices (they are dependent on imported chrome ore).

Historically such supply cuts marks the bottom for a commodity.

6 Likes