@ayushmit Ji, What is your impression on the performance of the company based on your Plant visit on March 16, 2023. What will be the impact of El Nino phenomenon on the company. Thanks for your contribution to this thread.

1 Like

Nuvama site visit report attached.

File_1679731629818.pdf (447.0 KB)

6 Likes

Thank you for your response.

Regards.

Raj

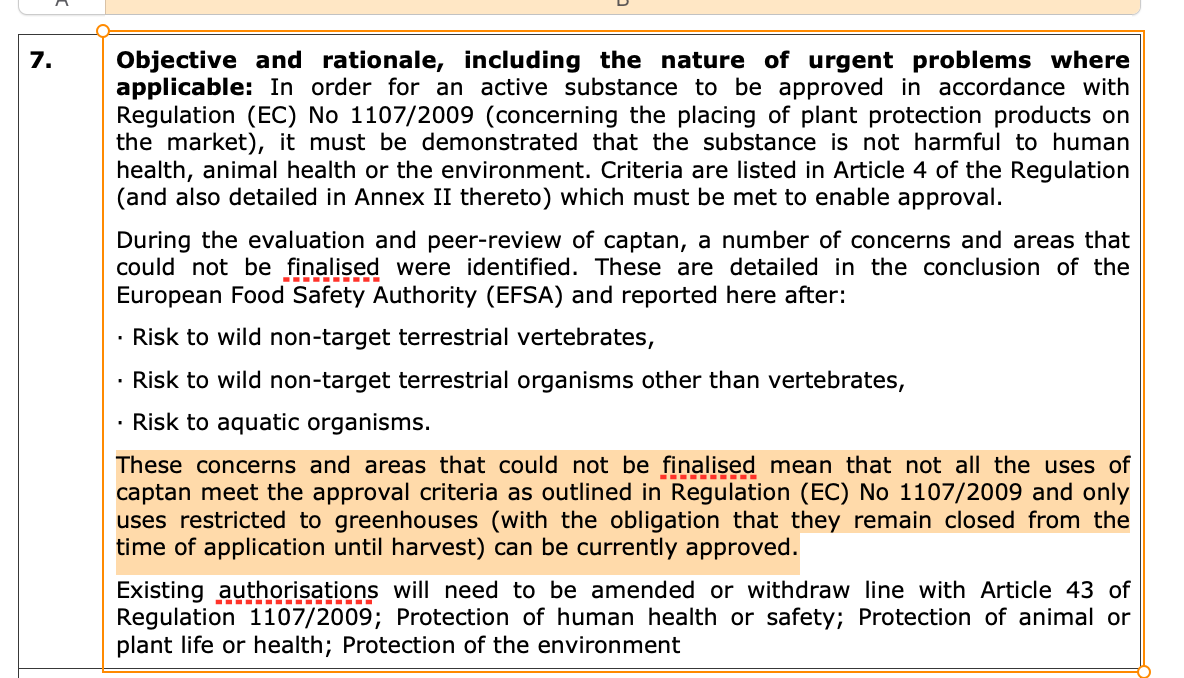

I was searching EU ban on export products, and found the following for captan. The document is from September 2022, but the proposed (partial?) ban is from Q1 2023. Financial year = Calendar year in EU so it may show a little impact starting Q4 23. Irrespective this is something we must clarify from management.

Link to this document is available here. It would help if someone can dumb down this section about communication between EU and USA regulatory bodies.

3 Likes

India Pesticides Limited Q4 FY23

Results in line with expectations.

Revenue up 23% YoY for FY23

EBITDA margin at 22% vs 30% YOY for full year.

Highlights from Q4 concall

![]() In advance talk for collaboration with Japan based Pharma company for API

In advance talk for collaboration with Japan based Pharma company for API

![]() Received registration for Thiocarbamate product in US. Expecting 50cr sales.

Received registration for Thiocarbamate product in US. Expecting 50cr sales.

![]() Headwinds continues globally. High cost inventory is still a concern for next 1-2 quarters.

Headwinds continues globally. High cost inventory is still a concern for next 1-2 quarters.

![]() 110cr capex planned for FY24

110cr capex planned for FY24

![]() Will be able to maintain current EBITDA margins of 21% and improve from here on in next 2-3 quarters.

Will be able to maintain current EBITDA margins of 21% and improve from here on in next 2-3 quarters.

5 Likes

My notes from the last two concalls are below. IPL has been able to do good growth in sales, however margins have been lower due to raw material and power cost inflation.

FY23Q3

- Hamirpur commercialization will happen in FY24, as plant must be operational in FY24 for tax benefits. Will start with intermediate manufacturing as it doesn’t have much regulatory requirements

- Not facing any demand problems

- New product contribution was 25 cr. this quarter, expect 250 cr. from incremental capacities in FY24

- New product contribution: 12% of sales in 9MFY23

- 8% volume growth + 8% price growth in Q3FY23

- Major competitors are based in Israel, very limited Chinese presence in their molecules. Customers are unable to increase product prices, but pricing have been very stable

- Export increase was driven by expanding global reach and customer base

- Have not completely used the high cost inventory, it should be consumed by Q4

- Not sure of reaching 50% gross margins, expect it to stabilize at 46-47%

- Projecting EBITDA margin of 23-25%

- Capex: 54 cr. in 9MFY23. Will maintain 100 cr. annual capex for next 3-4 years. Expect to maintain 2.5x fixed asset turns in incremental capex

- By FY24, can easily reach 1000-1100 cr. sales

- Technical volumes this quarter: 4000 tons (vs 3900 last year)

- Rice husk cost is around 850-900 currently, still carrying some high cost inventory

- Major portion of new herbicide sales will start coming in Q1FY24, must build inventory for that as it’s a Kharif product

- FY24: will launch 4 products

FY23Q4

- Guidance: 1200 cr. by FY25

- Newly launched herbicide received TEQ certification in the European Union

- Obtained registration for one thiocarbamate product in USA (will contribute 15 cr. in FY24 and has potential of 50 cr.). Will be launched by August. Received with a customer who started working with them in last 4-years

- USA currently contributes 30 cr.

- FY23 product launches: 10 formulations + 3 technical + 1 intermediate. New launches contributed 120 cr. to sales in FY23 and will contribute 175 cr. in FY24. New products are import substitutes and faces competition from China unlike current list of products where China is not a major player

- Expect fixed asset turns of 2.25-2.5x on newer capacity

- FY23 capex: Expanded installed capacity in Sandila by 2,500 MTPA to 24,000 MTPA (@ cost of 68 cr.). Running at 70-75% capacity utilization

- FY24 capex: Will incur 50 cr. capex at new plot in Sandila unit (2 blocks; to be commercialized by end of 2023; will have dedicated blocks for new molecules) + 60 cr. in Shalvis Specialities

- Indian Registrations: Received 6 technical registrations and 100 formulations

- Hamirpur: Will commence operations of first plant by Q4FY24

- Looking to supply a pharma intermediate to a Japanese multinational

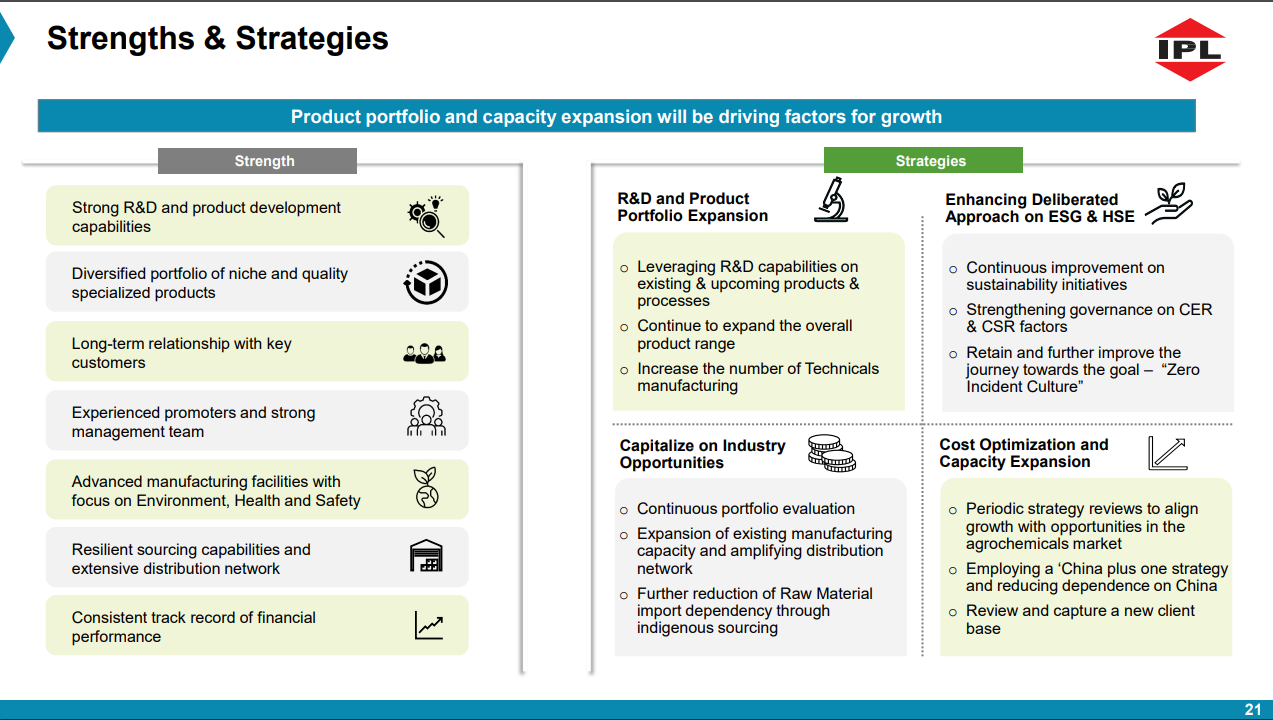

- FY23 R&D: 12 cr. Making arrangements for some vapor-phase reactions, started nitration and hydrogenation. Expanding into stabilizer, additive products, and fluoro specialties

- Have long-term supply arrangements with major customers, based on a formula of conversion cost plus raw material costs adjusted every 3 months. Doesn’t include fuel or manpower costs

- High cost inventory prevails as inventories bought in February have seen 10-12% price decrease by May

- Reason for higher inventory is for a Kharif season product (45 cr. finished inventory)

- Hard to get back to 50% gross margins in near term

- Product ban: Ziram and Captan were not banned in India

- Legal: Out of 9 cases, 2 have been decided in company’s favor. All these are in relation to formulation business

- Captan & Folpet: Adama controls large part of volume, but IPL supplies low quantity to Adama. Very backward integrated compared to Adama, starting from chlorine

Disclosure: Not invested (no transactions in last-30 days)

17 Likes

From recent concalls looks like growth for next too years won’t be more than 12-15%. Plus the margins also would be under pressure for next 2-3 quarters

Bad set of results from IPL, with sales declining by 8% and EPS by 63%. There was really interesting commentary from management about newer products being lower margin (despite having higher realizations). Additionally, these products face more competition from China, unlike their current product basket. There is a material risk for IPL’s longer term margins as these newer products seem more competitive, and maybe company finds it hard to scale back to 25%+ margins. This being said, even 20%+ EBITDA margin is in the highest decile in this industry. Concall notes below:

FY24Q1

- 17 cr. of net realizable value was taken due to sharp drop in prices, 7.3 cr. was sold and 9.8 cr. inventory is still to be sold

- Technical prices dipped by ~20%, expect to grow by 10% in FY24

- Volume drop of 8-10%. New products have higher realizations, but margins are lower as Indian formulators try to offer same absolute rupee margins per kg

- Capacity utilization was lower at 51% (vs 70% in Q4)

- New product contribution was 40 cr. and should be 170 cr. in FY24

- High cost inventory will be consumed by Q2 and hope to get to 20% EBITDA margins by Q3. Current inventory is 190 cr. (from 225 cr. in March 2023). Do not expect any further inventory losses unless there is another round of price cuts

- FY24 capex: 50 cr. for IPL (1 intermediate + 1 technical block + power of 33 KVA) + 60 cr. for Shalvis. Asset turns will be 2.25-2.5x for newer capacity

- Local raw material sourcing increased from 58% in Q4 to 65% in Q1 (of imports, 50% comes from China)

- Newly launched herbicide has started being exported to Europe and plant has been stabilized. It can be “aclonifen”

- Have received 20 cr. order from USA customer for the new thiocarbamate product

- New launches: apart from the herbicide, have launched another product and 2 more products will be launched in FY24. Two technical are import substitute and 1 is for export. Also launching an intermediate for a herbicide they manufacture (backward integration)

Disclosure: Not invested (no transactions in last-30 days)

15 Likes

IPL has announced on 31st August of acquisition of a land adjacent to the Sandila plant ( ~ 2.83 acres), probably this was one of the reason for the stock to runup in the last week. However upon further investigation from google map, the land does not seem more than 12% of the existing plant.

Realistically, how much will this additional land generate revenue or create scope for debottlenecking capex.

Reference : https://www.bseindia.com/xml-data/corpfiling/AttachLive/f79fa710-3d1a-42a6-b768-e5692f6e4182.pdf

Image 1: Most likely this is the land acquired or land of similar size has been acquired

Image 2: Looking at the green warehouse roof cover, the entire area is under IPL now.

Disc: Tracking the stock.

5 Likes

Hi everyone,

I have been following this company since its IPO days. It has been mostly in downtrend from ~350 levels but the recent up-move with a huge huge volume has intrigued me whether it could be an operator game? Though the company has been maintaining its range of 280-310 after this up-move. Could anyone please share any insights or news which I might have missed (only know about land acquisition for plant expansion)?

Please go through Company Concalls and their commentary is very positive. IPO was at high valuations and maters got worse with War and Supply chain issues/China dumping. Things have stabilized in last quarter and any improvement in coming quarters will lead to significant appreciation as management is going with significant capex.

I got surprised when I heard that IPL export substitutes are at lower margins than company overall and look for same in this quarter.

P.S-Holding tracking position from 220 levels and looking for additions around 270 levels

Saw this interesting thing in Company’s annual report:

Seems company has good political connection… For small company’s event PM of the country came for innaugration

1 Like

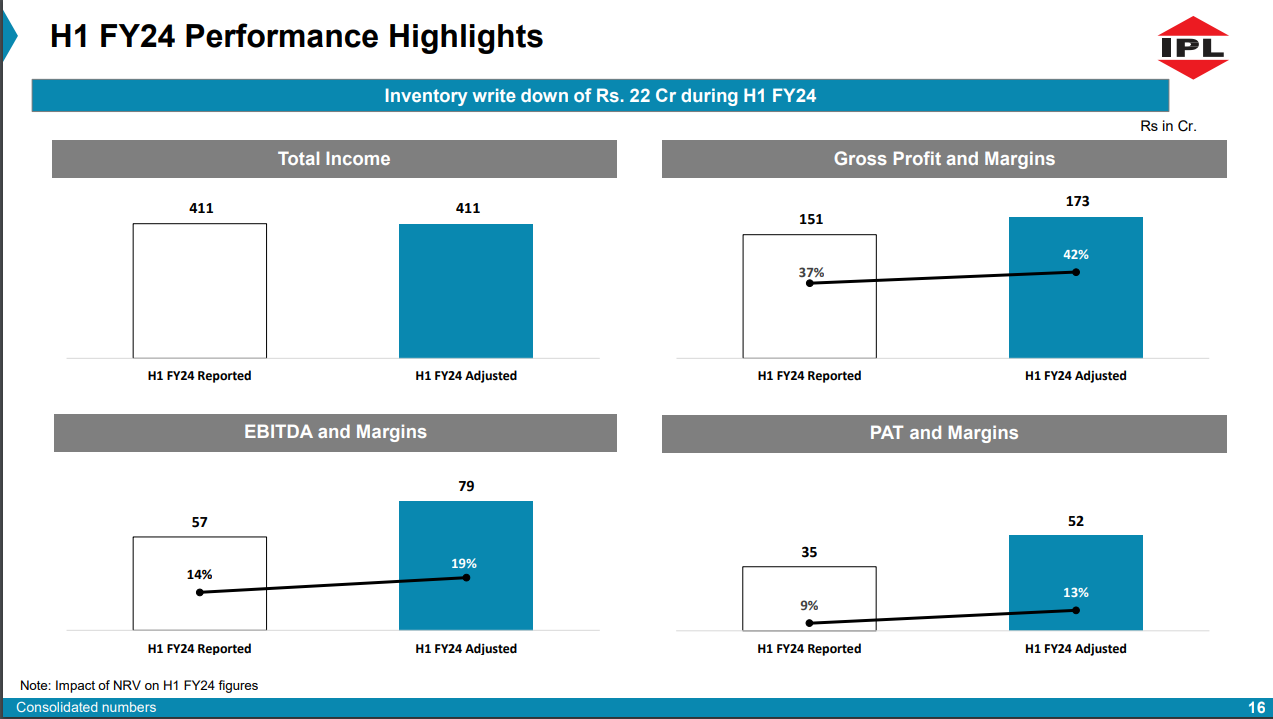

IPL continues to suffer from inventory overhang in global markets, and have pivoted towards selling more formulations in India. They announced setting up a marketing co for formulations in export market, something similar to Sharda Cropchem. Concall notes below

FY24Q2

- Inventory loss of 6 cr. in Q2

- Pesticides I didn’t know they make

o Fungicides: Etridiazole, Dodine

o Insecticides: Diafenthiuron

o Herbicide: Flufenacet - Industry scenario: Continues to face headwinds due to destocking in international markets and price declines resulting from oversupply of raw materials from China

- Domestic formulation: 15-18% EBITDA margin. Export formulation is higher margin but volumes are very low

- LATAM: don’t have direct subsidiary but are present through partners (8-10% revenue contribution)

- Company is planning to setup a subsidiary for marketing formulation in export market in an asset light business model (something similar to Sharda Cropchem)

- For new products, want to maintain 20-22% EBITDA margin & 43-44% gross margin

- Prosulfocarb: very high inventory in end market resulting in volume pressure for IPL

- Expansion

o Intermediate block and technical block will be commercialized in Q4FY24. Will augment production capacity by ~2000 MT

o Acquired land adjacent to Sandila plant for future expansion

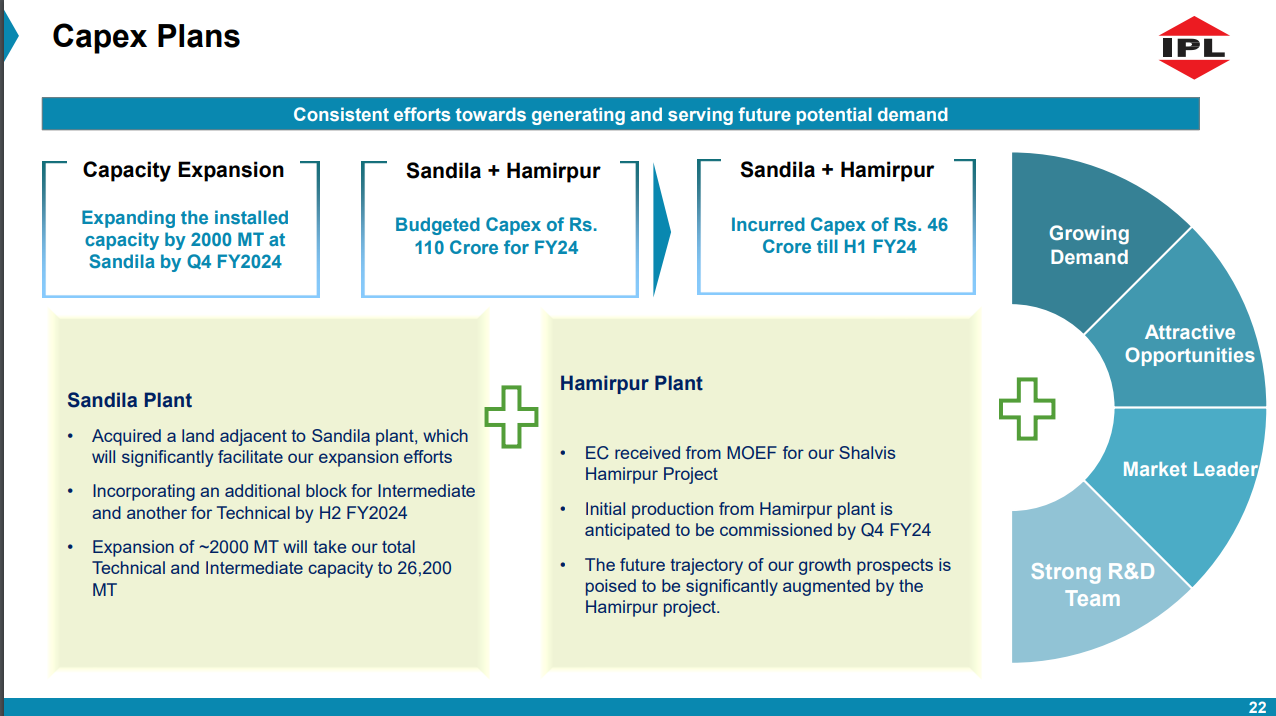

o Have spent 46 cr. in H1FY24 (budget of 110 cr. for Sandila + Hamirpur)

Disclosure: Not invested (no transactions in last-30 days)

4 Likes

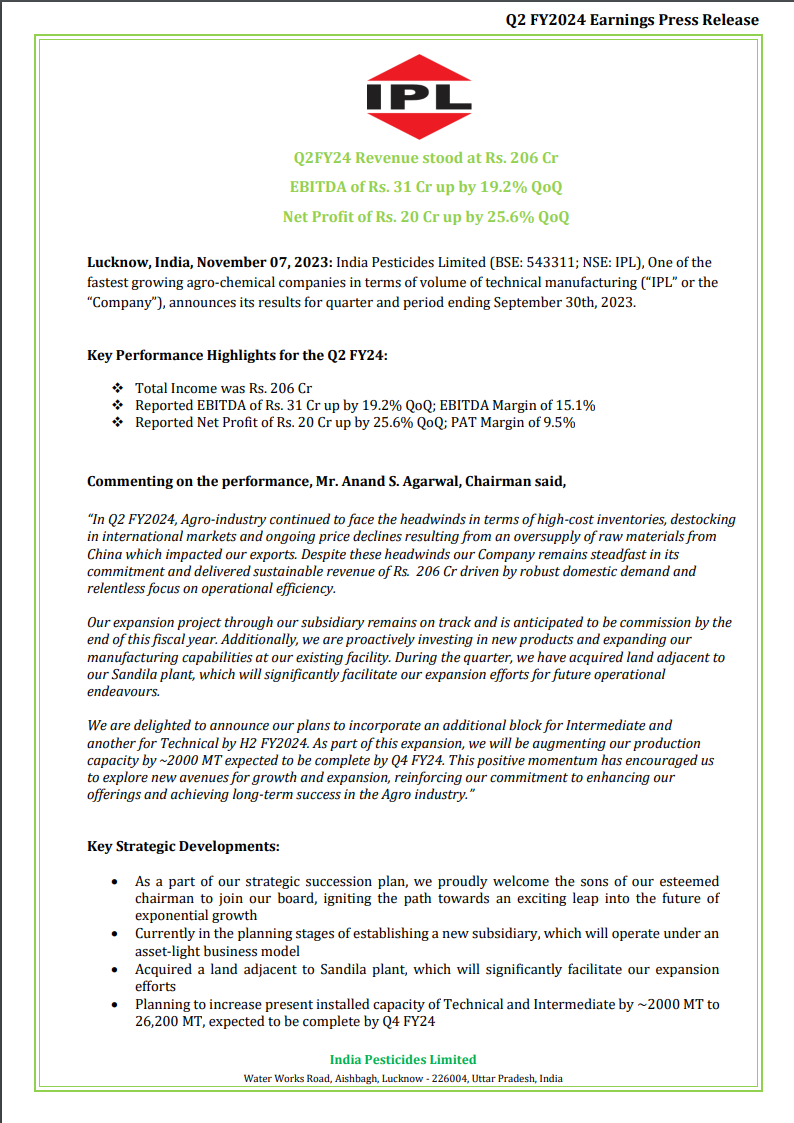

India Pesticides reported its financial results for the second quarter of fiscal year 2024 (Q2 FY24), ending on September 30, 2023. The key highlights are as follows:

- Total revenue for Q2 FY24 stood at Rs. 206 crore.

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) was Rs. 31 crore, showing a significant increase of 19.2% compared to the previous quarter.

- Net Profit for Q2 FY24 was Rs. 20 crore, indicating a 25.6% increase quarter-on-quarter.

- Despite challenges in the agro-industry, such as high-cost inventories, destocking in international markets, and price declines due to oversupply of raw materials from China, IPL achieved sustainable revenue of Rs. 206 crore. This was driven by robust domestic demand and a strong focus on operational efficiency.

- IPL is continuing with its expansion project through its subsidiary, which is expected to be commissioned by the end of the fiscal year. The company is also investing in new products and expanding manufacturing capabilities at its existing facility. In the quarter, IPL acquired land adjacent to its Sandila plant, which will support future expansion efforts.

- IPL plans to incorporate an additional block for Intermediate and another for Technical by the second half of FY2024. This expansion is expected to increase production capacity by approximately 2000 metric tons, with completion scheduled for Q4 FY24.

Key Strategic Developments:

- IPL is implementing a strategic succession plan, welcoming the chairman’s sons to join the board, signaling a transition towards future growth.

- The company is in the planning stages of establishing a new subsidiary with an asset-light business model.

- IPL has acquired land adjacent to the Sandila plant to facilitate expansion efforts.

- There are plans to increase the present installed capacity of Technical and Intermediate by around 2000 metric tons to a total of 26,200 metric tons, expected to be completed by Q4 FY24.

- Capital expenditures (Capex) of Rs. 50 crore have been planned for IPL and Rs. 60 crore for Shalvis Specialities Limited (a wholly-owned subsidiary).

- IPL is exploring opportunities for further diversification into new chemistry.

- The Hamirpur Project is expected to be commissioned by Q4 FY24.

3 Likes

IPL witnessed good expansion in margins due to change in product mix. Volumes were lower by 30% given the industry scenario. Among peers, IPL reported one of the best nos. Concall notes below.

FY24Q3

-

Witnessed 30% lower volumes, blended pricing was same

-

Outsourced conversion of on raw material and paid job work charges of 4 cr. (part of other expenses resulting in higher GMs). Adjusted for this , gross profit margin was 50%. Believe 48-52% GMs are sustainable

-

Entered a 3-year contract with a Japanese company to supply an intermediate

-

Received Technical Equivalence (TEQ) certification by European Union (EU) for herbicide technical product

-

China is putting up very large plants for popular products

-

Expect 15-20% sales growth in FY25

-

Incorporated “Amona Specialities Private Limited” (asset light marketing company)

-

Have spent 60 cr. in 9MFY24 (budget of 110 cr. for Sandila + Hamirpur)

-

Raw material pricing has stabilized

Disclosure: Not invested (no transactions in last-30 days)

6 Likes

It had a brutal fall today.

20% LC.

Was it just the market correction that got extended to this stock, or perhaps some news came out?

Seems a good level to start building, if fundamentals are intact?

2 Likes

Is there any ptice rigging, allegation, or some news pertaining to the counter.

It has been hitting LC consistently for last few days.

I was looking for some news about it. Couldn’t find one.

Is something brewing?

3 Likes

Yes nothing specific is out in terms of news or any fundamental change except for promoters reducing 2-3% stake that too a few qtrs bk, dont seem to make sense of these continues 20% and 10% LCs on the stock.

Unless something is brewing and people with inside info are offloading?

Promoters had allotted shares before IPO at very less price and same was a Red Flag reflected by many analysts on the promoter credibility. It seems market has something on Corporate Governance or some Operator tie up has got exposed resulting into this carnage.

I could not see anything majorly negative in this company apart from above and may take a tracking position at levels below 200.

3 Likes