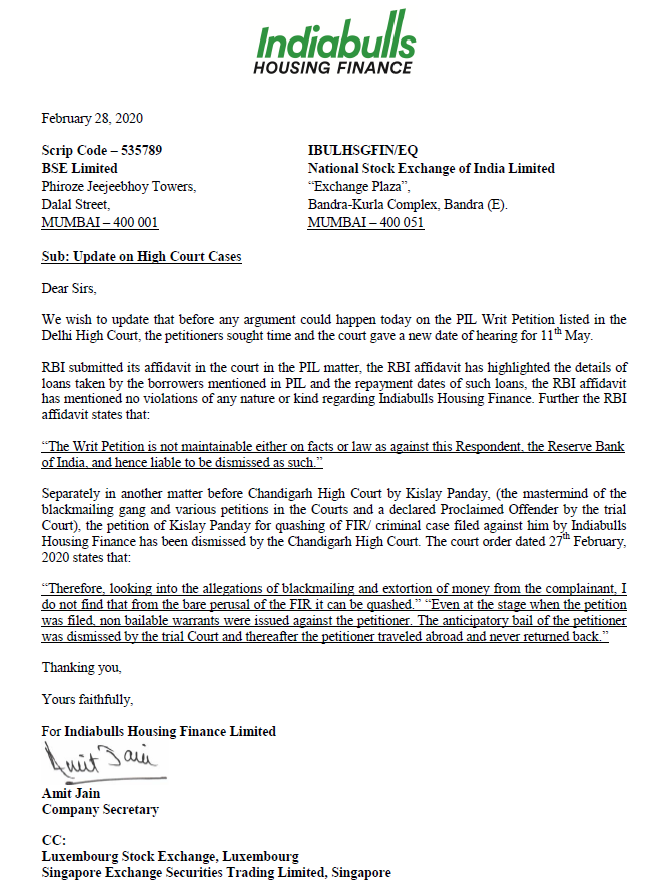

RBI submitted its affidavit in the court in the PIL matter, the RBI affidavit has highlighted the details of loans taken by the borrowers mentioned in PIL and the repayment dates of such loans, the RBI affidavit has mentioned no violations of any nature or kind regarding Indiabulls Housing Finance. Further the RBI affidavit states that:

“The Writ Petition is not maintainable either on facts or law as against this Respondent, the Reserve Bank of India, and hence liable to be dismissed as such.”

1 Like

Can you search for this writ petition in Delhi high court website and provide the link of the actual RBI affidavit. Would be good read to go through the original source, rather than the press release issued by the company.

So RBI was also a respondent and is saying it’s not maintainable against itself and should be dismissed ??

The company will not take a risk of misquoting RBI in a court document. About 15 months back, YESBANK tried to misquote an RBI finding and RBI immediately came down very heavily on them. So, it is fair to assume that if RBI doesn’t rebuke IBULHSGFIN, then what the company said is correct.

2 Likes

Bhaskar,

I don’t know how to search this write petition, can you search and share the actual RBI affidavit for forum members.

This particular case is Writ Petition (Civil) No. 9887 of 2019. We can search this case in the below manner: http://delhihighcourt.nic.in/case.asp

choose case type as writ petition civil - W.P©

case no:9887

year: 2019

enter security digit code as shown

This opens up order/judgements page (http://delhihighcourt.nic.in/dhc_case_status_oj_list.asp?pno=965494) and gives 1-2 page of order like adjourned etc. Unable to find the case material like RBI affidavit etc.

1 Like

It’s 9.1%. Sounds good to me at least

The issue would have inspired more confidence had it been bigger. For a company with a BS of Indiabull’s size isn’t Rs 200 Crores peanuts? Should they have tried raising say Rs 5,000 Crores?

1 Like

Press Release Moratorium Cases Apr 23 2020.pdf (542.9 KB)

It’s good to see IBHL isn’t listed in the companies opted for moratorium. Says much about it’s liquidity position

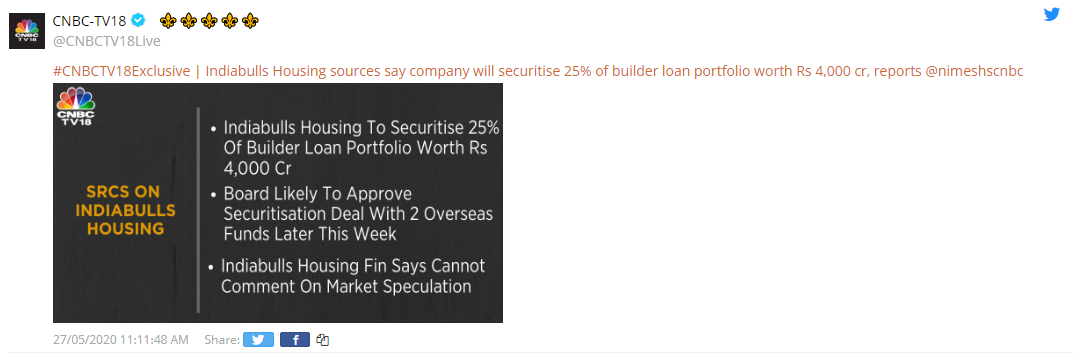

Its very difficult to securitise Builder loan portfolio in the current scenario. the main reason being:

- These are generally risky assets.

- These are generally structured debt which are being done by NBFC as RBI norms are not applicable like land funding, Quasi equity instrument etc.

- If RBI norms are not followed then no Banks will be able to purchase such portfolio. If RBI norms are followed then probably a hand full of Banks are presently capable of taking such risky bet (in my opinion only HDFC). HDFC will buy only the best of best assets and that to may be with some haircut.

Only high quality assets will be securitised after which there will be big question on the quality of left over assets. - Assets are being securitised implies liquidity crunch i.e Company is neither able to raise fresh equity nor it is able to re finance its existing debts.

- If you are not able to raise fresh fresh equity or debts you will require money to repay your existing maturing debts which the Company is trying to manage by securitising its assets.

- IMHO the Company is visibly going in the direction of DHFL and we have Corporate governance issues also in the Company.

Disclosure : Not invested tracking for knowledge gain

1 Like

Value2017 you said, if the company able to raise funds between 9.5 to 10% it will be big positive, Now the company raised money at 9.10 interest rate.

[Indiabulls Housing Finance Ltd] on May 18th announced it has raised Rs 1,030 crore by issuing bonds on a private placement basis. The company on May 18 allotted 10,300 secured, redeemable, non-convertible debentures of face value Rs 10 lakh each, aggregating to Rs 1,030 crore, on a private placement basis, the company said in a regulatory filing.The coupon rate on the bonds with three years tenor is 9.10 per cent per annum (payable annually).

Dear Vishal , Fund raising is not a one time affair but a continuous exercise for NBFC. So if they are able to raise fund then why would they securitise the assets. Generally NBFC lend to developers comfortably above 12%.

So if you are able to raise fund at 9.10% then why would you sell your portfolios which are generating more then 12% returns.

1 Like

The current rate of interest being charged on retail home loans by India bulls is 10% and I believe they must be cautious by not extending loans to builders currently. The recent raising of funds may be to meet immediate liabilities.

So, Gagan Banga has been saying that Indiabulls moving forward do not want to compete with banks but rather enter into tie-ups with banks and co-originate most of the loans and then sell them to the banks. Maybe this is part of that strategy?

Discl: ~15% of portfolio invested.

That is not a ‘strategy’, it is the only option available which almost all NBFCs have been taking, with lack of funds, to co-originate loans with Banks!

2 Likes

Could you elaborate on cogeneration with banks ?what exactly it means? Who sanctions the loan initially? Is it the same like bundling the loans and selling to banks else how it’s different? If banks take over the loans, who absorbs the risks?

Sorry, bit lazy to type, searching for “co-originate loans with Banks” throws up some good links:

1 Like