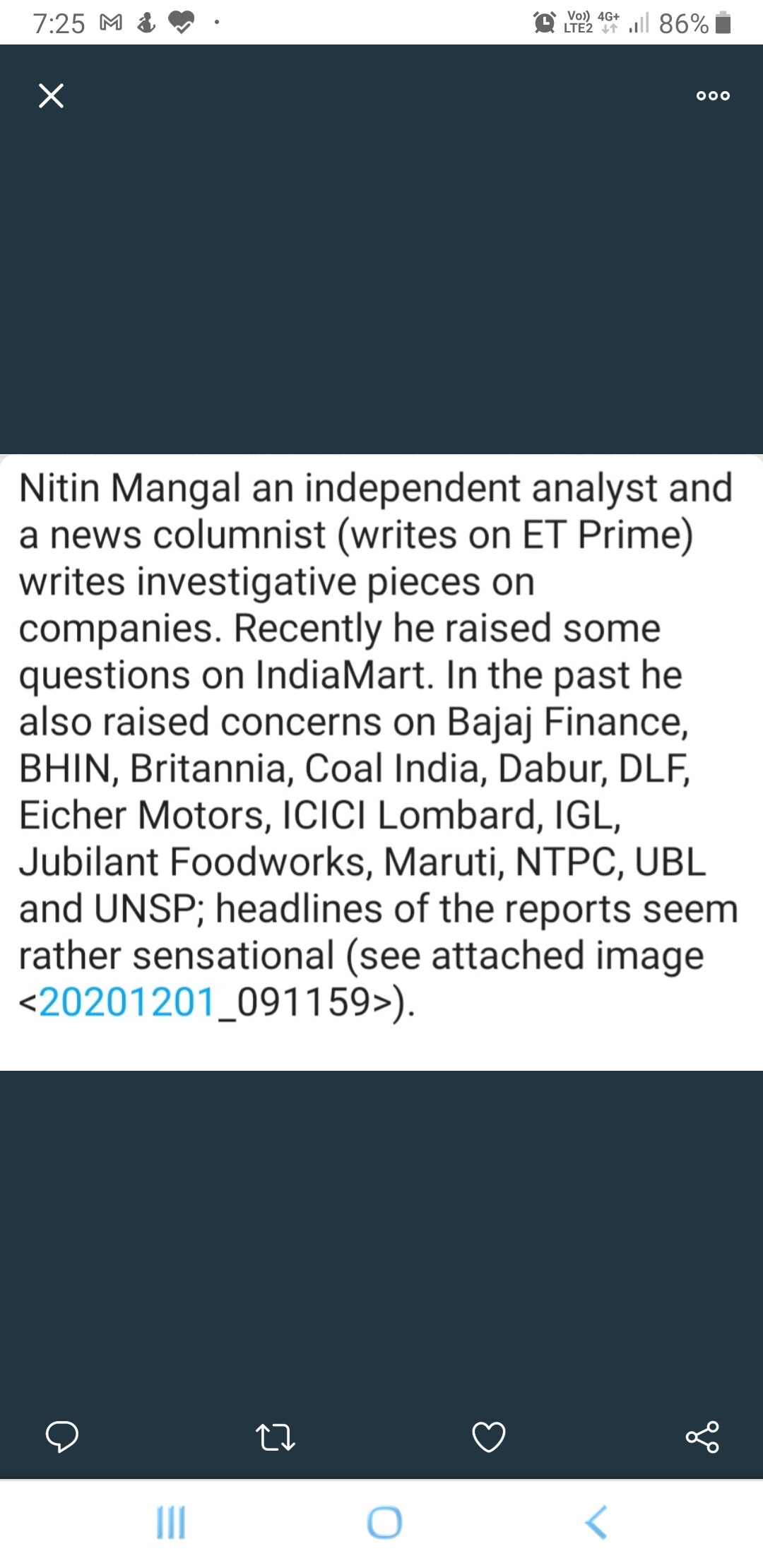

One of the comments in above tweet described author in a different light- if true pretty much sell a story type content. Quoted organizations are of some pedigree.

I am attaching a summary of the report Indiamart Report Summary by Nitin Mangal.pdf (299.3 KB) .

The table of contents, especially the appendix - “Screen shots of random questionable “Verified” profiles on found on IndiaMART” should give a good idea what Nitin has uncovered.

I have had a chance to speak with Nitin about this. What my discussion concluded was that there are good grounds to suspect that many of the verified suppliers on IndiaMart are spurious. He has put out such a list which includes marquee brands. For eg anyone can verify that and may also see suppliers such as Bajaj Finance Limited claiming to be ‘suppliers of water jars’ and so forth. It makes one wonder how can Bajaj Finance Limited be verified to sell water jars, and so on.

Further some transactions, as can be seen from ToC, are suspect according to his analysis. I have had a chance to discuss some in detail with him and as an analyst myself I concur with his conclusions.

Disc: no investments

2 Likes

Since I am invested, did some quick checks on few names mentioned in above post report link( bajaj fingerless, eicher…)…idea was to see authenticity if they are registered suppliers

In both cases GSTN is correct, brochure etc is correct - don’t see a scam part in these cases on quick look.

As is the case of each such marketplace platforms( flipkart/amazon/Alababa

of the world included) there are going to be scammers which use similar names/ images etc, while validation process of Indiamart can be under question like other platforms, this doesn’t make them fraudster.

Better Questions to be asked are what efforts Indiamart is putting in to protect buyer and sellers - pay with Indiamart addresses this partly where they address this fraudulent aspect https://help.indiamart.com/knowledge-base/payment-protection-buyer/

There are bound to be some takers of such investigative SEBI approved analyst, wonder what they stand to gain from such paid reports. Why not just go to Quora and read real life examples of being scammed on such platforms - fact is all of the marketplaces are full of such negative reviews across internet.

The interfaces may since have changed, which is why he took screenshots at the time they existed. I have seen many of those he mentions and can vouch for them. It appeared that the Trust seal had no meaning.

The above is just one piece in the analysis that includes various others including financial statements analysis. This is part of an a complete analysis to figure out an independent view of a true and fair picture of the firm and requires analytic/technical skills. Very few, even in this highly qualified forum possess them, and hence they are valued.

The job however, can be dirty because who wants to stand between an ‘investor’ and his fancy. But folks pay up for such intellectually independent analysis to know the gap between fancy and reality. It’s like a car enthusiast who had long set his eyes on a pre-owned Porsche 911 that’s come up for a rare sale. Before ponying up say ₹50 lakhs, he may add good sense to his dying desire by asking a top class mechanic to do a check and paid irrespective of whether you buy. Top money is worth it.

3 Likes

Firstly thank you @diffsoft for bringing this up and supporting with your own views/validation. Given your vast experience in markets, its a valid call out for many of us invested. Hope this is okay to challenge with a counter view , in the spirit of collaboration.

question is that this is this a process improvement and data validation aspects, similar problems exists on marketplaces. Shouldn’t we also acknowledge efforts taken by company to safeguard buyer/sellers?

Agree that most here lack tools and background to decipher every aspect of analysis. What about FII who have been increasing stake regularly - they do have resources and processes, right?

On a quick look of mentioned analyst LinkedIn profiles he has challenged stocks with pedigree for one or another reasons - don’t see analysis as wrong but most of them have done well. Seems points raised are mostly inefficiencies. Didn’t see him catching DHFL or yes banks of world.

If we question telemarketing practice of Bajaj finance - don’t know which NBFC is called quality.

If we see outages issue in HDFC Bank digital infra, that seem like an improvement area rather than revisit hypothesis.

This has always puzzled me to see most of VP seniors not participating in so called digital platforms threads here - its good to see some call outs on possible m8nor red flags - but are we missing forest for trees?

If market collective wisdom says some thing - its pointing in other direction, all digital platforms has been well rewarded by market - Naukri, Indiamart, Affle, Route. Naukri no doubt has a quality in diff league and rest of pack will have to earn market trust over period.

Agree that being vigilant is imp( esp at current valuations), missing out riding on digitization theme IMO is a missed opportunity.

Invested in all names above, booked profit periodically as well except Naukri.

3 Likes

You are welcome and I may not be able to respond to every query. I should also mention that I am not speaking for or on behalf of Nitin. He is a good friend, we talk and I can guarantee his integrity.

From your query I can infer that you are probably expecting an analyst report to be like a college project report. No. An analyst report is written with a certain goal in mind, for a certain audience (in this case his current and prospective subscribers), as an input to their decision making, with a certain analytic approach. The conclusions are probabilistic and tilt where the balance of evidence and analysis point to. He does not own the stock so he has not feelings for or against it.

Yeah they do have processes. They can be right, they can be wrong. They have been right and they have been wrong. Some FIIs may have bought it, some may have looked and rejected it and you will not know (quoting Taleb: Absence of evidence is not evidence of absence). Others may want to buy the stock and feel reassured that some of their favorite FIIs have bought it. That should not be a consideration for an independent analyst.

Stock can do well even if there are issues related to the business, or even if there is fraud. I don’t think you have to look far for that!

You don’t know. You may say that you haven’t seen him catching DHFLs and others, but others may have and you may not know about it.

Finally, I can PM you his email and you may email and talk to him. I just got into the conversation here because I just felt like standing up for him, knowing him. That’s all.

All the best with all your investments ![]()

4 Likes

IndiaMart Founder & CEO in another intrsting interview :

2 Likes

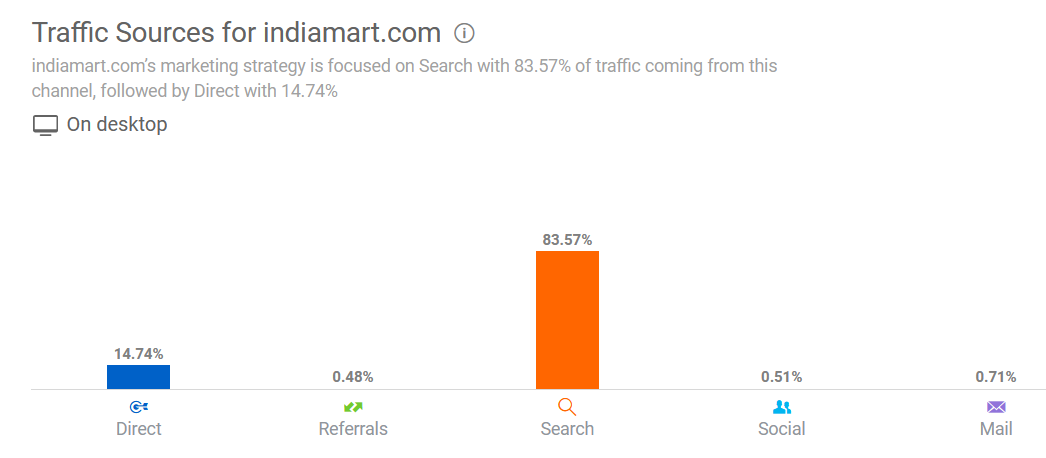

The demand seems to be largely driven by google search, hence demand side network effects do not seem as dominant. For a brand like amazon direct traffic is the main source of traffic which is a stronger proof of demand side network effects.

4 Likes

Just adding to your point, my interpretation could be wrong. Found few things in the DRHP, which every India mart Investor needs to know:

-

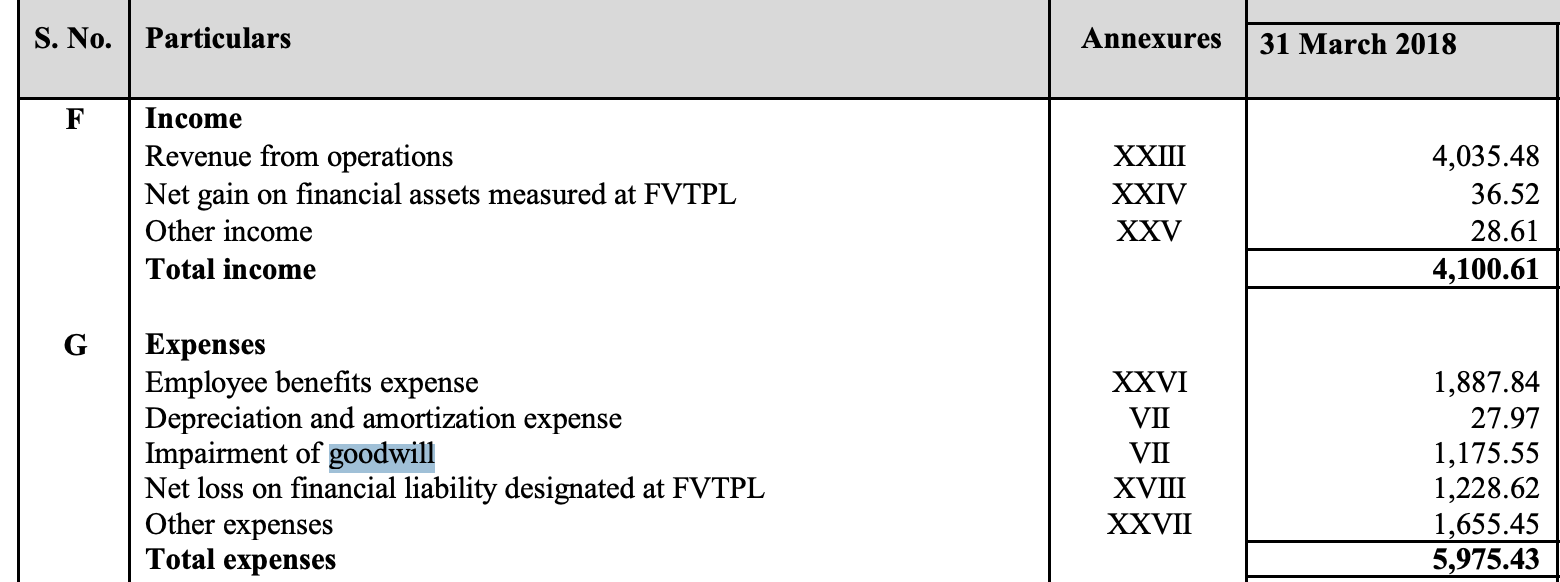

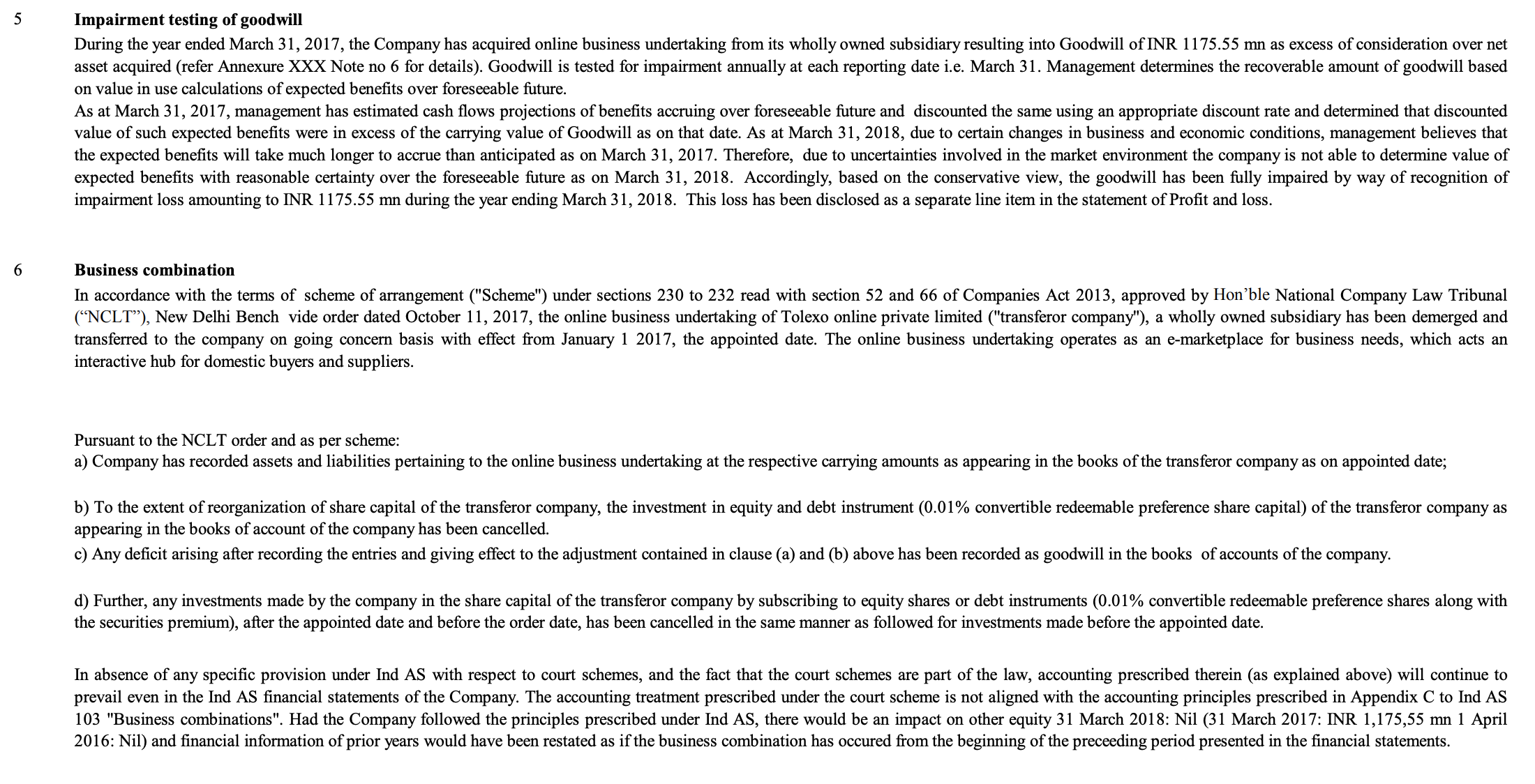

Impairment of goodwill worth 117 crores within 1 year of acquiring from its wholly owned subsidiary. Moreover, they haven’t given the key assumptions used in creating the goodwill (i.e discount rates, etc)

-

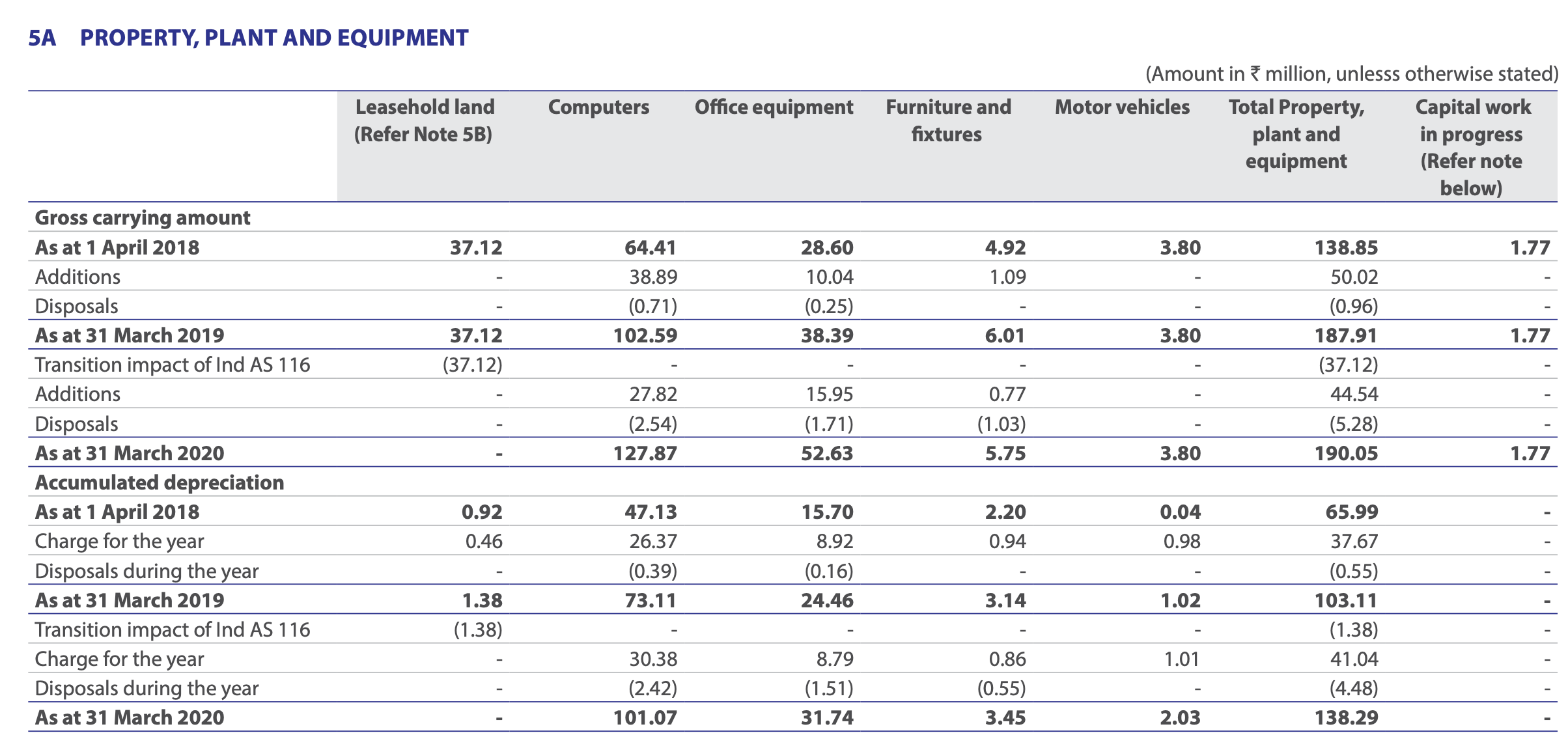

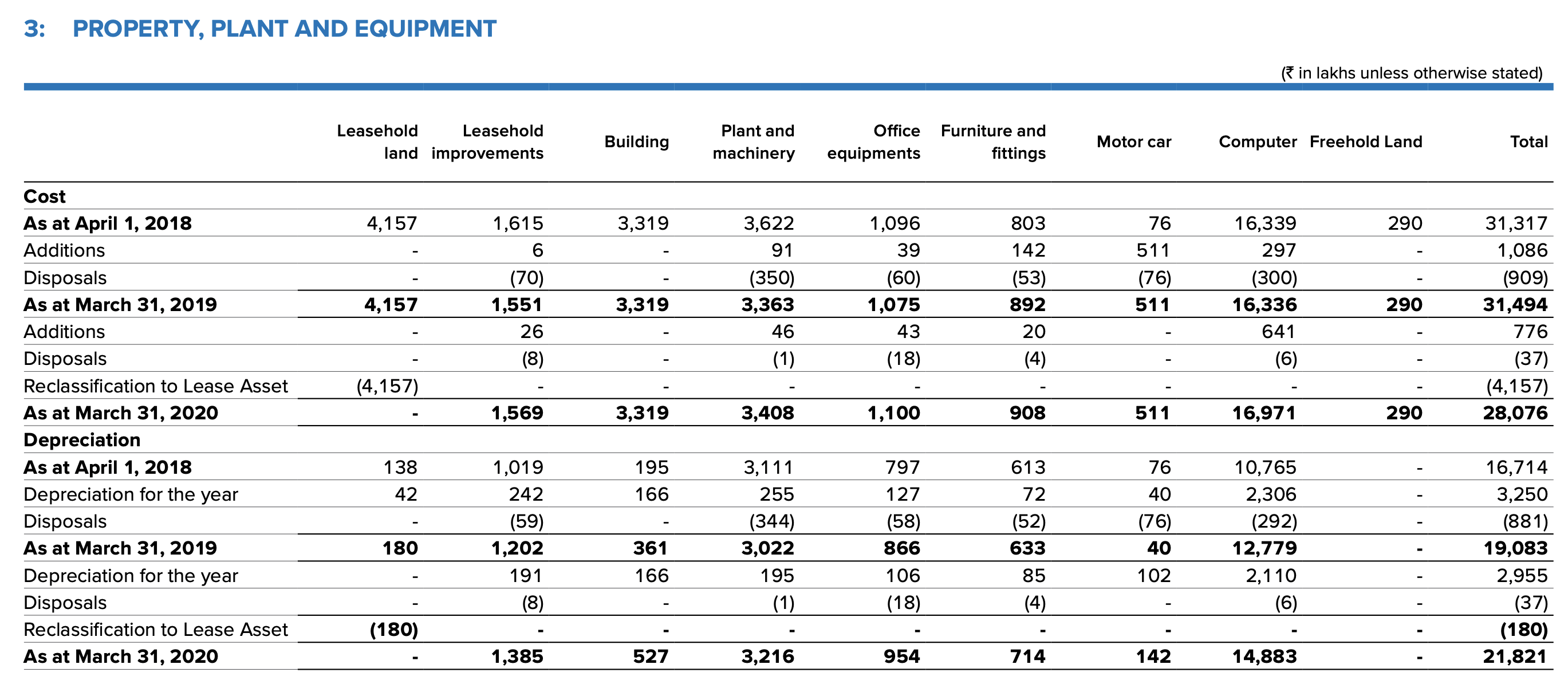

When compared to Just dial. India mart has a topline of 651 crores vs 800 crores for Justdial. However, when we look at the computers in gross block. India mart has computers worth 10 odd crores vs 148 crores for Justdial.

-

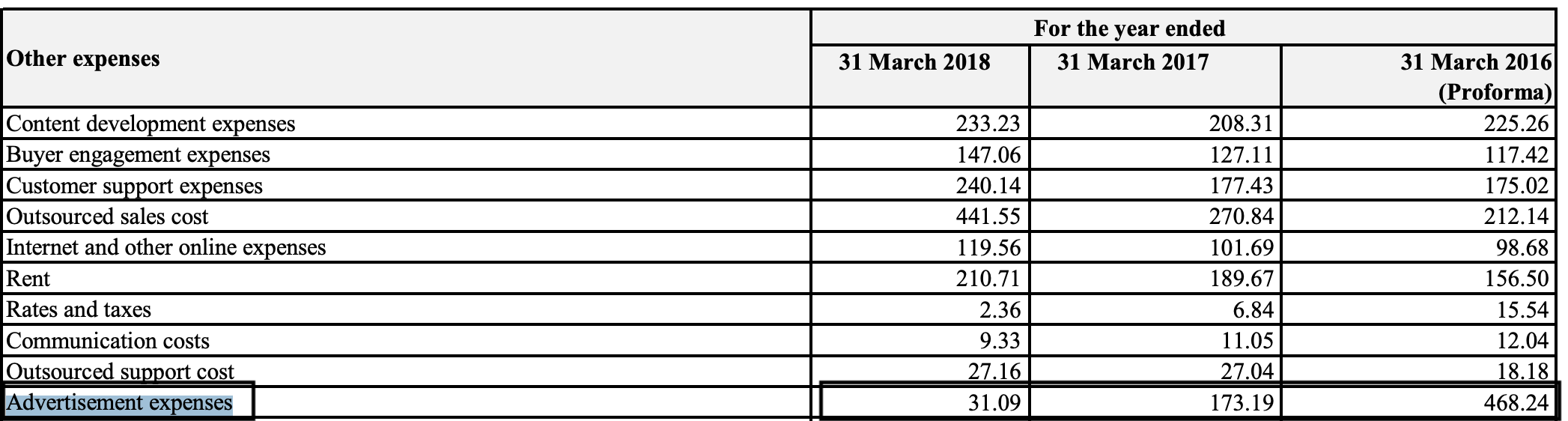

Profitability jumped close to IPO by reducing Advertisement expenses as a % of sales from 18.5% to 5.4%.

India Mart (Computers comparison with Justdial)

Justdial

Lets look at the impairment:

Reasons for impairment

Disclosure: Not invested. Just some food for thought. This is not a buy/sell recommendation.

7 Likes

Let me give some dessert for your thought

I am wondering if you have gone through the concalls and mgmt. talk before raising this hardware expense issue.

Two things - 1) they had hired Big B for branding which was discontinued subsequently. This led to sharp decline in marketing costs.

- They have stated on the concall that they mostly lease their hardware requirements rather than keep it on their own book. This is quite sensible since hardware specs keep changing and spending bulk amount on fast depreciating asset is not advisable. This is quite funny that you consider this an issue for Indiamart since it was a big red flag for potential investors in JD not too far back. Analysts have been flogging JD for splurging on hardware.

Disc: exited recently making 4-5x here and remains on my watchlist.

3 Likes

Excellent observations all @Worldlywiseinvestors

Saying I made an error of 117 crores (assuming figures are in ₹ million) for a firm of its size within a year of purchase is either poor judgment or very creative, even if the acquiree was a subsidiary.

On Computers, again the right place to look. Usually I tend to compare with a firm in the industry or close, who’s accounting I know is honest. For me it’s InfoEdge and a comparison show the same observation as yours. Also usually one should expect rise in Computers to closely linearly related to rise in permanent employees unlike other classes of asses like heavy machinery, land, office equipment and so on.

To be sure this should not lead one to jump to the conclusion that there is fraud, but lead the analyst to dig deeper and understand. It should arouse his curiousity and he will be rewarded with a superior understanding of the business.

3 Likes

Just wanted to clear up some information regarding use of Similarweb for insights. Just use it with a pinch of salt as these stats (free version) are not very accurate, especially for the Indian market. Some of the reasons are:

- The Traffic sources mentioned above is valid only for traffic originating in “desktop” and doesn’t include mobile, when in India, traffic sources are heavily skewed in favour of mobile due to smartphone revolution and cheap data boom last 4-5 years.

- Mobile usually contributes to more than 90% of traffic in most cases. Even conservatively, very rare to see desktop traffic cross 15-20% in India across genres.

- Indiamart also has more than 10 Million installs of their app on mobile ( source: https://play.google.com/store/apps/details?id=com.indiamart.m ) and thats a LOT for a primarily B2B app. This ensures a lot of traffic comes from mobile.

- The “visits” figure in Similarweb doesn’t refer to “unique user”. So, when the same user “visits” 3 times a month, its counted as 3 visits rather than 1 unique user. So 10 Million+ installs on app, plus heavy skew of mobile usage in India, means we can not use the “Desktop” data to make any generalisation regarding “direct” traffic vs “search traffic” for unique users (which is the stronger metric in digital).

- Even the “search” data, if you do a deep analysis of the keywords, you may find a larger chunk of them being “brand” keywords like “indiamart”, “india mart”, “indiamart login”, “indiamart seller”, “indianmart buyer” and so on. This means the searches are more “navigational” and no different than “direct” traffic as far as Indiamart’s brand strength is concerned. The web browsers have ensured users don’t type the full “www. xyz. com” anymore.

Even after all this, Indiamart ranks very very high in Google search results for its category. This itself is a huge MOAT, as it s very very tough to unseat rankings when one of the variables Google uses is “history” and Indiamart has a very good score. When your traffic is growing, and you have massive depth in your site across categories, and results are relevant to keywords, your ranking doesn’t change much unless you screw up big time.

Net net, I don’t think we can come to a conclusion that demand side network effects are not dominant.

In fact, it might be the opposite in the b2b category.

Now all that being said, the current share price of Indiamart at Rs 6000+ is making me feel dizzy.

Disc: I did ride the rally from 2000 to 4500 and exited as I felt it was very high.

6 Likes

Could explain the continual rerating.

3 Likes

The price has run up substantially over the past period. The stock has gone 2-2.25x over the last 6 months. The tailwinds looks solid, the buyer side traffic is up 40 percent year on year, the management still expects to add around 5k customers per quarter for the next 3-4 quarters which i believe is on a lower side(around a 15 percent growth). I expect the company to have a subscriber base of around 3lac by end of 2023. Also with operating efficiency kicking in and some increase in average revenue per customer, I expect the company to hit 600 crores PAT by end of FY 2022-2023. The stock is not cheap at current valuations and there is no reason for it to be especially with other internet plays backed by VC getting ridiculous valuations, a company with actual solid fundamentals and a sustainable business model should do well on the next 2-3 years. What the company does with 1000 crores+ cash is yet to be seen. Also the company should eventually move from providing additional services over and above (e.g. online payment, insurance etc) subscription models. Once this kicks in effectively(very tough to execute), the possibilities could be endless for the company. I am not looking to add at current valuations, but will add if I see exceptional growth either in subscriptions or introduction and effective implementation of newer services.

Disclosure - Invested at lower levels.

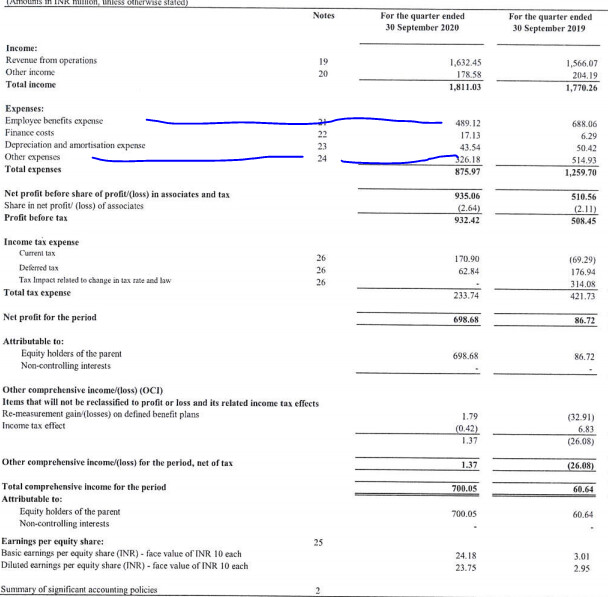

I was going through their September results, it seems employee benefit expenses and other expenses have gone down considerably and the drop in these two is contributing to much better net profit.

I was checking EPF portal for Indiamart, I see higher EPF deposited for July/Aug months in 2020 than previous years which means salaries should be more than previous year. Please shed some light on what has lead to lower employee cost and other expenses.

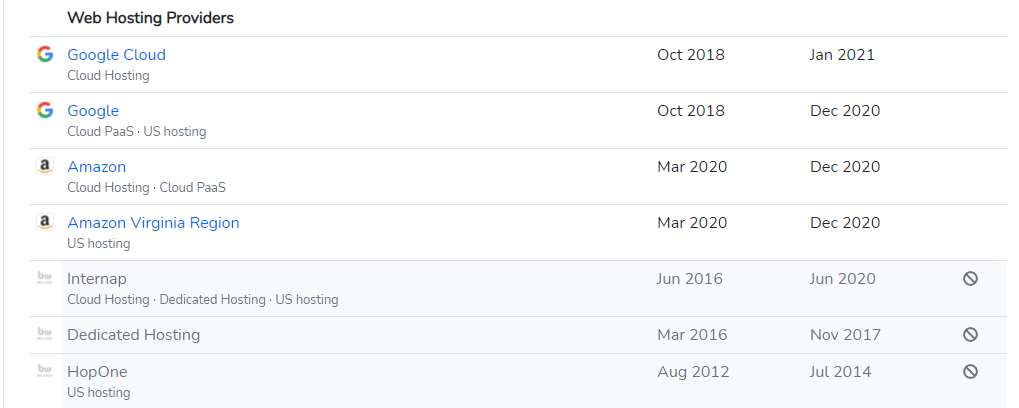

Another question I have is around the infra structure they use to host to online content? Do they use a cloud service like AWS or Azure or do they have in-house setup? I could not get any information around this in their AR as well.

2 Likes

Indiamart is using Google Cloud and AWS for hosting as you can see from below screenshot. I have captured the same from Builtwith.com which gives relevant information about any website

4 Likes

Lower other expenses - savings driven by overheads and travel etc, if not all, some of it should come back.

Employee benefit exp - sizable pool is sales folks - lot of payout which is linked to sales is commissions, likely to be less in current scenarios, also flexi arrangements on call centers ( contract/ outsourced ops) staffing would have been optimized.

For a non seasonal platform biz sequential qoq would be a better way to look at - emp exp has been reducing over each quarter prior to covid as well ( mid 40 in FY19 to 39% by mar 20 , covid has made them accelerate it to 30% currently and thus operating leverage is playing out well, as expected from a platform biz.

4 Likes

Indiamart planning to raise funds through issuance of equity shares or other securities convertible into or exchangeable into Equity Shares or non-convertible debt instruments along with warrants or any combination thereof by way of Preferential Allotment, issuance of American Depository Receipts (“ADRs”), Global Depository Receipts (“GDRs”) or Foreign Currency Convertible Bonds (“FCCBs”), Qualified Institutional Placements (QIPs) or through any other permissible mode or any combination thereof, subject to applicable laws and necessary shareholder/ regulatory approvals, as applicable.

1 Like

Interesting development. But what is the need for the company to raise funds? The QIP will be sharply lower than the current market price and the company has over 1000 crores in cash and doesn’t require a lot of capital for the current business to sustain. An acquisition opportunity maybe ?

When stock becomes expensive it makes sense to raise some money and keep for bad times irrespective of whether you need it or not.

11 Likes