CBR 3: RISK MANAGEMENT

Basics of Business

The retreading industry thrives on cost benefit against purchase of new tyre. This works for commercial vehicles where speed is not key for driving, for passengers car retreading is insignificant.

Retreading is old practice in India, pretty fragmented due to geopgraphical reach and point of delivery. It is actually the retreading technicians in different town does the job. Indag supplies material to these technicians via whole seller distribution network.

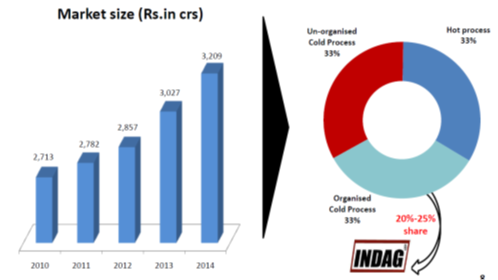

Retreading can be done through cold and hot processs. Cold process is where Indag is engaged into. Of total industry business of 5800 Cr cold process occupies 33%. But a lot of business is un organized. Hence from organized market Indag is market leader having 60-70% share.

The raw material require chiefly is rubber which is an agriculture product mostly cultivated in Kerala. The factory location at Himachal Pradesh has dragged the inventory days higher.

Indag is majorly a domestic seller and buyer.

Customer view

Truckoperators are major customers of Indag via retreaders tecnicians. It’ a well diversified customer base.

Retreading advantage with customer is cost savings on mind. The only factor deters them is safety post retreading. With little incident and low speed requirement of commercial vehicles it is not so dififcult to convince the customer to buy the product. The other way is difficult to win the loyalty of technicians who are front facing ultimate customers. There are plenty of competitors in market but with a distinction. Indag product is cutting edge, the situation where customer switch is further cost benefits. Un organized retreading are further cheaper.

If retreading does not exist tomorrow the cost of maintenance will go up higher for commercial vehicles which will have a cascading effect on products and services managed by these vehicles. Retreading also environmental friendly in terms saving energy used for an alternate new tyre, the government will keep promoting.

Supplier View

Rubber is the chief raw material. Limited players available in India, however can be imported as well.

Key Risks

Management has not specified any risks to be looked upon.In absence I tried to apply the known risks for industry:

Alternate mode of transport- rapid urbanization will be supported by metrol rail and other means of transport. This will impact the passenger car tyre business. However goods carried by railway will impact.

Increaesed power among suppliers- import of rubber have a healthy trend. Unlikely suppliers will dictate the game.

Shifts in technology- retreading technology is not proprietary. Hence any change in technology by the scholars have to be bought by all.

Emergence of competitors- yes there is a risk with low capital investment required it can be a threat. What a new competitor may find is unattractive margins, and deal with tireless end users.

Limited geographic distribution- no, customers are spread across.

Over reliance on too few customers- no, diversified customer base.

Porter five force

Bargaining Power of Customers: plenty of sellers, customer have lots of option to choose.

Bargaining power of suppliers: rubber prices are commodity driven with plenty of choices available from outside as well.

Competition in the industry: though many players are there the competition is concentrated with Indag having a major share in cold process retreading.

Threat of substitute products: All alternate source of transport. Saying that Road carrier is last door mile connectivity, it will retain in its niche place at least in shorter distances.

Threat of New entrants: bit low, as it doesn’t attract high organized players due to superior margin though low capital intensive. But unorganized players will have their presence considering their connectivity and penetration.

Impact of Inflation

Price increase ability- not much

Cost reduction- yes (inventory)

Low capex requirement- yes

One off revenue against recurring

Retreading is reusable product but with a life cycle restriction.

Overview of Company financials

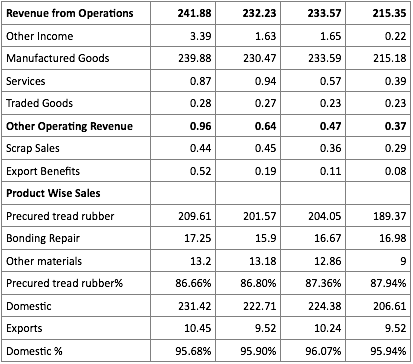

The main source of revenue for Indag rubber is selling of manufactured goods. Within the spectrum of manufactured goods precured tread rubber have a lion share almost 85-90%. The other income seems to be on rise with higher interest and dividend income. Yet very small portion of total income around 1% of total income. Domestic sales are around 95% plus.

On expenses side Indag pays for raw material, which are carbon black, rubber and chemicals. Apart of raw material employee expenses, packing expenses, power and fuel, freight are some of more spent expenses.

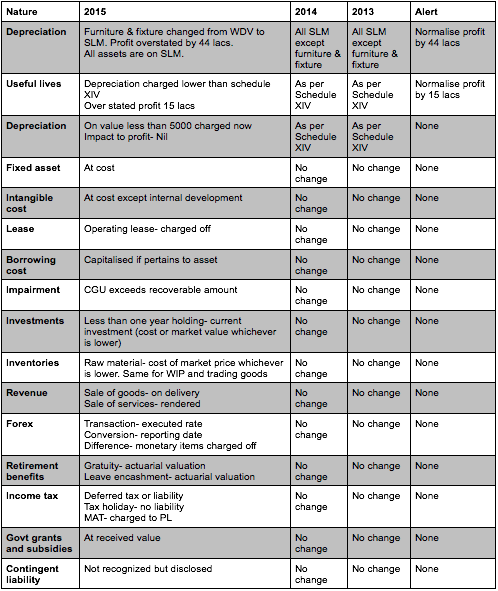

There is a change in method of depreciation which has dragged down the depreciation amount but insignificant.

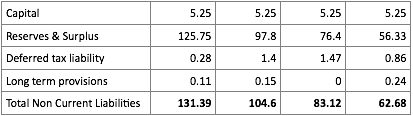

Indag does not have debt except it paid small money to income tax department as interest on tax due.

Indag doesn’t have any long-term liability. Completely shareholder fund is used.

Fixed asset and current assets are key component, which are funded by current liabilities and shareholder.

Most of adjustments to cash flow has been dividend, interest and depreciation. There is no unusual item.

Key takes away from financials:

Indag gross, operating and net margin is on rise year after year. This can be seen in reduction of lower operating expenses.

In terms of SG&A spending Indag doesn’t have much allocation.

Balance Sheet

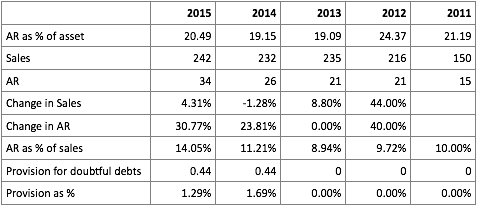

Accounts Receivables

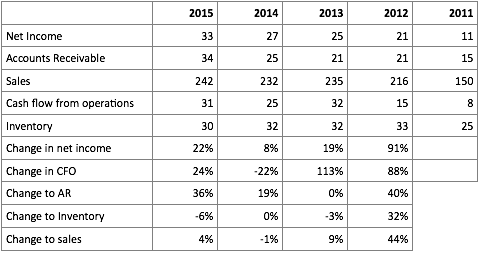

AR as gross exposure to total asset remain range bound except last two years where it moved up to 14% of sales. Whether this increased brought any issues:

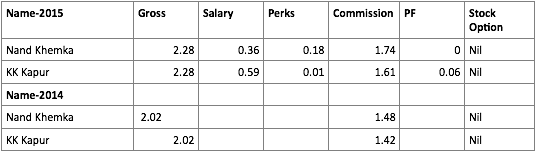

Provision was nil previously, 44 Lac could be seen from 2014. …Appears to be single customer as become static in 2015. This is around 1% of AR, 99% of AR is good and healthy.

The AR balance is rising bit faster than sales. As I could notice sales have stagnated around 200-250 Cr during last four years. Perhaps to retain customer extended credit period has been given.

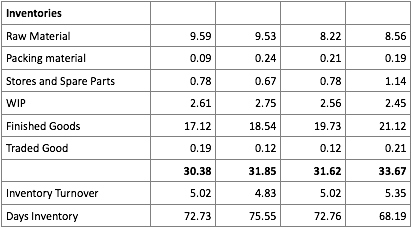

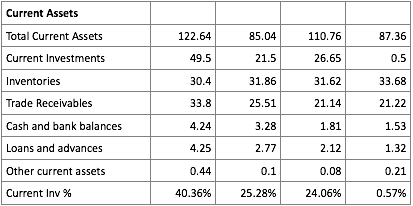

Inventories

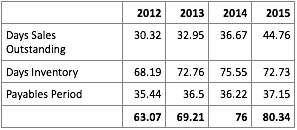

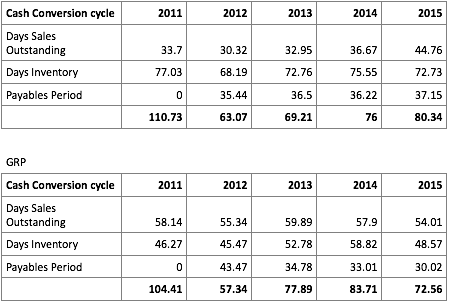

On and around inventory days is 65-75 days, 8-10 comes from ordering cycle as raw material is available in far south where as the factory is north India.

There has been no improvement or deterioration in inventory.

Among other current assets the current investment has increased from almost nil to 40% now. These are investment mostly in debt mutual fund with short-term liquidity period. The free cash flow has been pumped into market instruments.

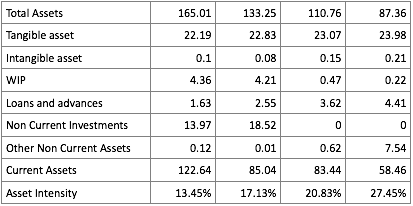

Non Current Assets

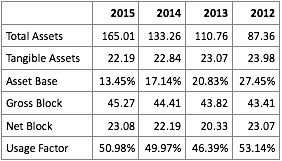

Tangible asset portion has been going down from 27% gradually to 13% at the current moment. This means there has been no capital expenditure in past four years. We know the current expansion will end in April 2016. However the company is not capital intensive.

The non-current investment of 14 and 18 Cr during 2014 and 2015 is outcome of strong free cash flow, which is invested in bonds, shares and mutual funds.

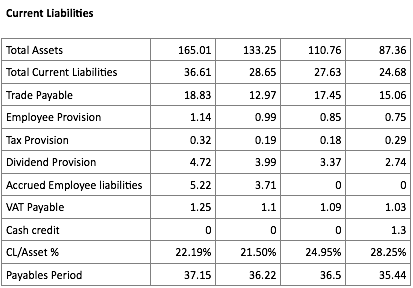

As the sales increase along with free cash flow, with little capex requirement Indag has managed to pay off short-term debt of 2012. The current liability share has been reduced to 22% from 28% of total assets. This is despite higher commission payment to directors. The decrease is mainly on account of increased total asset and constant current liabilities. This can be seen with constant payables period.

There has been no long-term debt what so ever; the entire funding has been given by equity shareholders all along. Indag enjoys entire capital from equity.

Profit & Loss Account

Revenue

Revenue recognition policy:

Sale of goods- Delivery of goods.

Sale of services- when services are rendered.

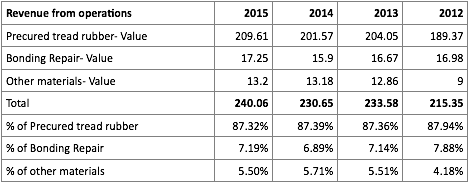

Indag rubber earns 87% of revenue consistently from one product i.e. precured tread rubber. Also non operations revenue has been insignificant till date.

Indag sells maximum of its products in domestic market around 96%.

Cost of goods sold

The direct expenses have been decline from 72% to 64%.

Gross Profit

Indag has been able to mark up from 28% to 35% over last four years.

Other (Selling, General and Administrative) Expenses

Indag has been spending higher and higher money. However this is the section of other expenses, I didn’t come across any major advertisement or sales commission spends. Difficult to confirm whether this additional spend has resulted additional mark up.

Depreciation and Amortization

The impact of depreciation on net income has been diminishing from 9% to 5% over 4 years.

Non recurring charges and gains

There is no non-recurring charges or one time gain as reported in financials or foot notes.

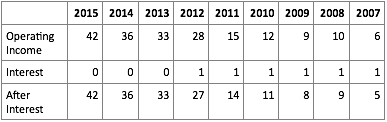

Operating margin has increased from 13.08% to 17.35% over four years.

Interest Income and expenses

Insignificant amount.

Taxes

The corporate tax rate in India is around 35%, with surcharge around 39%. Indag is enjoying tax advantage; even competitor is paying more than 30%.

Net Income

Both net income in terms of value and percentage have gone up.

Cash flow from operations

As the net income increased, the cash flow also increased. This shows the ability of company not only to generate earnings but cash as well.

Analysis of Growth Drivers

Revenue of Indag rubber has grown at 19% compounding rate, Operating income 27 and net income 29 respectively.

But the ride is bumpy; during 2013 revenue slow down, even 2014 it went negative growth. But Indag managed to post better operating and net income. Let us understand how?

During last four years in terms of value the key products hold their share consistently. However production and sales quantity are not available to analyze further.

Managed to sell more goods and services?

In terms of value key products has been grown mildly. I couldn’t confirm whether the quantity of sale has increased or not.

Managed to raise prices?

Quantity of sale is not available, so I couldn’t find out whether prices for product have expanded or not. However the expansion of gross margin indicates there may be some price increase. The margin expansion is also due to fact company was enjoying excise benefit for a five year period.

Managed to sell new goods or services?

All three key products have been sharing same set of revenues. There are no additional goods or services cuts into major sharing.

Bought another company

Indag has not acquired anyone during review period.

Quality of growth

The net income has grown almost in line with operating growth. However the operating income growth has gone much of revenue growth. One of the reasons is excise duty exemption at plant. Operating cash flow is even grew stronger at almost 42% CAGR.

Analyzing the profitability

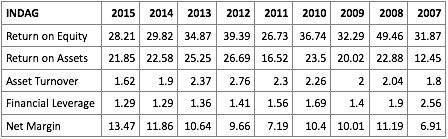

Indag’s superior return on equity is contributed to:

Higher net margin though squeezing asset to sale both guys has been at par, may be GRP is slightly better. The high margin comes partly from excise exemption as well.

Indag is comparatively debt free. Although GRP as well doesn’t carry a lot of debt.

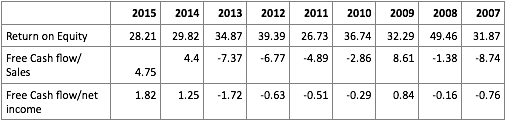

Impact of free cash flow on ROE

Although Indag generated a good deal margin and return on equity it failed to generate a lot of free cash flow. The operating cash flow as we saw earlier has been healthy. Is it the capex then?

Capex has gone through roof even as late till 2013, barring 2 years capex has been around 15% of sales or more. Are these growth capex or maintenance capex I will check later.

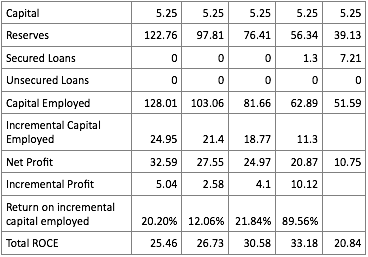

Return on Invested Capital (ROIC)

Indag have nil debt on balance sheet, hence there is not much difference between ROE and ROIC.

With bond rate at 8% and say add another 7% for all risk at higher side WACC works around 15%. The ROIC of 28% provides 13% assurance.

There is a ample chance to increase ROIC as well by reducing inventory holding period.

Financial Health

Indag has no debt, hence financial leverage does not impact returns.

Current and Quick Ratio

Current ratio always exceeds 2.5, what more comfort is quick ratio has gone beyond 2 now. It was always above 1 though.

Return Generated on Additional Capital Employed

It appears the entire capital that is generated from business and retained (reserves) and incremental profit has not delivered the same level of ROE as the original capital had.

The bear case

I have covered the negatives and if but scenarios under “special situation”.

Debt Management

Motivation for debt

With little capex requirement and sufficient cash flow its unlikely Indag will go for debt in near future.

Opportunistic

The company has not utilized free cash flow in increasing R&D or sales promotion or perhaps it is not required.

Growth capex has been minimal also, the company is not capital intensive.

Solvency Power

Indag does not have long term debt or even short term debt. Hence debt equity or coverage ratios need not be tracked for time being.

Current ratios and quick ratios are very healthy as discussed earlier.

Off balance sheet liabilities

A total of 9.71 Cr estimated.

7.93 Cr pertain to entry tax determined under jurisdiction.

Income tax demand 1.59 Cr.

No restriction on lease by tenants.

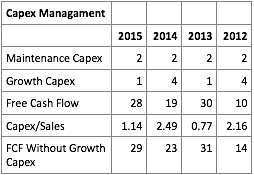

Capex Management

Capex to sales is around 1-2%. This is even with recent expansion. If we remove growth capex Indag generated 83 Cr free cash flow in last four years. Its almost 20% in three years.

The tangible asset base has been going down in terms of total asset base despite of recent capital expansion. Its clear growth capex is not enough to damage free cash flow.

In terms of usage the net block hovers around 50%, this mean management estimation of useful life and maintenance goes hand in hand with operational target.

Short term financial strength

Inventory has been major dragging force behind a delayed cash conversion cycle. Two reasons I guess Indag has fallen behind competitor one location plant is at awful distance from raw material location. Second is seasonal nature of raw material.

On customer front Indag has done exceptionally well.

Long term financial health

Indag has never used debt, always utilizing share holder money. This gives enormous potential to low cost of capital and less risk.

Debt Maturity Schedule

The company have no short term or long term debt.

Financial Integrity

Declining Cash Flow

For two years net income tracked the CFO, for other two years it was fallen apart. During last two years the AR has risen much faster than sales. However inventory has been on declined in last 3 years.

In a nut shell over cash flow has not declined.

Serial Charges

During last five years there has been no one time restructuring charge or unusual charges.

Acquisition

During last five years Indag has not acquired or demerged any company.

Departure of CFO and Auditor

There has been no departure of Auditor or CFO.

Except entry tax liability there has no been audit qualification either.

Provision for doubtful debts

Very minimal amount of 44 lacs has been provided.

Gains from investment

Apart from interest and dividend there has been no other income. In revenue from operations we couldn’t find any one time gain as well.

Employee benefit provision

The actuarial valuations are done by experts, provisions are made as per statute. Company have very little role to play, market linked instruments are not allowed in India.

Over of understatement of expenses

I didn’t found any susceptible cost to analye like R&D, maintetance, marketing etc.

Usage of reserve

The only reserve Indag have is general reserve where the retained earnings are accumulated.

Change in accounting policies, estimates

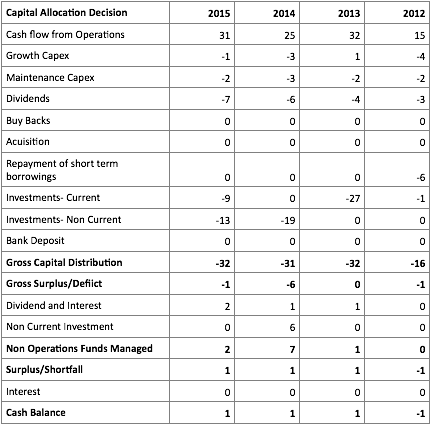

Capital Allocation Decision

Below is the table showing cash generated and distributed:

A bulk of free cash flow has been reinvested to equity, bonds etc. Around 20-25% further distributed as dividend. Even the recent growth capex is minimal. This indicates company is less capex oriented.

The current and non current investments together form 20% of MCAP now.