Disclaimer:- Firstly I have invested handsome amount in IndiaMART so can be biased.

The whole model till date was that IndiaMART have clients that are hard to get and have seen leads and have also listed them and made them able to be there only place so they were looking like a monopoly in many aspects and made barrier that are becoming very easy to break that was one of the few things that I personally was very skeptical about at first that yes it is hard to register and have leads etc but with internet boom is it really that hard china have already seen such event taking place in ecom etc with alibaba not with there b2b but with there ecommerce market place, this made this barrier to be much easier to break with good promotion and huge cash to burn.

Then the real change happen they become profitable and seeing margins that can even rise more seeing there model this made me wonder can they do upper pushing that they might be doing but can be accelerated and also make them a monopoly at the same time.

This can easily be done by one thing that is called as proprietary software and by just not being the only a marketplace but a whole system and be there pattern from there accounting to shipping and that was very hard to get and also much harder to develop.

Then there investment in other come and that is the real upsell and also a moat that is hard to breach that is now a competitor not only need them to be having similar in number but also to get them they need to convince them to change there way of buisness as now proprietory software and other services come into play that make switching cost so high that it make no sense and make them to stick with they and also take higher packages and also be more integrated player.

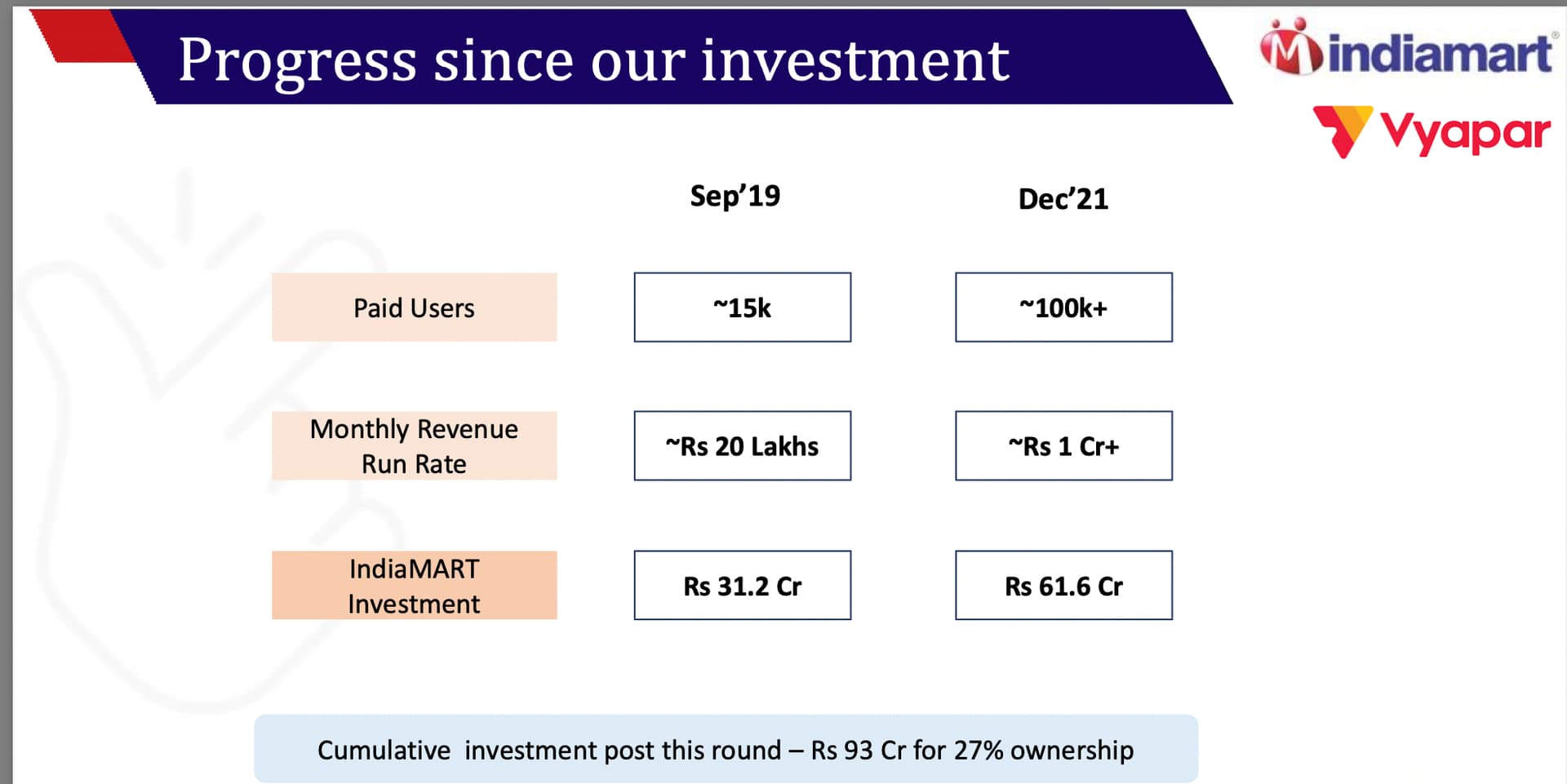

Just see there last 2 year Buying in other companies either taking a good stake or acquiring a majority or even compete takeover this is indicating this only.

For example

M1 exchange msme discount and invoice software.

Easy e com :- inventory management system saas company.

Agillos e-com:- saas for inventory procurement.

Truckhall:- market place for trucks and logistics.

Legnisty services:- saas to manage legal workflow.

For some it may look they like to invest in saas and tech company but what these all have in common these can be seen as value added services and be made into any b2b business.

Just see many things like logistics,legal work, inventory procurement and even management is important and that make this a valuable addition

IndiaMART is trying to move towards one-stop-shop for SME businesses, rather than being just a discovery platform. Ideally these should increase customer stickiness while generating additional revenue. We have to see how it will play out in the coming years.

The key monitorable will be the number of paying customers and revenue per customer.

I agree with your point they are not only sme but even export market also as this if become a place for all indian b2b buisness then it can easily diverse into export also as we have also seen it invest in many logistics company also.

It can play out and both management track record and there action are doing good and to a great suprise they are also acquiring stake or wholly own at very reasonable valuation also.

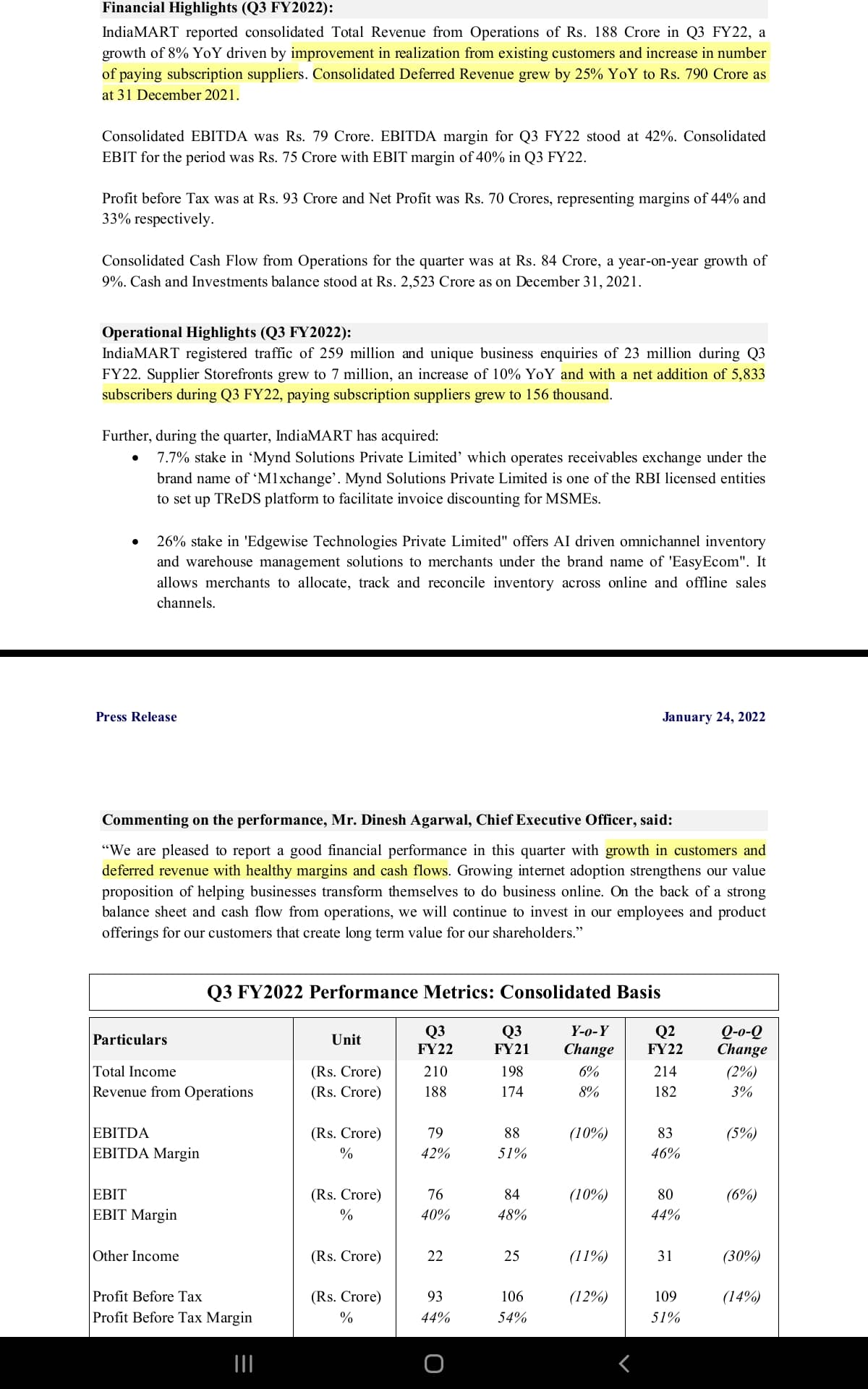

Nos look flattish on face value, however key metrics of Deferred revenue, collection, paid subscriber additions seems healthy.

Given this is a proxy play on MSME digitization - doubt mkt was expecting good growth given in sector given stress in sector , as long as future trajectory looks good, hopefully things should stabilize and look up. Many small size investments and cash pile should help to grow aggressively as MSME sector comes out of Corona impact.( though they are not a hyper scale biz model, have a huge runway, a near Monopoly, a 20-25% trajectory is needed to get market excited)

Need to hear mgmt commentary in concall to get better idea. Been an opportunity cost in last year or so and Technically looking weak on charts.

Profitable growth - They continue to grow at slower pace, but highly profitable with excellent return ratios. This is important in the long run. I personally like businesses that produce profit and convert profit to cash.

Gradual increase in paying subscribers - Rather than throwing freebies, management is intent on increasing paying subscriber base, though at a gradual pace. There is a long runway here.

Working capital efficient - Collects money in advance from customers

Conservative revenue recognition - Has good backlog of advance revenue which will can cover a few quarters at current run rate.

Timely raising of capital - A bit debatable as a management skill, I like that management raised money at high valuation helping existing shareholders.

The question of course is valuation. From P/E of ~100 it has come down to ~50. In my view, IndiaMART is a 15-20% topline grower, potentially for a significantly long time. Would the markets continue to give 50+ P/E to a 15% grower is the elephant in the room. Interestingly right now Justdial is valued higher on P/E basis.

I invested at much lower levels and continue to hold for now. Current beating of high P/E stocks and a news letter from Monarch AIF on the risk to the high P/E stocks has got me to start thinking…

Does anyone have information on how the customer churn rate is looking now? Pre-COVID used to be around 20%, and there was a report in November that said it was a “few notches higher than the pre COVID levels”

I was invested in this, but got out 3 qtrs back when during two concalls the challenge of growth was outlaid by promoters very subtly - total available GST registered suppliers vs what they have on their platform etc. So I booked profits thinking will re-enter later.

Recently as part of browsing through my Smartkarma account, I came across analyst report published by Nitin Mangal who has developed forensic audit specialization. While report is paid one, summary is available free to read. And it does not sound very exciting:

I am clearly not able to understand the massive decline in price, though I entered in the lvls of 6k

and want to average, but really not able to make up mind

though conviction is still intact

I think overallQ3 results are not very impressive but also does not warrant such kind of price action. The deferred revenue has shown good yoy growth, company is finally getting aggressive with big acquisitions around ecosystem, under penetrated market. Thinking of increasing my allocation on this decline

If we look over this we can see in the whole system of deferred revenue so the real impact and the real impact and real positive goes time to time and is mostly delayed.

This is due to there model that is Deferred revenue so new users may change over time that was seen why during covid there growth was massive so the covid impact on Balance sheet will last longer but rise will be more sudden also.

The pain of employees migh last long but there saas play might turn out good

There monopoly in saas b2b based can be a massive gainer.

I am personally seeing that they have handed mostly all handling to billing etc but the next step might be into b2b lending partnership

I went through the above discussion & I also slept over my thoughts on taking an unbiased view.

We have seen most of the things which are currently negative about the business. This looks like a beautiful SELL side story.

On the contrary, if I want to look at the positives nothing concrete comes to my mind besides investments in startups which may or may not yield us the kind of returns we expect. I am not able to build a Buy-side story for myself.

Having said that I again went through all my notes & certain other discussions on various platforms.

@The_Seeker has talked about Nitin Mangal though I could not get the paid report however, I was able to find out this interesting video which gave me Goosebumps. (I may be biased because I am a subscriber to this channel).

Sales growth was less than 10 qoq and profit was less qoq, cannot have for 50+ PE companies. Managed to escape 15% lower circit. Story is intact but facing headwinds.

Post Covid, expenses will go back to what they were, plus salaries have increased, these will be a drag on margins.

*Number of customers will increase at the rate of 6000 odd (per quarter, I guess). As customer gets older revenue per customer increases (interesting).

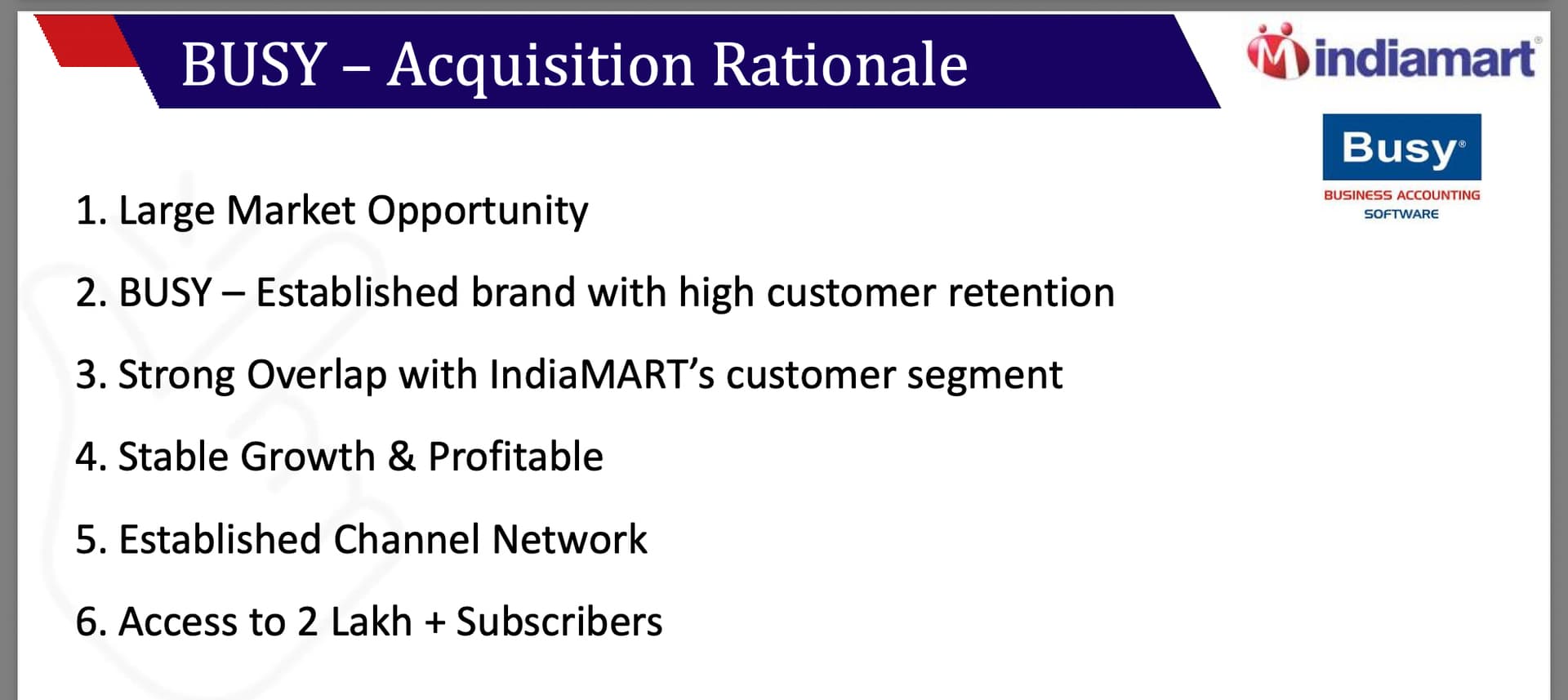

*Busy acquisition. Aim is to increase its reach, currently only North India. Its a robust product, 25 years old company. Great opportunity to cross sell. Aims 40% growth. Currently 42Cr sales.

The problem with IndiaMart is the huge expectation mismatch between what the market expects and what the management is content with.

The whole thesis behind re-rating of IndiaMart in FY21 – was that the pandemic and ensuing lockdowns will force SMEs to jump on to the online bandwagon. Perhaps 5 years of potential “SME digitization” would happen in one year. This assumption took the stock from sub-Rs.2000 level to Rs.9000 plus.

But the assumption was belied, the SMEs never came in droves and IndiaMart’s numbers actually went down. Paying suppliers dipped in FY21 and IndiaMart called out ‘stress on the SME sector’ for the same. In other words, the analyst community completely misread the SMEs.

Ordinarily one would expect the stock price to get hammered back on this realization. But it sustained – in the hope that sooner or later the pandemics & lockdowns would end and the SMEs would rush in. Q3 FY22 was as normal a quarter as normal could be. The second waive had subsided and everyone was back on to the streets. But the SMEs are in no hurry to rush in! Not beyond the same 5 or 6,000-odd-per-quarter range, not much different than before. And all these days, the management did nothing much to pull them in, like a big ad spend, discount schemes, freebies, branding or something else. The management seems content with their baby-steps growth.

When one looks at the macro size of the SME opportunity, these numbers are miniscule. But that is the analysts’ problem, IndiaMart doesn’t care ! It is surprising the expectations mismatch continued for so long. Based on stock exchange disclosures, the management has frequent meets with analysts and fund managers. Yet, the analysts couldn’t read them? I am surprised.

I see that you are invested in the stock and I like your comments in various threads so I think you really understand this business and have realistic expectations hence wanted to get your views on above few points -

To a layman like me, 5000-6000 new SMEs per Q additions sounds like a really big, decent number and good growth…more so if these are paid additions!

Can you pls let me know why this is not considered good growth by analysts?

With such good numbers addition, does management need to do anything else…if they start adding in lacs, can they handle it?

Someone mentioned that Indiamart has a SaaS component…do you also believe Indiamart to be a SaaS product…I am just trying to understand that are all websites/platforms a SaaS product? (that is if the customers need to pay for using it?)

What difference do you see with advent of RIL into similar business with acquisition of JD…have you tracked JD mart’s growth as its competitor?

Apart from being in business since 25 years, what moat would Indiamart have to compete with others with big pockets entering this area?

Only I can notice on this front is: First mover advantage. and also To replicate business by any new entrant or exising guys…not that much easy…and more over they developed software to include other products like vypar etc…it is not that much easy …example: Alibaba…Everyone know…what they do…no one able to replicate that same alibaba from past 10 yrs…

I may be wrong in my thoughts correct me…if any where I am wrong.