Please don’t make assumptions, the aspect was just to understand the stock and not play any kind of blame game etc.

We don’t know if analysts or HNI investors or FIIs or whoever took up prices. Does that matter and should we care? The only aspect important is that was there exuberance or not - and seems there was. Thats what I meant by my point.

All due respect for everyone in the investing ecosystem. This moreover includes people who analyse and put in a lot of effort to understand fundamentals - a lot of the information is great to consume. I wouldn’t go even as far as mentioning someone’s folly - if invested in Indiamart since 2019 - would that be a folly? Anyways - no point in debating a point which has no consequence to the business view/analysis.

On the Indiamart point - yes the company is still richly valued and yes cost cutting has been done. My point was that they way it was done - and the fact that it was done - and profit was doubled in a drastically difficult year - was very impressive. I specifically mentioned that I was impressed with the capital allocation and the prudence. The fact that anyone can do that is pretty random as I think companies should be judged on what they do. My question was purely on if it would be prudent for Indiamart to keep investing on marketing when the entire SME ecosystem was shaken.

Again - my view here would be I am not as sure considering past track record! If you are, great, no issues.

That is precisely the view I was trying to question. Investors will stay away is again too generic. My premise was will earnings be affected - and I was trying to judge that. Maybe others can predict generic investor behaviour.

Valid question! Depends on a lot of aspects including business longetivity, quality of management, earnings, growth anticipated, time horizon of the investment. I cant predict 15% growth though for sure - that much I know.

Another minority acquisition by Indiamart. They have acquired 26% of Agillos E-commerce for 26 crore valuing the company at 100 crore. The revenues of the acquired company for last 3 years are -

While we will have to wait and see how the acquisition pans out and what plans Indiamart has for integration, valuing a company with 29 lakhs of revenue at 100 cr does seem a bit questionable. They have essentially valued it at 340x revenue.

There isn’t a lot of information available on Agillos online but I wonder what technology or capability could this company have that Indiamart could not build something similar for a cheaper price with all their resources.

Nice thought, but their acquisitions are beyond reasonable. Buying only part of the small businesses…… and not able to justify that during concall worries me.

Data security is very sensitive issue.

Is Indiamart capable of handlling same with utmost care? I know same have happened with Zoomcar,Zomato & Bigbasket.

Just wanted to share with all & wanted to know consequences of this issue…

Wrt #6, you are right, very hard to get confidence on a high growth rate. Especially since, in the latest investor concall even the promoter himself said that they need time to figure out a game plan on how to achieve higher growth given the apparent disruption caused by the pandemic. Needing time to figure something after such an adversity is reasonable. However paying 85x multiple given the above doesn’t seem too reasonable.

Agree - despite all the things I am very impressed by especially regarding management - valuations have again become too frothy inspite nothing really changing over the last couple of months, and I am still worried about a COVID wave. Booked out recently and will look to add if we see substantial dips and pessimism around the stock again.

Yeah, what mgmt has been able to achieve since 2015 is quite commendable. Having so many customers paying regularly up front is no mean feat.

Just that the almost all current monetization seems to be around lead generation (though they do that quite aggressively as play store and twitter comments/complaints indicate). For this valuation (went up by further 10% today!) to be justified as an entry price, there probably needs to be at least one more solid monetization driver. At any some particular lower valuation, certainly attractive.

Key monitorable is Indiamart results is deferred revenue collection, which has grown by 20% YoY. As per mgmt, revenue is typically 20 months average of deferred revenue collection. EBITDA margin should stablise around 38%. Higher margin in the past quarters was due to cost savings during Covid19, which were not fully sustainable as per mgmt. Not justifying the valuations in any way.

yes agree… deferred revenues & cash collection from customers is very strong …

when the results were not really good, market saluted it based on optically good revenue numbers

but now when the results are actually good, market is hammering the stock again based on optically bad revenue numbers…

from next quarter onwards the accounting & actual internals both would start looking good

In most businesses which collect cash after revenue is recorded its a lag indicator… like debtors of 90 days

but businesses which collect cash upfront for 1 year/ 2 year packages its a lead indicator… so cash is collected first & revenue will be recorded later

Re: ‘collections’ EBITDA.

Nice work it def makes sense. INM has stated several times (and rightly so), collections is the lead indicator and needs to be watched closely. But your ‘cash operating profit’ methodology is unique. TY for the insight

Re: the revenue booking / accounting

I have a different pov. My interpretation is that ‘web services’ are what we know as subscription income. And ‘lead based services’ is when they sell add-on leads package to sellers who may fall have exhausted their quota and want a top-up. So while there is definitely a component of lead based services in their revenue, INM’s predominant revenue is ‘web services’ and hence accounted pro-rata

PS- My first post in Valuepickr so pl excuse lapses of this 100% newbie

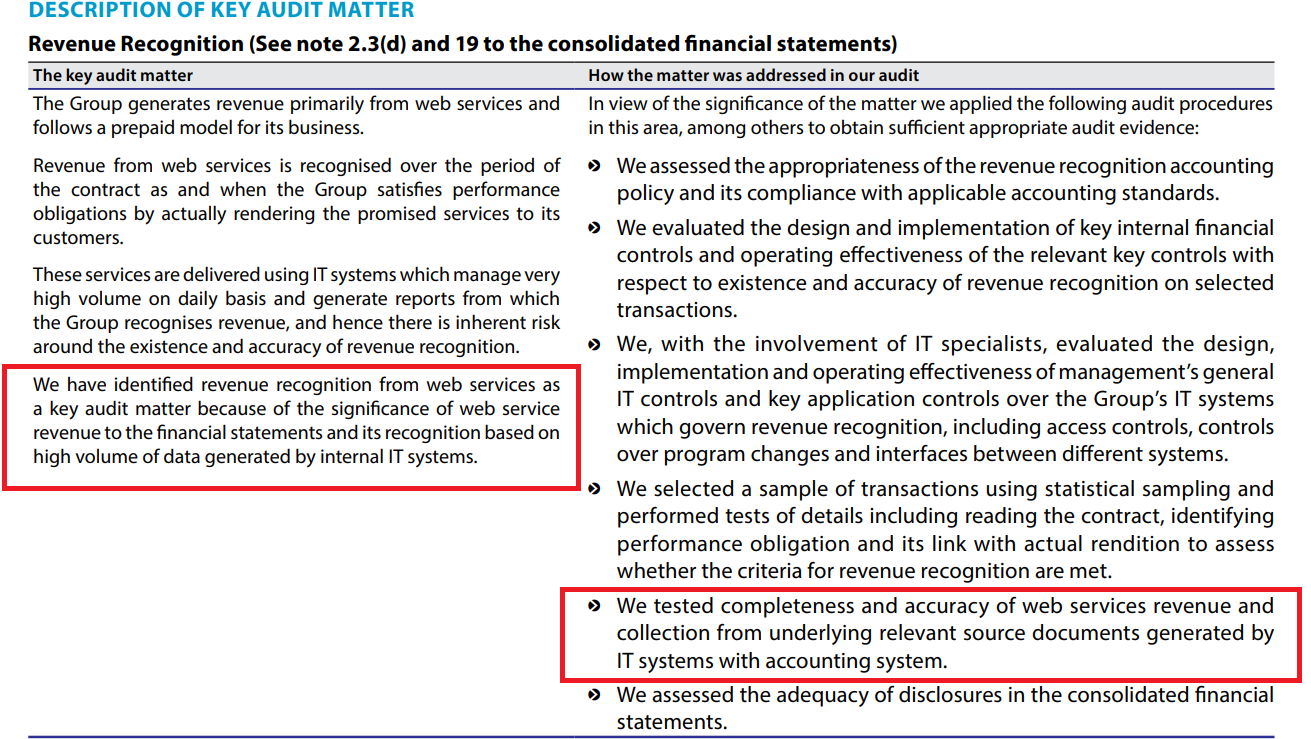

Even for “web services” the audit report mentions revenue recognition is based on volume data generated by the company’s I.T system. But practically, the numbers you get from volume based reports may not be much different from pro-rata I feel, so it will come to the same thing.

Sry for late reply didn’t get the alert - rather got the notification but didn’t take notice of it. Still v much finding my feet here!

You’re v systematic in presenting. Need to learn that and a lot more from good folks like you. TY