Market Cap - 440 Crores

Order Book - 2600 Odd Crores

FY 14 Profit - 24 Crores

CMP - 182

The company is acknowledged as a pioneer in the industry of RCCC Pipes, Water Supply Schemes, Pipe Laying etc

Details : http://www.indianhumepipe.com/AboutUs/WhyIHP.aspx

Business :On a turnkey basis, IHP executes combined water-supply projects, i.e., undertaking the complete job of water supply from source to distribution centers. This includes construction of intake wells, water sumps, water treatment plants, water pumping stations, installation of pumping machineries, for water supply to various towns and villages of India.

**Latest Results : **

http://www.bseindia.com/xml-data/corpfiling/AttachLive/Indian_Hume_Pipe_Company_Ltd_270514_Rst.pdf

Ofcourse, NAMO’s focus may lead to a further improvement in Order Book

The stock can be considered as a beneficiary for new Water Supply Schemes of Govt. Worth a look.

**

**

Request others to join and debate on this story.

At the recent AGM, management indicated that they are looking to monetize the land bank. Company has a lot of land acquired before Independence. Now some of the land is being developed. There is a plot of land at Hadapsar near Pune, at Wadala in Mumbai and another one in New Delhi which are being developed.

Check out the latest annual report. On the back cover there is map of India marked with plots of land situated across the country.

CMD Rajas Doshi indicated that with improved road network, company does not require land parcels across the country to store pipes. So most of these parcels would be available for exploitation.

But the management is the slow and sure type and they have indicated that the Delhi and Hadapsar properties will be developed over the next three to five years.

Regarding core business, company’s order book is at a record high. Traditionally NPM is in the region of 5 per cent, but it has been lower in the past few years due to high interest costs. Now with improved business sentiment management is confident of booking contracts with higher margins.

It has orders from all the major states in the country and the outlook seems to be good with the new government concentrating on water and sewage products.

Disclosure: holding and adding on dips.

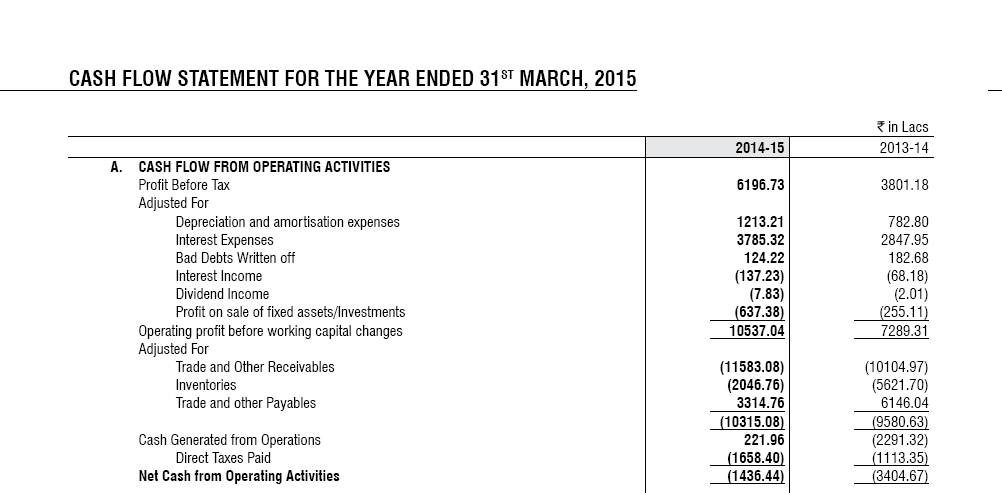

Cash flows seem terrible - a negative OCF of Rs 72 Cr. and an increase of Rs. 102 Cr. in receivables in FY 14.

Seems like cash flows are much behind earnings - not a stock you should touch IMHO. So many stocks that did this for a while suffered eventually when liquidity runs out - IVRCL, opto circuits etc.

If a compay’s OCF is not keeping pace with EBITDA, it’s a flag.,

1 Like

Haven’t looked into it but agree with Raghu 100%. OCF must be there, if it is not there, a logical answer should be there that they r investing in inventories like KRBL etc.

Moreover P/E is 18+, very high for this kind of business, i will stay away

company will be developing a plot of land at badarpur in delhi. some 3 lakh sq ft carpet area equivalent.

In another announcement on June 2, co announced that the Hadapsar land in Pune will be developed in association with Doshi Realty. That and the Delhi Badarpur land together are around 75000 sq metres.

Putting a valuation of around 60k per sq metre for these land parcels (just for calculation purpose to estimate cash flows in next 2-3 years by which time hopefully the land will start yielding money) the land value comes to around 450 crores.

Now market cap of the co is around 730-750 crores.

Applying Grahamian logic (though cash in books are 2-3 years away) the core business which generated revenues of 1000 cr and net profits of 41 crores for fy 15 is available at around 300 cr if one takes out land value. And the core business seems to be on a good footing with the PM talking about smart cities and Water being a priority sector. Order book is to the tune of 2500 crores as mentioned in fy 15 results footnote. That is 2.5 times current annual revenues.

What is interesting is that as is evident from the thread and comments made earlier, management seems to be walking the talk and in colloboration with some well respected names in the realty space viz. Sobha in Delhi and Doshi Realty in Pune. If they could monetise a couple of other land parcels things could get real interesting.

Technically the stock broke past its all time high ( posted back in 2007). and made a new high of 366 in Jan 2015 and is now taking support close to its earlier high region of 290 (plus or minus 10-15 Rs).

In technical parlance there is a principle called change of polarity. Here whenever a stock breaks its all time high then on subsequent declines it tends to find support at those zones. It seems to be the case in Indian Hume where the zone of earlier resistance (read topping zone) is offering support.

disc: Invested at near current levels more as a techno funda bet with proper stop losses in place.

This is not a recommendation and all members/readers are requested to do their own due diligence and take an informed decision.

1 Like

At the last AGM management indicated that they will gradually start monetizing more land parcels. But it will be done gradually depending on the road connectivity. Remember the land parcels were originally acquired to store pipes in different locations across India. But with road connectivity improving many locations are becoming redundant for storage of pipes. These will gradually be developed.

The management atleast seems to be walking the talk about monetising the land parcels.

I think for both these land parcels Indian Hume will get a share of revenues(around 48%) so that 450 cr you arrived at will have to be accordingly adjusted. Also order book is now around 2100 cr as 300cr of slow moving orders were removed this yr. One thing that concerns me is that this yr incremental orders were quite low so all that talk of sanitation for all hasn’t resulted in increase in orders yet.

Disclosure: No holdings; on my watchlist.

greyfool,

the figures I used are back of the envelope calculations of land value.

Actual revenues for Indian Hume will be as you mention 48% and as per the deal, land development, permissions etc costs will be borne by Indian Hume and rest construction and other marketing etc costs will be borne by the partner. The correct picture about the amount accruing to the company will be ascertained by looking at the project launch details whenever that happens. Say if there are x no of flats or villas to be sold at y price we can get an idea about revenues coming to co by getting 48% of x multiplied by y.

But what I did was to get a rough idea at base land prices and assign an approximate value to the valuation of the land bank. And these are the ones where management has done the tie ups.

There is also a land bank at Wadala which might be next in line.

The co has around 22 factories across India and from what I gather from old timers, some of them are pre independence times.

Yes agreed. There is definitely some value of assets that is not captured in present stock prices. For reference the exact details to the deals proposed/signed so far:

-

Badarpur deal with Sobha: 48.5% of 2,96,062 sq. ft

-

Proposed terms with Dosti Realty for Pune and Wadala plots:

For Pune co will receive 40% of sales generated from 5,19,772 sq.ft. For Wadala (86,670.65 sq.ft) terms are proposed & not yet signed.

1 Like

AGM was add by Mr. Rajas R Doshi CM & MD.Key highlights by Capital Mkt

Order book as end of June 2015 stood at around Rs 2100 crore as against Rs 2700 crore in the corresponding period of the previous year. 90% of the orders are from water supply, sewerage and management service business and rest are drainage orders.The order book position is after removal of some slow moving orders of about Rs 200 crore. Rest of all the orders are as per the schedule.

About 35-40% of orders are from Andhra Pradesh. Management expected orders to pick up in FY’15 given the Telengana issue got resolved. However, things are moving slowly and orders although have been bid for are yet to be awarded.As per the management, it is difficult to give a timeline on when these orders will be awarded. More than Rs 5000 crore worth of orders are in the bidding stage.The company will be able to retain some margin benefits due to lower raw material prices, however the real benefits of economies of scale is yet to be seen.

Presently as per the management, it has about 20 lac square feet of salable area of all the properties put together. The entire portion will take about 3-4 years to develop and then generate funds for the company in long term.Overall, FY’16 will be more on improving the cash flows for the company, working on receivables recovery and steady growth for the company.

3 Likes

Rajas Doshi seemed disappointed that orders are slow in coming. Orders under various central government programmes too are not being awarded speedily. He highlighted the fact that the order book was lower in the current year compared to last year.

As for developing property, some revenues are expected from the Hadapsar property when bookings open next year. Developing the reminder of the Wadala property under the Slum Redevelopment Authority scheme would be time consuming.

Developing the property at Badarpur in Delhi is not going to happen in a hurry because of the slowdown in the NCR property market. It would take at least six to seven years for the Badarpur property to be developed.

1 Like

please note that the stock has greatly benefited from margin expansion. Gross profit margin is more than 6 per cent which is far above average.

some updates from the AGM:

Chairman Rajas Doshi pointed out that funding for the projects undertaken by IHP comes from central, state and local governments. Last year’s performance was impacted because the central government has stopped providing funds to states under various schemes. Because of this state governments could not pay for work done or work had slowed down.

The company has also had to take additional working capital loans and pay interest on the same.

Now things are getting better with some states like Andhra Pradesh and Telengana prioritizing irrigation and water supply projects from the

funds provided by the centre. During the post-AGM discussions Mr Doshi also pointed out that Tamil Nadu was also accelerating spending on irrigation projects now that the elections in that state are over.

All the three southern states could be commissioning major projects and IHP will be bidding for many high-value projects. The latest Annual Report indicates that the company has many high-value projects (some valued at Rs 800 cr plus) from the three states. There is no clarity on whether there would be such projects in future, though.

Interestingly competition in the high-value segment is lower, Doshi said. He however noted that bigger players compete for the high-value projects while there are many more competitors for the smaller value businesses.

Doshi also pointed out that the order book valued at around Rs 2800

crore would be executed over next one to one-and-a-half years. THIS

WOULD BE A BIG PLUS PROVIDED FUNDING TO STATES ARE NOT CLOGGED. TRADITIONALLY, NET PROFIT MARGIN FOR IHP is around 5 per cent though it swings both ways regularly. THIS IS THE REVERSION TO THE MEAN WE SHOULD BE WATCHING OUT FOR IMHO.

IHP is mainly into supply of water though it does undertake water treatment projects also, according to the Chairman. He however pointed out that water treatment is not the company’s core business.

Work on developing its old factory land at Hadapsar in Pune and Delhi are going slow as the local governments are working on the rules governing use of industrial land for housing purposes. Doshi said there would be more clarity during the next AGM.

disclosure: holding decent quantity.

4 Likes

latest results here:

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/62CE849F_D480_4901_82E9_3541735D17E5_174027.pdf

Topline has doubled while bottom line has tripled. 1:1 bonus also declared.

balance value of work on hand has fallen slightly. so going ahead this performance may not be repeated.

disclosure: holding

1 Like

Blowout results:

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/e895e9bf-1345-46ec-91fa-5ef32d103f97.pdf

A few observations:

Topline up more than 50 per cent yoy while bottom line has zoomed 350 per cent.

Profit margins in the core business is up 15 per cent as against 10 per cent in the year ago period.

Final dividend on enhanced equity from bonus shares also declared.

Softer raw material prices have helped, but management has managed to keep construction expenses under control so as to make the most of operating efficiencies. Better still finance costs have come down which shows that cash flows are being managed better.

Management is finally cutting down on debt after asserting at past AGMs that it is great to run a business with Other People’s Money (CMD’s words). May be it is the fear of banks that are squeezing highly indebted companies, but it makes good sense for share holders: both long and short term borrowings are down by a good measure.

Trade receivables are high, but this is a problem while dealing with government agencies.

Management seems to have executed much of its pending order book which has fallen from Rs 3097 cr to Rs 2656 cr.

At CMP of Rs 435, the stock is 22 times trailing earnings. What appeared to be a slightly over valued stock this morning looks poised for an upside!

disclosure: holding in core portfolio.

2 Likes

@ayushmit

INDIAN HUME PIPE COMPANY LTD SCREENER.IN

Narration Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17

Cash from Operating Activity -48.34 -27.18 36.36 20.92 24.15 4.17 -34.05 -3.92 45.74 146.26

Cash from Investing Activity 16.33 -18.20 -27.95 3.39 -2.36 -10.22 -8.74 5.69 -9.72 -12.52

Cash from Financing Activity 39.74 35.68 -4.60 -9.03 -34.00 0.63 37.81 4.41 -48.01 -102.62

Net Cash Flow 7.73 -9.70 3.81 15.28 -12.21 -5.42 -4.98 6.17 -11.98 31.12

As per screener , CFO for FY 15 is -Rs ( 3.92 ) Cr and annual report is Rs ( 14.36 ) cr, but FY 14 is matching between screener and Annual report

How Rs ( 3.92 ) cr is arrived at?

@hitesh2710

Have analysed some of the parameters. Considering the infrastructure development planned by the GOI, IHP in a better position to capitalise…Though QoQ EPS growth, Annual EPS growth, D/E ratio looks positive Net profit to OCF is not matching in 2015 & 2014 . In the past 6 months it ran up quite a bit

what’s your take?

Now Maharashtra government is fast-tracking pending irrigation projects with some help from the centre. Since 78 of the 104 projects are from Vidarbha, home region of Chief Minister Devendra Fadnavis, one can expect the government to award tenders to those with adequate experience in the field.

The Rs 10,000 crore outlay could see Maharashtra compete with Andhra and Telengana in revamping the irrigation infrastructure. It remains to be seen how much of these orders are bagged by Indian Hume Pipes.

For the record, IHP has an order backlog of around Rs 3500 cr and the company booked revenues worth Rs 1800 cr in the last financial year.

disclosure: holding in core portfolio.

Shiv Kumar