Off loading Indag Rubber working papers, please feel free to send me questions. I do have some shares in this company but my purchases are back in 2011, this is 2nd refresh document. The investment workings are based exclusively on publicly available information.

First about competitive advantage

Moat Overview

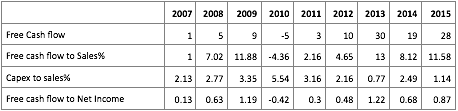

Excellent growth numbers in Sales, EPS and free cash flow. Book value has been mildly erratic as lots of free cash flows invested to bonds and shares. ROIC has been outstanding.

Free Cash Flow:

Except one case Indag has managed to generate a good amount of free cash flow. In percentage with sales last three years saw numbers above 10%. Also we can see FCF clocked more than 100% of net income in few years. Indicates two things:

Indag is able to generate more cash than earnings indicating low debt and non discretionary expenses, also not much of GAAP adjustments.

Constant free cash flow allows Indag to take more suitable decisions regarding capital allocation.

Return on Invested Capital

It tracked almost similar territory as ROE due to absence of debt.

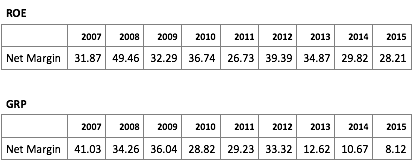

Net Margins

The margin is in uptrend, now crossed 13%.

The big competitors are not listed in market; the only player, which was listed, is GRP a bit bigger size with revenue of 340 Cr. The margin has been shrinking.

Return on Equity

Indag has posted a very healthy ROE across the years. The competitor GRP started almost similar fashion except loosing out in last few years.

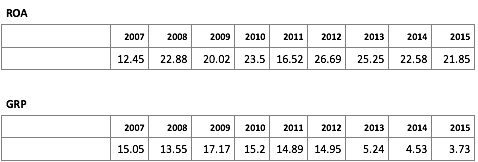

Return on assets

Extra ordinarily high above 20. This also indicates Indag has been able to squeeze more out of assets. GRP had a good ROA , again lost out during last few years.

Good free cash flow, outstanding ROE and ROA, moderate but increasing profit margin are good indicators of moat.

Can moat be explained if any?

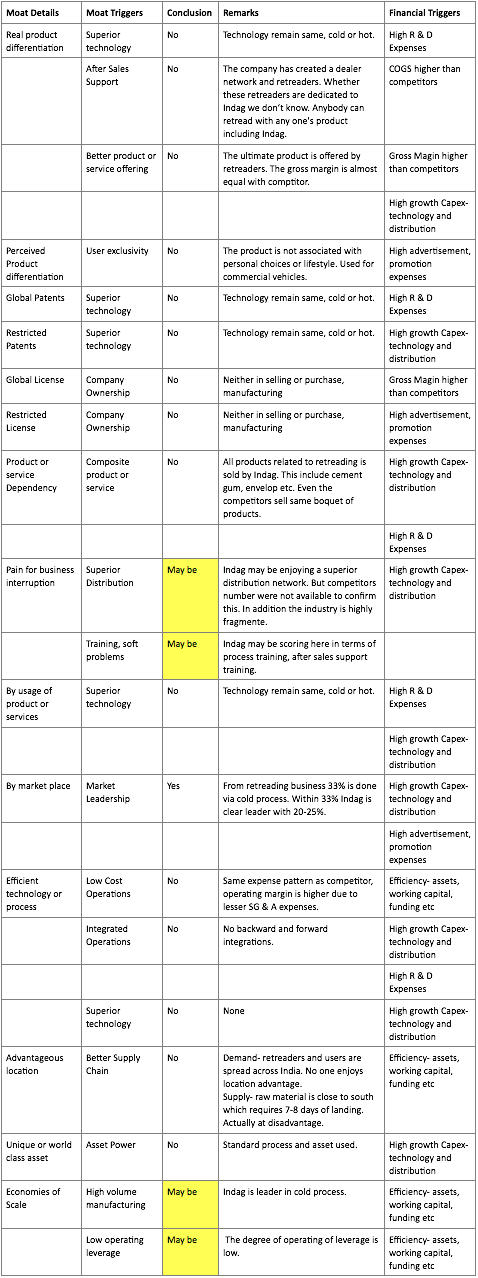

The financials hinted there may be some sort of moat, let’s look at moat component.

A detail exercise attached in WP-CBR1. At four places I could sense there could be a chance of moat:

Superior distribution network via dealers and retreaders, which may be creating a switching cost for non-financial pain.

Again after sales support, training help for retreaders, who may be creating a switching cost for non-financial pain.

Indag is a market leader may be involved in high volume manufacturing. Cost advantages.

Indag have a low degree of operating leverage. Cost advantages.

Longevity of moat

Depth of moat (High, Medium, Low)- Indag’s moat may be coming from switching cost which will not alter the usage pattern of customers. Same case with cost advantage. There is no depth of moat. Low depth of moat.

Width of moat (few, several, many)- the distribution network and after sales support may be required several years to get replicated by competitors. The one with cost advantage without technological advantage may be difficult to get replicated for several years. Hence the width of moat is for several years. This need to be confirmed with superior working capital position, capital efficiency and other similar factors below in different sections.

The Industry View

The market size and sales are on rise year after year. During last 7-8 years I didn’t see any downward or cyclical trend in sales. Though firms are profitable competitors profit has gone down in last few years. The industry is fragmented, however in cold process segment Indag is market leader with a lion 65-70% share.

Operating and gross margin are fairly high above 25-30%.

The industry in general not high flying but moderately consistent. ROIC has been healthy for guys out there in retreading.

Driving force behind industry- lower cost of vehicle maintanence

Competition within industry- fierce but unorganized

Macro picture- will continue to grow

Industry trends- radial tyre is new generation tyre with high longevity.Hence retreading cycle will increase.

Cash conversion cycle- debtor and creditors are moderate where as inventory depends on location. If you are in south its more suitable due to rubber plantation.

Cyclical exposure- mild exposure, commercial vehicles are also used for essential goods. Even with economic down turn the maintenance will continue.

Pricing power- teasing

Demand volatility- retreading has lifecycle, less volatility.

Subtitute product-retreading itself is an substitute product, hence one can ignore and buy a new tyre instead.

Industry rivalrly- the competition is based on services , with more dealer network.

Low cost country threat- China.

Reason for failing- not came across a case of failure.

Pricing Power

As the quantitative data were not available related to sales I coudnt check the prices charged by Indag historically. However if Indag raise price for it’s products then customer will either switch to unorganized players or competitors.

But Indag comes with quality, a teaser price customer wont mind to pay as it will save him from frequent maintenance and support.