While pessimism continues to weigh on the Indian stock market in general, and on IEX in particular because of fears around market coupling, IEX’s underlying business continues to grow at a steady pace.

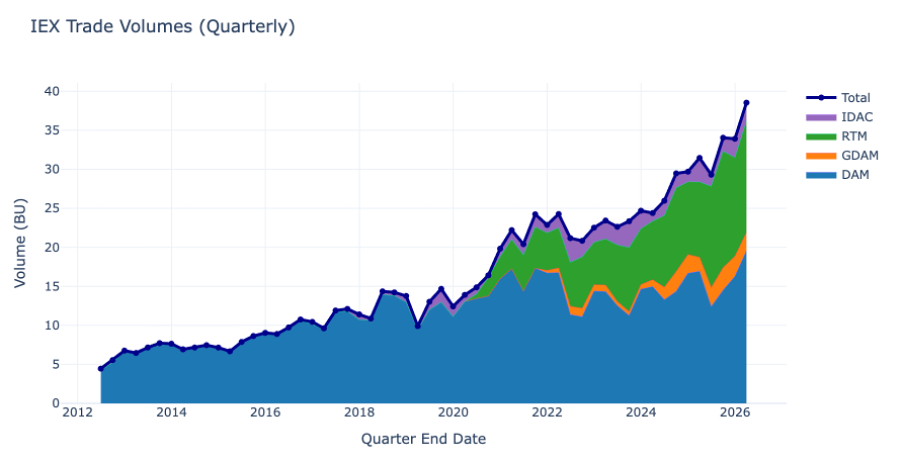

On a YoY basis, IEX has delivered 20%+growth in Q4 even though underlying electricity consumption has grown only in the low single digits. This suggests that IEX has two key growth levers. The first is the structural rise in electricity consumption alongside India’s broader economic growth. The second is the increase in supply-side uncertainty driven by the growing share of renewables, which can further accelerate exchange-based trading growth. In that sense, any increase in energy uncertainty in India is likely to be a net positive for IEX.

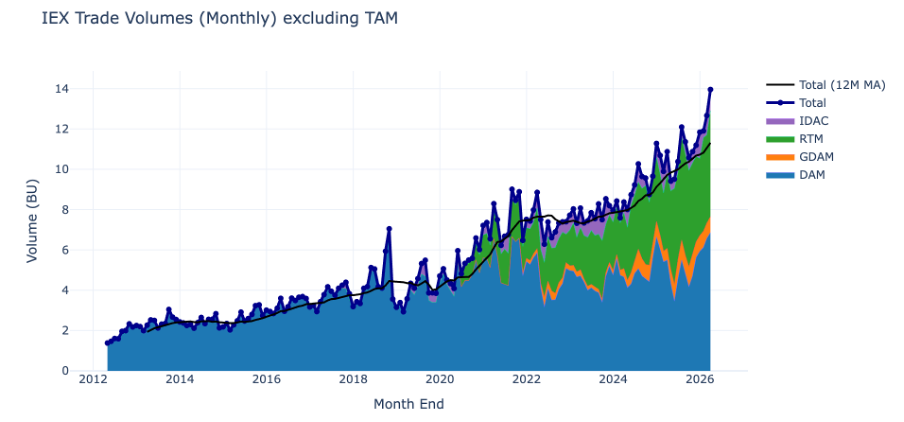

If we look at the monthly numbers, the trend appears a bit noisier, but February and March stand out as all-time high months.

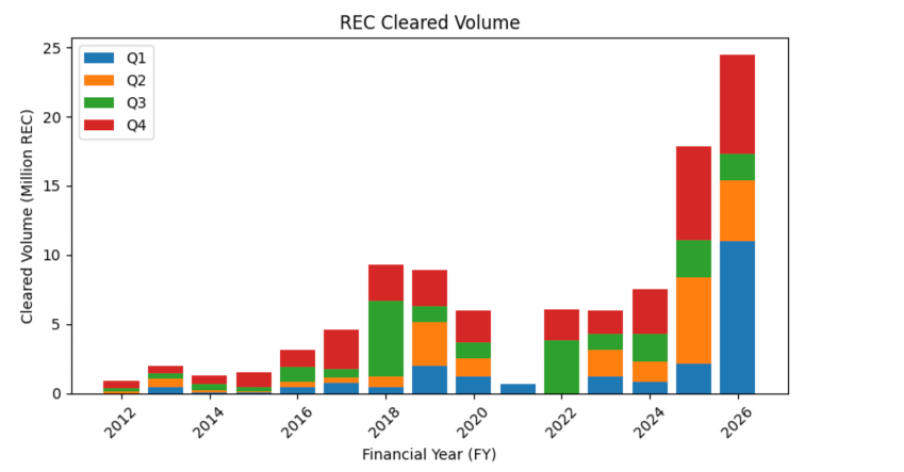

On the REC front, the overall market is growing, and IEX continues to hold more than 50%market share. There is some uncertainty because of the CERC draft paper on alternative mechanisms. However, since compliance requirements for buyers are measured at the full-year FY level, quarter-to-quarter comparisons may not always be meaningful.

On the other hand, as discussed earlier in the thread, an exit from IGX could create a one-time or two-time upside. A similar possibility may also exist with the proposed Indian Coal Exchange.

Given IEX’s near-monopoly position in the DAM and RTM segments, fears around the impact of market coupling appear somewhat overstated. Even if coupling eventually happens, implementation is likely to take years and face multiple legal and regulatory hurdles. That too won’t automatically result in market share loss. APTEL has not stayed the CERC order of July, partly because CERC itself is not expected to implement it without first framing the required regulations. And whenever those regulations do emerge, both the July order and the regulations are likely to face prolonged legal challenges.

As long as solar and wind capacity continue to expand, they will increase supply variability, with wind creating uncertainty and solar causing excess supply during certain hours. That dynamic should lead electricity trading volumes to grow faster than overall electricity consumption. Growth that comes with little or no incremental cost is often the most value-accretive kind.

Disclaimer:

All numbers from IEX website, only DAM, GDAM, RTM, and IDAC included

TAM and other smaller trading segements excluded

not a recommendation, views may be biased.