So does that mean he is hopeful of reviving the business? Or is it just to fool the current stakeholders?

IBulls went to court to restrain ICRA from revealing their credit ratings. What does that imply?

Disc: Invested and one of my larger holdings

So does that mean he is hopeful of reviving the business? Or is it just to fool the current stakeholders?

IBulls went to court to restrain ICRA from revealing their credit ratings. What does that imply?

Disc: Invested and one of my larger holdings

Why promoter gone to court against rating agency to prevent release of downgrade of the rating? Looks surprise!!

Sameer has opted for Nil Salary and Gagan opted for 75% salary cut. On an average senior mgmt opted for 35% cut

Good action. However, overall integrity of the promoters depends on their landing quality and siphoning of money at backdoor (Rana Kapoor). Salary is very small amount compare to other means to get money in pocket. Promoters are buying shares from open market and taking cut in salary - are these to encourage retail investors (confidence building) or to hold the share price from crash till someone exit safey?? I do remember that Rana Kapoor was telling Yes Bank Shares are diamond and will never ever sell it!! ( Yes Bank shares: Diamonds are not to be sold: Rana Kapoor's dig at co-founder’s family - The Economic Times )

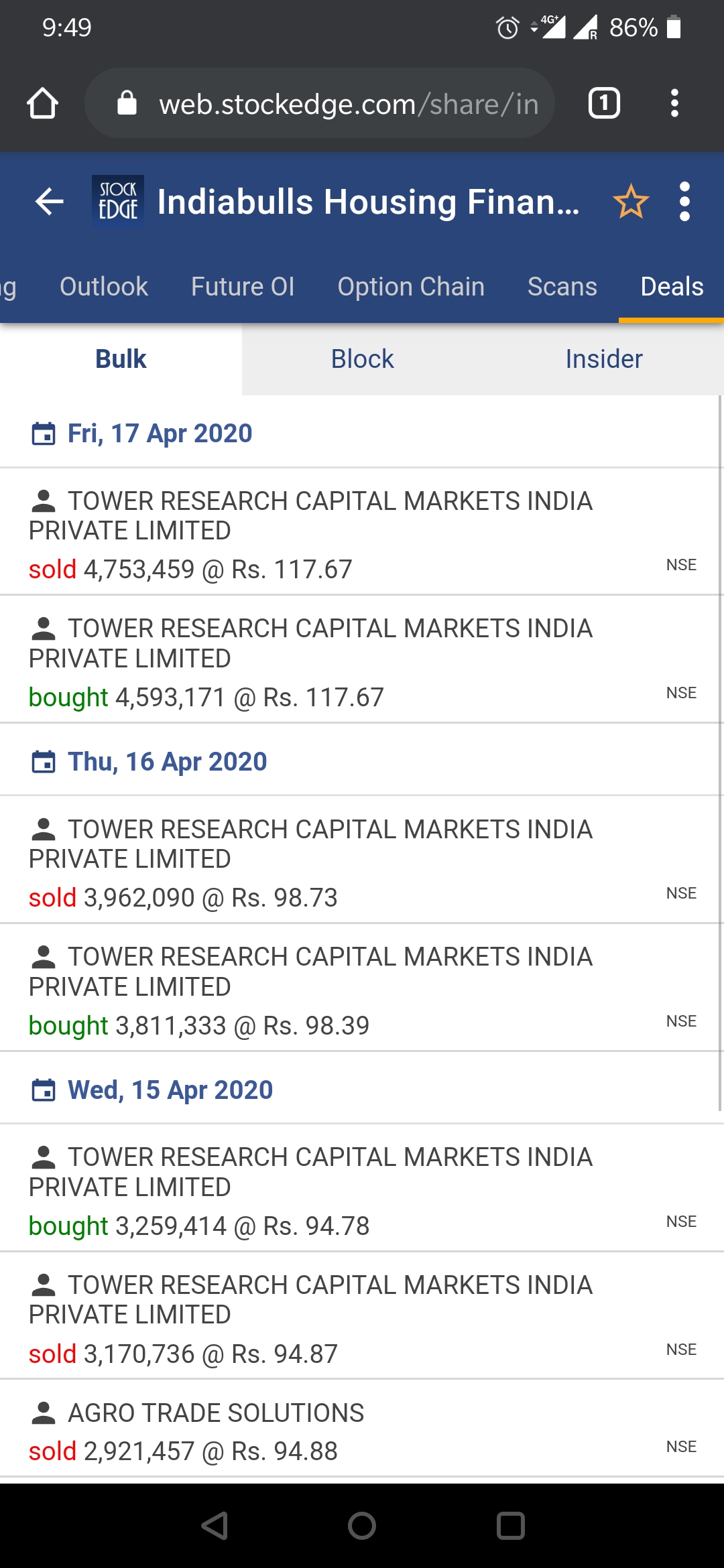

Do anyone know about Tower Research Capital ? This FII is known for high frequency trading in stock market.

When they play high frequency trading at very high volume, stock normally remain only buyers or only sellers range. Retail investors get trapped in such eyewash ‘only buyers’ and buy shares at high price. I just analysed few trades by Tower Research in Indiabulls. Their buy bulk deal is smaller than sell bulk deals keeping stock price artificially higher and sell small lots to retail investors at higher price. Be careful and stay away from such stock to protect your valuable capital. You will not find Tower Research name in their shareholder list as ideally they are high frequency day traders working for other FII / Promoters for their safe exit and dump it to retail investors!!

More on Tower Research Capital - bad name - paid penalty!!!

Another red flag is dividend payout ratio. It is very high ~50% for an NBFC (In year 2016, payout ration was 81%!). Why an NBFC pay very High dividend where as money is main raw material for their growth. Why don’t you doubt an NBFC which distribute 50% profit to their shareholders and borrow money from market by paying 8-10% interest for business growth? Is this to keep shareholders happy for ‘short-time’ untill crisis unfold like DHFL!!

Disc: Never touch such company ! I follow rule no 1: Never lose capital!! (I may be proved wrong in my analysis but just shared to protect capital of fellow investors!!)

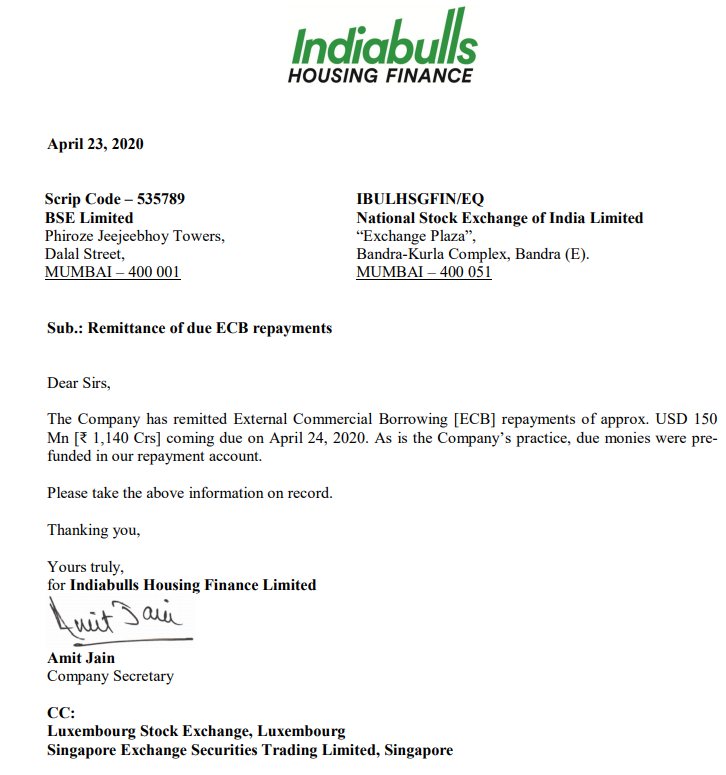

The Company will now face challenges in roll over of its maturing NCD and bonds. As per available information in spite of TLTRO by RBI the situation is very tight for high rated bonds also.

There is total risk aversion and in this time I do not think that it will be easy for Indiabulls to roll over its maturing liabilities which will eventually lead to liquidity crunch. If roll overs of existing debt are not happening

forget about new credit lines.

The stock has fallen from 52 W high of 846 to low of 85 and is now trading at 125. It is amply clear that stocks do not fall 85% without any reason and time and again it has been proved by stocks like Yes Bank, DHFL,Manpasand Beverages, P C Jwellers,Vakrangee, 8 Miles… and there are various others in the list. I was always tempted to buy at such steep falls but this forum taught me how to restrain.

So for me the writing is on the wall and its a clear NO GO for any retail investor.

Disclosure : Not invested in IBHF or any of the above mentioned stocks but following for learning You do not need to make mistakes to learn but you can learn from others mistakes.

Though there are lot of red flags. One positive which I got from rating analysis document that company is moving from Big ticket loans to retail finance and affordable housing sector. Need to track the changes closely

This statement you will find in most of NBFC con call now a days!! But what about big tickets loan they have already on their books? Exponential loan growth of past is due to their big ticket loans only, which could not be achieved in small ticket loan!! One big ticket loan default could Wipeout profit. Small tickets again now crowded place and have intense competition.

In my opinion it is too little and too late…you can follow the last 2 to 3 concalls of DHFL whereby they had also made similar statements… its not easy to recover big ticket loans (in the current scenario) which they have already disbursed to real estate developers…

One thing to follow for existing investors is how efficiently they are able to infuse new capital, get new credit lines and roll over their maturing liabilities.

If they are simply burning their existing cash to pay of liabilities then this will probably not last long.

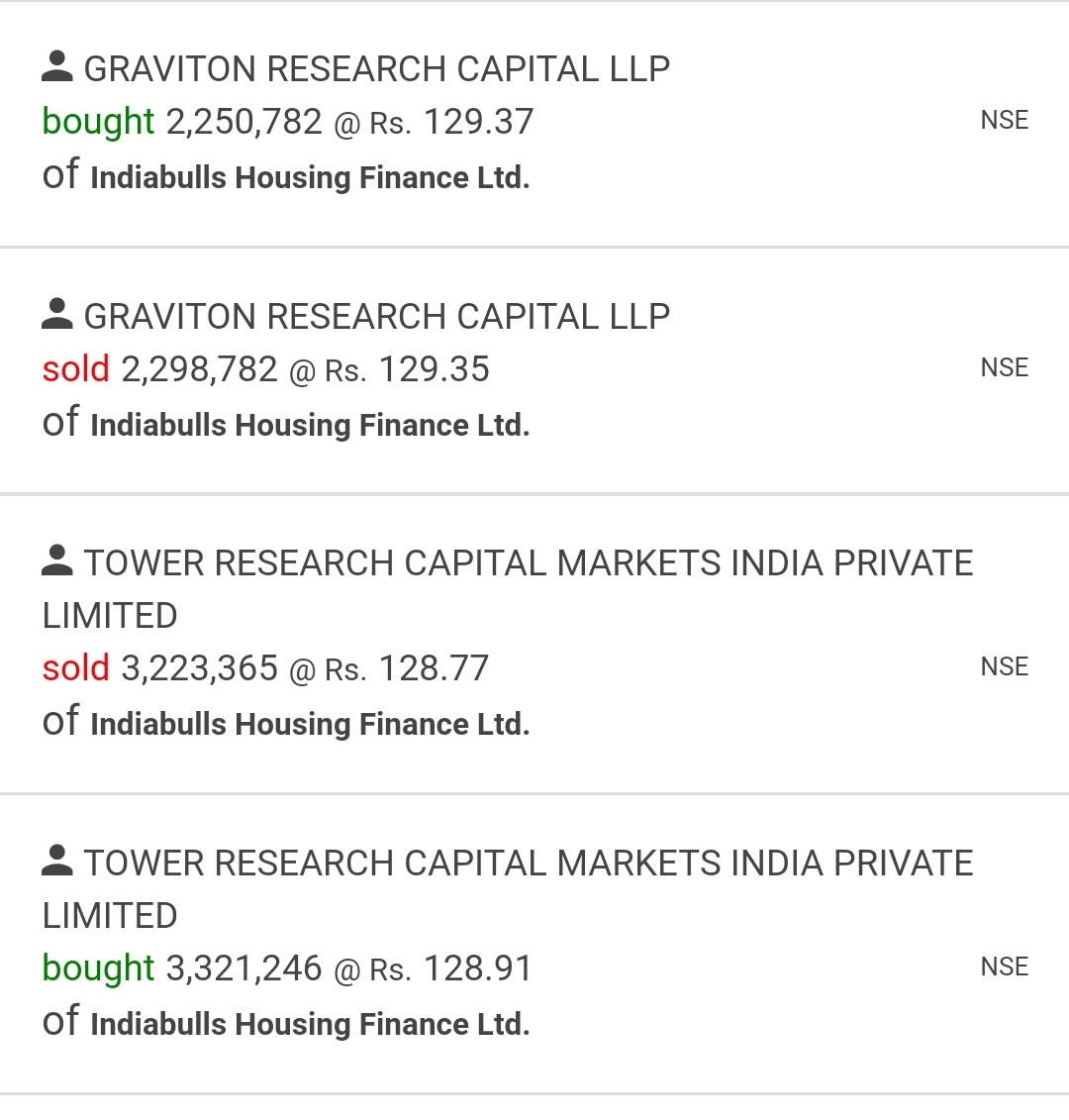

Another high frequency firm joined today for Indiabulls housing finance : Graviton Research Capital LLP refer today’s bulk deals.

Overall, in April more high frequency traders

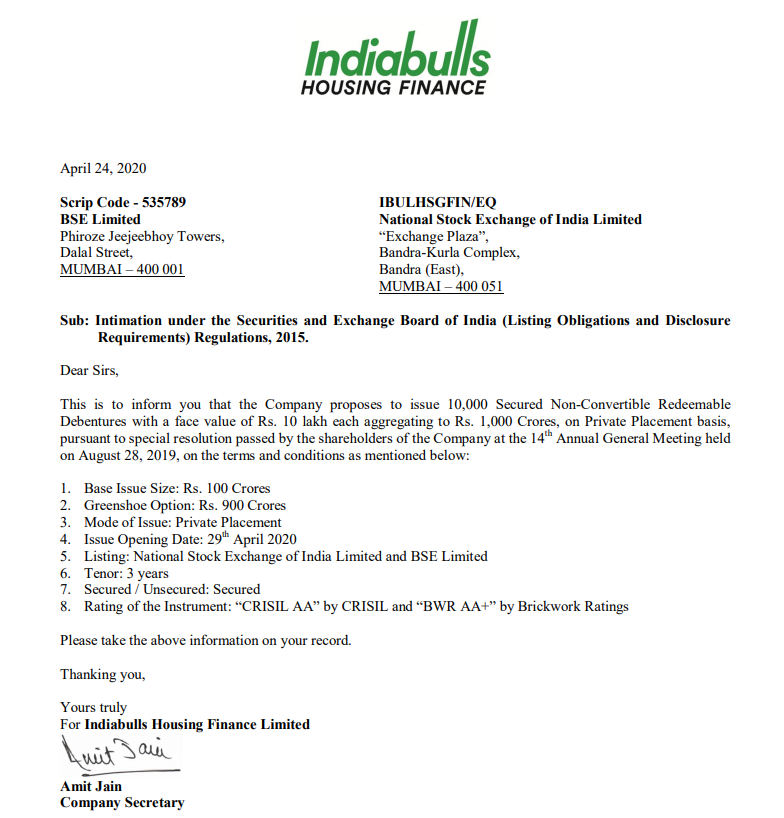

Lets see at what interest rate they are able to raise money? Will it be fully subscribed?

In my opinion If they are able to raise money at a ROI below 9.5 to 10% it will be big positive…

Liquidity raised from equity dilution is better than raised from borrowing money from market!

For Bank / NBFC … velocity of money is important… (Lend fast and more, collect efficiently and lend again)…if company borrow and not able to lend or not able to collect efficiently and lend again…it is negative for any Bank/NBFC.

Till date many NBFC and low grade Private bank were able to show top and bottom line growth by playing only half of the money velocity cycle i.e. borrowing fast and lending fast …but failed to recover money effeciently…this is landmine/explosive situation as it will destroy company by higher NPA and Higher provisions . !!!.

Sometimes investors fail to recognize quality of growth of balance sheet… companies playing half cycle only could show excellent top and bottom line growth by wholesale lending to poor guy who must pay higher interest rate. By lending poor guy at higher interest, company could show excellent growth in top and bottom line in first half of the cycle but go bankrupt in second half. We have examples…Yes bank, DHFL, PNB, PNB Hgs Fin, Indiabulls Hgsf…many are in pipeline!!! Investors who has extra ordinary skill / luck could make lot of money by entering at start of first half and exit at end of first half cycle!! But many are in loss as they buy when growth at peak (end of first half) and remain invested!! Only few has such skill like Basant M (who entered and exited PNB Housing Finance on right time!!)

I consider Indiabulls Housing Finance is the second largest housing finance company run by competent management(Mr Sameer Gehlaut is IITian from Delhi, It gives high dividends, Promoters bought Millions of shares recently from market, Its Price fell due to rejection of bank merger which in turned made negative sentiment for lot of investors about investing on this company. Bank merger rejected by RBI to false PIL filed against them in court. But these are blackmailing gang who filed fake PILs in high court, Indiabulls already got clean chit from Ministry of Home Affairs and Reserve Bank of India. I remember 2018 when its stock was very 1400 Rupees and it is use to called a very strong and fundamentally strong But now this is available at throwaways price now. There is proverb by Stock maket Guru’s “to make good money in stock market try to grab a fundamentally strong stock which is facing temporary problem”. Is this that stock ?

Hi i dont agree with you.

There were issues with the Company in the past also. The promoter lacks credibility. Further for an Nbfc to give such a high dividend is not all right. The money could have easily invested in the business.

Please note that no share falls 90% without any reason

How are you sure that RBI rejected the merger solely on the basis of PIL filed against them? RBI does not comment on the reasons of rejection. There is a fit and proper criteria for promoter/directors of banks. Don’t forget that RBI kept pulling up Yes Bank for their divergence lapses and did not extend Rana Kapoor tenure. So they are aware of the going-on, maybe slow and late to react but sure to react.

“The affidavit makes it clear that many of the allegations could not have been investigated by the central bank since the information was not available with the institution but to suggest that the RBI gave a “clean chit” to Indiabulls is highly misleading. On the contrary, many of the observations and allegations made in the writ petition have been found to be true by the Reserve Bank of India.”

As a rule, I stay away from promoters having a link with politicians.

https://www.newsclick.in/The-Maze-of-Political-Links-of-Indiabull-Sameer-Gehlaut

Also when you talk of blackmailing gang don’t forget the company’s conduct: