So far looks like MFs are simply averaging down a bit & waiting till Q3/Q4 pre/post CERC order implementation or are just plain sceptical and directly seeking answers from management

1 Like

Apologies for a novice question

How could HPX male impressive gains in TAM. What are the chances of HPX replicating this success in other segments after coupling.

would appreciate any insight, thanks

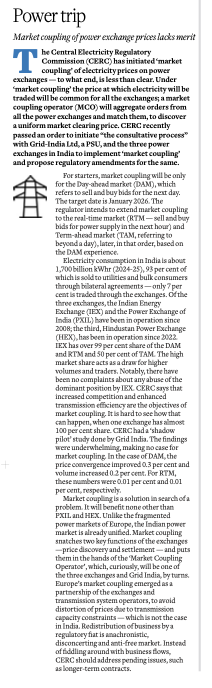

Agree with what its written in the article:

Market coupling feels like a solution chasing a non-existent problem. The only real beneficiaries appear to be PXIL and Hindustan Power Exchange.

Unlike Europe, where electricity markets were fragmented and needed integration, India’s power market is already a unified platform.

This move effectively takes away the price discovery function from individual power exchanges and hands it over to a rotating Market Coupling Operator (MCO), comprising the three exchanges and Grid India. However, financial settlement will still be handled by the respective exchanges for their own bids, as clarified in IEX’s latest concall.

In Europe, market coupling was a cooperative effort between exchanges and transmission system operators, designed to address genuine issues like price distortion from transmission bottlenecks. Those conditions don’t exist in India.

Reallocating business through regulatory intervention, rather than market forces, feels outdated and counterproductive. Instead of interfering with the natural flow of market operations, CERC should focus on unresolved priorities like improving mechanisms for long-term power contracts, enabling Contracts for Difference (CfDs), scaling up Battery Energy Storage System (BESS) products/contracts, and streamlining Virtual Power Purchase Agreements (VPPAs) recently introduced. These reforms would deepen the market and drive real progress, rather than just reshuffling volumes.

Disclaimer: Invested

10 Likes

Beg to diifer with you regarding the clearing and settlemen process. IEX has clarified in latest concall that the clearing and settlement will sill be handled by respective exchanges

1 Like

Thanks for pointing that out. You are right. After rechecking the IEX management commentary, I realize the MCO will be responsible only for price discovery, while clearing and financial settlement will still be handled by each exchange for bids submitted on their platforms.

2 Likes

Understanding Market Coupling, IEX, and Why I’m Still Confidently Holding

Let’s decode what market coupling means for India’s power exchanges — and why I continue to hold IEX despite the noise. A thread for serious investors

- What is Market Coupling?

It’s a centralized regulatory mechanism — all buy/sell orders from various power exchanges (IEX, PXIL, HPX) are pooled, and trades are matched on the most efficient price.

The exchange offering the best rate clears the trade — not the one the user picks.

There is strong speculation in the market that coupling will help HPX & PXIL gain volumes without needing to fight IEX directly in pricing or liquidity.

- Round Robin Explained

Under the phased rollout (starting Jan 2026), exchanges will take turns acting as Market Coupling Operators (MCO) in a round-robin model.

While the exact frequency of the rotation (e.g., monthly, quarterly, etc.) hasn’t been explicitly detailed in the public information I have, the core idea is that the three power exchanges (IEX, PXIL, and HPX) will take turns acting as the MCO on a rotational basis. All trades during that time will go through that operator’s systems. It’s like IPL matches being hosted in different cities — to avoid monopoly and share infrastructure load.

Grid India (which is owned by the Government of India, under the Ministry of Power) will act as the backup & audit operator, ensuring fairness and neutrality — ensuring no manipulation, just like a referee in a match.

This is CERC’s way of avoiding monopolistic behavior.

- Is It Like showing BSE/NSE quotes on broker platforms like Zerodha ?

Not really. Zerodha gives you quote visibility, but you choose where to execute.

Under market coupling, you won’t know which exchange you’re routed through — the algo picks the best.

It’s like IRCTC auto-picking the best route instead of letting you choose the train.

Untill now, IEX was offering lower pricing, due factors discussed in Point 4 below.

- If PXIL Couldn’t Dent IEX for 17 Yrs (HPX for 3 years), Why Now?

Exactly. PXIL (launched Oct 2008) and HPX (Jul 2022) haven’t gained ground against IEX (launched Jun 2008) because of IEX’s:

- First-mover advantage

- Superior tech infrastructure — near-zero downtime, fast execution

- User-friendly UI/UX — for both large buyers and smaller discoms

- Trust built through regulatory alignment + transparent pricing

- Network effect — as volumes built up, more participants joined for better discovery

So while market coupling levels the price playing field, it doesn’t eliminate platform differentiation — which still influences where participants choose to place their bids.

CERC’s order may change the way pricing is done, but it does not eliminate the need for strong, liquid, and trusted platforms. And in that race, IEX is still miles ahead

So yes, the platform strength, consistent reliability, and reputation as the “default” choice created a self-reinforcing loop of trust → liquidity → deeper discovery → more trust.

That’s hard to replicate overnight.

- The Real Challenge of Market Coupling

Yes, price discovery becomes centralized.

But platforms still matter — for infra, execution speed, dispute resolution, etc.

IEX has years of reputation, infra maturity, and trust. That edge doesn’t vanish overnight.

Think Zerodha vs others — same price, different user experience.

- Why I Invested in IEX in the First Place

- India’s exchange-based power trading is just 6–7%, which was just 4% in 2021 (vs >50% in developed nations)

- Massive energy tailwinds: Data Centers, AI, EVs, Residential demand

- Government push for market based energy pricing from traditional PPA.

- Innovation: IGX (Gas), Carbon Exchange, Derivatives

- Clean balance sheet & high ROE

- A dominant operational moat built over time

- Why did IEX divest portion of IGX’s Stakes — Is it a Red Flag

In 2022, IEX sold 4.93% in IGX to IOC, bringing in strategic sector expertise to bring IOC as a strategic partner, drive gas market growth, share risk and capabilities

Strategic motive of IOC behind joining IGX was to become a partner with sector expertise—from LNG terminals to CGD networks—supporting gas market growth and aligning with the government’s push to raise gas in India’s energy mix to 15% by 2030.

This aligns with other strategic investors such as NSE, GAIL, ONGC, Torrent Gas, Adani Total Gas—creating a consortium backing IGX’s scale-up. IEX’s leadership in gas trading moves from being a pure owner to a strategic partner, sharing risk and expanding legitimacy across regulatory and distribution networks. (Source: livemint.com/companies/news…)

As a result, IEX holds ~47.28% stake; IGX now equity-accounted (not consolidated) as an Associate In essence, IEX pivoted from owning IGX outright to forming a broader gas-exchange ecosystem with other large investors. This was a deliberate, strategic move—not regulatory pressure or retreat—and positions IGX for scale in India’s evolving gas economy.

Strategic partnership ≠ weakness.

- If CERC’s own report said there is no benefit, why implement it?

The 2022 report submitted to CERC clearly stated “no proven cost advantage” to consumers.

However, there could be political pressure for fair access to new exchanges, push for de-monopolization of IEX, and Global alignment with European-style market mechanisms.

Whether it helps the market or not — we may only know after implementation.

- Demand Explosion Ahead

India’s power demand is on the verge of an inflection:

- AI already eats up 4% of global electricity

- Semiconductors = power guzzlers

- Data Centers: 1.4 GW → 9 GW by 2030

- Inter-region power transmission lines: 119 GW in FY25 to 168 GW in FY32

- EVs = consistent grid demand

- Rising residential power usage: Even Tier 2/3 AC demand rising fast. AC is now a necessity, not luxury.

All this needs real-time price discovery, transparent allocation, and efficient balancing — and that’s exactly what power exchanges enable.

No serious digital or industrial ambition can succeed without vibrant, market-based electricity systems.

IEX may face cycles. It may get regulated.

But it won’t become irrelevant. So no, I’m not blindly holding — I’m betting on the pulse of a growing economy.

- No Promoters = Bad? Think Again

Some worry about high public holding, and infact it can be a red flag in some cases.

But in IEX’s case, we should respect clean, well-governed business models that run efficiently without a promoter. It’s not retail sentiment driving the core here — it’s FIIs and DIIs taking calculated long-term bets. That speaks volumes about the quality of the business, management, and moat. Ownership patterns alone don’t define risk.

The absence of promoters isn’t a flaw — it’s a design choice. Let’s not forget:

- Zero debt

-

80% margins

- Monopoly-like grip (till now)

- Strong institutional faith: Public holding only becomes a problem when the business doesn’t have institutional conviction — that’s not the case here. the numbers speak louder than opinions

- Strong regulatory tailwinds in the long run

In fact, here’s how shareholding changed (Sep 2022 → Jun 2025):

DII: 22.39% → 34.12%

FII: 15.79% → 18.53%

Public: 61.54% → 47.07%

Attached the trend from screener.in

That’s institutional validation in action. While the retail crowd exits fearing uncertainty, the real smart money is quietly accumulating.

- My Take on Market Coupling

IEX may face short-term regulatory headwinds.

But its liquidity moat, infra strength, brand equity, and innovation pipeline remain unmatched.

As coupling clarifies, IEX may gain even more trust as the market matures.

It’s not just a price discovery engine.

It’s the plumbing of India’s digital & industrial growth.

- Final Word

I’m not blind to risk.

But when you’re betting on the system’s core infrastructure — energy rails of a fast-growing economy — you don’t exit at the first sign of change.

You track, learn, position, and ride the maturity curve.

IEX is one of my highest conviction long-term holdings. Period.

Would love to hear your views — agree, disagree, or add to the thesis. DMs open.

Disclaimer: These are purely my personal viewpoints, not investment recommendations. I am not a SEBI-registered Research Analyst (RA). Please do your own independent and thorough research or consult a qualified financial advisor before making any investment decisions. This content is shared for educational and knowledge-sharing purposes only.

25 Likes

Yes, it turned out to be a long post — but I felt it was necessary to simplify and explain IEX’s regulatory complexity, optionalities (gas, carbon, green), and the market-coupling risk in plain terms for investors who may not follow these developments closely.

Sometimes clarity needs depth. I’d rather be long and useful than short and confusing.

Happy to engage further — open to views

1 Like

While Market Coupling is set to impact only the Day Ahead Market (DAM) — which contributes roughly 30–40% of IEX’s total revenue — it’s important to view this in context:

IEX holds ~85% share in DAM. Even if this share gets halved due to coupling, the maximum revenue impact is ~20–26% of total.

But IEX is not just DAM:

60–70% of its revenue comes from other products — Real-Time Market (RTM), Green Term Ahead, Green DAM, Term Ahead, Cross-border Trade, etc.

IGX (Indian Gas Exchange) and ICX (Indian Carbon Exchange) are scaling up fast, and could be game-changers.

Yes, we saw a sharp correction (~30%) in stock price when the news broke, but:

- Recovery followed strong quarterly results

- QoQ performance is improving steadily

- At some point, mean reversion kicks in — market can’t ignore fundamentals forever

My take: Even if one revenue stream shrinks, others are expanding, and the monopoly-like edge in tech, trust, and infra isn’t going away soon. Punishment for uncertainty has its limits.

Let’s watch the business, monitor the results, not just the headline.

8 Likes

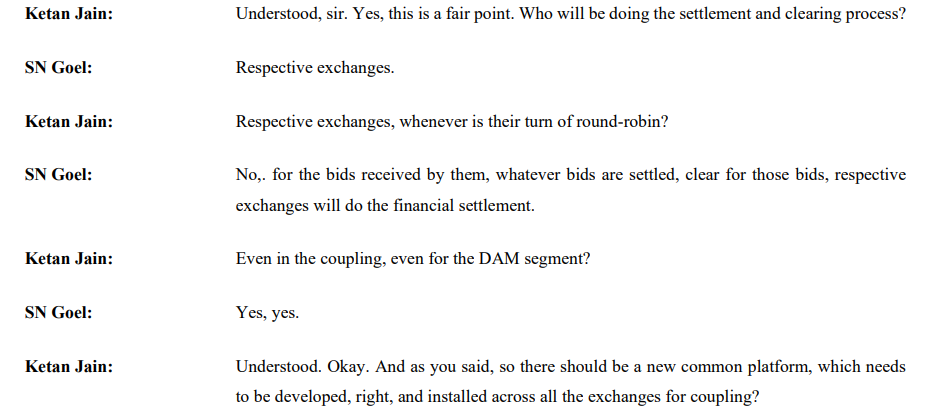

Will market coupling not ensure we have common software running on all three exchanges? I know clearing and settlement has to be handled by the respective exchange whose bid was matched but there will be a common software for all 3 exchanges. This was confirmed by management in the recent concall as well. So this takes away one of the tech edge over others.

1 Like

Implementation details of market coupling needs to be worked out. The common software you are referring to is for price discovery. There will still be other functionalities that each exchange currently handles, including integration to client’s systems, data analytics etc.

While I don’t know all the details, I don’t think price discovery will be a such a complex piece of software that other exchanges cannot implement. Moat that IEX had was network effect that led to much better price discovery on IEX. It is not because of the software.

We need to see how the details will get worked out. Could buy bids from IEX be matched with sell bids from PXIL? If yes, each exchange will have only one leg of the trade. Not sure how exchanges can handle settlement in that case.

We will have to wait for implementation details to emerge.

5 Likes

Regarding IGX dilution → IEX will need to further dilute to bring down the holding to 25% over a period of time. No single entity can hold more than 25% in an exchange.

They will have to do either IPO or more strategic sales. The latter is helpful in brining sponsorship.

4 Likes

I read IEX’s explanation about market coupling, but honestly, it didn’t feel very convincing. Here’s why:

- With market coupling, exchanges will start competing more on fees than on volumes. This can lower overall margins. I also read that IEX usually charges higher fees than others, which might hurt them going forward. Management says it’s a very small portion of cost but it will still affect negatively.

- The management keeps saying their platform is better than others. But I couldn’t find any solid proof of that and in what sense it is superior. And even if their platform is good, I’m not sure that alone is enough to keep their customers from switching.

- I think it’s pretty clear that IEX will lose some market share. Since prices will be the same across all exchanges, IEX loses its edge as the most liquid platform.

- Lastly, there’s still a lot of uncertainty. Even the management didn’t seem sure about when and how market coupling will actually happen. That doesn’t build much confidence.

So overall, I feel it’s still early to take a strong position on this. Things are unclear and changing, so it’s probably better to wait and watch.

6 Likes

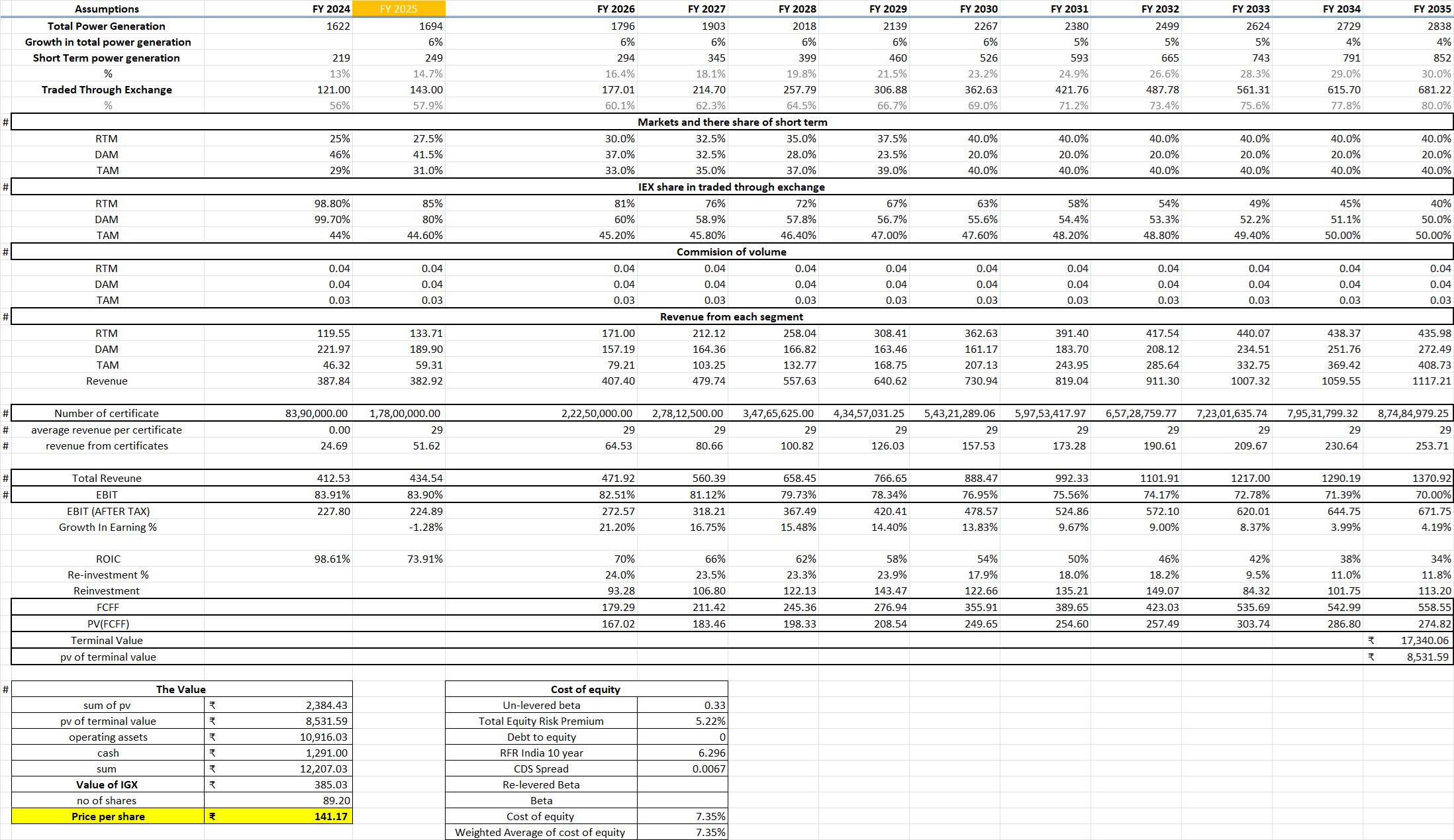

IEX Model.xlsx (57.5 KB)

My Assumptions

I expect total power generation to grow in India at 6% (Indian GDP growth) for the next 5 years, and then after that, the growth rate will decline to 4% till the 10th year.

The short-term power generation market would increase from the current 14.7% to 30% in 10 years because of the following:

- Because of climate change, it would be hard to predict weather and also power demand, which would increase peak power demand.

- Increase in renewable energy generation capacity, which is more variable.

- Expiration of old Power Purchase Agreements — this volume would come to exchanges because of cheaper electricity.

The volume traded through exchanges would also increase from 57.9% to 80% in 10 years on the back of:

- Lower prices on exchanges

- Increase in private participation as distributors, who are likely to purchase from exchanges

- Systems like (BESS) grid-scale batteries, which would get charged through exchanges

- Exchanges being more transparent

- Government push towards exchanges

On exchanges, the three major segments are RTM (Real-Time Market), DAM (Day-Ahead Market), and TAM (Term-Ahead Market). I believe that on the exchange, RTM and TAM would hold 40% market share each, and DAM — which is currently decreasing — would reach around 20% in the next 10 years.

Now, the big question is: what would be the market share of IEX after market coupling? It’s very hard to say anything about this because of the lack of clarity around the regulation itself, but I have still tried.

-

I believe IEX’s market share in the DAM segment would fall from the current 80% to 50% gradually in the coming 10 years.

-

In RTM, it would decrease to 40% from the current 98.80%, because this is one of the fastest-growing markets, and holding market share would be very tough in this segment.

-

TAM would not have an impact from market coupling because in this segment, it works on bilateral matching rather than liquidity matching.

-

The number of certificates would increase significantly as regulators tighten rules regarding renewable purchase obligations and other regulations, and more open-access consumers also want to improve their ESG score.

I have primarily focused on transaction fees, while ignoring membership fees and other business services, as they account for only a small portion of total revenue.

A pricing war is unlikely in the main segments because commissions are already capped by CERC, and a reduction may lead to a further reduction in the cap. They are also unlikely to get a revision of this upward for a long time, and because of inflation, it means a net reduction in the commission over 10 years.

Because of the increase in competition, margins would decrease from the current 83.90% to 70%.

ROIC would decrease because the company would need to reinvest a little higher than what it is currently doing to maintain earnings growth.

Terminal Assumptions

-

4% growth (long-term GDP growth after 10 years)

-

The required cost of equity, 7.35%, is calculated using CAPM and its inputs:

- Beta — industry average for finance (non-banking and insurance)

- Equity risk premium — implied equity risk premium

- Risk-free rate — 10-year India G-Sec

I have priced IGX at the current P/E multiple of IEX (26) and profit for FY25 of IGX ₹31 crore, which gives it a value of ₹814.37 crore, of which IEX owns around 47.28%.

Other optionalities like the International Carbon Exchange and the Coal Exchange are still too small to be added to the valuation.

I have also attached the model if anybody wants to run different assumptions

Disclosure: I am not SEBI registered. The information provided here is for educational purposes only. Consult your financial advisor before making any decisions. These posts neither advise nor endorse

7 Likes

I feel - this is quite a bearish case.

The market shares will remain the same by the end of FY26. Any hit in market share across segments will come in FY27 only. Given the pace of execution, that segment should be DAM only.

The hit to RTM should come in FY28 or later. Also, the Excel Model considers 85% RTM share and 80% DAM share in FY25. I think the market shares across these two were more than 90% in last fiscal year.

Post-coupling, all exchanges will see the same price; what differs is:

- Trading fees & rebate structures

- Tech stack speed, API friendliness, co-lo

- Settlement & credit flexibility

- Extra products (TAM, green, RECs, ancillary)

The other two exchanges are behind IEX. They do not have span of solutions what IEX has. It is hard for me to imagine people doing DAM trades on PXIL and coming to IEX for other solutions. The brands are less trusted along with their tech-stack. Hence, I would not predict a fall from 90%+ to 60% in the very first year.

Let’s think in another way.

If there is a small captive power plant that buys approximately 10 MW of electricity every day to fulfill its shortage.

In a month, they will buy 72,00,000 units.

Power price = 6 Rs per unit

Monthly expense = 4.32 Cr Rs

IEX fee is 0.04 Rs per unit. The overall IEX fee in this transaction is 2.9 Lac Rs in a month. The competing exchange can take 1.5 or 2 Lac fee on a 4.32 Cr transaction.

I feel that small players might not switch. Large industrial/C&I buyers & traders** will split orders to hit rebate thresholds across both exchanges.

4 Likes

I am trying to understand PTC India Short term trade as power trader in the market, I see that in recent time it has given ~30% volume to IEX . If I look at the PTC India con call they are not allowed to trade in HPX as they hold more than 5% equity holding. Basically management considering

- As of now holding its equity and it wish that it will be allowed trading trade - so basically volume is available in HPX too

- Market coupling that too management consider positive for the growth for HPX.

My understanding is as company confident to any of the above 2 option to play and benefit they are not considering selling its stack for time and make it qualify to sell on HPX.

Just wondering even in the case of market cupelling did not happen and gov allow PTC India to sell its volume in HPX will it not move considerable volume to other side of IEX market?

3 Likes

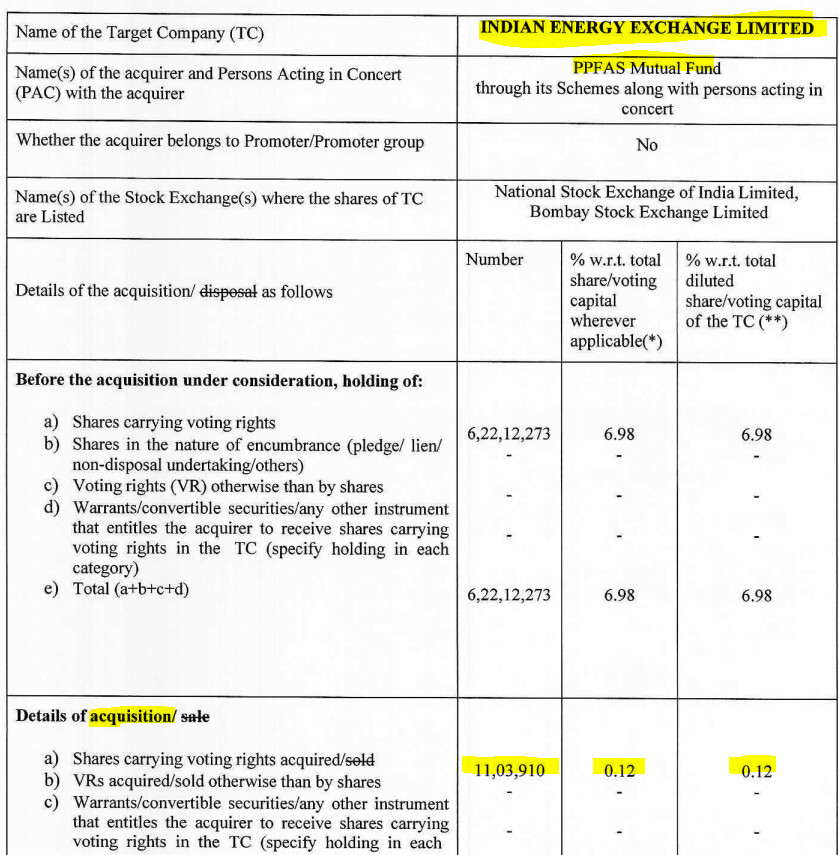

Parag Parikh Financial Advisory Services (PPFAS) raises holding to 7.1% in IEX

PPFAS Mutual Fund has recently increased their stake in Indian Energy Exchange (IEX) scrip.

-

Their holding went up from 6.98% to 7.10% as per the latest disclosure under SEBI’s SAST Regulation 29(2).

-

The purchase was done via the open market on 21st August 2025.

Now the curiosity part: What might they be seeing that perhaps the broader market is ignoring? ![]()

- Do they foresee structural tailwinds in India’s power trading market?

- Is it about long-term volumes shifting from bilateral PPAs to exchange trading?

- Or is it just opportunistic buying given current valuations?

Would love to hear the community’s thoughts on this move.

Source:

2 Likes

Even with this purchase their allocation to IEX in PPFAS Flexi cap won’t cross 1%. I would look more from that point of view rather than looking at 7.1% stake in IEX. In their unit holders meet earlier this month in Pune, there was a question on what they will do with IEX where Rajeev did not answer it specifically saying the July factsheet was not out yet and they did not want to pre-empt their portfolio transactions. It would be interesting to see if they will do any follow up purchases.

5 Likes

They cant buy beyond 10 percent stake right?

2 Likes