B2C and B2B are completely different businesses. I dont see Whatsapp being a competition to IndiaMart.

I also saw messages that JustDial app is more user friendly compared to IndiaMart. My view is UI and technology are just enablers - what is important is the ability to get more RFQs for the sellers and more options for the buyers. Network effect will play major role here and first movers have advantage.

Below is summary of my analysis:

The company’s Business Model is good. It’s a Platform Business and good scope for expansion.

Balance Sheet is average (They are increasing Equity Capital, Total Debt to Net Worth is more, but D/E is less)

P&L and Cash Flows look good.

Ratios looks OK. The Du Pont of ROE shows the Leverage Component is more, this is a negative.

It has some MOAT and time will decide if MOAT gets stronger or weaker.

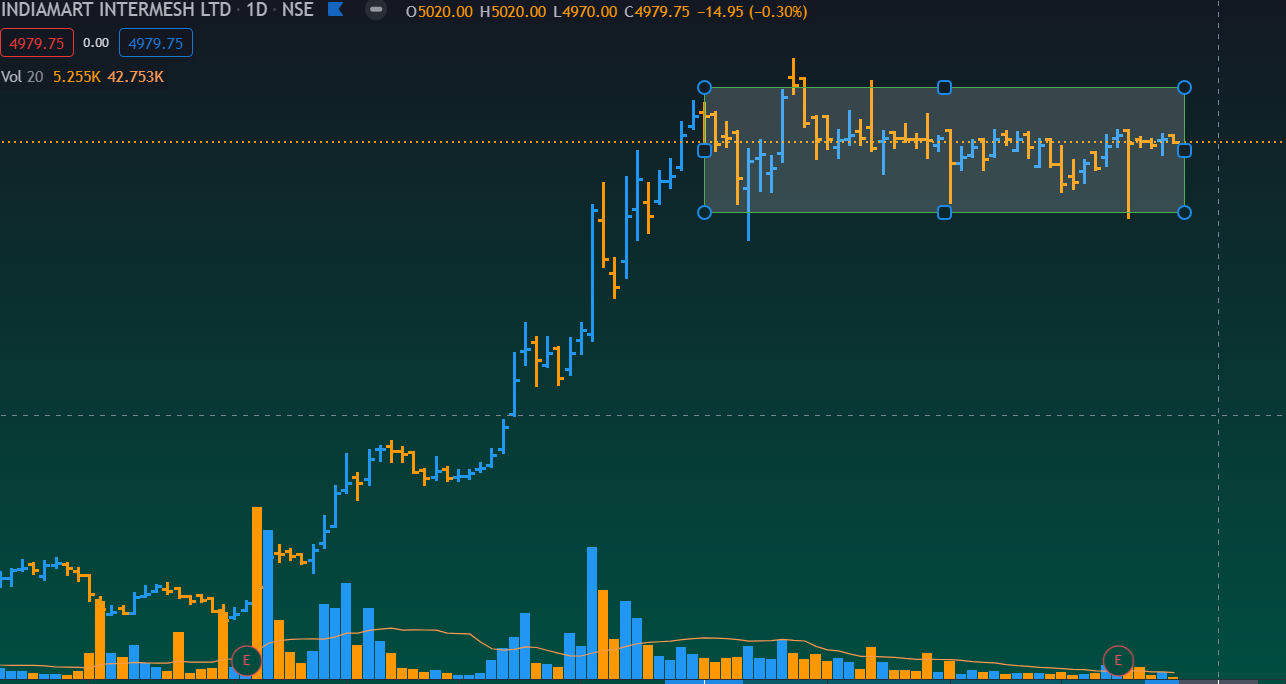

Technically i am seeing the stock is in Distribution/Correction phase.

I read through all the posts on this thread and thanks for the research.

One thing i am not confident about is the current Valuations (current CMP is 3x-4x on DCF, Dhando). I know these are not correct valuation methodologies for this kind of Business

Any one did Valuations on this Company. Can you share your Insights?

Is Just Dial catching up with Indiamart B2B business ? Any Scuttlebutt news (in field) regarding just dial entering into this segment ? Is is a threat to Indiamart?

This is actually more detrimental to JD, if Indiamart can place barriers to entry in this industry it will be great news for IndiaMart in the future. Regardless, the management believes that JD’s entry will expand the market and considering I have little to no faith in JD:s management I don’t believe they are a genuine threat to IndiaMart.

Broad data view , there is some merit in threat and looking at Indiamart performance, it was bound to attract competitors

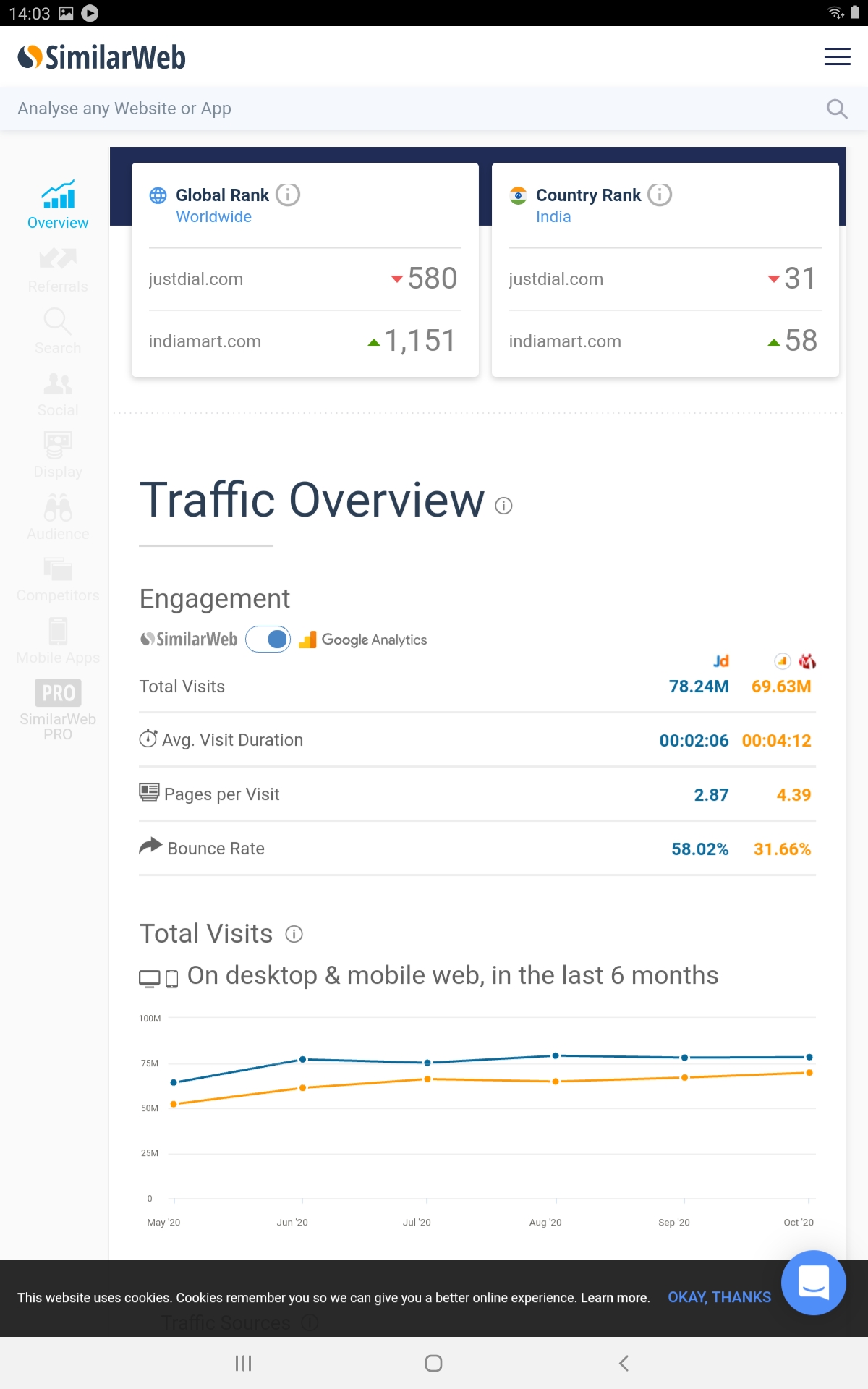

1 Traffic volume is similar range( quality likely to differ)

2 JD bounce rate is way higher than indiamart, implies indiamart is more relevant to traffic/visitors

3. Time/pages spent is higher on Indiamart - again higher relevance

I was trying to understand Indiamart’s moat and I was not able to pinpoint towards which one of the following was the actual moat for the company:

I have seen countless comments stating the most of the online platform companies cater to the B2C segment and Indiamart does not have a threat as it is a B2B platform. So does this mean that Indiamart’s moat is the nature of the business segment (B2B) itself which makes it unappealing for new comers to enter (i.e a high barrier to entry), and the moat will get eroded once a company has enough interest/resources to enter the B2B segment?

The B2B segment does not have a high entry barrier but Indiamart has created a moat for itself due to its first mover advantage and a substantially high market share. This will indicate that the moat will be eroded only when a competitor with better service/costing/innovation enters the B2B segment and starts taking market share.

The subscription based model ensures that Indiamart is able to make customers pay in advance and ensure customer retention in spite of new competitors entering the market.

I came up with the above 3 points for moat based on my observation. I may be wrong and the moat could be something else entirely.

Hence, I would really appreciate it if someone could shine more light on the moat of the company.

You missed the most import of all NETWORK EFFECT

Sellers know that the consumers are in IndiaMart, thus more sellers onbaord IndiaMart.

The same goes on for consumers, they know the sellers are in IndiaMart platform, thus more consumers onboard the platform. ba dum tss there goes the biggest moat!

From what I understand, Indiamart’s moat is the network it has created between the consumers and sellers.

But that raises another question in my mind…If a new player enters the B2B segment (let us assume its Just Dial), all Just Dial needs to do to break Indiamart’s hold is to create a parallel network by offering better services/lowering the cost of services. Wont that create a cash guzzling competition of ‘who grabs more market share’? Isn’t this the same problem that has plagued most of the online platforms e.g. Ola vs Uber, Zomato vs Swiggy?

In the scenario Just Dial does create its own network, has Indiamart placed any safeguards in place which will insulate it from the threat of new competitors, apart from lawsuits?

I also have a follow up question in regard to the B2B segment…is the B2B segment large enough to accommodate multiple large players or is it a zero sum game?

Please correct me if my understanding is incorrect on any of the points.

Amazon vs Flipkart, Zomato Vs Swiggy etc etc…all needs big pockets is what I understand. A second player wanting to grab market share offers discount by virtue of Investor’s/Promtor’s/company’s money and the defendant does same.

Point is, does JD have financial muscle or interested investor to put that money? Insights welcome on this front.

Good interview covering customer additions and impact of Covid, sustainable cost rationalization, cash utilization, tech investments, near term and future growth rates.

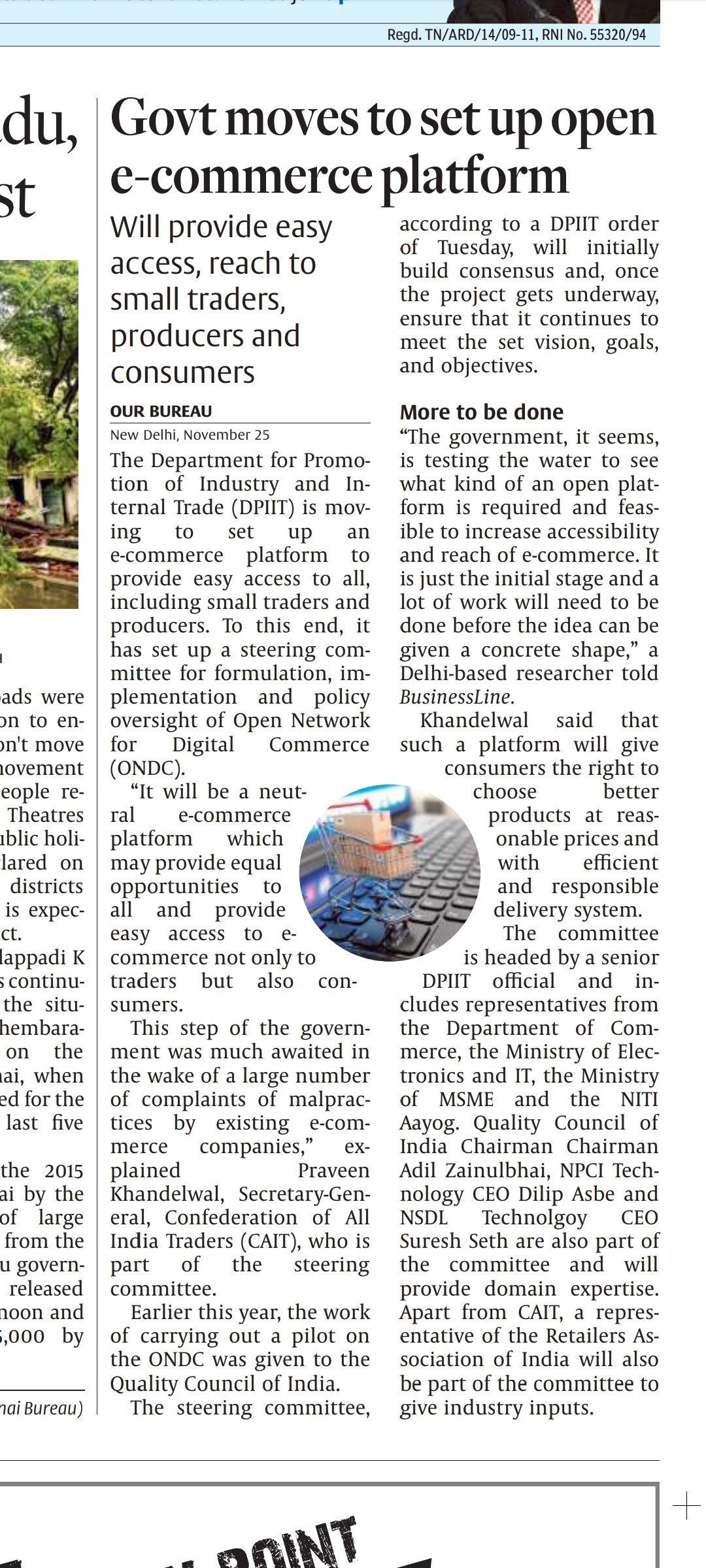

It will be a neutral ecommerce platform which

may provide equal opportunities to all and provide easy access to e- commerce not only to traders but also consumers.

On opportunity size - 4-5 million potential B2B customers ( half of GST registered businesses being B2B), they currently have 1.4L paying base - appprox 4% mkt share. Overall Registered suppliers are much much higher - which is needed for network effect.

At 5000 paying customers addition per quarter - revenue addition will be similar to last few qtr patterns i.e. 8-12 cr incremental revenue, given operating leverage, bottomline impact will be 5-8 cr per qtr. We are yet to add higher revenue per customer in mix - out of 140K+ base, which will add further upside to revenue and bottomline.

Company generated 260 cr cash last year, yearly addition likely for each year at 20- 30% / year( revenue increase at 15-20% per year - 3/4 by new paying customers and rest by other levers).

what does one pays for 300cr cash generation, growing at 20-30%/ yr.?

Next few years as base increases, other revenue streams will open up as well and, ARPU inching up will add meaningfully as well.

Mkt participants seem to be not fully trusting in potential of such platforms and longevity they have.

Can you please shed more light on the point you made on the longevity of such platforms?

I am a complete novice in this sector and I am trying to understand how Indiamart’s market position will be in 5 or 10 years down the line. Especially with competitors such as Justdial or Udaan coming up in the B2B space.

Could Indiamart be dragged into a fight with these competitors which might affect the cash generation potential? or does Indiamart have a strong moat in place which makes it immune to any new competition?

The thread has lot of material on Indiamart market segment vs other players such as Udaan, both have been around for sometime and growing while co-existing as their target segment are not at conflict yet. Indiamart presentation and annual report will give good idea on mkt potential and runway.

JD is going to try and have a direct competition, let’s see how this pans out, IMO

Jd is late to party, though have been around for long

Court cases in such tends to drag long , look at FMCG guys - they tend to have such fights now and then. Its a noise and distraction.

Mkt size is big and as of now network effect and platform characteristics are demonstrated by Indiamart , any incumbent is yet to make a big dent.

Naukri has seen many forms of competition come and go but has been able to retain leadership consistently.

Next few qtrs should tell us If Indiamart is able to fortify and strengthen its position and exploit digitization wave. As of now my money is riding with them.