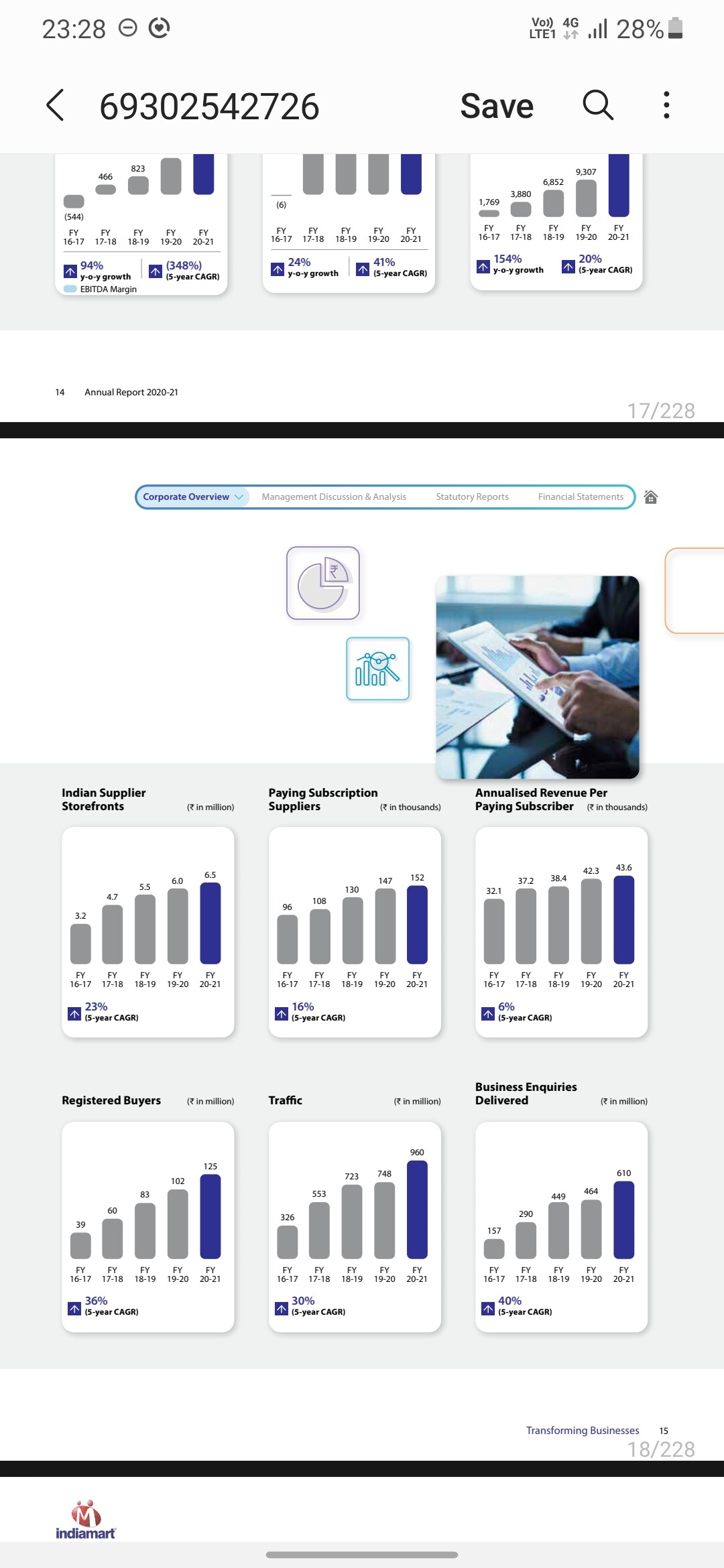

Paying suppliers are 152K.

An addition of 6K per quarter is 4% growth.

16% annual growth is decent, but not impressive because it’s 95% revenues come from paid subscription, considering the high PE it’s been trading at.

2 Likes

I think yes, they do need to keep getting better.

To ward off competition they will have to constantly make the subscription a better value proposition, and that’ll be it’s moat.

May be not lakhs, but yes, I do feel five figure additions some quarters later, as covid is receding and msme environment resuscitating.

Q2 call and performance

-

All leading indicators- Deferred revenue, billing and collections, Subscription additions in a healthy growth trajectory - current revenue is function of past quarters Deferred rev, future revenues will be based on current Deferred rev( that’s the biz model)

-

MSME stress n rebound - going by addition in Subscribers of 5.8K this Qtr and guidance of better addition in future, things looks better from here on - 4% QoQ growth is 22% annualized.

-

Mgmt tone for first time appears from super conservative to decent growth ahead - operational indicators being - sales and svc staff hiring, aggression in acquisition( 100% in Busy, second round in Vyapaar), though still shying from high growth guidance but comfortable with 20%+

-

Post Busy acquisition ( Top 3 ERP in India), a sizable revenue growth will come on top of core business - 188cr Q3 is their core biz, annualized closer to 800 cr, Busy + all remaining will add say 100 Cr annual - net -FY 22 at 900 base

-

FY23 - can do 1100 - 1200 cr revenue and at 38% OPM margins - 350cr-400Cr profits, current mkt cap is 15K cr( cash being 2Kcr and high cashflow core biz), sub 40 PE for a 20% grower and have a portfolio of investments in adjacency. Cash generating machine to continue inorganic acquisition.

-

Near future -Q4 22 will look good on topline with near 200 cr revenue( 210 if Busy numbers get added) but likely flat/lower on EBDITA due to margins normalizing to sub 40% from FY21 average of 45%+.

Capital allocation

- Busy acquisition at 500 cr cash for 40cr revenue and 25% profit profile, 15% growth looks sub optimal - esp Busy being On premise solutions in cloud era. However mgmt explanations on having small mid size being target segment for Busy( like Tally) and super sticky biz have some basis. To be seen if they can increase growth rates beyond current 15% type.

- Vyapaar is a very high growth trajectory and they have increased share to 27%, target segment being micro and DIY type customers.

- Legistify doesn’t look adjacency (legal), but does serve same customer base of MSME

All in all initial euphoria is over, Expectations are reset, mgmt has their own moderate way and pace of execution, valuations are much reasonable compared to any other listed tech focused player, here onwards need 2 QTR of stable(20%+) growth and successfull delivery on acquisition portfolio for market to develop growth narrative again.

Invested

8 Likes

Hi,

I don’t have any special knowledge of this business, but let me attempt to answer your questions from my perspective. Again, I am talking about the expectation mismatch rather than what is right and what is wrong here:

I think when one talks about the SME opportunity, the numbers bandied about are in a totally different league. India reportedly has around 6.3 crore SMEs. GSTN database itself now has more than 1.2 crore registered businesses. Around 1.5 lac new companies were registered with MCA last year. Banks have disbursed over 5 crore MUDRA loans in each of the last two financial years. In the context of such numbers, IndiaMart’s 6000-per-quarter is a drop in the ocean.

This is precisely where the management skill comes in, right? What did IndiaMart do with their Rs.2,000 crore cash pile is the question I have. Reduce prices, offer longer packages at same prices, link prices to successful conversions, offer cashbacks and discounts, come up with referral schemes, go on an aggressive marketing and branding campaign, deploy field force at mass scale to up the enrolments – there is a lot you can do to activate the market*. IndiaMart did too little, too slow I think. Just when the market was expecting them to press on the accelerator, IndiaMart retrenched junior level staff to save costs.

Yes, IndiaMart can be looked upon as having a SaaS component though I would not generalize this to every platform company. (Not sure if I understood the question fully here)

I haven’t tracked JD Mart’s growth any closely and I don’t think Reliance’s entry poses a threat to IndiaMart. I think the opportunity size is large enough to accommodate multiple players.

I think the above points make it amply clear what I would expect from the management. They have the money, they have the resources, they have a head start, now just go ahead and do it. As Winston Churchill once said, “never let a good crisis go to waste”. But I think IndiaMart just did.

*(One hypothetical example – Banks disbursed 5 crore MUDRA loans. Tie up with banks to offer 1 IndiaMart premium account at a 50% discount with every MUDRA loan, optional at the borrower’s choice. Even if 1 in 10 borrowers accept your offer, look at your numbers)

10 Likes

They have outsourced sales team (or at least a part of it) after Covid. I do remember management saying this in one of their concalls in last 2-3 qtrs.

And given the perverse incentives in sales (incentive bias mental model) and non-stop pressure, such fraudulent cases can and will happen. Let us hope that is at a much smaller level (don’t have any data to quantify it).!

1 Like

On the size of opportunity, most of the analyst are considering the entire available SME pool. However in 2 earlier concalls that I listened to management said that they will onboard only “GST verified” SMEs, which is a much smaller subset (or at least it was back then ) of total GST registered SMEs.

Completely agree with you that mismatch of expectations is one of the key problems here. Everyone is expecting and hoping it to be next Alibaba. People forget that Chinese market is different where many big players have political backing and hence they have grown to such huge sizes.

The other overhang on stock price was QIP done some time back, which will ensure that ROE remains depressed for some time. Also, since almost all major MFs bought into QIP there are not enough large buyers available in market to support further share price rise (learnt this nuance from Gautam Baid’s book).

Another point to think is with so many acquisitions (and more likely to happen) will it end up like InfoEdge? Hard to say as nature of acquisitions are different…

Time to let the dust settle rather then rushing in head first on every fall!

5 Likes

Mr Dinesh Agarwal talks about margins for next qtr of 35% & ranging between 35-38%.

He also talks about scaling up of Busy on pan India basis. Also, about Vyapar.

Disc : Invested.

First I have invested in it so take it with some bias

When we look at earlier concall and there management mostly they have outperform there own numbers they have projected at start of covid around 3-4k new addition and have able to achive 5-6k+ that is a very prudent management overall and also there own margin call were also mostly outperformed so there own projection atleast be most likely be achieved.

There deferred revenue is a double edge sword as it just delay the inevitable loss in the buisness and that make it sometimes overlook the fact that covid impact was just next to nothing in initial covid time but it is now reflecting they have already said there revenue were around 799cr ie more then 198cr currently seeing only 188cr so this mismatch might play out and there will be time were actually numbers might not be that easy to justify as they have grown there buisness and as they work on Deferred revenue but there expenses are current so can have a mismatch and sudden jump can also be there atleast in margin side.

If anyone who have an account on IndiaMART and is a active payer of there services are they trying to sell you software ie cross selling is there or not as there new aquisition should be argued they can do that as there own user base and there aquisition user base are in the somewhat same domain as it they are able to do that then it create a moat of software shift that may make business to not switch as now they not only need to switch platforms but also many key software.

They have good potential and growth in there own core marketplace type buisness but there next growth trigger is there software aquisition and there ability to cross-sell them efficiently as they all are mostly good and somewhat profitable business but if they are given free customers by this method then they can increase there revenue and as cost is very much constant so can even make profit to be even higher over time.

This last point is very important as if they are able to do it effectively there own aquisition and investment can be hyper growth territory and also make them more sticky over time as buisness become more reliant on them.

4 Likes

Are we falling for narratives/stories when we say “huge growth potential”, “crossell and upsell opportunities”, “hyper growth territory” etc?

Can you help quantify these terms? May be that will help bring more clarity and conviction!

2 Likes

With a difference.

Mr. Agarwal said about the recently acquired Busy, it’s currently North focused, and he intends to make it pan-national. I assume, with the large database of MSMEs he could competitively cross-sell this product.

Now in hands of DA I would like to track the progress of Busy from 42Cr rev. This will help me build conviction in the management.

2 Likes

Thank you @The_Seeker @Chandragupta @jamit05 and other senior members for your wonderful insights.

Here are my further thoughts on IndiaMart especially on its acquisition of Busy.

The revenues are almost 41Cr. Where the management has itself said, that is mostly from North India.

Just a scenario, if by next FY, they are able to expand to west, south & east and are able to make 10 cr from each region. Then the story becomes more powerful.

Is this possible, I think so, with the kind of reach IndiaMart already has. Can they grow it to substantial revenues (maybe 200 Cr in 2-3 yrs time frame.)

All these are non-real situations. But this looks possible as of today.

Dis - as above, Invested.

1 Like

If we look at there just pure aquisition.

Busy accounting software that is one that sme need and can easily integrate with there platform and people pay for that so they not only sell it to there client but also make busy older sme clients to be on IndiaMART.

Easy e-commerce this is basically an inventory management software solutions work more like a saas and you get how this can be sold very easily as business need such software so they act as a advertisement for them.

When you see there recent and even past investment all have one thing in common they are all related to buisness functioning from inventory, accounting to leagal matters.

These are mostly software that have annual fees so they can sell them as a package to existing customers as one or even sell them individually.

Like if you have listed and paying IndiaMART only then you might need accounting and inventory software for better management and gst so either you pay other software provider that will not have integration with IndiaMART or get similar softwares as a package deal with IndiaMART that will not only make new customer but also make existing customers to take higher packages as it will act as a better deal over-all for them and also will tie them in there ecosystem.

These are point that make cross-selling and upselling possible.

For growth there core business is already in a industry that is growing fast and is also digitising fast so they will also grow in there user base as more msme emerges and also start to use them.

1 Like

I listened into the Q3 concall yesterday. Some points I noted on “narrative vs numbers”:

- Current paying subscriber base is 156+K with big percentage at the bottom of the pyramid with lowest subscription fees

- Subscriber churn every qtr impacts the net addition of new paying subscribers which is currently at 5k-6k range/qtr and management is hoping to increase it to 7k in future. Please note, most new customers are in lowest subscription fees category

- There is an overlap of 15-20% of subscribers between Busy and Indiamart. My guess is these customers are the gold and platinum category for Indiamart. So remaining adressable pool for cross-sell and upsell is about 80% with lower capacity/willingness to pay

- Busy is standlone, license driven software right now. Management has said they will try to explore shift to cloud platform and SAAS model over 2-3 years. They need 1 year to get full hang of Busy and create new roadmap

- For subscribers who are already on Tally or other similar software, they will not be keen to move to Busy as these software is sticky in nature …whatever your accountant prefers, MSMEs will stick to it…

- for MSMEs struggling or unwilling to pay higher subscription charges for Indiamart, buying such software is additional cost that many micro and small businesses definitely cannot afford. Just talk to any micro and small business owner/entrepreneur and you will get idea on this

- For medium size businesses, they will already be on existing software and probability of moving to Busy is low (as articulated in pt. 5 above)

So in my view, cross sell and upsell is more narrative at this stage and less real. In future it will change, but that is all hope at this stage. Also, Indiamart Intermesh management likes to move forward at its own pace (for good or bad, it is what it is - may be they want more stable business growth vs hyper unprofitable growth).

So while future potential definitely exists, we need to temper our expectations on hyper growth, cross sell and upsell at least in near term.

@Chandragupta has perfectly articulated this in his post.

What would be more interesting at this stage is to track when operational leverage kicks in. Need to remember though that costs will increase for Indiamart in Q4 and Q1 (due to hiring and salary hikes).

9 Likes

I wonder, even they have said most of the things are not in line… still a buy call.

Disc : Invested

1 Like

Good summary. My take on this is that Indiamart is still expensive given that its growth rate is slowing down.

- By the time they take Busy to the cloud, there will already be a 5G rollout in India, newer technology players and more acceptance among SMEs to take their accounting books to the cloud. So the whole thesis of buying Busy could be challenged.

- I wonder how much effort they have put in retaining existing customers and improving their experience. Their website and app always looked cluttered and somehow gives me the impression that they don’t have a product mindset in their DNA. This is my subjective opinion and I do not intend to doubt Mr. Agarwal’s organization-building skills.

- Senior management seems to be focusing more on inorganic growth, while the opportunity and market size in their core offering are still to be fully exploited.

Disclosure: Sold out a part of my holding and booked a loss.

4 Likes

Hi MadhuG. Its been a long time.

Regarding IndiaMART, last some quarters were muted due to low activity in MSMEs. Pandemic-related. Poor performance by leading banks as well.

However, last quater bank results were good. Excellent in some cases, esp retail side has been good.

With this increased retail and MSME activity, I feel IndiaMART will see a pick up in earnings. 20% should be easy for 2022.

Dinesh Agarwal has also communicated positive guidance. He is cautious of making too many forward looking statements, but likes this talk about the process.

4 Likes

I think 20% growth is no brainer for IndiaMART for short to medium term unless some nasty surprise shows up (which once in a while does!). Given the current valuations, I was thinking if doing a reverse DCF calculation might help to get some insight on likely return expectations from here on?

3 Likes

Hi,

Imo there is nothing new here.

This has been highlighted several times by INM itself. For instance: QIP document of '21: Risk factor # 11:

“We acquire a significant portion of our suppliers on IndiaMART through the unsolicited creation of supplier storefronts and such suppliers may refuse to consent to their information being made publicly available on our online marketplace, which may negatively affect our business and may subject us to various legal claims…”

PS - Am ot getting into whether it is right, wrong or the shade of grey. Just saying that this has been officially disclosed as a risk by the Company itself.

5 Likes

Yes, indeed. When one gains experience, one tends to look at the overall picture and not go by one single line of thought, or one single narrative even though backed by numbers, because certain businesses exist for years and decades. Having said that, one cannot simply brush off a discomforting evidence, particularly when the stock is trading at very high valuations, it might help someone having a perspective.

Not invested.

1 Like

Nothing to wonder

One has to look at the recent acquisitions and especially the field / areas of these acquisitions. No doubt HDFC Securities have analysed all of that and they can’t be wrong.