Using their app to get loan it is just to check how efficient their app is. It is fabulous. Loan approved in an hour and disbursed in a day. If your cibil score good then anyone get loan disbursed on the basis of their previous track record. Their employee also help me in the process.

8 Likes

Saw your video on it presented last year.

It was trading at 1.8 Price to book value that time.

Today it’s trading at 2.0 Price to book value. Book value had grown 40% in last year so do you think this growth is sustainable for next few years.

Didn’t find any research report on it apart from symmatrix where they are valuing it at 2.5 Price to BV.

If you can guide on what seems fair valuation to you.

Thanks.

The management is guiding to take aum to 1 lakh crs by 2025 from 55k-60k cr currently that applies 25-30% growth. If they are able to get close to this target then valuations are still very reasonable.

Disclosure - Invested

5 Likes

@Worldlywiseinvestors What is the right way to value this NBFC? And which segment of NBFC companies we should compare to understand the relative valuation?

The reason is that due to CoLending my doubt is their Book Value the right representation?

2 Likes

I have one confusion here on IIFL.

-

Management has given guidelines of 25% aum growth and 20% ROE (3.5% ROA based on current leverage). Current AUM is 64k Cr.

-

Estimated FY24 PAT based on these numbers should be around 2800Cr ( ie: Expected FY24 AUM times ROA)

-

However management has given a PAT guidance of 2100 Cr (25% growth in bottom line) in FY24.

These two numbers don’t match here. To folks following the company, please suggest if there is something wrong in the numbers here

1 Like

People following the company, will the ban on IIFL Securities hamper IIFL Finance? If I understand correctly, they are separate entities with different businesses, but will it impact the IIFL “brand”, thus affecting IIFL Finances.

And are there any corporate governance red flag in this company as well?

2 Likes

Though we can argue that they are seperate entities, the same promoter ironically holds 15% stake in IIFL securities as well. Looks like that there are some serious corporate governance issues in this group indeed. Exited my position completely today.

7 Likes

What could be probable demèger scenario in iifl finance if it happens in future

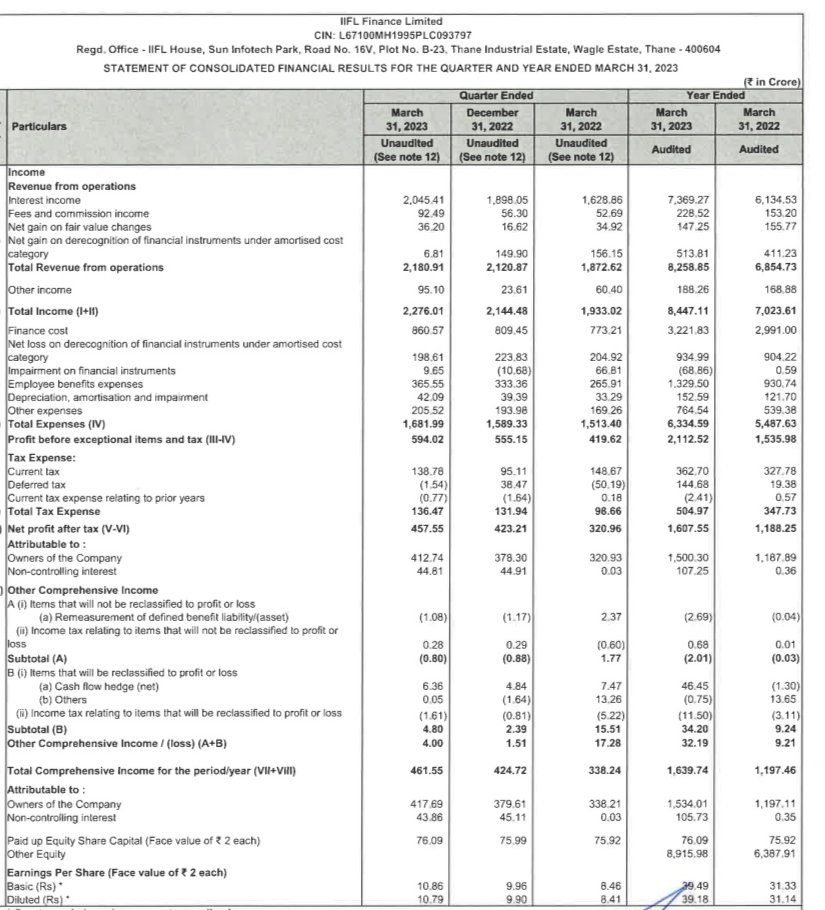

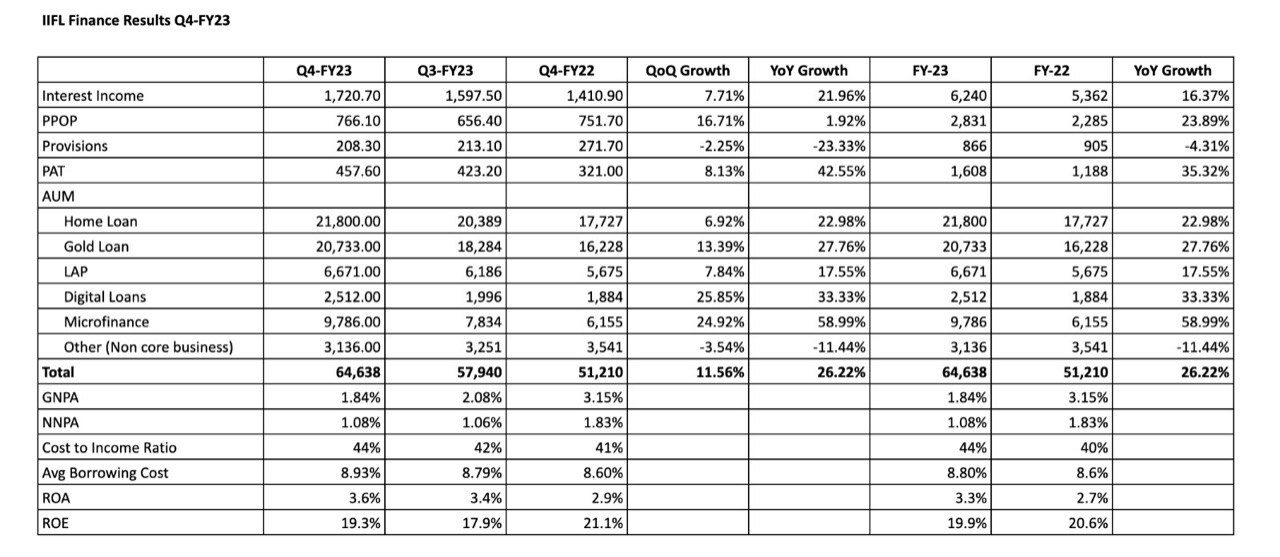

IIFL Finance Results

Some key points:

- NPAs falling,

- Microfinance growing fast (FY23 - 9786Cr, H1FY24 - 11307Cr),

- ROA touching 3.7%,

- Cost to Income flatting and expected to fall further,

- Q4 is usually the best so PAT should touch 2000Cr for the year,

- Sharp growth in Home Loans AUM (FY23 - 21800Cr, H1FY24 - 24000Cr) - Sticky book,

- Sharp Growth in Digital Loans AUM (FY23 - 2512Cr, H1FY24 - 3539Cr),

- GNPA went up in Gold Loans from 0.8% to 1.2%

- Co-lending in Gold Loans is now 35% of the AUM

Disc: Invested

7 Likes

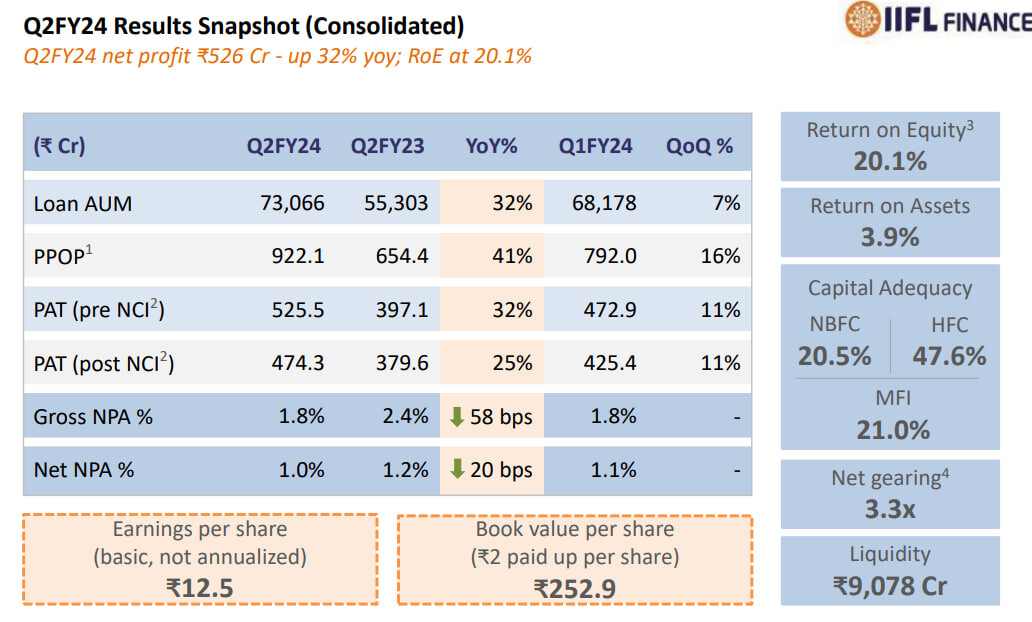

IIFL Finance ltd Q2 concall highlights -

Loan Book @ 73k vs 55.3k cr, up 32 pc

NII - 1001 vs 724 cr, up 38 pc

PPOP - 922 vs 654 cr, up 41 pc

Provisions - 252 vs 196 cr, up 30 pc

PAT - 475 vs 380 cr, up 25 pc

Gross NPAs @ 1.8 pc vs 2.4 pc

Net NPAs @ 1.0 vs 1.2 pc

Book Value / share @ 252 vs 215

RoE - 20.1 pc

RoA - 3.9 pc

Loan book break down -

Loans on company’s books - 44k vs 35.2k cr

Assigned assets - 18.4 k vs 15.4 k cr

Co-Lending - 10.5 k vs 4.7 k cr

Total - 73 k vs 55.3 k cr

Sector wise breakdown of loan book -

Home Loans - 24k vs 19.6k cr, up 22 pc

Gold Loans - 23.7k vs 17.8k cr, up 33 pc

LAP - 7.2k vs 5.9k cr, up 21 pc

Digital loans - 3.5k vs 1.99k cr, up 77 pc

MicroFin - 11.3k vs 6.7k cr, up 67 pc

5 yr CAGR of loans AUM growth @ 23 pc

5 yr PAT CAGR @ 28 pc

Avg loan rates -

Home Loans - 11 pc

Gold Loans - 18.5 pc

LAP - 18.6 pc

Digital laons - 22.4 pc ( primarily for MSME lending - unsecured loans )

MicroFin - 24.4 pc

AVG yeild- 17 pc

Avg cost of borrowing - 9 pc

Spread - 8 pc

Cost/Income @ 43 pc

Avg ticket size -

Home loans - 14 lakh

LAP - 7.7 lakh

Digital Loans - 0.7 lakh

Gold Loans - 0.75 lakh

Aim to reach AUM of 1 lakh cr by end of next FY

Company continues to remain cautious on unsecured lending / personal loans. Sounded skeptical of due diligence process followed by new gen Fintechs

Gold loan growth driven by company’s distribution strength

IIFL housing finance gets funding from National Housing Board at concessional rates - helps keep cost of funds under check

Company expects to maintain its NIMs at 7-7.5 pc or thereabouts

Management doesn’t see any credit demand slowdown if the economy remains robust - the way it is today

Avg life of Gold Loan portfolio is 90-120 days

Company believes, cost of borrowing has almost peaked in India. May move up-down by 10-15 bps, not beyond that

Company has slowed down its branch expansion spree. Should lead to lower Opex going fwd as more branches mature and their AUMs increase. Ex - IIFL’s gold loan branches have avg gold loan AUMs of 8 cr vs 22 cr for Mkt leader

Avg tenure of Digital loans varies from 6 months to 2 yrs. This is a high risk area. Hence the company is very aggressive in provisioning against Stage -3 assets wrt Digital loans. Despite that, returns are fairly attractive

LAP product in smaller towns etc has attractive rates. However, it also involves higher cost of origination like the cost of verifying the title, valuation of property etc

Q2 RoA @ 3.9 pc. Should be able to maintain the RoA range between 3.7-4.0

Credit cost range guidance given by the management @ 2 or thereabouts

Price war in Gold loans business witnessed in last FY is now abating. Hence the lending yields have gone back up

Co-Lending and Assigned books mainly consist of Gold, Housing loans and LAP

Current branch count at 4596 vs 3700 LY. As the new branches mature, operating leverage should kick in. On an avg, a branch breaks even in 18-24 months

Disc: Hold a tracking position, may add more, biased, not SEBI registered

7 Likes

What will be the impact of RBI’s yesterday’s AIF decision on IIFL’s business?

Don’t know about the intricacies - to be very frank

However, IIFL’s lending book is largely retail and small business loans. Hence - this order should be irrelevant as far as IIFL is concerned

First thing - that came to my mind ![]()

1 Like

The matter has been under litigation and it seems that IIFL Securities has got relief.

Please see the recent news.