The company has secured orders worth about 380 crores in last month for water supply and drainage which is about 20% of FY 17 sales.

AGM 2018 Notes:

Mr. Rajas Doshi was the only person actively answering all the queries.

1. Updates on Land development: (most asked question)

Company has entered into MOU with different developers for Hadpsar, Badarpur and Wadala locations. Company must spent on FSI and other requisite approvals.

-

Hadapsar, Pune:

Potential development area is around 13 Lakhs Sq. Ft. INHP revenue share is 40%. -

Badarpur, Delhi:

Potential development area is around 10 Lakhs Sq. Ft. INHP revenue share is 48.5%. MOU with Sobha developers. This land needs to be converted from Industrial to Residential for which company needs to spend money. Sobha has indicated that it will take another 1 year to get the approvals. -

Wadala, Mumbai:

This land is fully encroached by slum dwellers and therefore this would be SRA project. Potential development area after considering SRA’s share is approx. 40,000 sq. ft. only. Company has entered into MOU with Dosti developers for this land parcel.

Overall, management did not sound very confident about these land developments and it seemed that this may take forever. One should not estimate any cash flows from these land developments while arriving at intrinsic value. Also, management is not looking to monetise these through outright sale. Management mentioned that there is no liability on part of the company under RERA if the project does not start / complete on time as they are only providing land. This needs to be checked.

-

Margins will remain stable during the year.

-

It takes about 18-30 months to complete the project based on its size.

-

L&T, Subhash projects were few competitor names acknowledged by the management. There are also local players in specific regions.

-

Debt: Mr. Doshi is of the opinion that it is not good to do business with own money only. He said that as long as ROE > COC, they will continue with debt.

-

Promoters are not looking to increase their stake. They want to ensure there is enough float in the market.

Discl: Not invested

2 Likes

The Act makes both the developers and the landlord or any such party which is beneficiary of a sale of a project and receive payments from consumers as real estate developers (Promoters), and are liable to adhere to the Act.

1 Like

Did the MD say anything about the margins.

From Annual report and results i could understand, raw material cost impacted them a lot.

this could be big for IHP if it bags a few orders from this scheme

disclosure: holding

shiv kumar

2 Likes

Indian Hume Pipes AGM Notes

Like in the past years Rajas Doshi took the dais and answered questions from investors. He informed that IHP’s order book stood at Rs 5300 cr which would take around 18-30 months to complete. Doshi said many of the project works involve laying pipelines over large areas and negotiations have to be held with land owners before the pipelines can be laid.

With elections over, the order pipeline is expected to improve.

Doshi was bullish on new orders from the new initiatives like ‘Nal se Jal’ being taken by the Jal Shakti ministry of the central government.

About 90 per cent of the company’s orders involves various projects. The company uses its own production of hume pipes where required. It buys GI and plastic pipes from other suppliers if the project requires it.

Doshi refused to speak on margins when asked about the softening of price of steel and other inputs. Some contracts have a price escalation cost while other don’t, he said.

Investors were concerned about the new Andhra Pradesh government reviewing orders signed by the previous regime. Doshi said IHP has around Rs 1000 crore worth of orders from Andhra Pradesh of which notices for cancelling Rs 700 crore worth of orders have been sent to the company. He added that the company was taking legal opinion on sorting the matter out.

He gave the impression that the Jagan Mohan Reddy government may still go ahead with these projects because water supply was a big priority in the state.

Apart from Andhra, other major states which are giving big business to IHP are Telengana, MP, Chhatisgarh, etc.

IHP is undertaking Rs 40 crore worth of capex - the Nagpur factory is undergoing capacity expansion while another factory is being set up in Maharashtra. Long term loan of Rs 50 crore from HDFC Bank tied up.

Following the merger of associate banks with itself, State Bank of India’s share in loans to IHP will be reduced. The company is looking for new banks to source loans from. (IHP has traditionally been depending on financial institutions for working capital loans. At an AGM some years ago, Doshi said the company prefers to play with other’s money and hence borrowed from banks for working capital).

Doshi was also non-committal on margins. But this is common to the management of other EPC companies as well.

Interestingly, IHP’s low-profile sleeper business is showing signs of coming to life. According to Doshi the railways are giving good orders and the company has Rs 90 crore worth of orders from the railways.

The company’s attempts to monetize its land holdings are moving at a slow pace. A residential project on the company’s 48,000 sq mtr land at Hadapsar in Pune is stuck because of height restrictions due to its proximity to an airport. The factory at Vadgaon has been closed and the land is being used for a commercial cum residential project. The development potential was 49,000 sq metres or 6,43,000 sq ft.

Converting the company’s land at Badarpur near Delhi from industrial use to residential is proceeding slowly and plans are being submitted to the local authority, Doshi said. Replying to a question, Doshi said IHP had the capacities to develop the properties on its own, but lacked the marketing muscle to sell to end-users.

I may have missed some points. Others who may have attended are welcome to add.

disclosure: holding

Shiv Kumar

6 Likes

Hi, thanks for sharing the notes. Did the management mention something about the progress/funding of the past orders? Are they experiencing delay in release of funds?

This co along with other players in the DI pipe segment could be a big beneficiary of the Govt focus and need on water infrastructure improvement. And given that the valuations are not demanding…future could be good if the execution happens.

Any way to keep track of execution happening in this sector?

1 Like

The Company’s order book stood Rs. 4,355 crores in Q1FY20 as against Rs. 3,459 c

was mainly due to a range of new projects in Gujarat, Karnataka and Madhya Pradesh accounting for

orders. The largest order in all 3 categories (completed, on going & new projects) was related to providing drinking water to habitations which also hints towards the growing requirement of such projects in the country. 3 new orders from Gujarat combining to Rs. 660 crores (which contributed a meagre 3.5% of the new orders last year)

Fellow members could you throw some light “Why it’s falling sharply”

last quarter results were bad that is why. order book is at record

levels and I expect better peformance in the near future.

disclosure:holding

shiv kumar

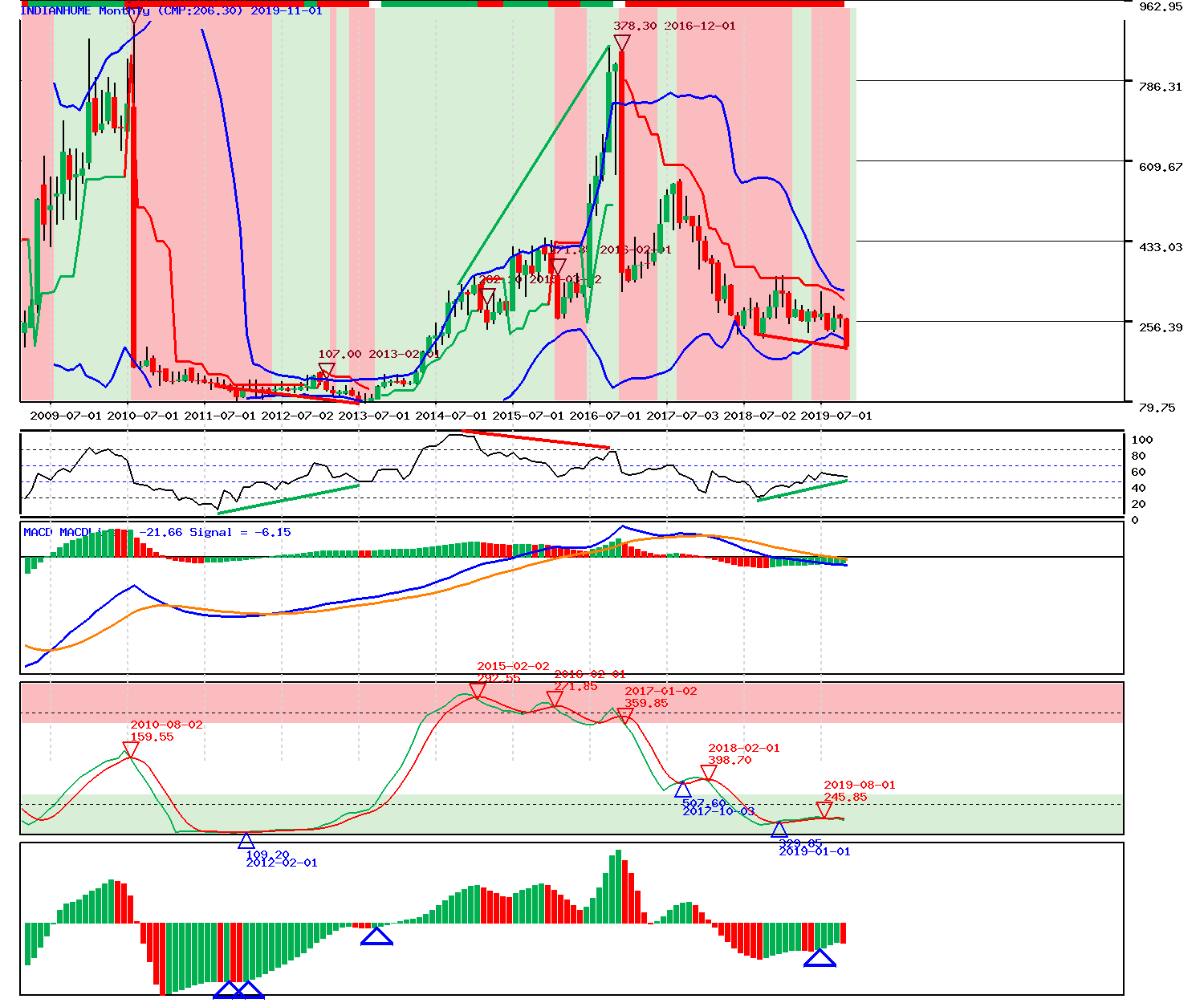

Indian hume pipes if stop falling around this area then it is showing RSI +ve divergence on monthly charts (showing such pattern on monthly charts is big thing … see the past chart that it was worked earlier)…

For investor wait for a month more to confirm this before any investment …

Anyone tracking the development in this company ? Last 5 quarters have been disappointing except for March’20.

Would like to know if there is any development on the land development front.

I understand that IHP would get revenue share in the development for their lands in Hadapsar, Badarpur and Wadala parcels.

Since these developments were signed couple of years back, any progress on the completion / marketing response.

Further, I also read that Mr Doshi said that the company is not keen to monetise their share of the development. If it is not sold after completion, how would holding such large inventory be beneficial to the shareholders? Rental income?

Core business is low margin. If mgmt decide to sell real estate, and redeploy funds to better their margins, it would be more interesting rather than keeping the real estate and fetching some rental income.

I felt IHP had great potential and beneficiary of the ambitious river linking project and invested here. but that story isnt playing out.

Disc: Invested

IHP is unlikely to directly benefit from the river linking project. they are mainly into water and sewage projects. as for land redevelopment, it is a long haul. Monetisation of earlier projects like the one at Wadala provided investors with a good dividend income.

disclosure: holding since long and biased.

2 Likes