Did a top down deep dive into IndiaMart Intermesh to understand the full potential of the business.

Key points -

A list of all investments made by IndiaMart along with stake, what they do and their valuations

-

Simply Vyapar Apps Private Limited (26% stake) - Last round valuation 116 crores. Accounting and tax invoicing company.

-

TruckHall Private Limited (25.02 % stake) - Last round valuation - 44 crores. Online Marketplace and software development for the logistics industry and managing Superprocure that digitises freight sourcing.

-

Legistify Services Limited (11.01 % stake) - Last round valuation round 11.8 crores. Through its SAAS based ERP tool “Legistrak” offers organizations to manage legal workflows such as litigation tracking, notices management and legal vendor management.

-

Shipway Technology Private Limited (26 % stake) - Last valuation round - 70 crores. Shipway Technology Private Limited is engaged in the business of developing SaaS based solutions which allow small businesses to automate their shipping operations.

-

Mobisy Technologies Private Limited (8.98%) -Last valuation round - 111 crores -Mobisy owns Bizom which is an integrated platform for distribution and salesforce management of businesses.

This is over and above their in-house CRM, lead manager and payment gateway.

The above investments signify that IndiaMart wants to create a one stop shop for addressing all MSME needs. The company expects one large ticket size acquisition and multiple smaller investments which are synergistic to the IndiaMart model over the next year.

So IndiaMart has already hinted at 8-10 synergistic small investments, they have already done 5 investments (4 in FY 2020-21). This is in-line with what 1688.com does which provides a lot of value added services in areas of payments, tax invoicing and basic management software and incremental services.

1688.com a subsidiary of Alibaba Group holding company is one of China’s leading online business-to-business (B2B) marketplaces, with 120 million users and 10 million companies listing their products on the site and earns revenue through subscriptions.

1688.com has around 900,000 paying members. The business of 1688.com has done very well across the last few years primarily due to an increase in the average revenue from paying members for the past 3 years despite the fact that there has been no major increase in the number of subscriptions.

FY 2018/ 2019/ 2020 - RMB7,164 million / RMB9,988 million (+39%) / RMB12,427 million (+24%)

Average Revenue Per User - 7960RMB (INR 81,988) / 11098RMB (INR 1,18,738) / 13807 RMB (INR 1,54,000)

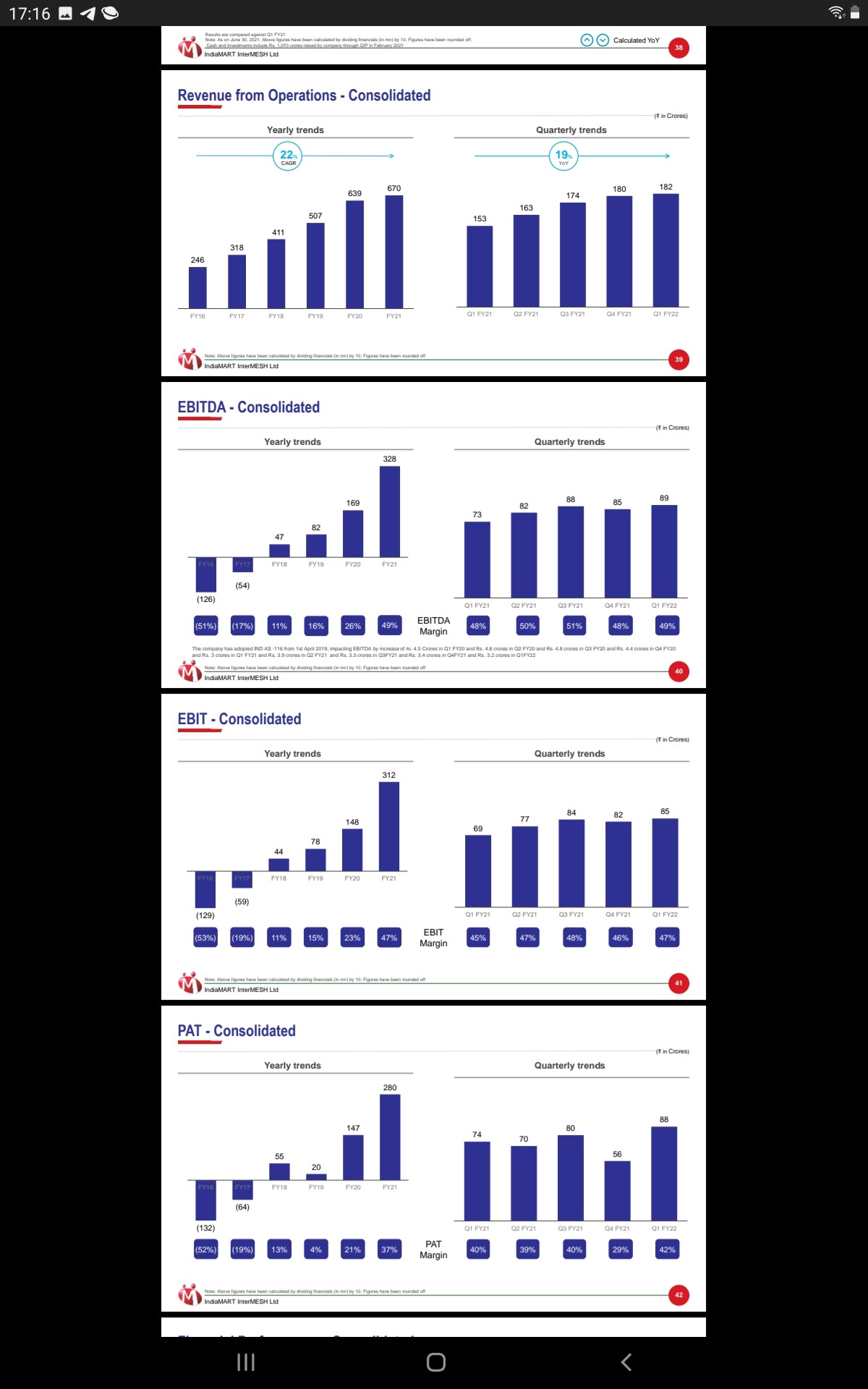

1688.com does 1.5 billion USD in sales almost 20 times what IndiaMart does (due to having 6x more subscribers and more than 3x ARPU) and is still growing at very high rates which shows the possible runway IndiaMart has, if it executes efficiently. 1688.com has EBITDA margins of over 50 percent, while IndiaMart has a sustainable EBITDA margin in the range of 35-40 percent. Investments in technology and value add products will keep the range lower than the more mature 1688.com at least in the near future.

This also shows the potential for IndiaMart and their vision is also aligned with providing value added services in addition to increasing subscribers.

Disclosure - Invested