CERC is out with draft amendments to PMR 2021 with some meaningful changes to Market Coupling. Very good analysis by ex-regulator. Still a lot of issues open, i think more litigations in FY27 btw IEX and regulator.

6 Likes

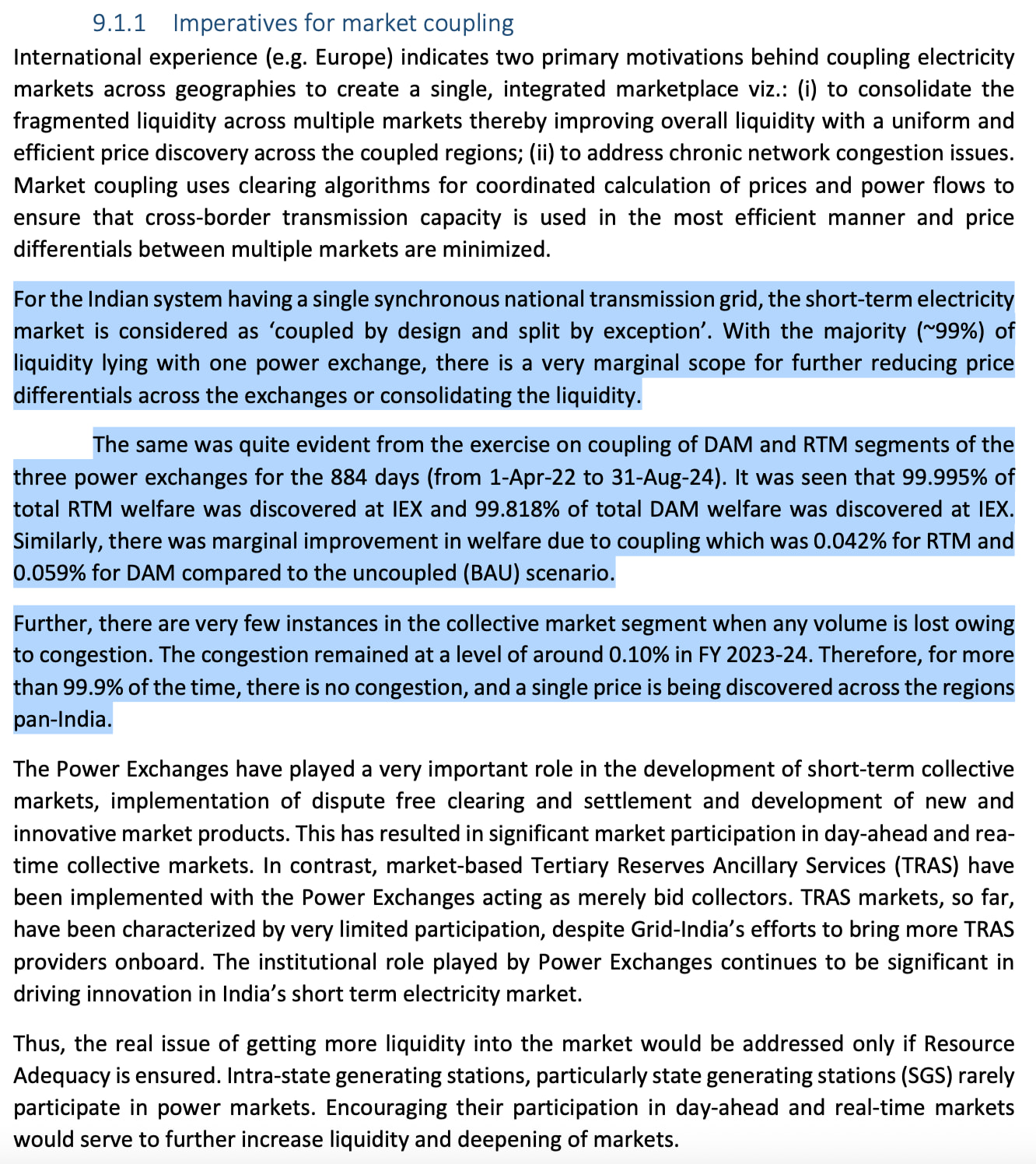

From the Jan 2025 Grid India report. Based on this - IEX doesn’t really lose out much in the shadow pilot that they have done. So what’s the worry? Even after coupling - liquidity will drive price discovery and since 99% is traded on IEX. Very few things can go wrong for the company if coupling goes ahead the way it has been described here.

Disc: Invested - might be biased.

2 Likes

Buyers and sellers want liquidity. Currently IEX has the most volumes so buyers and sellers have no option other than IEX. Post coupling, all exchanges would have same liquidity so the buyers and sellers would go to the exchange which has the least fees.

1 Like

In simple terms: Exchange will become a Broker post coupling, IEX was NSE and post coupling it will become Zerodha. So valuation multiple will obviously change from monopoly to big player in the game (and sector as well changes).

Disclaimer: Invested and biased, managing risk via position sizing in portfolio

4 Likes

The difference is that power exchange market is fraction of equity market. So I don’t know if IEX becoming a Zerodha is such a nice thing for investors.

This is unclear to me. How was the shadow pilot done? I assumed that it is done with the then pool of orders. IEX is currently a monopoly, so for the shadow pilot most order would have been from IEX. I think we may not infer from this that this is how the resulting market would be after market coupling. Please correct me if my understanding is incorrect.

I have a few queries:

- Why is govt / CERC bent on market coupling though there isn’t evidence of significant gain?

- What are your views on the impact of IEX volumes when market coupling is implemented?

- Would a power trader use IEX competitor for DAM while on IEX for RTM?

- After market coupling what in your view are the moats that would still last?

Disclosure: Invested. Complete novice to power trading domain.

1 Like

In the Blog shared by @harshc- author rpsingh states the two shadow Pilots were done. One 4 months long and the other 29 months.

The specifications of both these pilots are yet be to be released to the public. But it should be released before implementation of coupling.

3 Likes

Here are my thoughts on your queries. I am biased as I have a position.

- IEX has around 99% mkt share in short term. Other competitors have been lobbying cerc to make some changes to get some share. Cerc might want to curb iex’s dominance as it might pose a concentration risk. (eg. If something happens to iex’s server then entire trading could come to hault affecting entire grid). I still don’t understand how making grid india MCO solves this.

- I think if grid india is made MCO, there will be competiton among exchanges as to who offers minimum fees. I dont think it will be 33% for all three competitors as the gencos and discoms would be a bit hesitant to switch to others. I assume iex will still lose some mkt share in long run as others might start offering way less fees to lure discoms.

- I heard ishmohit from soic say in his video that he talked to some power trader and that trader didnt even know the other 2 competitors. We need to keep in mind that the power traders represent either gencos or discoms as i don’t think individuals trade electricity directly. So if a competiting exchange provides services at lets say half the fees, the discoms would notice it.

- Initially there might be resistance but I think ultimately it will lead to loss of moat. Lets assume the current discoms/gencos trading on iex would face friction switching between exchanges but new ones would go to the exchange which charges the min fees.

Sorry for the long post. Trying to explain my thoughts clearly.

These are my own thoughts based which I have deduced from studying the developments and management commentary. I still have some doubts whether coupling would happen or not given its low economic impact. I also have very less insight on what happens to mkt share if coupling happens.

5 Likes

1 - Why is govt / CERC bent on market coupling though there isn’t evidence of significant gain?

Like you said there is no rational reason for doing this given the economic surplus even in handpicked data and conflicting shadow pilot reports and CERC stance. Optics of Monopoly seems bad, but again given IEX has no pricing power, so there is no case for abuse of dominance, which is typical ground to go after monopolies. One could speculate on possible reasons which have made the government go after other businesses in the past but they add no value to current discussion. Legally IEX has strong ground to litigate against these reforms and delay implementation. What stance Supreme Court takes and how soon this reform actually gets implemented is judgement call.

2 - What are your views on the impact of IEX volumes when market coupling is implemented?

Big traders like PTC who are also co-promoters of some exchanges will definitely move the volumes as soon as coupling is implemented and impact can be in the range of 30%.

3 - Would a power trader use IEX competitor for DAM while on IEX for RTM?

A lot depends upon how this gets implemented. Rival exchange would demand for interoperability of margins across different exchanges. But doing this would generate systemic settlement risks and fall under Payment and Settlement Acts 2007 which in turn would require RBI oversight and regulation. EU has a system of Central Counterparties/Shipping Agents which settle trade among themselves while traders keep their margin at one exchange. However in EU this is a necessity because of different countries/regulators being involved and doesn’t make sense in Indian context as such and again would require coordination with different set of regulators. As long as margin interoperability is restricted switch from IEX would be irrational for most users.

4 - After market coupling what in your view are the moats that would still last?

Coupling as envisaged by CERC if implement would impact moats/powers as follows:-

Cornered Resource - Severely Negative as proprietary algo shifts to Grid India

Network Economies – Severely Negative as price discovery moves to Grid India

Switching Costs – Negative as users get same price across exchanges, some conservative users might still stick with IEX given bigger Settlement Guarantee Fund

Scale Economies – Negative as reduced volumes available to amortize fixed costs, per unit profit comes down

Brand – No impact due to coupling, demonstrated history of reliability and trust.

Process Power – Minimal impact due to coupling, changes to bid format etc may limit IEX innovation but IEX has grown the market over 2 decades to institutional knowledge of customer needs and system limitation remains untouched.

Counter Positioning – NA

The judgement call that investors have to make is whether CERC can actually implement market coupling as envisaged. In EU even when economic surplus was meaningful, it took almost 2 decades of regulatory effort to couple the market, can CERC with no meaningful economic surplus implement the coupling?

5 Likes

Valuation multiple changed long back and I don’t think IEX is trading at premium at any given theory.. It is either fairly priced or undervalued..

4 Likes

Agreed, that why I am still invested ![]() but Regulatory uncertainity remains and it won’t let it go anywhere meaningfully unless some final clarity emerge.

but Regulatory uncertainity remains and it won’t let it go anywhere meaningfully unless some final clarity emerge.

Reducing concentration risk with respect to critical national infrastructure like power seems to be the only logical reason & motivation so far from govt side for setting up Grid India and challenging IEX’s monopoly status, imho.

4 Likes

Buyers and Sellers of Power are another set of stakeholders. They need reliable platform to trade, efficient price discovery mechanism and fail-safe mechanism to ensure honouring of contracts. We need to observe how well the proposed Framework addresses them. Some of the questions that come to my mind

1. Further, who will choose the exchange to use for the trade- the MCO developed algorithm or chosen by the Buyers and Sellers? What I mean by that is

a. where will the Buyer and Seller initiate the trade, in the exchange platform or in the MCO platform.

b. If initiated in the Exchane’s platform, after price discovery can that transaction be allocated to some other exchange by MCO.

c. If the Exchange gets the tright to the transaction initiated in its platform, , the price discovered may be different but volume of exchanges may not change much .

d. If the Buyers and sellers do it through MCO, how the deals get allocated to exchanges ? If so, MCO becomes the Exchange in reality.

e. How will the Cross Exchange transactions i.e. Buy transaction in one exchange and sell transaction in another exchange be paired , settled and the related risks and responsibilities of exchanges for that transaction

Let us wait and watch the evolution of power regulations

Disclosure: Invested and Biased. Not a Buy Sell or Hold recommendation

5 Likes

The concentration risk would get transferred from iex (pvt but heavily regulated) to govt while introducing more risks during the transition and post transition as @Ramanathan_Narasimha pointed out in the above post. Still dont understand the reason for pushing this change.

Disc. Invested and biased

2 Likes

Other interesting thing would be to understand the thoughts of other power exchanged regarding grid india as MCO. This reduces them to the “broker” as well instead of exchanges. Anyone has any idea on their management’s commentary?

For other exchanges it is net positive. They have very small market share today. Even through they may not have moat as exchange, their revenue as a broker will increase.

So far Govt’s motivation wrt concentration risk (assuming that’s the only motivation) appears to be clear.

That doesn’t automatically mean the govt has already found the right solution yet. So far, it seems like the govt is trying out options.

What’s also clear is that since IEX has gained a monopoly status in this business, including it’s potential to be far more innovative as compared to the rest of the players, it’s also the best in the game.

As a result, IEX is far likely to withstand issues arising from changing govt regulations- which could be the reason why mutual funds continue to hold IEX.

Its ability to innovate and not simply give away marketshare without a fight would be a key point to watch out here.

Disc: Small current investment

6 Likes

As you correctly mentioned iex has been better in terms of innovation than its competitors but i feel if coupling is implemented, iex would have no reason to launch new products but rather focus on being the least cost provider.

If iex, or in fact any of the power exchange wouldnt develop a new product knowing that it will be coupled. Any pvt company would not deploy its resources if it cant benefit from it.

Cerc wants to deepen the market but the part about innovation is also not addressed in the new draft. I think cerc has to provide a valid reason to implement such a big change. (There was a proper legsl term but forgot it) So lets see how cerc handles this.

Disc: invested and biased

1 Like

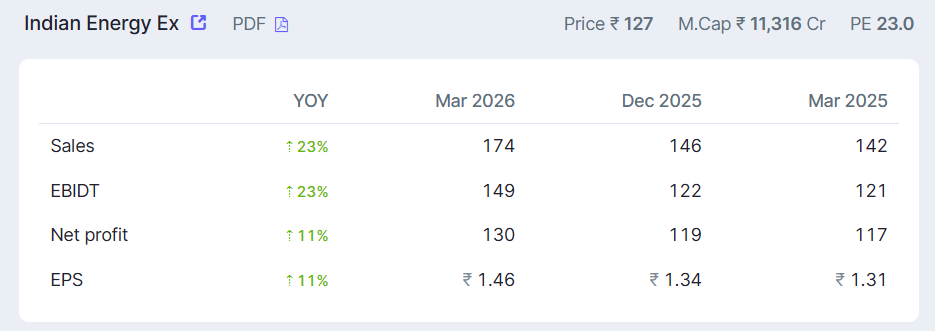

Quite Decent Q4 Numbers.

Source: Investor Deck

Barring market coupling and CERC overhang, IEX can still do good.

6 Likes

Just a thought experiment. Please provide feedback if you think the logic is flawed.

Total SA Revenues incl other income is 745Cr.

78.4% of the total revenues is transaction fees, and since DAM+G-DAM segment is 46% of the total product mix, the revenues at risk due to market coupling is 269Cr. Balance revenue is 476Cr which is not at risk. The RTM currently is 34% which grew 41%. Assuming all other drivers stay intact and the company grows ex. DAM at 15% CAGR, revenues could potentially reach 1000Cr in 5 years.

Does this sound plausible, or due to the market coupling there would be 2nd/3rd order effects which could impact revenues of other segments and hence the above logic does not hold.

Disl: invested

2 Likes

Very much possible but the biggest risk in my honest opinion is cerc waking up one day and slashing transaction fees by half.

1 Like