After a long time, the Indian defense sector seems to be abuzz with developments. Indian companies are trying hard to get a foothold into this lucrative space.

I wanted to start this thread to keep track of all the sectoral changes.

Overview of the Indian Defense Sector

India’s defence exports in the previous seven years have exceeded Rs. 85,000 crore (US$ 11 billion).

GOI changed the automatic route limit for FDI in the defence sector to 74%

GOI opened the defence sector for private participation

In 2021, Defence Acquisition Council (DAC) boosted the ‘Make in India’ initiative by according Acceptance of Necessity (AoN) — to capital acquisition proposals worth Rs. 7,965 crore (US$ 1.07 billion) — for modernisation and operational needs of armed forces.

GOI dedicated the seven defence public sector undertakings (PSUs) to improving functional autonomy, efficiency, growth potential and innovation in the defence sector.

Over the last five years, India has been ranked among the top importers of defence equipment.

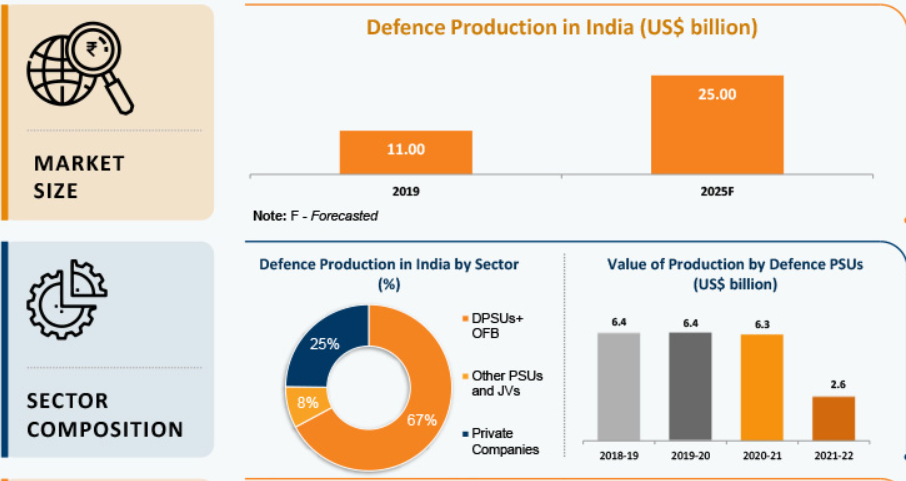

India’s defence manufacturing sector has been witnessing a CAGR of 3.9% between 2016 and 2020.

The Indian government has set the defence production target at US$ 25.00 billion by 2025.

Defence exports in the country witnessed strong growth in the last two years.

As of 2019, India ranked 19th in the list of top defence exporters in the world by exporting defence products to 42 countries.

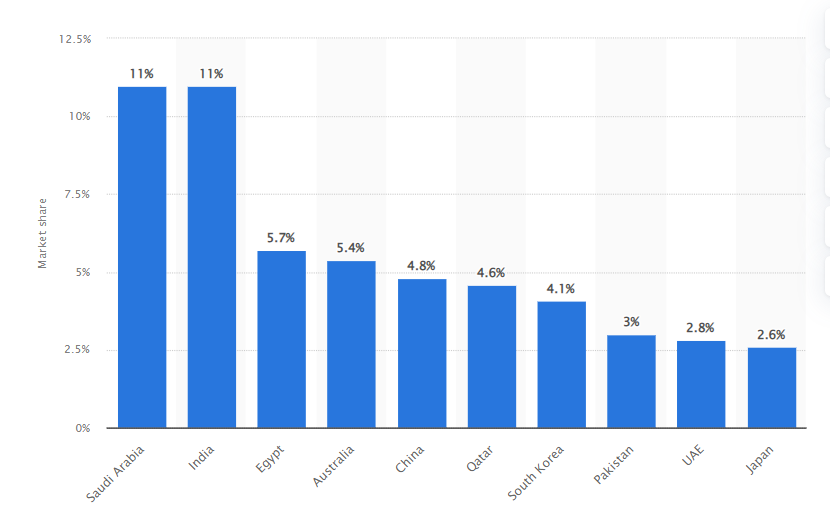

India and Saudi Arabia are the largest arms importers in the world.

The defence ministry estimates potential contracts worth ~Rs. 4 lakh crore (US$ 57.2 billion) for the domestic industry in the next 5-7 years (2025-2027).

The government formulated the ‘Defence Production and Export Promotion Policy 2020’ in defence manufacturing under the ‘Aatmanirbhar Bharat’ scheme.

The ministry aims to achieve a turnover of Rs. 1 lakh 75 thousand crores (US$ 25 billion), including export of Rs. 35 thousand crores (US$ 5 billion) in aerospace and defence goods and services by 2025.

The Indian government is focussing on innovative solutions to empower the country’s defence and security via ‘Innovations for Defence Excellence (iDEX)

Introduced Green Channel Status Policy (GCS) to promote and encourage private sector investments in defence production.

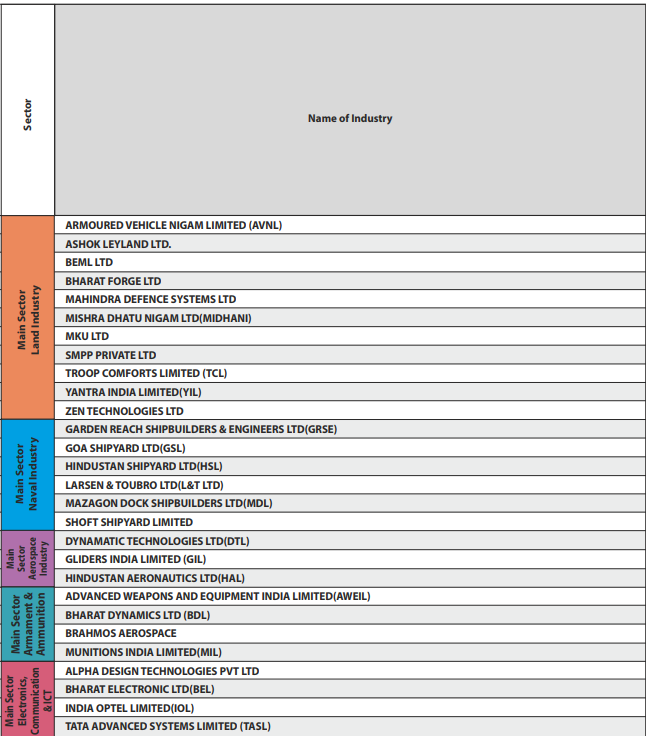

The Major players are; BHARAT EARTH MOVERS LIMITED (BEML), BHARAT ELECTRONICS (BEL), HINDUSTAN AERONAUTICS LIMITED (HAL).

BEML is stated as a manufacturer of rail coaches & spare parts and mining equipment in Bengaluru.

BEL engages in the manufacturing of specialised electronic equipment requirements of the Indian Defence Services.

HAL operates as an aerospace and defence company. The company uses international design, under licence, to build and assemble aircraft and engines.

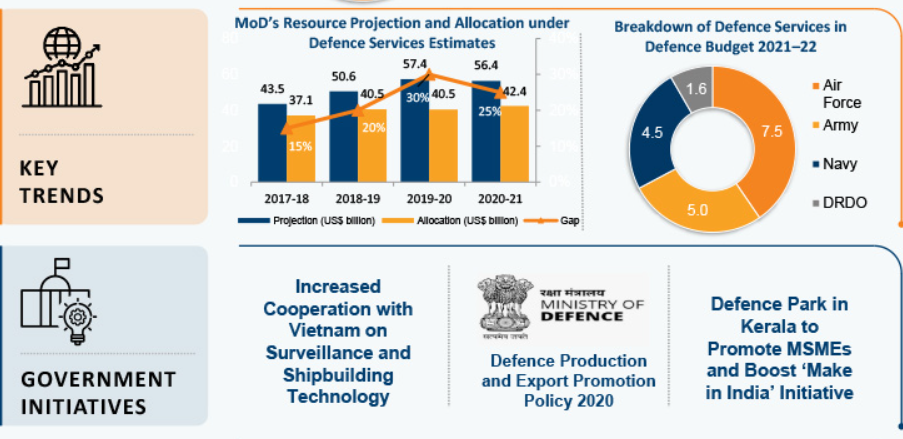

India’s Defence budget for FY 2022-23 stands at US$ 54.20 billion (Rs 4.05 lakh crores)

In 2020, India and the UAE have agreed to take their defence cooperation further through joint production and mutual trade.

This move is expected to boost domestic defence exports and achieve defence export targets worth US$ 5 billion in the next five years.

India plans to spend US$ 130 billion on military modernisation in the next five years and is also achieving self-reliance in defence production.

CHANGES IN THE DEFENCE SECTOR

The Defence Minister of India, Rajnath Singh, June 7, 2021, released an E-Book on 20 Defence Reforms in 2020.

India intends to become a global manufacturing hub for defence equipment.

87% of all defence acquisition approvals were from domestic vendors during 2020

The ministry decided to dispense with the requirement of the Integrity Pact Bank Guarantee (IPBG) to reduce the financial burden on the Indian defence industry, a move aimed at promoting domestic manufacturing.

Indian government clashes with foreign defence sector over offset demands.

The government has imposed penalties on several original equipment manufacturers from 2013 to 2021 for defaulting on their offset obligations.

50% of India’s offset obligations worth $13.52 billion across a set of 57 contracts have resulted in either penalties or the threat of them.

According to a research report released by defence think-tank Stockholm International Peace Research Institute (SIPRI), India’s military spending grew to US$ 76.6 billion in 2021, up 0.9% from 2020.

The UK and India signed a new defence cooperation pact and planned to finalise a free trade agreement by the end of 2022.

Defense spends were on the rise even before the Russia-Ukraine war. The war has shown the need for self-reliance and preparedness in defense.

In 2021 Iran’s military budget increased for the first time in four years, to $24.6 billion. Funding for the Islamic Revolutionary Guard Corps continued to grow in 2021—by 14 per cent compared with 2020—and accounted for 34 per cent of Iran’s total military spending.

Eight European North Atlantic Treaty Organization (NATO) members reached the Alliance’s target of spending 2 per cent or more of GDP on their armed forces in 2021. This is one fewer than in 2020 but up from two in 2014.

Nigeria raised its military spending by 56 per cent in 2021, to reach $4.5 billion. The rise came in response to numerous security challenges such as violent extremism and separatist insurgencies.

Germany —the third largest spender in Central and Western Europe—spent $56.0 billion on its military in 2021, or 1.3 per cent of its GDP. Military spending was 1.4 per cent lower compared with 2020 due to inflation.

In 2021 Qatar’s military spending was $11.6 billion, making it the fifth largest spender in the Middle East. Qatar’s military spending in 2021 was 434 per cent higher than in 2010, when the country last released spending data before 2021.

India ’s military spending of $76.6 billion ranked third highest in the world. This was up by 0.9 per cent from 2020 and by 33 per cent from 2012. In a push to strengthen the indigenous arms industry, 64 per cent of capital outlays in the military budget of 2021 were earmarked for acquisitions of domestically produced arms.

The most crucial project between DRDO and industry is the Advanced Towed Artillery Gun Systems (ATAGS). After years of effort by the Ordnance Factory Board (OFB), the project was handed over to private industry to develop the gun system designed by DRDO.

The ambitious project is the medium-altitude long-endurance unmanned aerial vehicle (MALE UAV). The indigenous drone will give India the capability to undertake credible Intelligence, Surveillance and Reconnaissance (ISR) activities

The DRDO is currently collaborating with a French original equipment manufacturer (OEM) for developing an aero engine for the advanced medium combat aircraft (AMCA) project which is under the Special Purpose Vehicle (SPV) norms.

DRDO has been successful in testing Hypersonic Technology Demonstrator Vehicle using the indigenously developed scramjet propulsion.

The DRDO is currently working on the scramjet engine required and the materials required to withstand the thermodynamic stresses in hypersonic vehicles.

A very good seasoned investor at a recent conference just gave the following names with a 1 line comment:

Defense: Next decade will be for such companies. Shortage of stocks in this space.

BEL

BDL

HAL

BEML

Midhani

Mazdock

GRSE

I personally own BEL, but will be looking closely at the rest of them.

The above page has such great valuable information esp. since the ‘lower cost research, development and production’ that India can provider to the favored national world can be amazing. This could be the start of a new ‘outsourcing world for India’.

Pls correct me if wrong, India itself imports most of its high end defence systems, equipments, technology - How can it become the export hub in this context?

Also, for defence, I dont think world will look for a cheaper destination - which has been one of the main reason for success of outsourcing in other sectors…

R&D is the biggest reason for companies to become big in this sector. R&D, innovation & cutting edge original tech…would be good to know which listed defence company in India is doing all this to support India and then rest of the world? Which company is making the best of the best available equipment/machine/tech etc.? Thanks

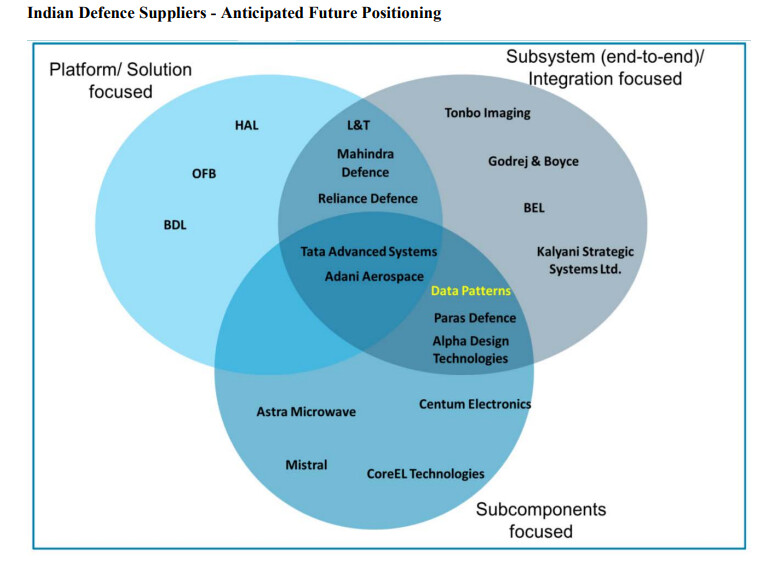

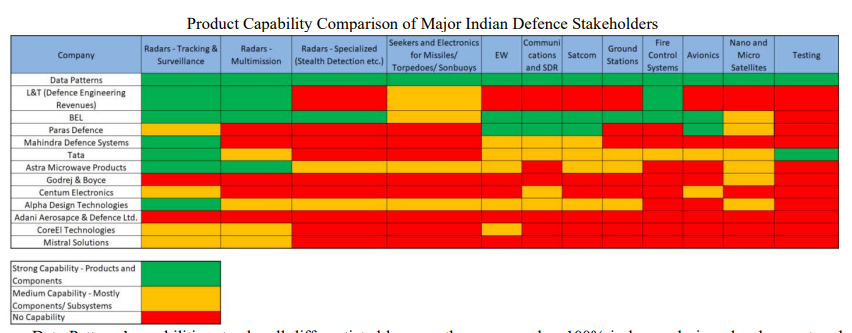

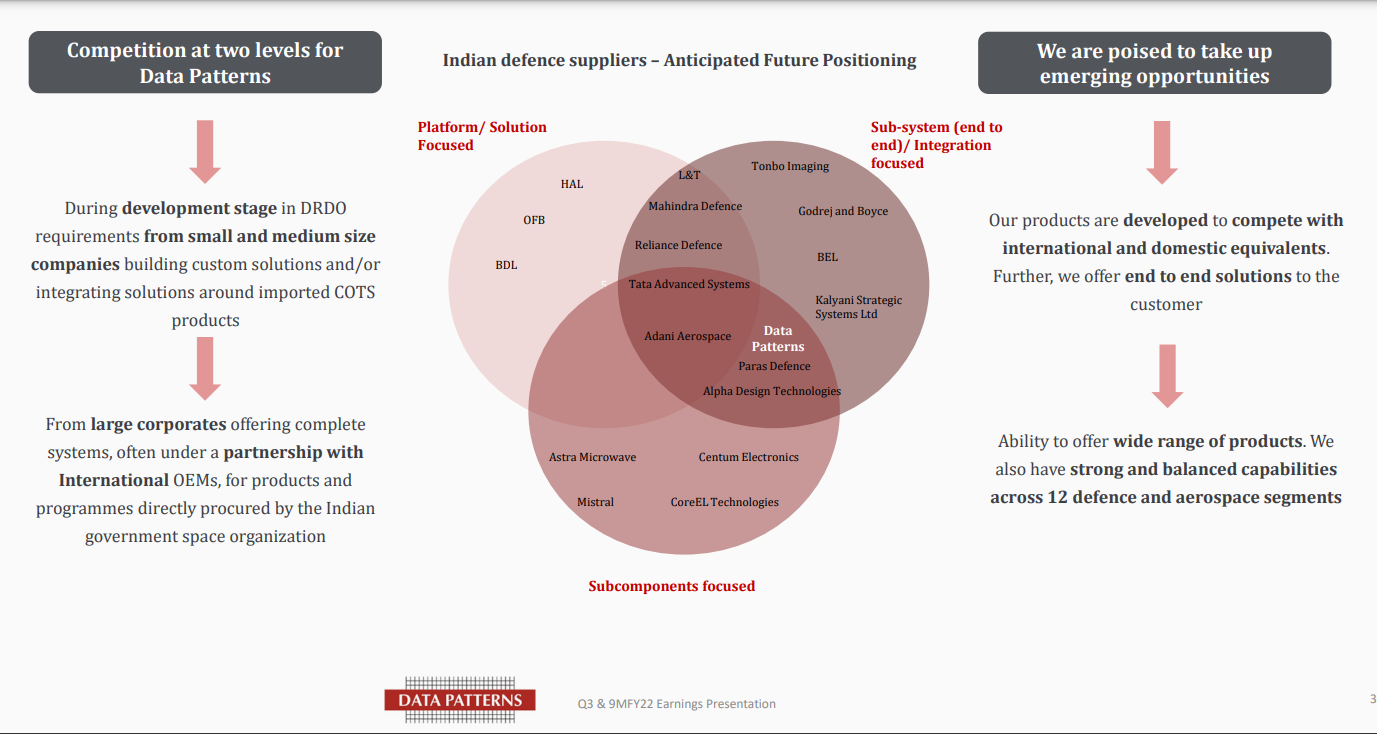

I have tried to do an analysis of listed companies on the basis of available information and segementation suggested by Data Patterns. Would welcome inputs or other views from others.

Category

Business Characteristics

Financial Features

Companies

Sub Components

* Requires high degree of specialisation/ experience

* High operating margins

Astra Microwave, Mistral, Centum Electronics, Core El, Paras Defense, Data Patterns, Alpha Design

* Depends on orders from Sub-system/ Platform companies

* Very high working capital requirement

* Requires continuous research on elerging tech or new platforms

* Cash Conversion cycle is unusually long

* One sub-system can fit multiple platforms / sub-systems with some customisation (like an automobile)

* ROCE is average on account of high working capital despite high margins

* Most of the players have zero competition in Indian context

Sub Systems

* Requires high degree of specialisation/ experience

* High operating margins

* Indian companies do not have requisite R&D budgets

Defence aquisition council (DAC) on 06/06/2022 accorded Acceptance of Necessity (AoN) for capital acquisition propositions of the armed forces amounting to Rs 76,390 Cr under Buy(Indian), Buy & Make(Indian) and Buy( Indian -IDDM) categories. This will provide boost to Indian defence industry and reduce foreign spending.

The DAC has accorded AoNs for manufacture of Dornier aircrafts and Su-30 MKI aero engines by Navratna CPSE M/s Hindustan Aeronautics ltd.

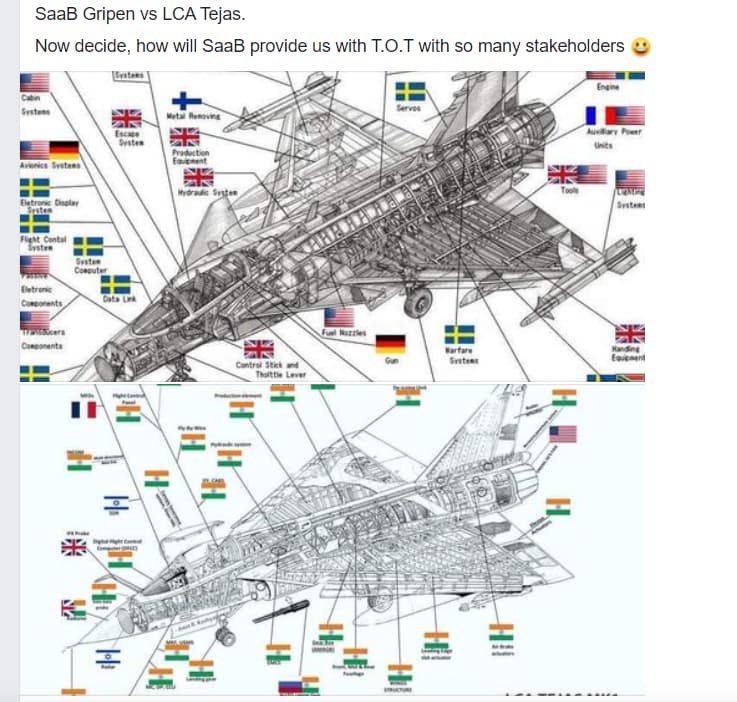

what is this about can you pls elaborate? The pic is not clear. whats the top picture and bottom picture? I see India flag at at many places in bottom pic but none in top pic…

I think the picture refers to Saab gripen aircraft compared to LCA Tejas fighter in terms of indigenous components. Sure a domestic manufacturing of a platform will always result in benefits to local companies in the long run as compared to just the cost of acquisition. In the Tejas example one has to look at share of value from indegenious components in the airplane rather just the number of parts. Overall that share will increase over a period of time as the volumes get delivered.

Image shows the complexities of defense Procurement Process. You can not simply go ahead and sell a product because it was assembled in your country you need to take approval from all the technology partners\stakeholders. That is where politics plays a big role. In case of SAAB Gripen with so many stakeholders any time situations can go wrong and your million dollar predator will be lying idle since supplier denied parts.

It is high time the government lets the private sector improve and develop the new generation fighter jets rather than rely on a single government corporation (HAL).

Look at how the US develops fighter jets via competition between Boeing, Northrop Grumman and Boing.