Infoedge does have a venture investment arm called Info Edge Ventures (Infoedge | About Us). Since its wildly successful investment in Zomato, InfoEdge has been betting on more startups outside its core operating areas, so essentially they operate like any other VC firm in this regard.

Indiamart on the other hand has only made strategic investments (startups that are directly related to their core operating areas) so far and is likely to continue doing so. It’s unlikely that they will look to make money from these deals.

In any case, it’s going to be difficult for them to compete against the likes of Accel, Elevation, Nexus, Sequoia, SoftBank, TIger and other top VC firms to bag marquee deals that make big money for investors unless the startup sees a strategic advantage in going with Infoedge/Indiamart.

Another small investment by IndiaMart. This disclosure is given under Regulation 30 read with Schedule III of SEBI (Listing Obligations

and Disclosure Requirements) Regulations, 2015 that Indiamart Intermesh Limited (hereinafter

referred as “Company”) has indirectly, through its wholly owned subsidiary, Tradezeal Online

Private Limited, agreed to acquire 22% of the Share Capital (on fully diluted basis) of Truckhall

Private Limited (herein after referred as “Entity”) through SSHA signed between the Parties.

Total revenue of 1.48 crores in FY2020, consideration value of 44 crores with the company investing 9.68 crores. Valuation at 29.72x Sales. The company operates in the business of creating online marketplace and software development for the logistics industry including running and managing a digital platform ‘SuperProcure’. SuperProcure is a SaaS based platform that digitizes the entire freight sourcing, by finding the best possible rates through a transparent bidding

and auction structure,and dispatch monitoring system of the logistics department of any business, offering complete and-real timevisibility of all the events in the entire dispatch cycle, from indenting to delivery, via alerts, dashboards and reports, which improves collaboration amongst all stakeholders leading tobetter efficiency in the entire process. The acquired company has a turnover drop from 10.53 to 3.69 to 1.48 crores in the last 3 years. While the line of business looks synergistic to Indiamart the financials don’t. Kind of also seems evident that there are going to be smaller acquisitions rather than full blown takeovers by the company similar to the Infoedge style business model.

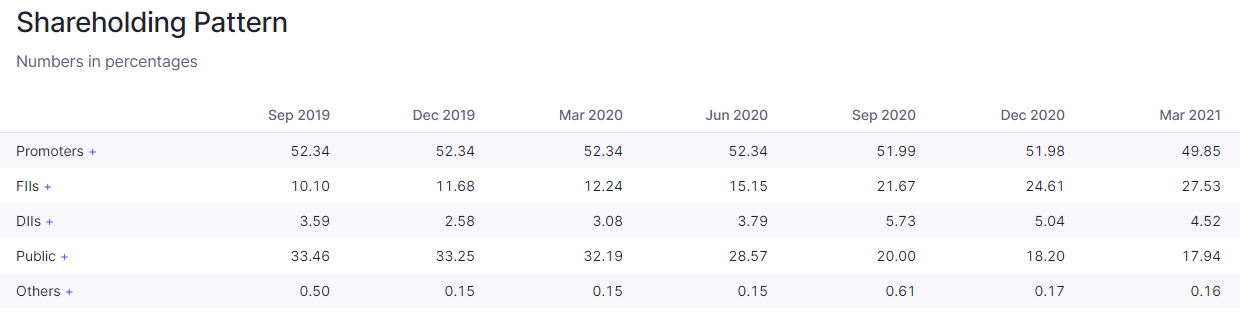

Decreasing promoter holdingis making me dis comfortable in Indiamart. Initial small reduction in Q3, I thought its due reason for promoters to enjoy some benefits after long holding and serving period when valuations are good. But now holding going below 50% is causing me to think on the valuation stretch of the share price. Particularly considering 2.5% reduction in last 3 quarters - considering avg valuations promoers have liquidated equity worth 600+ Crores.

Though I wasn’t aware of this earlier, in the last few days I have noticed that Just Dial and their ‘JD Mart’ are one of the top advertisers with the IPL this season. And considering the viewership the IPL gets throughout the country, JD mart is sure to get a lot of visibility. This raised some questions in my mind:

I realize that the “threat of new entrants or competitors” topic has been discussed a lot in this forum. However, will this advertising move by JD Mart finally make Indiamart loosen their purse strings and spend the enormous amounts of cash they have?

A point in favor of Indiamart is the massive market share it currently enjoys along with some loyal customers who have signed up for a couple of years. But considering the size of the untapped market does JD mart have a chance to grab the new market with their advertising, thus reducing Indimart’s overall share?

If JD mart does start chipping at the market share thanks to the advertisements during the IPL season, when will we see start seeing the results: The next quarter or will it take longer?

We have to believe in the capability of Mr. Dinesh Agarwal.

He runs this Bussines more than 20 years, Also he has a long vision, I thought he already made a plan to compete with JDMART.

Also, Company made many strategic investments that will give an extra edge to there business.

I don’t think so it’s easy for JDMART to compete with Indiamart.

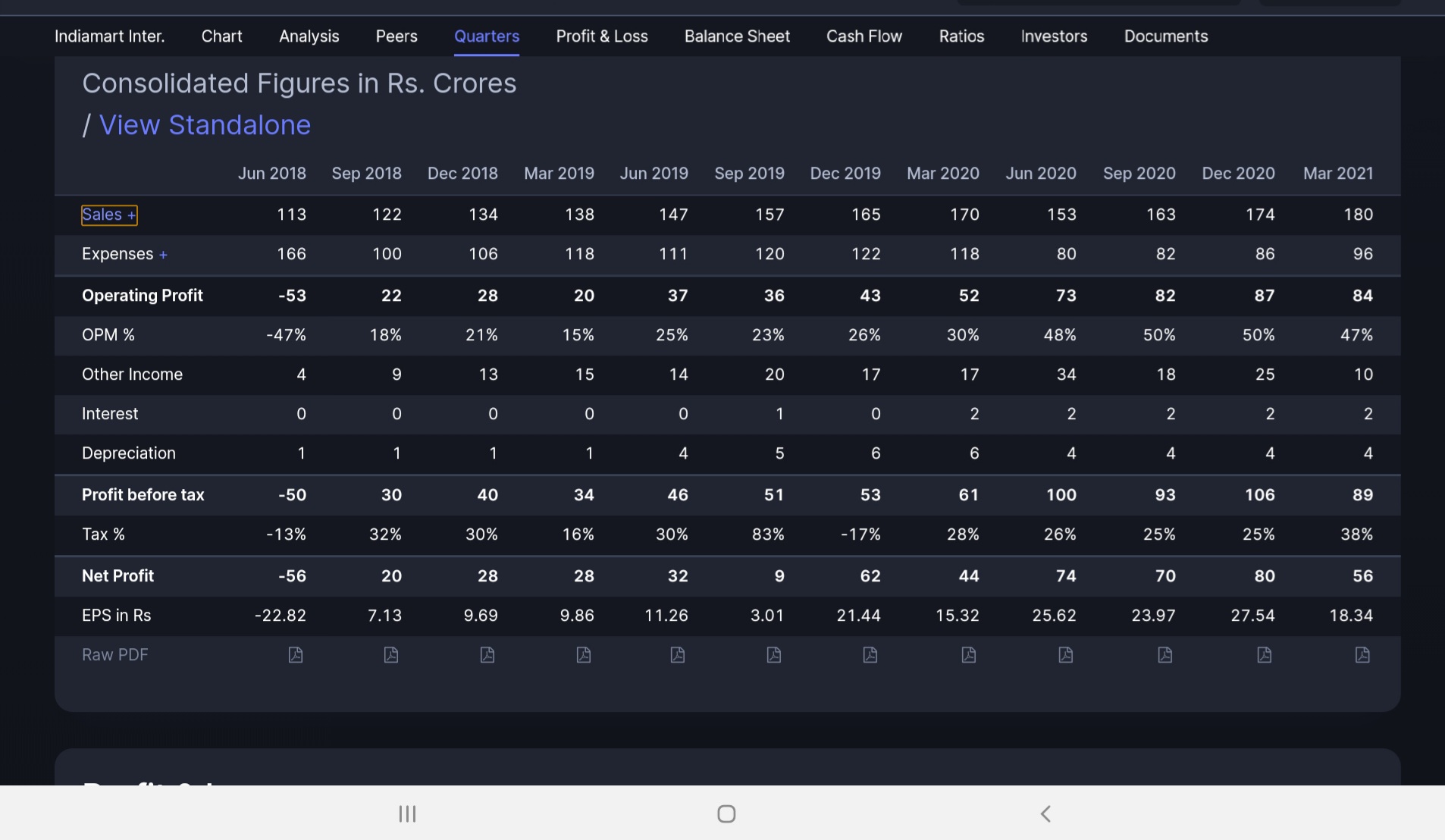

Disappointing numbers by IndiaMart. Customers growth at only 4k customers in this quarter when comparing to growth of 9K(4k lost customers) and 7K(1.5k lost customers ) customer acquisitions per previous quarter. Topline has increased by 4 percent Q on Q, PAT has dropped sharply on account of increase in employee benefits and slight increase in other operating expenses and a drop in other income.

Important to see management commentary tommorow, with nationwide lockdown a muted Q1 can be expected.

While there have been 3 small acquisitions when and what the synergistic benefits are remains to be seen.

Only positive is increase in operating cash flow due to renewal of longer term contracts passing through deferred revenue.

One key metric of average revenue per paying customer has marginally moved up QoQ as well as YoY - a key attribute for SaaS setups

PAT looks down ( thus EPS) due to drop in other income, at operating profit level it is flattish QoQ and up YoY

On QoQ the revenue performance is inline with their listed history - it has always ranged between 3 to 5% type ( and that is model of SaaS organizations) - see 2018 / 2019/2020 - and market has rewarded them crazily with this revenue growth - infact it was bottomline that has shown drastic improvements- now looks more sustainable floor

100% organic traffic and no marketing spend - known fact but shows they are not fighting for acquisition or mkt share on paid basis yet( competitive intensity indicator - a good sign with noise around JDmart launch). More in concall.

Traffic and enquiries continue the upward trajectory both YoY and QoQ - network effect sustaining- one can argue about conversion to paying customers but thats the whole idea with time lag if one has this huge platform

Small ticket investment across adjecncies and again SaaS solutions mostly( gives an idea around mgmt conservative nature before going big and direction of capital allocation with focus on adjecncies)

Collection and deferred revenues looking good and healthy

Nothing to say about insane margins, slight dip,on QoQ but still very high

Small dividend payment is good gesture

Large cash 2K cr+ - wonder what they will do with this large sum given mgmt investment history ( timing of QiP was smart to build this war chest though)

The company is looking to acquire or invest in one large company in the next year.

All other acquisitions will be in line with their last 3 acquisitions.

They are not acting like a VC, they only invest in companies with which there will be synergistic benefits. Expecting a portfolio of 7-10 companies / services which can be cross sold and integrated with IndiaMart Intermesh, one or two companies may not work out.

The company expects to grow atleast 25 percent in the long run. (Very Skeptical how is it going to be possible) (would require the company to add 28- 30K, unlikely going to happen in FY 2022)

No aggressive advertisement spend.

Have waived off a one time 5k charge when integrating a new supplier to system.

No direct impact currently due to JD system.

The management also replied to my query on the call which related to acquisition of Truck Hall Private Limited (Superprocure software) whose revenue fell from 10.8 crores to 1.5 crores in FY 2020. They were originally a logistics services company and than switched to a business model which was related to Software as a Service model. The company is growing at more than 100 percent and could have synergistic effects.

There is a churn of around 10 percent across the board.

Per Dinesh , Have been a 25% rev growth organization and would like to be in future as well - this happens by two levers

New subscription- need 20000+ additions a year - this has happened in FY18, Fy 19 but not in FY20 and FY21 - expect this to happen once economy stabilizes

Upping of avg subscription- this is playing out alright if not to desired levels

Potential universe/ target set - product focused SME which 2.5 to 3 million ( out of 12M+ registered SME with GST) - Indiamart believes 20% - 25% of this population can be their paying customers - that is 4 to 5 times current subscribers base of 1.5L.

Quality of subscribers - They called out about stringent measures that have slowed down on boarding-GST, phone and email verification, lat-long and so on

At this point it is clear that lower strata of Indiamart target customers pyramid are clearly impacted by covid and are very fragile, Q1 22 will be washout like last year and thus FY22 will be on similar lines as FY21 or worse if 3rd wave sets in later. Acquisition and inorganic growth will not play out at least in numbers in FY22. Infact sales hiring will take EBDITA back to 35 to 40% range and affect bottomline.

With no visible short term growth triggers which justify premium valuation, some money has started to / will move out and float will determine fate and new floor, need to watch out for recent low of 7600 range, defending that need to be watched out for.

Seems like the market hasn’t analysed the result accurately. The quarterly net profit for Q4 is 55.7Cr which was 80.2Cr in Q3. At first it looks like profits slipped by 30%.

1.Now look at the other income which is 10.4Cr in Q4 as compared to 24.6Cr in Q3.

2.Also look at Tax impact related to change in tax rate and law which is of 10.9Cr which is paid for the first time due to changes in the taxation, which was not levied in Q3.

now add the difference 55.7 + 14.2 + 10.9= 80.8CR for Q4 as compared to 80.2CR in Q3. The company has in fact given a marginally better result than Q3.

if the data i shared is incorrect, please enlighten me.

I think the current pullback is warranted given the growth expectations built into the price.

If Indiamart wants to command a high growth internet business multiple then they need to deliver 30% + growth like clockwork every year. Facebook, Google, Alibaba etc are still delivering that kind of growth at 1000x scale - so there’s really no excuse for Indiamart.

IndiaMart revenues only comes from subscriptions which is cyclical as it depends on economy performance. This also means that IndiaMart will perform better when economy does well. This is mainly because of B2B nature of business. While hyperscaler like Google/FB has mixed of services B2B and B2C, which balances somewhat.

I believe in the strength of IndiaMart’s business over the longer term but I don’t buy this argument. In India, every year promoters will find an excuse to blame the economy - Demonetisation, GST, elections, bad rains, NBFC Crisis, Covid, etc. The truly great businesses are the ones that become essential to their customers, have well diversified business models, and are resilient to these kind of shocks. The best B2B SaaS businesses have benefitted from the pandemic and not suffered.

The existing business they have is 5-15% growth business.

The call you need to take is are you prepared to bet that payments, tax invoicing, basic management software, loans and logistics to its existing network can evolve into something bigger? If you dont think so, you should exit the stock.