Any views on Sameers resignation? If he had plans to relinquish, what was the reason for increasing his stake? Will it be put on block? SS Mundra being at the chair, will IBHL come out woods sooner?

Thanks in advance

QIP of Rs 750 Crores at a price of Rs 206 per share (which is half of the book value) doesn’t inspire much confidence in the company’s financials. If they have the liquidity and the Capital Adequacy that they claim to have why would they issue shares at such cheap valuations? The Management was asked about this in the AGM and Mr. Banga said they would raise the absolute minimum necessary. But it doesn’t make sense unless they think the share price is overvalued or that the liquidity they have is not sufficient for the coming days.

Any insights?

Again indiabulls taking another hit due to a failed bank…it owns 5% equity in LVB

Anyone knows the exact amount indiabulls invested in LVB

Seems like it is Rs 190 crores - preferential allotment at Rs 112. I would have thought that they should have already recognised part of the loss if they had the investment marked to market - and if they did there is perhaps an additional 1/6 of the value hit this quarter (assuming the current value they recognised the investment at is approx 1/6 of the preferential price as on Sep 30)

No impairment loss is accounted as at 31 March 2020. You can check note #10 to financial statement (attached to the annual report for the year 2019-20). Considering they have sold investments in Oak North - the losses that they would account on LVB will be set off against profits from Oak North and will not be very visible in the current years’ financial statement.

Thanks,

AJ

Seems, IBHFL is up for sale or are exiting the business of lending to Home buyers. They are anyways giving up 80% of the total loan to HDFC and only retaining the remaining.

Not sure how they are going to grow their overall assets in the next 3-5 years. Their strategy of expanding to Tier 3 and 4 cities / towns should come with relatively higher cost (at least branch network needs to increase and business per branch would reduce).

Any idea on when is the dividend getting paid to investors. The dates seems to be confusing.

Record date is 31st May and investor will receive the dividend by 17th June.

What does the following extract from this article mean?

Indiabulls Housing will originate retail home loans as per jointly drawn up credit policy and retain 20% of the loan in it’s books and 80% will be on HDFC books.

IBH will service the loan account throughout the life cycle of the loan.

Does this mean they will service 100% of the loans but only earn interest on 20% of the loans? Is it for all loans originated or issued by IBH?

This is co-lending. Let’s say if you want 10 Lakhs loan, India bulls will connect with you and process all the activities but additionally both India bulls and HDFC will also need to approve your loan.

Once approved, HDFC will send 8 lakhs to India bulls and you will receive 10 Lakhs from indibaulls.

So ideally both firms HDFC 80% and indiabulls 20% provided you this loan.

What indiabulls get 20% of your emi payment and 80% goes to HDFC. And risk also goes 20:80. If you don’t pay, HDFC will take 8 lakhs hit in their books and 2 lakhs by indiabulls

Why it benefits indiabulls: they get the entire processing fee and only needs to retain 20% of loan. All their operating metrics will improve(quarterly presentation has one slide for those metrics) Anyway these HFCs will securitize these loans after some time. Instead of doing it later, this is faster method.

Why it benefits HDFC: they no need to use their front end workforce and only backend team need to approve. So less operational expenditure

Is this such a super model: yes, but it might to operational challenges. Approval process has to go for 2 lenders. What indiabulls considers good profile are some of guys who might not be eligible from HDFC point of view

Super !!! sharing. Make sense.

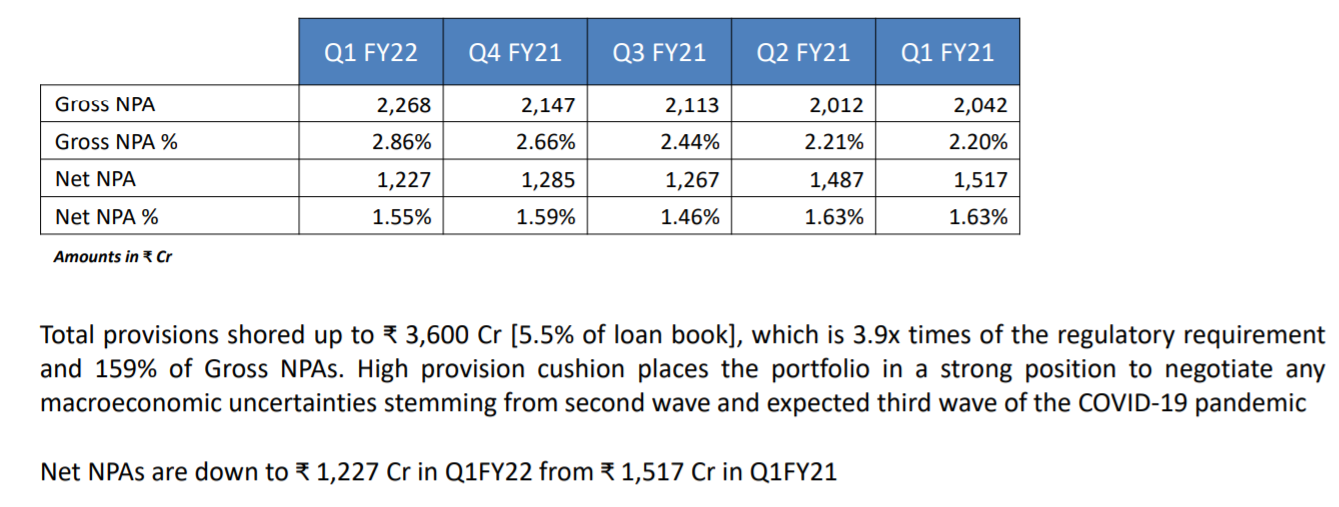

When I am looking into the Q1 FY22 investor presentation, GNPA reported as 2.86% of the loan book and total provisions mentioned as 5.5%, but NNPA is 1.55%. So far, I thought NNPA = GNPA - Provisions, But here that’s not how NNPA looks. I see this similar difference in some other firms also. How this calculation works?

First of all, 5.5% is of total loan book i.e. 70k crs around 3.6k crs and NNPA is around 1227 crs so it is almost 3.9x of NNPA but as they also held provisions for stage - 2 assets. They have not disclose the stage 2 assets in concall.

This is rough calculation and correct me if I misunderstood any point.

Thanks!

Yes correct. Here GNPA and NNPA are calculated with AUM, but provision of 5.5% they mentioned with loan book.

Just to add, they do not required these much provision to be maintained for regulatory requirements but they move some additional assets to stage 2 (in INDAS, you need to calculate the ECL which will have variables like PD, LAD and Loan to value so if you can trick one of these variables - you will different outcome as ECL) so they can maintain this kind of provision - they have mentioned in concall somewhere in the concall but I do not remember the exact quarter.

Thanks!

Why would a person take loan from india bulls housing finance at 8.5% where banks are giving out housing loans at a rate lesser than 8.5%?

How does IBHF acquit customers?

Even when banks says we are giving loan at 6.5%, this is base price, this is not given to all. Even same banks lending loan to some people at 9%. All this is based on how they assess the customer profile. Banks wish to take the creamy layer and they will reject remaining group. Reasons may be credit score, higher loan size, documentation and many more.

When this pool looks for loan outside banks, these Indiabulls, DHFL, Repco, Bajaj Housing, these are second cheapest source. These companies employs many DSA whose job is to make connection with the developer of properties and identify potential clients