Yes that’s a rule. Any AMC cannot buy more than 10% of a company.

Kenneth Andrade of Old bridge is also increasing IEX on their portfolio

Can you explain your WACC assumptions? The equity risk premium looks very low.

Nifty 50 average return over ten years = 13.15% and risk-free rate = 6.4% for government bond. That itself should make equity risk premium = 6.75%. Additionally, the beta coefficient for IEX is >1 not 0.33

1 Like

- The implied equity risk premium used is from Aswath Damodaran’s website.

- The beta is the average for the Financial Services (Non-bank & Insurance) industry.

- I believe a business’s risk stems from high fixed costs (operating leverage) and finance costs (financial leverage). The low values for both of these in this business validate the low weighted average cost of capital.

1 Like

All makes sense, except for the Beta which I would say is higher than 0.33

1 Like

You might want to check Kenneth Andrade’s views and logic as to why he bought into IEX. That will help answer some of your questions. Given that PPFAS is also has a conservative strategy and follows value investing, it probably would overlap.

Also dont forget, its a healthy cash generating machine that will throw excess cash which will be distributed as dividends which is a bonus for MF. Not everything has to be high growth business in a mutual fund holding.

4 Likes

Do you have any video or podcast where Kenneth shared his view on IEX? i know his Old bridge MF is holding around 4% of IEX at MF level but would love to hear his views specifically.

4 Likes

In this GenAI first world, searching and finding something is far more easier across all formats. Do your due diligence first (if not done already). If you still dont find it, search some more. It helps to become better investor to dig out information!

6 Likes

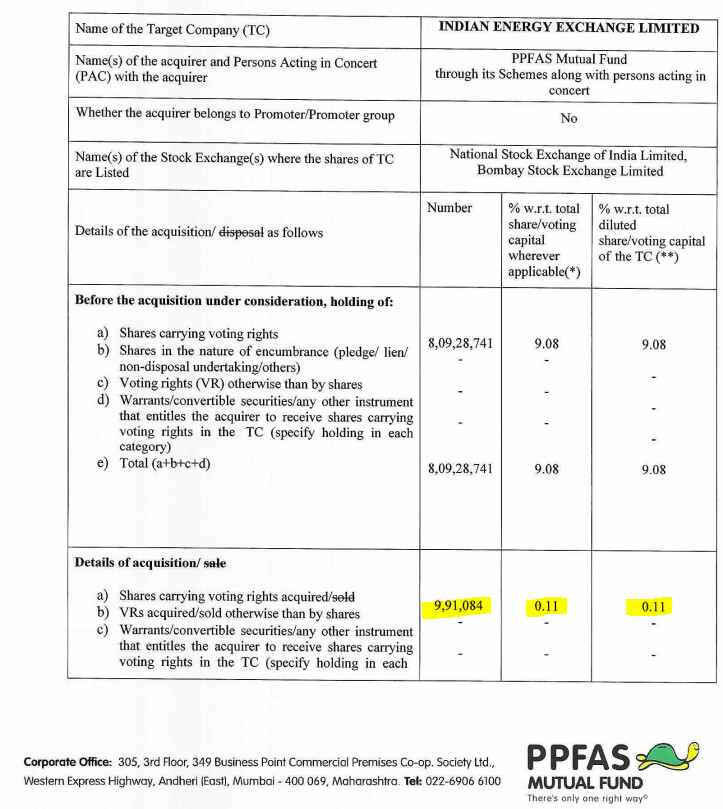

PPFAS buys more of IEX

Now holds about 9.19% of IEX

PPFAS Flexi cap now holds 0.89% (as per the latest August 2025 factsheet) from previous 0.53%.

5 Likes

As a consultant who’s worked extensively in the electricity space - idk how coupling will work.. all of us still go and tell clients (DISCOMS and C&Is) to procure from IEX especially for green energy

10 Likes

Can you please elaborate what you mean by ‘idk how coupling will work’. We have heard from IEX management about the challenged in implementing coupling. Will be very helpful for the forum to hear from someone with work experience in the field, as outside-in view.

Disc - invested.

8 Likes

Oldbridge/ Kenneth Andrade adding more IEX to his MF holdings as well.

2 Likes

We are sharing our detailed analysis of IEX’s performance, growth drivers, and sectoral trends as part of this discussion. We invite other members to share their perspectives, insights, and counterviews to enrich the conversation.

Indian Energy Exchange (IEX) is India’s premier power exchange, providing a country-wide automated platform for electricity, renewable energy, and certificates, with cross-border trade capability. It offers transparent, efficient price discovery, and liquidity, serving over 8,100 stakeholders in 28 states and 8 union territories, including more than 4,900 commercial and industrial consumers. Through market price optimisation, IEX helps to maximise social welfare.

In Q1 FY26, IEX witnessed total revenue of ₹184.2 crore, a 19.2 percent year-on-year growth, and PAT of ₹120.7 crore, a rise of 25.2 percent. Electricity trading volumes grew 15 percent at 32.4 BU, led by DAM, RTM, and GDAM segments. RTM volume jumped 41 percent, green markets rose 51 percent, and RECs were up 150 percent, as there was improved compliance and regulatory support. Enhanced supply from wind, hydro, and coal lowered market clearing prices within DAM and RTM, whereas other revenues increased because of mark-to-market gains from fund investments.

The CAGR returns of Indian Energy Exchange (IEX) indicate differing trends across time horizons. The 1-year CAGR of -33.1% reflects significant short-term decline, likely due to regulatory developments, lower market clearing prices, and market volatility. The 3-year CAGR of -0.7% shows near-flat performance, suggesting that gains and losses over the medium term have largely offset each other. In contrast, the 5-year CAGR of +15.7% highlights strong long-term growth driven by increasing electricity trading volumes, dominance in DAM and RTM markets, renewable energy integration, and diversification into IGX and ICX. Overall, IEX demonstrates short-term volatility but robust structural growth and resilience over the long term.

The PE chart over the last 3 years indicates fluctuations - beginning near 40, rising above 55 in late 2024, and later declining to around 28-30 in 2025. It shows valuation movements with a recent transition to lower multiples, reflecting changes in market dynamics or earnings performance.

Long-term sector drivers are still positive. Electricity demand in India is likely to expand at 6 percent each year through 2032, while IEX has traditionally expanded 2.5 times demand. Renewable and hydro capacity is likely to increase to 60 percent by FY30. Novel market mechanisms like Battery Energy Storage Systems, FDRE, and Round-the-Clock RE will increase liquidity further. Policy initiatives like the Shakti Policy guarantee fuel availability and encourage trading of un-requisitioned excess power on exchanges.

Product and regulatory initiatives comprise electricity derivatives on MCX/NSE based on IEX DAM prices, possible extension of Term Ahead Market contracts to 11 months, Green RTM, Virtual Power Purchase Agreements, and capacity markets under the Resource Adequacy framework, all anticipated to push volumes.

Market coupling in DAM, a CERC mandate from January 2026, is a risk factor, though now applicable to only (35-40)% of volumes. Challenges in implementation can delay full impact, and IEX’s moat->95% market share in DAM/RTM, tech strength, and customer interaction are the buffers, particularly in RTM liquidity and service differentiation.

Diversification enhances growth opportunities. IGX recorded highest-ever gas volumes of 24.6 million MMBtu (+109 %) with PAT of ₹14.1 crore (+87 %), backed by OMCs, refineries, CGD companies, and mandatory biogas blending. ICX released 44 lakh I-RECs and is examining Extended Producer Responsibility trading. IEX is also considering India’s first Coal Exchange, in collaboration with the Ministry of Coal and subject to legislative support.

Overall, IEX has market leadership, solid financials, structural growth drivers, and product diversification. Although market coupling is a regulatory headwind, IEX’s technological advantage, high liquidity, and increasing platform presence in power, gas, carbon, and coal markets place it well to take advantage of India’s increasing demand for electricity as well as energy transition.

We have shared our analysis of IEX and would be happy to hear the views and perspectives of other members. Your insights and counterpoints will help enrich this discussion.

-

How do members view the impact of market coupling in DAM on IEX’s overall volumes and competitive positioning?

-

Do you think IEX’s diversification into IGX, ICX, and a potential Coal Exchange will become significant growth drivers in the next few years?

-

How do you interpret the short-term negative 1-year CAGR (-33.1%) versus long-term 5-year CAGR (+15.7%) temporary volatility or structural challenge?

-

Will renewable integration and BESS/storage mandates meaningfully increase exchange liquidity, or are there operational constraints?

9 Likes

A beautiful 360 degree analysis on IEX investment thesis and antithesis:

14 Likes

This clearly shows that “Common Man / Retail Investor” is always at disadvantage in Indian markets which in spite of tight regulations have loop holes which are extracted by people with special privileges leading to gains for them but might result in loss for middle class retail investors.

Such incidents not only tarnish the image of the Regulator (CERC here) but raises doubts about whether these regulators are doing their job with honesty and transparency. I have raised concerns about regulator on other social platforms earlier.

It seems that, there might be many more such unearthed cases and retail investor should be cautious while investing in companies with small size even though it might be a market leader. Prima facie, here IEX management as of now may not have done any thing wrong but still its investors are at a loss to some extent.

Diversified Portfolio with a single stock not beyond 5%-6% is a safer strategy in Indian markets, at least for middle class investor.

Disclosure: I had a small position in IEX during 2022-23 but at high valuations and after that, I was not able to understand the business fully hence exited with no profit/no loss. I have mentioned about role of regulator in market coupling seems too much efforts with not much gains, on other social platform.

(I have edited this post as my understanding about News was not fully correct earlier).

4 Likes

This insider trade was done by CERC officials. Why should this ‘tarnish’ IEX’s reputation?

5 Likes

I don’t think that is interesting because it does not affect company’s business and company and its employees or KMPs are not involved even indirectly in it.

2 Likes

This should affect CERC, not IEX. It could be a positive news for IEX which has challenged CERC’s coupling decision in the tribunal. There’s a possibility of delay in implementation of market coupling.

9 Likes

Market Coupling never made sense from the start. With more than 80% of the power being negotiated via PPAs instead of via exchanges , the idea of “Market Coupling” is nothing but a scam to keep the price of IEX below a certain threshold. But for whom and how long ? The SEBI investigation could unravel more.

3 Likes