I think a bulk of the 31,134 Cr is sitting at 0 days dpd. So in the first column, 1-30dpd must be barely anything. That’s the only explanation I can think of.

1 Like

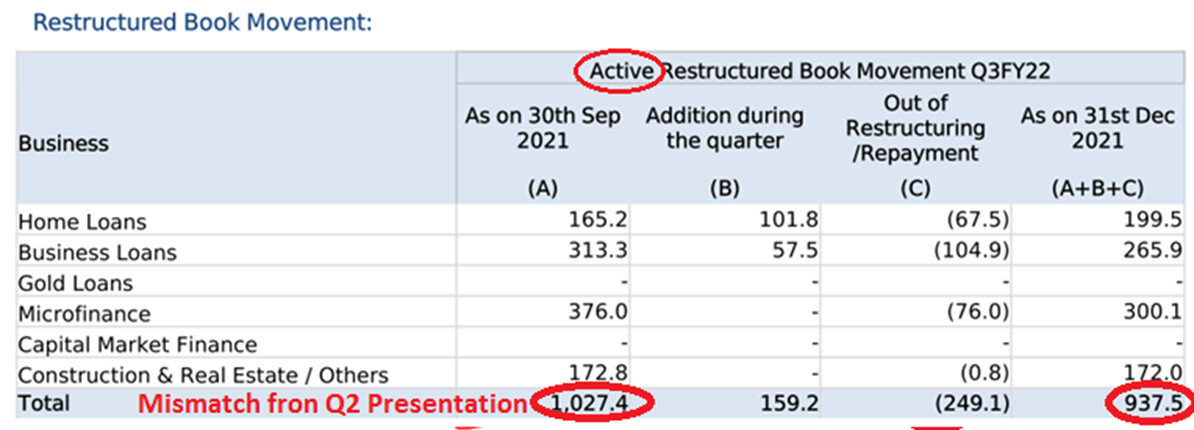

Don’t you think it’s strange that the entire restructured microfinance book has come out of restructuring? So in this quarter each and every restructured microfinance account became regular?

1 Like

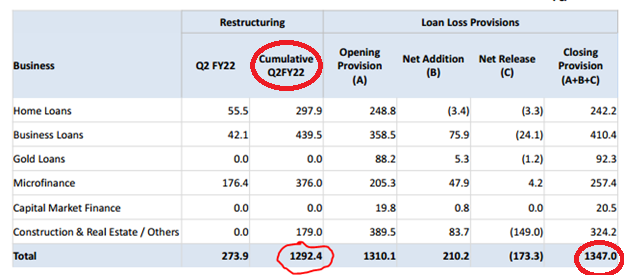

To me the rise in NPA it seems like mostly from restructured assets.

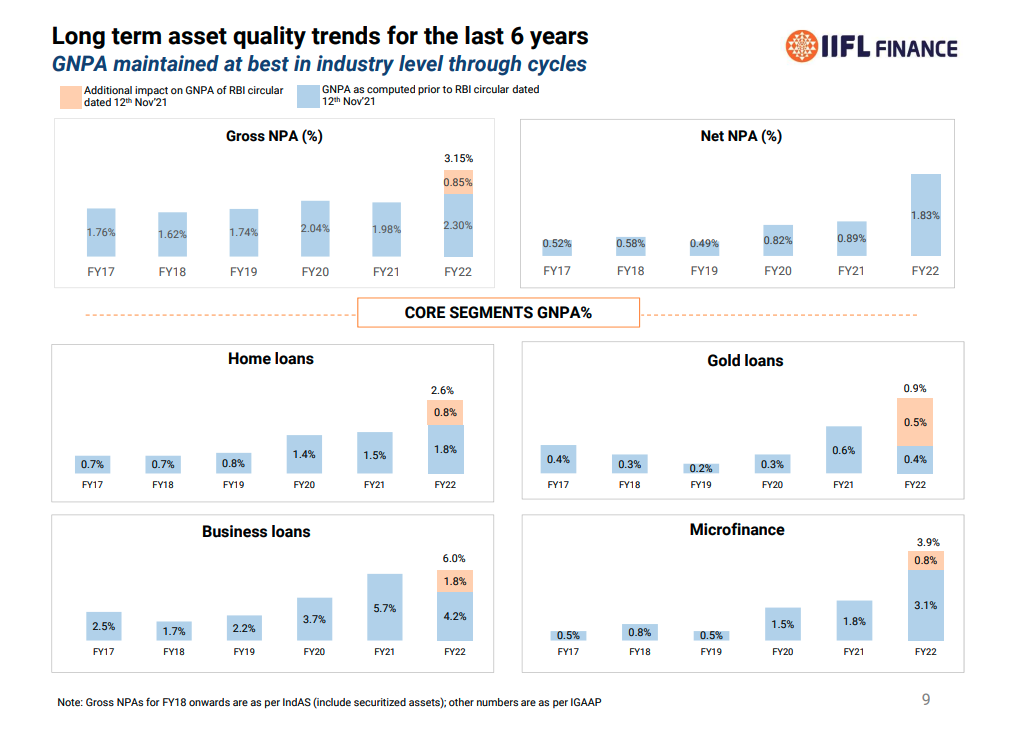

Lets take a look at the Stage 3 (90+ dpd) assets trend

Q2FY22

Q3FY22

Q4FY22

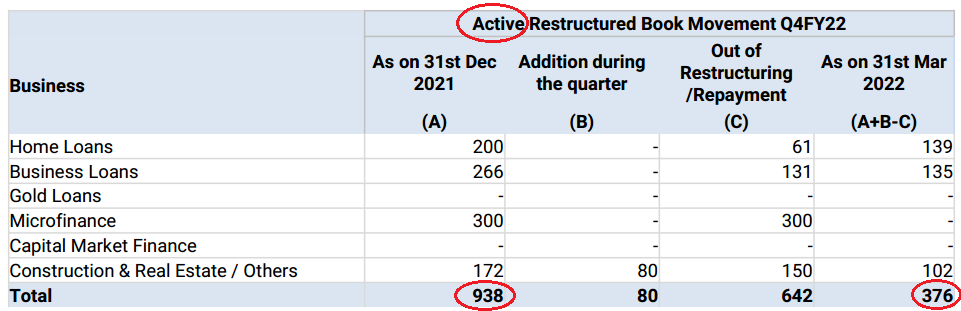

Now lets take a look at restructured loans trend.

Q2FY22

Q3FY22

Q4FY22

Please note that there is a mismatch between Q3 & Q2 restructured loan data. Maybe my understanding is wrong.

So the question is what is the source of this new Stage 3 assets or GNPAs. Whether it’s from the restructured loans or the loans disbursed after 2nd wave? If it’s from the restructured loans then it’s fine. Because as of now Restructured loan + Stage 3 = 1074 + 376 = 1500 cr and total provision is 1317 cr.

So this question needs to be asked in tomorrow’s concall.

Coming out of restructuring does not mean it’s standard. It can become either NPA or standard. In Q3 Stage 3 MFI was 124 cr and now it’s 221 cr. So net addition to stage 3 (since some loans are written off which we don’t know) is 97 cr. So maybe some of those 300 cr restructured ended up being npa and the rest is standard.

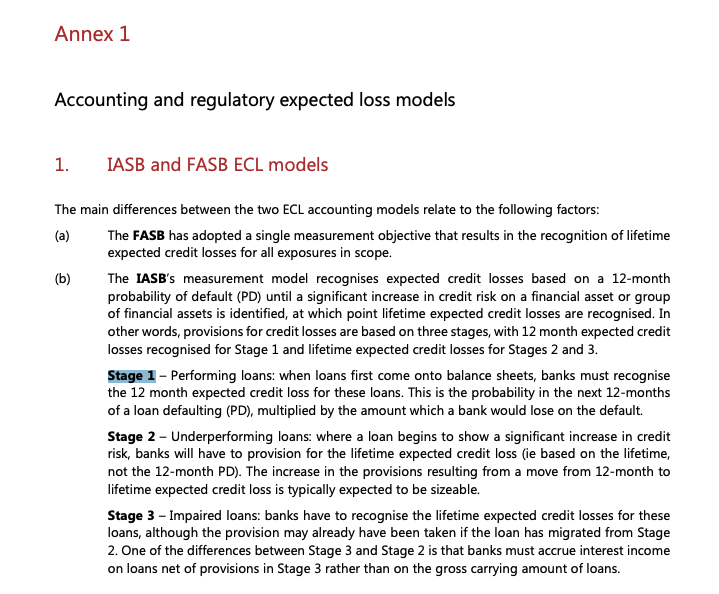

Easiest thing to do is to do Google search to understand what stage 1 means.

Stage1 loans are standard assets. If bank raises an EMI on day 0. Until Day 30 loan is considered standard because borrower has 30 day window to pay.

Even stage 2 is not considered very risky because some % of borrowers always are delayed due to 1 problem or another (eg: in my recent home loan, i ended up paying after 30 days because my loan account did not have enough money due to special circumstances. Of course i still paid within 45 days).

Stage3 is what is worth monitoring.

The rise in GNPA is due to the RBI circular as shown in 1 of the slides.

They had mentioned 1-2 Q for gnpa numbers top stabilize. Provision coverage is still fairly good. So looks like the panic might be unwarranted, of course need to listen to concall to confirm these understandings again.

Disc: Invested, biased

9 Likes

8 Likes

Supreme Court ruling on NBFC regulations: Five key points explained

3 Likes

3 Likes

Never heard HoldCo discount a central piece of thesis for simple subsidiaries structure where businesses are not disjointed (like in Piramal that has finance and pharma).

This thread doesn’t have any discussion around it either.

IIFL is all about lending but with ADIA investment, everyone’s back to drawing board determining its true market value (me included).

4 Likes

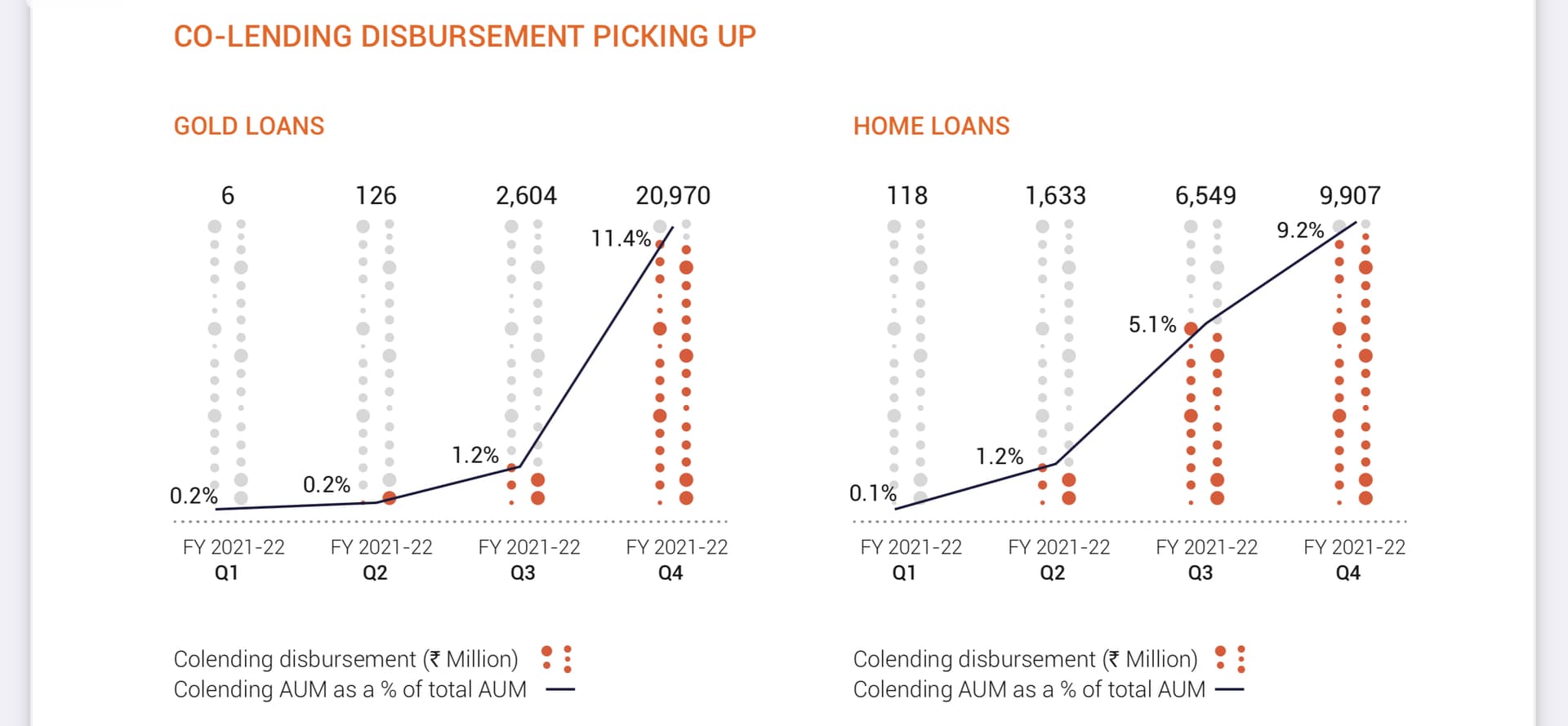

It’s interesting to track the progress here in terms of the new partnerships that are getting onboarded in different segments and how the co-lending book is evolving.

Also, quite interesting to see the management taking the JV route in building a suitable financial product here in deepening the penetration in MSME segment, as this space gets back the attention of the larger players. Curious to see the actual product, flow and use cases it serves here compared to traditional banking channels.

Disc: Invested.

7 Likes

1.What is the difference between Assignment,Securituzation and Co-lending(ASC) with example

2.In case if a loan become NPA in above process whether it is shared with bank or only sit in NBFC Book.

3.I have seen in investor presentation there is a income from assigned assets and commission income what it is?

4 Likes

Direct assignment is basically selling part of loans to a bank.

In Securitization the nbfc sets up a third entity, transfers the loans to it and issues securities on the back of those loans.

In co lending there is already an agreement in place on what % of loans sourced by the nbfc the bank will take and what % the nbfc will keep on its book.

Income from assigned assets is the pv of interest spread on the loans that have been assigned.

Say the loan is yielding 15% and nbfc assigns it at 10% and the tenure is 5 years.

On direct assignment the nbfc will book the entire income of 5 years upfront itself i.e the present value of interest spread of 5% over 5 years

6 Likes

1 Like

In co-lending NPAs are taken based on agreed percentage of loan between Bank & NBFC?

IIFLFinance

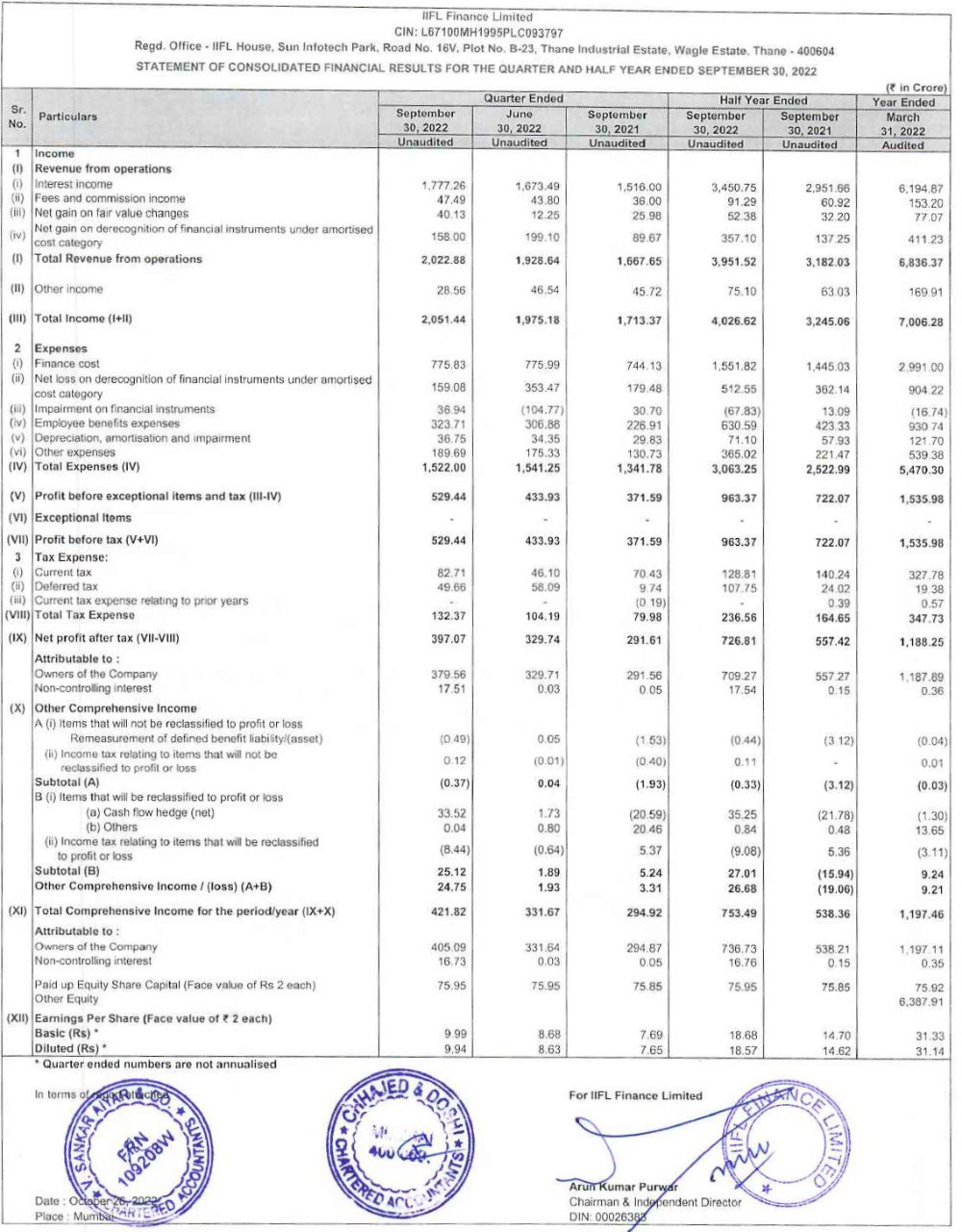

PBT 434cr vs 350cr,q4 420cr

PAT 330cr vs 265cr

Nice Analyst Day presentation from IIFL Finance.

IIFL Finance Q3-FY23 Concall:

-

Cost of funds for the company went up marginally which has been passed on to the customers.

-

Intense competition in gold loan from new NBFC and small banks; for some their rates are below cost of funds to attract customers.

-

Oct & Nov were not good for gold loan due to competition; now fintechs are also understanding that low cost lending is not a long term strategy; no knee jerk reaction on it by the company.

-

In the Home loan company is focusing on small loans and from spoke locations i.e, small towns and cities.

-

Microfinance industry doing very well; we are well diversified geographically

-

Strategy is to partner with good corporates for digital loans; tied up with no. of player and testing is going on with big corporates; company will announce more on it soon; these are unsecured loans (personal loans) for employees of the corporates.

-

PPOP of 772 cr up by 26% YoY; Loan AUM grown by 24% YoY.

-

Core products now comprise of 95% of total loan book which is retail in nature

-

Assigned loan up by 37% YoY; colending is now at 5700 cr; added Uco Bank and Punjab & Sind Bank for colending in gold loan.

-

Annualised ROE at 17.9%; Avg cost of borrowing is up by 10 bps.

-

Raised 4346 cr of term loans, bond and refinance in Q3 for liquidity and liabilities

-

Gold loan tonnage growth of 20% YoY

-

Out of total investments of 3,683cr in balance sheet; Invested around 1000cr into IIFL real estate funds, no much exposure in IIFL wealth; the amount received from ADIA is not deployed fully yet hence there is an increase in investments

-

In MFI there was total provision of 105cr and write off of 123cr due to old loans; newer loans are doing very well;

-

Credit cost will be in the range of 1.5 to 2%; slightly higher in the range for full year due to MFI write off of old loans.

-

Gold loan competition is largely in bigger cities like top 20 or 30 cities and company is focusing more on the tier 2 or tier 3 cities where competition is not much as company has branches in many small towns and cities.

-

Company will be maining the growth of 25% CAGR

-

Cost to income at 42%; target is to bring it down to 35% in next 4 to 6 quarters

-

At some point of time in future the company will also look for external investors in MFI businesses as well; IIFL infused 200 cr into the subsidiary.

-

Once the business becomes large enough Housing and MFI companies will be demerged.

-

In home loan under small ticket size i.e, less than 20 lakhs competition is very low

-

After aggressive expansion in 2020 and 2021 now it has been slowed down; it will be 10-15% expansion every year in future

-

Gold loan is available at 2589 branches and will reach at 3000 branches by FY24; 370 branches for home loan; company has adequate approval of branch expansion for next one year

-

Company will be comfortable at leverage of 4x from current levels of 3.2x; won’t cross 4x

-

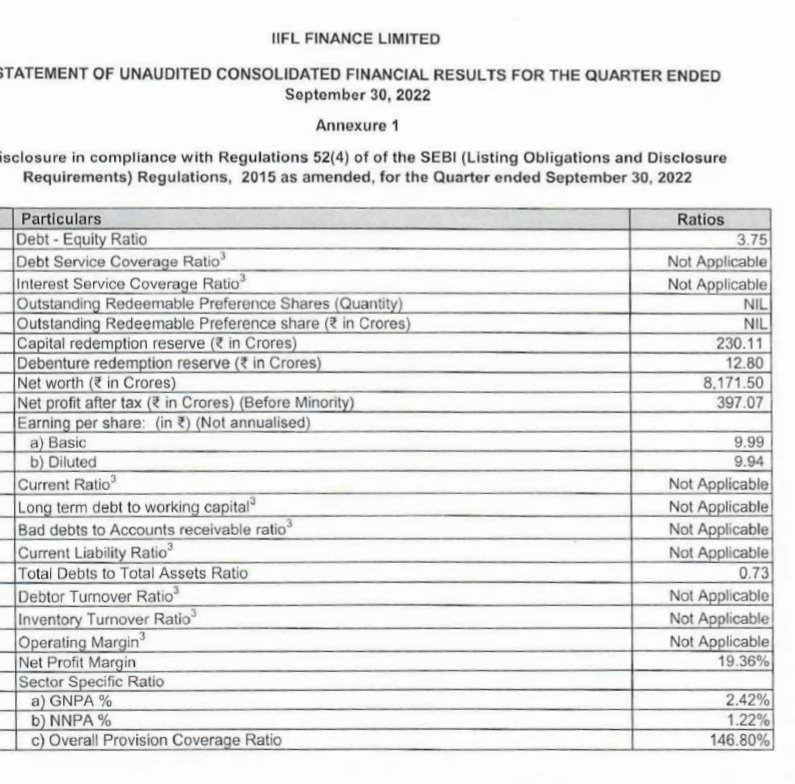

Target is to reach GNPA of 2% and NNPA of 1% at cosol level; currently it is at 2.08% and 1.06%

Disc:- invested.

25 Likes