I have to respectfully disagree with your points. Here’s why:

1. Benefits are overstated…

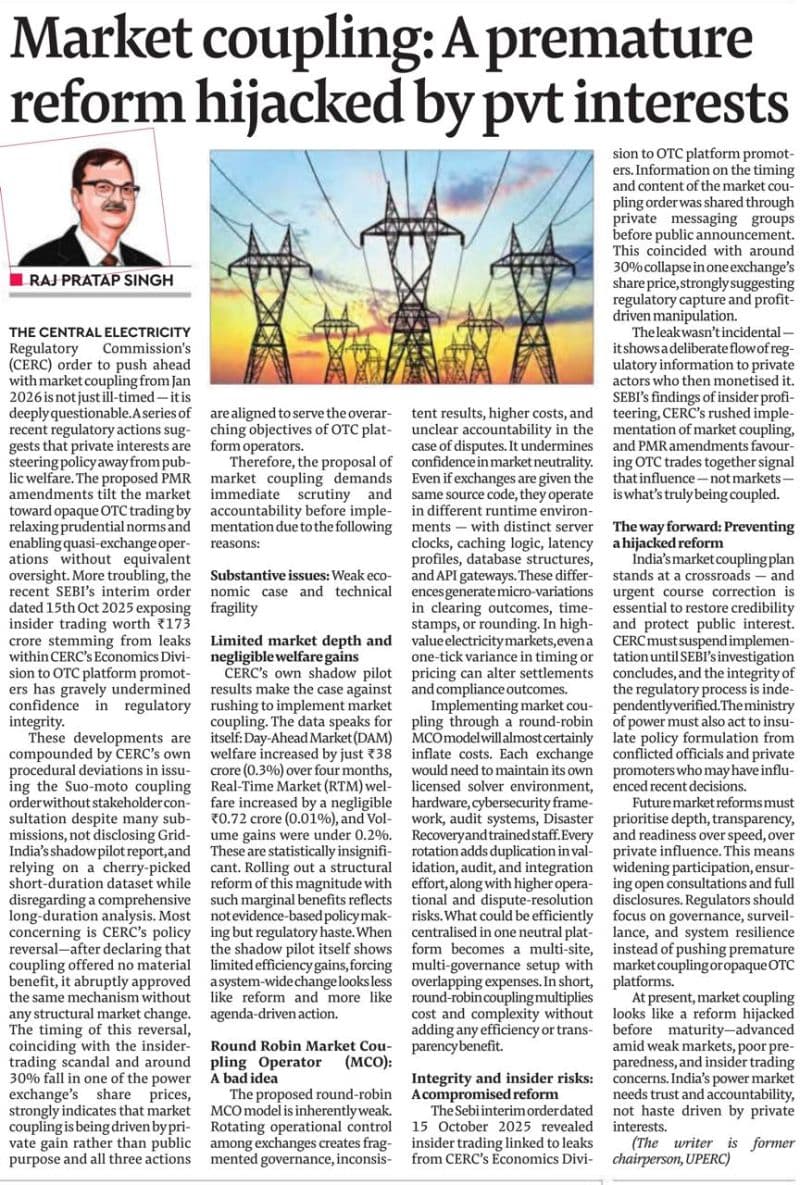

The pilot data itself shows minimal gains. Over four months, Day-Ahead Market welfare increased by only ₹38 crore (0.3%), Real-Time Market welfare by ₹0.72 crore (0.01%), and volume gains were under 0.2%. These numbers are statistically insignificant. Rolling out a nationwide market coupling reform with such marginal benefits reflects regulatory haste rather than evidence-based policymaking.

2. Not rushed? Still questionable…

The Grid-India shadow pilot report was not disclosed, and the decision relied on a cherry-picked short-duration dataset while ignoring a more comprehensive long-term analysis.

Most concerning is the policy reversal: after initially declaring that coupling offered no material benefit, CERC abruptly approved the same mechanism without any structural market changes.

The timing of this reversal coincided with the insider-trading scandal and the roughly 30 percent fall in IEX’s share price, suggesting that the move may have been driven more by private gain than public interest and aligned with the objectives of OTC platform operators.

3. Coupling hurts IEX, not just levels the field

Yes, the mechanism reduces IEX’s dominance, but it disproportionately benefits OTC players and smaller exchanges while punishing IEX, which built the market infrastructure.

4. Scandal is not separate??

The insider trading is directly linked to the reform. The leaks involved the exact timing and content of the coupling order. Trading gains coincided with IEX’s price crash, and the author of the order has been named by SEBI. This questions the integrity of the policy itself.

5. Coupling is not essential for renewables??

Grid efficiency can improve through better intra-day and real-time dispatch within the existing exchanges. Coupling adds high complexity, operational risks, and costs with little proven benefit.

Think of it like stock exchanges: we don’t couple NSE and BSE just to harmonize prices. Each has its own systems, clearing, and participants, yet the markets function efficiently.

Similarly, coupling PXIL, HPX, and IEX is not strictly necessary; the exchanges can already manage bids and liquidity effectively.