However I think, IndiaMart is already making an effort in this regard, if we consider this article :

Though it talks much about PayTm, but it also have comments from IndiaMart Mgmt. which I guess has a meaning.

Disc : Invested.

However I think, IndiaMart is already making an effort in this regard, if we consider this article :

Though it talks much about PayTm, but it also have comments from IndiaMart Mgmt. which I guess has a meaning.

Disc : Invested.

Google, Amazon, FB etc. are primarily B2C focused. They are after customer behavior as much as selling the products on the platforms. I doubt if any of them will get in to B2B in a serious way.

VC backed players like Udaan or another start up in B2B market place could become competitor to IndiaMart. Having first mover advantage, network effect should play in favor of IndiaMART. We have to see how well they can use it to defend themselves against emerging competition.

Disc- Invested.

Hello everyone,

I have a couple of questions regarding the future market potential of Indiamart:

In regard to the step taken by Google, I have seen a lot of posts which claim that Google, Amazon etc. focus primarily on B2C and hence do not pose a threat to Indiamart which is a B2B. Although I agree with the point regarding Amazon focusing on B2C, aren’t we all making an early conclusion that Google will also go only B2C? Mr. Pichai’s tweet mentions helping retailers selling to consumers. Could the consumers also be businesses? Please correct me if I am wrong.

As an addition to the earlier question, will Indiamart always have this persistent threat of “a tech giant swooping in and putting you out of business” over their heads?

In the region where I stay (Mumbai-Pune) I have come across TV channels such as Zee Marathi and Radio stations such as Radio Mirchi promote their own B2B/B2C markets. I am not sure if the same has been done in other parts of the country. I know these ventures are much smaller in size compared to Indiamart. But as these players have an exposure to a larger audience through media, could they become a larger threat to Indiamart down the line by taking away atleast some of the market share?

Disc: Not invested but interested (Feel that the current valuations are sky high  )

)

Hi,

I feel both the questions you asked are very valid and we should try to find out more information about this.

There is always a threat of a tech giant swooping into this market. Like you said, right now it would be too premature to assume that it can never happen. However, I do not see any such threat visible in the near term simply because this seems a whole different arena than the arena they are currently playing in. Amazon has spent years mastering consumer logistics. The logistics to deliver a phone and the logistics to deliver 10,000 bottle caps are completely different. There are too many niches in this segment and the unit economics would be incredibly difficult. This is the reason Indiamart too exited this model and focused on subscription model. I have not seen Amazon do anything similar in US or any other country. I would assume they would try this model in their home market first rather than directly in a country like India. Even if they ever do plan to start something, it would be more on the lines of what Udaan is doing(Finished goods) than what Indiamart does.

Indiamart’s unique advantage is the wide variety of products available on its website. To a normal individual it is hard to fathom the number of raw materials to make a finished good. Around 200 raw materials are required just to make a tyre. It will be extremely difficult for a new entrant to replicate the sheer breadth of products.

Disclosure - Invested and hence views might be biased.

IndiaMart denies investment/acquisition by the TATA group.

Though I dont see the competition from JustDial, as a major one.

Though the move is interesting though :

Did you check out JDMart app’s demo video (link)?

Somehow I feel it has a much better interface (UI) vs. IndiaMART app.

Given relatively stark valuation difference between the two (IndiaMART trades at 70-80 PE while Just Dial trades at 12 PE), things can become interesting for Just Dial if they’re able to take some market share in coming years.

This will be indeed a real life, real time, interesting case study to understand durability of network effects. Network effects postulates that, as more people join a particular network, the value of the network for the users grow exponentially. After a critical mass and momentum is gained, it is very difficult to dislodge the incumbent and exhibits winner takes all kind of characteristics. Most famous example being Facebook. It will be interesting to see how this pans out for Indiamart and JD.

JD has been a B2C company till now. While they have the data of many small businesses, it is to be seen how successful they will be in a B2B model.

It will be interesting to see how IndiaMart will respond to this.

IMHO JD spread itself too thin trying to do everything. Usually this is a winner take it all business beyond a critical mass due to the network effects. It would be one thing to have the b2b as another segment and quite another feat to be successfull at it.

At this pace company should do atleast Rs104 EPS in the current year. So stock is at 48x P/E FY21E v/s Route Mobile at 43x FY21E if it delivers Rs120crs PAT in FY21E. Affle seems more expensive at 90x plus. Comparing the 3 because they are all internet/mobile plays

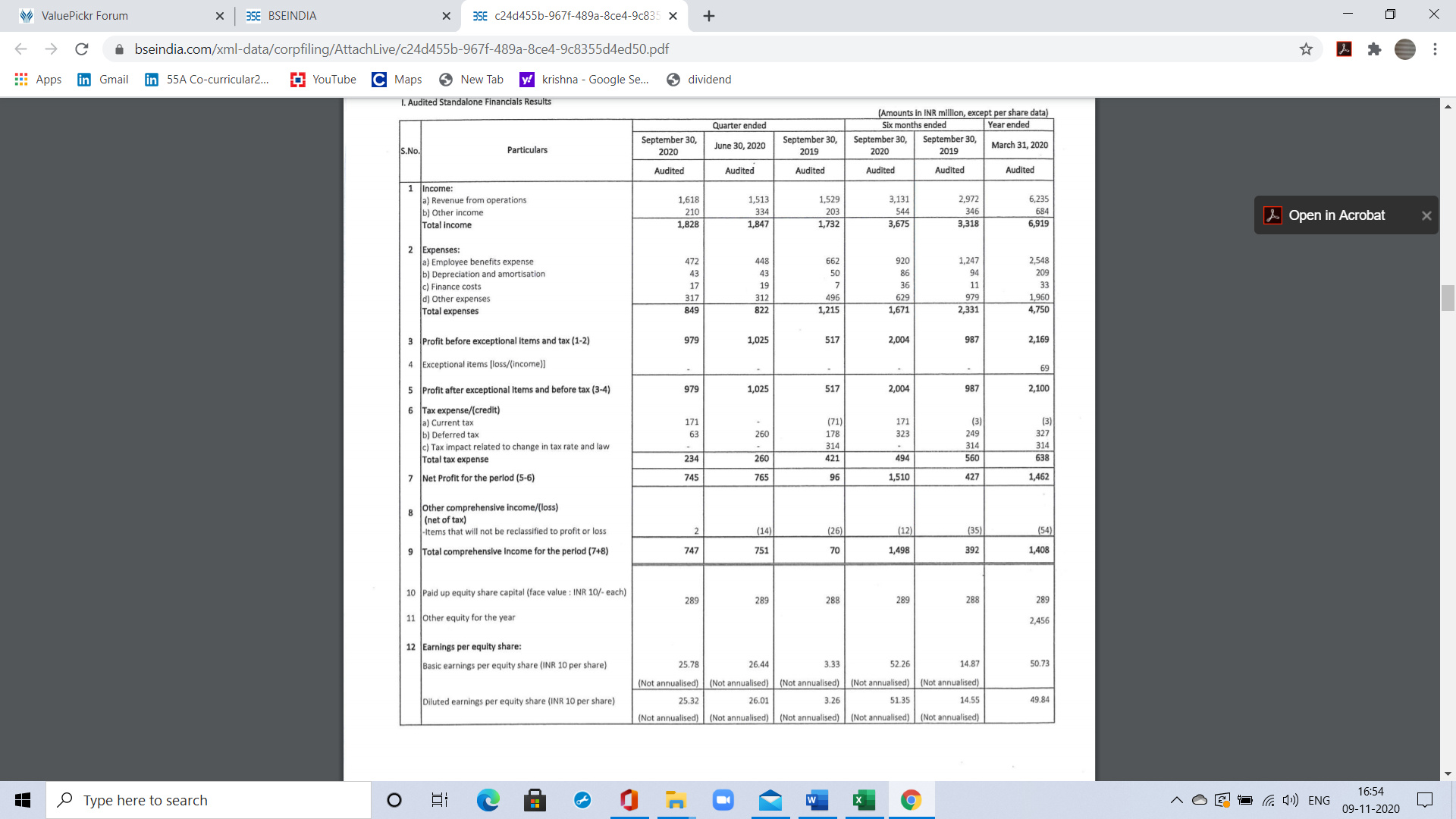

Strong operating performance. Number of paying subscribers have risen to 141k from 133k at the end of June 30 which is far ahead of what i estimated. The company should surpass March 2020 numbers of total subscribers at 147k and should start growing at around an 17-19 percent pre-covid rate for the next couple of years buoyed by covid induced faster implementation of digitalization play. Collection from customers (new) has risen 71 percent from June quarter and is only a 7 percent drop from September 2019 numbers. The company has cash on books of around 1045 crores or around 7 percent of market cap for organic or inorganic growth. Great margins and cost rationalizations by the company. The company is still not attractively valued enough for me to add in my portfolio but it still going to be one of the strong operating performers in the next 8 quarters. More clarity on outlook will be clearer after concall but have nothing to complaint.

Why top line growth so low ? Just asking…an idea…hardly 4%

You need to understand how revenue is calculated. So since the business is a negative working capital business it takes revenue for the entire period. So there are 2 revenues one is deferred revenue (so a 2 year subscription for a client will flow through 8 quarters despite getting paid before start of service) and one is collection from customers which are new customers. So deferred revenue is already received and will flow, now what one needs to look is collection from customers. Collection from customers has been very robust this quarter, a collection of 163 crores Vs 94 crores in the previous quarter and slightly lower 173 crores in comparable period. So basically companies topline has recovered from covid impact and bottom line has been boosted due to cost control measures by the management, half of which should be permanent taking into account last concall.

Seems company has recovered some what from covid impact. If by next quarter company gets 150K paid subscriber, it will be in uptrend in business.

Overall IMO results are good. Next quarter will give better visibility.

reduction in opex is though commendable.

I understand , platform business has 2 revenue components

| Name | Role | Qualification | Salary (Cr) |

|---|---|---|---|

| MR. dIneSH CHandRa aGaRwaL | Founder Chairman and CEO | BE | 4.6188924 |

| MR. BRIJeSH KuMaR aGRawaL | Whole Time Director | MBA | 3.3465 |

| MR. dHRuV PRaKaSH | Non Exec Director | PGDM IIM,A | 0.068 |

| MS. eLIZaBeTH LuCY CHaPMan | Independent Director | CFA | 0.06 |

| MR. VIVeK naRaYan GouR | Independent Director | BE, MBA | 0.025 |

| MR. RaJeSH SawHneY | Independent Director | BE and ME | 0.056 |

| MR. dIneSH GuLaTI | COO | BE, MBA | 8.24 |

| MR. PRaTeeK CHandRa | CFO | CA | 0.5276 |

| MR. aMaRIndeR SInGH dHaLIwaL | CPO | BE (Textile), PGDM IIMA | 2.83 |

| MR. ManoJ BHaRGaVa | Senior VP (Legal and Secretarial) | LLB, LLM | 1.021 |

| Sudhir Gupta | Senior VP | CA | 2.063 |

| Vikas Aggarwal | National Head | 1.81 | |

| Parag Agarawal | Senior Vice President | 1.625 | |

| Vikas Deep Verma | Senior Vice President | 1.385 | |

| Devendra Singh | Senior Vice President | 1.353 | |

| Vivek Agrawal | Senior Vice President | 1.328 | |

| Sunil Parolia | Senior Vice President | 1.11 | |

| Abhishek Bhartia | Senior Vice President | 1.076 | |

| Amit Jain | Senior Vice President | 1.06 | |

| Sumit Maheshwari | Chief Human Resources Officer | 1.026 | |

| Total | 34.6289924 | ||

| %PAT (147 cr as of FY20) | 23% |

Management Salary is 23% of PAT. This is pretty high and a possible RED Flag. Other members, please share your thoughts

Its not management salary as % of profits, it promoter family as a % of profits. Please recalculate using salaries of the agarwal family (dont include agrawal)

OK Considering only Dinesh, Brijesh, Parag (Share holder 0.74). I am not considering Parag Agarawal, Vivek Agrawal since they don’t hold shares, the Calculation is 7% which is OK for a mid cap

From my understanding, this seems to be more of a B2C move.

Currently, WhatsApp might not be able to provide a platform for businesses to reach multiple customers as IndiaMart does. But considering WhatsApp’s overall reach throughout the country, it might be able to help businesses get more customers organically through word of mouth. Could that be a threat to IndiaMart’s business model, or a portion of its revenue at the very least?