When i see the reported comprehensive profits for the year FY21, FY22 and FY23, company reported cumulative comprehensive profits of 2937 crores. In these 3 year periods, they paid divided of 417 crores in FY21, there is no equity raise happened during these years. So approx equity of company should have raised atleast 2500 crores from the end of FY20 to end of FY23. But equity did not raise in sync with profits.

When i am looking into equity statement, the difference in equity is explained by Utilization of Additional Reserve Fund (U/s 29C of the National Housing Bank Act, 1987) towards the provisions creation. Difference in provision creation via regular mode vs utilizing this fund is, there will not any trace of this utilization in P&L statement.

Assume a case where company chooses to create 10 crore provisions and it has final profit of 25 crore (excluding this provision) , usually companies will book this 10 crore under Impairment of financial instruments in P&L statement, so final profit will reduce by 7.5 crores(assumed tax at 25%) and the profit will be 17.5 crores. But if company chooses to use the amount from this reserve fund, In P&L statement, you will not see 10 crores under impairment and profit does not reduce will remain as 25 crores.

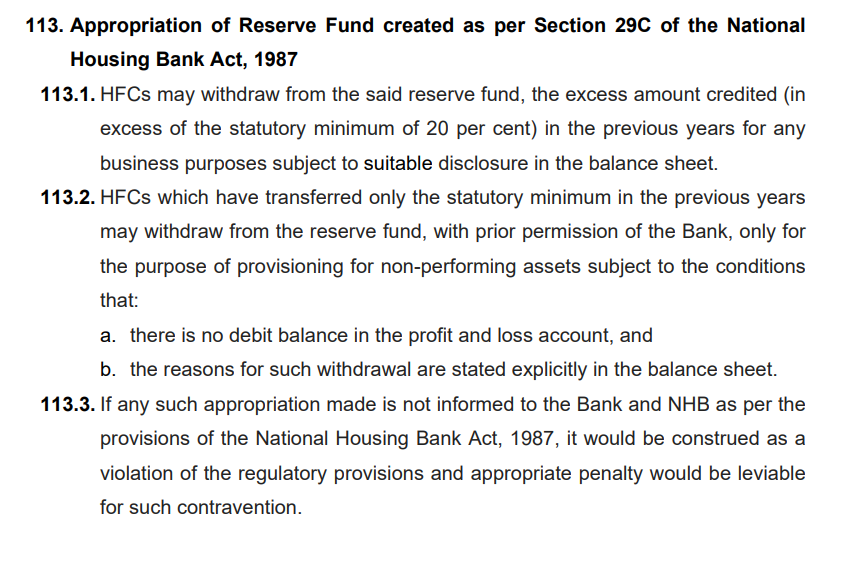

Now coming to this reserve fund, This is mandated by RBI to create this fund(i think it is 20% of profit) from every years profit before paying any dividend to shareholders. You will see all finance companies contributing to this fund every year from their reported profit. This fund will be used by companies in a worst case scenarios like covid, bad economic cycle.

But what’s happened in indiabulls is they create this fund in year 1 and they utilize this amount in year 2 itself and whatever they are creating in year 2 will be used in year 3. The pattern usually followed by all other companies and even in case of indiabulls before 2018 is they contribute every year, but they will use it rarely in one or two years, only in case of bad events.

-

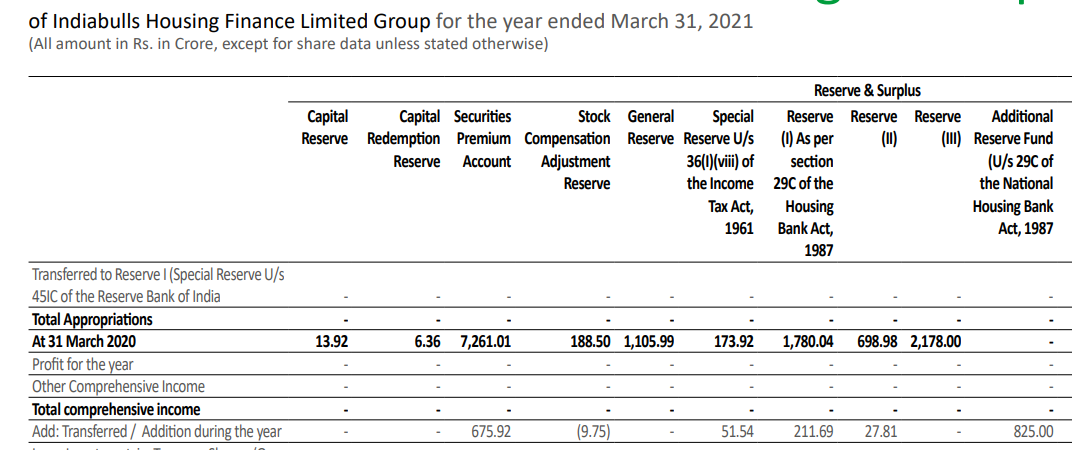

Added 825 crores in FY21 to the fund

-

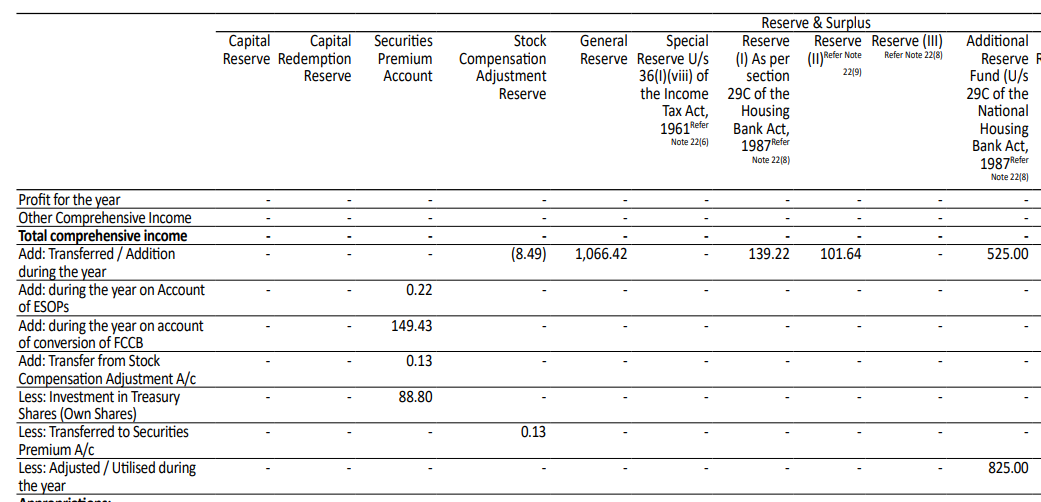

used 825 crores and create 525 crores in FY22

-

used 525 crores in FY23 very first quarter itself [Waiting for FY23 AR to see if they created further]

I don’t know why indiabulls chooses to create this fund and utilizes it very next year. By doing so, they are optically showing higher profit in P&L statement. Instead if they reported this as impairment in P&L, they reported will be much lower.

Disclosure: 1% of portfolio. These are not allegations against management and what they did is well within law. Point I am making is this approach of reporting profit and using reserve fund to increase provision seems very odd to me