INDIA PESTICIDES ( Estd - 1984 )

A mid sized agrochemicals company mainly focussed on making AIs ( active ingredients or technicals …akin to APIs in Pharma ). Company makes AIs of fungicides and herbicides. Company also makes a few APIs.

AIs made by the company include -

Fungicides -

Cymoxanil Technical ( to control fungal growth in grapes, potato and other vegetable crops )

Captan Technical

Ziram Technical

Folpet Technical ( used to control fungal growth at vineyards, cereals and as a biocide in paints )

Herbicides -

Prosulfocarb

Thiocarbamete family of Technicals ( used on paddy and wheat crops )

APIs made by the company include -

Anti Scabies drugs

Anti Fungal Drugs

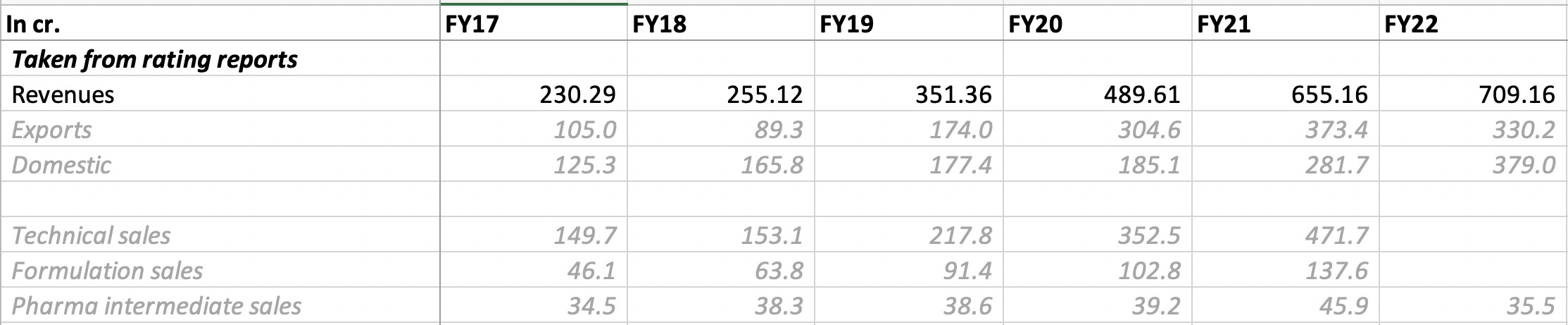

Contribution of AIs to the total sales at - 506 cr out of 648 cr

In addition, company makes and markets a variety of agrochemical formulations ( which also include a few insecticides , growth regulators and acaricides). Some of these formulations have the benefit of backward integration as the company would be making their AIs in house ( as brought out above )

Contribution of Formulations to total sales at 135 cr out of a total of 648 cr

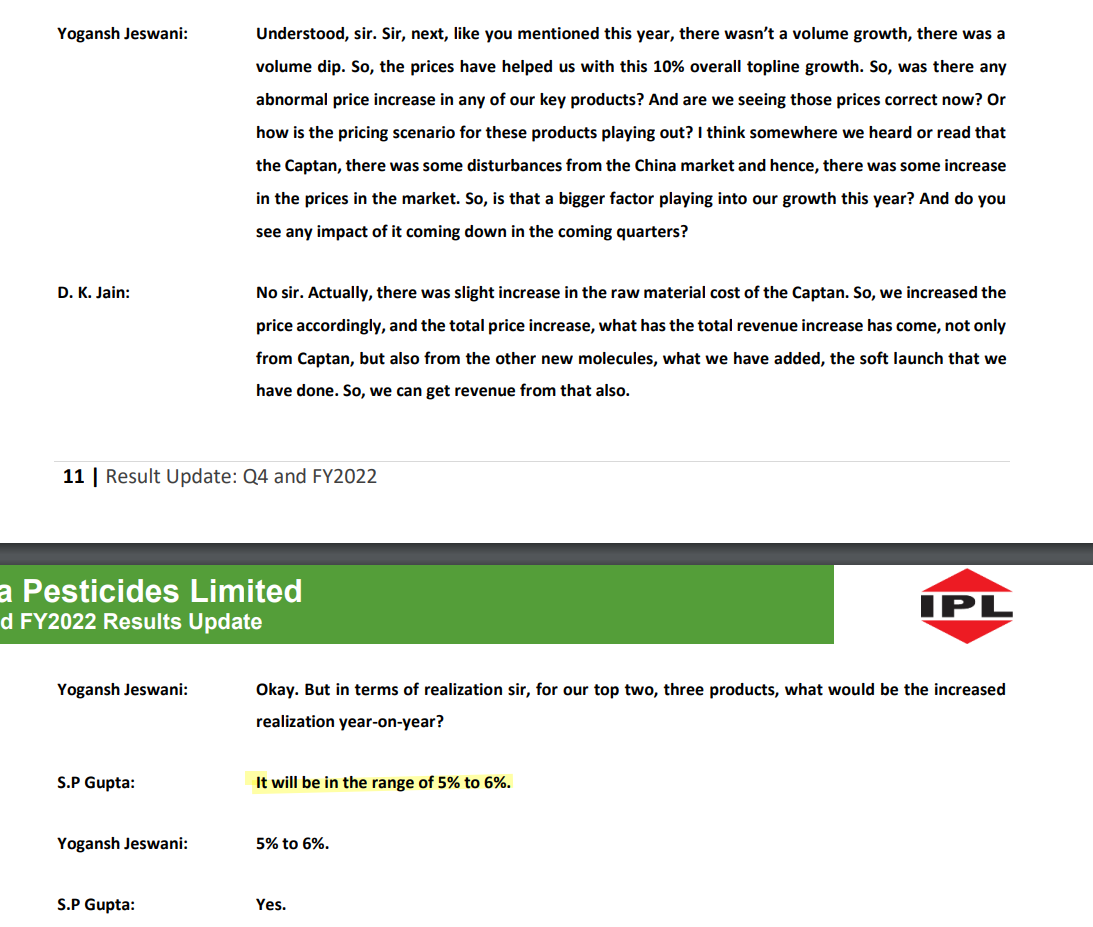

Company is the sole maker of 5 AIs in India and is one of the largest maker of Captan, Folpet and Thiocarbamate globally in terms of volumes.

Manufacturing facilities -

Two facilities- Both in UP

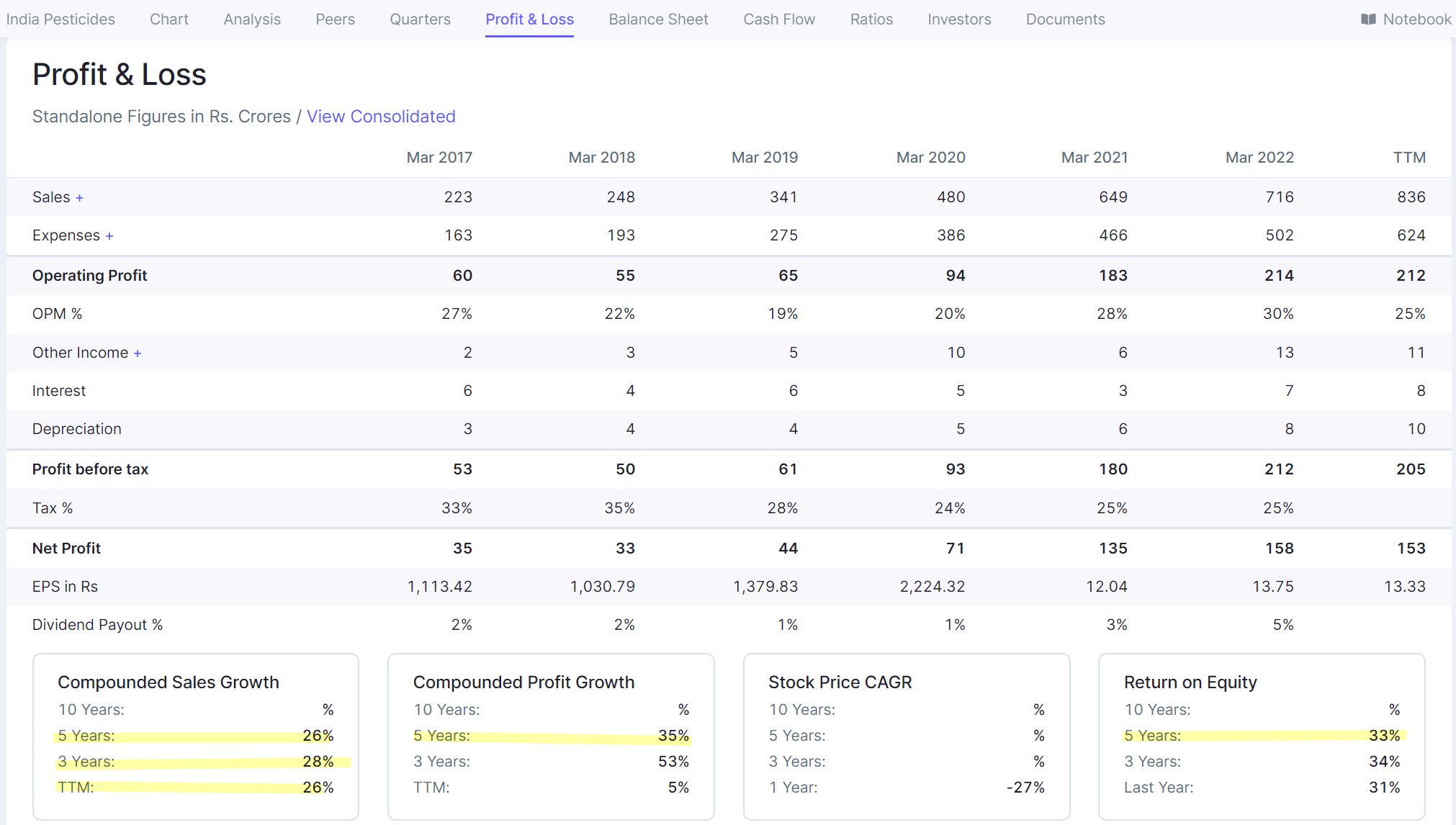

Current financials- Year ending Mar 21-

Sales - 648 cr . Last 5 yr CAGR of 23 pc

EBITDA - 189 cr. Last 5 yr CAGR of 29 pc

PAT - 134 cr. Last 5 yr CAGR of 57 pc

Mainly a B2B company. Has long term relationships with various multinationals. Key clients include - Syngenta, UPL,Conquest Crop Protection, Sharda Cropchem and Stotras.

57 pc of the total revenues currently driven from top 10 customers.

Current capacity - 19500 MT for AIs, 6,500 MT for Formulations

“Emergence of India as favourable manufacturing hub on account of trade Tensions with China has spurred the demand for indigenous offerings in agrochemicals” - Said Mr Agarwal ( Chairman ) in the AGM

Company’s plants have effluent treatment plants, warehouses and other essential arrangements for reducing effluents and hazardous waste generation.

AIso worth $4-4.5 billion are expected to go off patent by 2026. Company is focusing on this space along with their constant endeavour to expand their geographical footprint and customer base.

Key focus areas of the company -

Improvement in production processes

Improvement in quality and purity of current products

Undertake pilot studies to make new AIs to finally make them for their customers

The company reported an EBITDA of 183 cr and NP of Rs 135 cr for the Last FY. The EBITDA margins were at 28 pc LY. For the last 02 qtrs ( when most companies are struggling with input cost pressures ), they have reported EBITDA margins of 32 and 31 pc respectively. Combined NP for last 02 qtrs has been Rs 84 cr.

Company’s present mkt cap of Rs 3800 cr doesn’t look expensive. Plus the kind of margins that they are reporting definitely warrant further inquiry.

Another thing that’s quite interesting is that their margins are way better than even PI Industries !!!

Surely, they must be doing something that probably others are not. The only thing that comes to mind is - greater degree of backward integration ( something like Divis for their generic molecules )…but that’s only a guess.

Key risks - fall in margins going forward. Clearly, the current margins are really rich. We need to dig deeper as to how is the company able to generate such good margins and how sustainable are they.

Key triggers - Mkt recognition of their Industry leading EBITDA margins.

Consider this - their EBITDA margins for last 5 FY have been - 27 pc, 22pc, 19pc, 20 pc, 28 pc

The same for peers are as follows -

PI Industries -

24 pc, 22 pc, 20 pc, 21 pc, 22 pc

Rallis India -

16 pc, 15 pc, 12 pc, 12 pc, 13 pc

Insecticides India -

11 pc, 14 pc, 16 pc, 11 pc, 11 pc

I really think we need to get to the bottom of this secret sauce that’s giving them Industry leading margins. Surely, this will come up as the company conducts its next concall.

Excerpts from management commentary provided on CNBC on 21 Dec 21 -

(a) Capex of 70 cr likely to be commissioned for this FY

(b) Capex of another 70 cr likely to be commissioned in the next FY

(c) Expecting an asset turns of 2-2.5 on the same with similar margin profile as the company is presently enjoying

(d) Capex of 350 cr lined up for FY 24 …again with similar margins and asset turns of 2-2.5

(e) Company likely to clock revenues North of 700 cr this FY

(f) Revenues likely to hit 1000 cr in next 02 years

(g) Revenues likely to cross 2000 cr inside 04 yrs from now after all this new cumulative capex of 500 cr goes online

Attaching the video for reference…

Well…to me, this looks like a rare high growth, low risk, moderately priced bet in an otherwise richly valued markets. Could not find too many negatives about the company except for the fact that I am yet to fully comprehend the reason behind their Industry leading margins except for process efficiencies, careful product selection, tight cost controls etc

On Corporate Governance - nothing adverse that I could come across. But yes… it is always a work in progress.

Views are welcome … Specially the counter views.

Regards

Ranvir Dehal