A bit dated video but may be valuable.

A bit dated video but may be valuable.

Q3FY22 result analysis by them

Great analysis on IIFL Finance by @Worldlywiseinvestors and @suru27

🔴")

IIFL buyback of 50mn USD worth of bonds complete at par value.

As per Management commentary, this has been replaced with new debt which will reduce the cost of funds on this 50mn USD by 225 basis points, so a cost reduction of ~8.5Cr INR annually.

Sharing some of my notes on the colending piece from discussions with folks in the industry as it’s one of the lesser understood but critical pieces of the thesis considering the proportion that IIFL wants to take colending loans to its overall book.

Colending as a model while new to India, is a mature model in markets like Indonesia. Studying the evolution of the model in Indonesia might provide a reference point for how things might evolve in India too. In mature markets, it’s considered as a single business for both entities with a joint operating plan with metrics on how much loans to originate, what customer profiles to look at, acceptable levels of credit losses, pricing for the loans in terms of interest arbitrage between bank and NBFC. In a sense, colending fixes some of the issues from a NBFCs standpoint over direct assignment.

The core reason from a bank’s perspective to opt the colending model is it fits the bank when it might not have too many branches and have the reach and number of touch points of a large NBFC. Also, for many of the urban centric banks the model allows them to build a loan book in a segment of customer profiles and loan profiles that would be hard for them to build organically and to instead build it through colending partnerships. For example, for an urban centric bank to make the unit economics work to lend to tractor loans would be very difficult but relatively easy to co-originate these loans alongside a NBFC who has been doing that over multiple years and take 80% of these loans on their balance sheet.

The choice of NBFC to work with in the colending model comes from this point of choosing to work with NBFCs who has gone through multiple cycles lending to that particular loan segment in terms of customer profile and asset, has high number of touch points and infrastructure for collections and disbursals, has good quality credit underwriting standards and history of compliance.

From a customer standpoint - the flow is such that the originator of the loan becomes their touch point for the entire duration of the loan. The NBFC owns the customer. However, the bank has visibility on how the book is behaving under different circumstances which helps them to model things out in case they want to build their own book.

From the NBFC standpoint, important to track the number and quality of colending arrangements they have with multiple banks so that there is enough arbitrage to play with on the pricing front and also to mitigate the risk in terms of disruption in fund flows when you’re dependent only on few partnerships to grow your loan book in a particular asset class. If you have multiple lending partners, it becomes easier to pick and choose on how to distribute the loans you originate between the different partnerships and not be squeezed on pricing.

How a bank chooses which NBFC to partner with

Colending partnerships also require a good degree of integration of systems between the NBFC and the bank. The underwriting process has to be fixed beforehand before the loan is originated. The new CLM norms allow for colending to be run sequentially instead of parallely. However, this doesn’t increase the disbursal TAT as both the 80% and 20% portions need to be disbursed same day. But the loans are disbursed only after both entities have assessed and underwritten the loan.

There are few ways in which the model and underwriting flow works

The power in the dynamic between the bank and NBFC is very interesting. For the NBFC, they are getting lower cost of access to funds, they are growing their fee incomes, customer base on external funds and at higher capital productivity. For the bank, they are getting to grow their loan book with the access and reach of a large NBFC without having to replicate its distribution and collection infrastructure. If the NBFC already has deep pockets and is already mature in the ecosystem, the NBFC can pick and choose which banks it wants to work with without disruption to fund flows or getting squeezed on pricing. While from a bank’s perspective, the choice is to work with a set of large NBFCs where they can be reasonably sure that the NBFC can source customers and loans that will not be cannibalizing their own future loan book and also will not go belly up and will continue servicing the client and finish collections on the loan as the bank need not possibly have the collection infrastructure in place for that loan profile to finish the collections for the entire loan tenure, more so for high tenure loans like home loans. Opening up the balance sheet for customers that you don’t see is hard to do for a bank, which is where the NBFCs credit history, credit loss trends, size and scale of touch points, digital capabilities and relationship building comes into play.

Pricing for the colending loans is completely dependent on the forecasted credit losses expected on the book. Colending doesn’t start with a player who is new in the industry. Works both ways in terms of how pricing is structured for future co-origination based on how the previous co-originated book has behaved on credit losses based on credit quality indicators. The NBFCs get lower pricing on future co-originated loans if the previous book has had higher than modeled credit losses and vice versa.

Really a good info

On cost of funds how this model will reduce cost for a NBFC. If i am taking a 10L loan at 12%pa, with a NBFC and they have 20:80 model with a bank, bank have to source 8L for my loan and NBFC has to source 2L for my loan. yield for both the party remains 12% for what they lent to me. Now for 2L, NBFC have to still have to source fund via bond/term loan/cp. Here in this case they can raise funds at their usual rate. Could not able to understand, how this will reduce the cost of funds for a NBFC

Really informative video on the business of iifl finance.

Basically, banks will lend to NBFCs, and NBFCs will pass it on to the priority sectors, since they have a greater reach.

NBFCs will be the single point of interface for the customers and enter into a loan agreement with the borrowers. The agreement should contain the features of the arrangement and the roles and responsibilities of NBFCs and banks.

Ref: co-lending: What is co-lending, and how will it work?, BFSI News, ET BFSI

The ultimate borrower would be charged an all-inclusive interest rate.

The bank & NBFC make agreement at what % to lend…let’s assume it as 10% & 80:20 model…

Now if NBFC provide 10 lakh loan at 12 % interest rate…the additional 2% interest on 10 lakh goes to NBFC + 10% interest on 2 lakh…so NBFC get 20k+20k=40k on 2 lakh

For Bank it will get 10% on 8 lakh= 80k for 8 lakh

But still their cost of funds will not go down right. Still they have to source fund for remaining 20% of loan at the same interest rate as they raise before co lending model.

Hey Sidharth. The math works a little different than how you’ve mentioned. For a 10 lakh loan, with a 80:20 split, originated by the nbfc at 10% interest to customer and the pricing agreed with bank is at 8%.

The bank will make 8% on the 8 lakhs. And the nbfc will make 10% on 2 lakhs and 2% (differential in pricing between bank and customer) on 8 lakhs too.

The comment on lower cost of funds is that with better churn of capital, the blended cost of funds that the nbfc has to raise in future will come down for their overall loan book as opposed to what it would have been without CLM. Hope this clarifies.

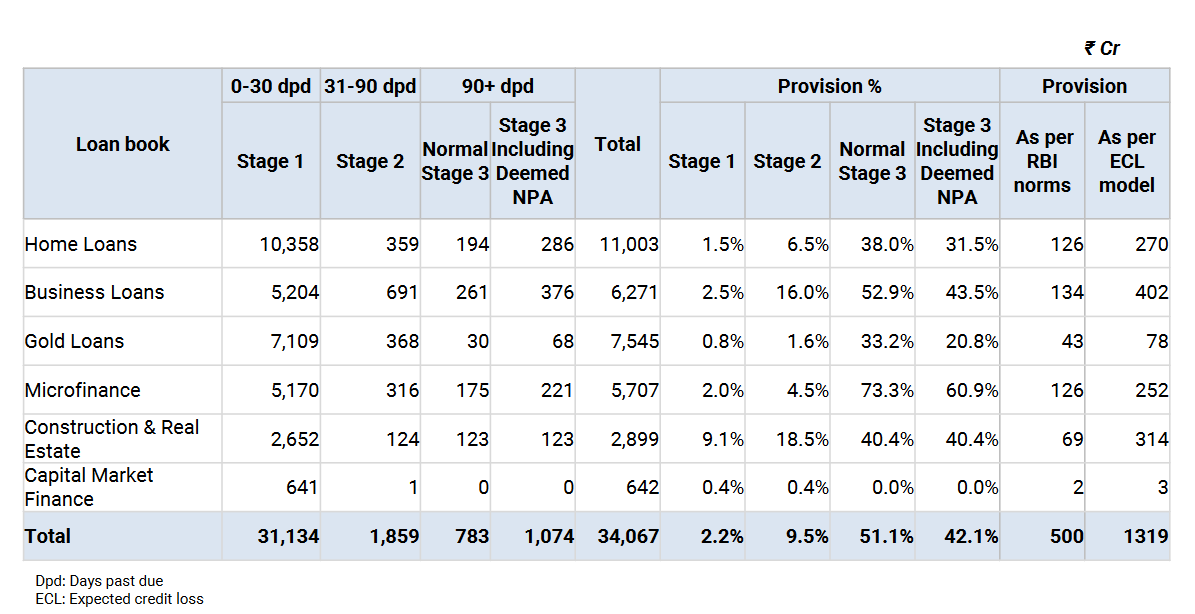

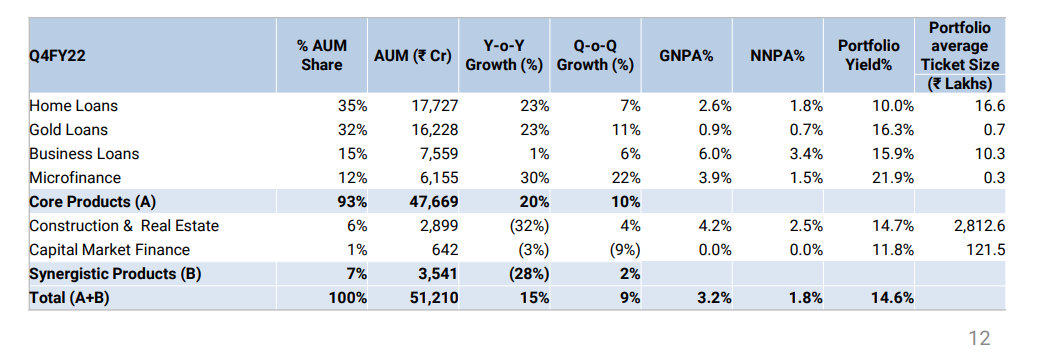

Spike in GNPA/NNPA

Yes every bank and NBFC that has reported till now has reported a fall in NPA’s while these guys are showing an increase. Not a good sign and when combined with their agressive lending and high leverage its a pretty worrying development. And keep in mind that the Loan Book has gone up QoQ, so the absolute jump in NPA’s must be high. Investor Presentation should have more details.

As per this from their presentation 8.6% of their book is Stage 2 and above-

Stage 3 itself is almost 3.1%!

There seems to be some issue with this data. The Dec’21 loans outstanding was Rs. 30,380 cr. This table shows that 0-30 dpd is itself Rs. 31,134 cr. Can you please share the source of this data?

Its from their latest presentation, just uploaded on BSE.

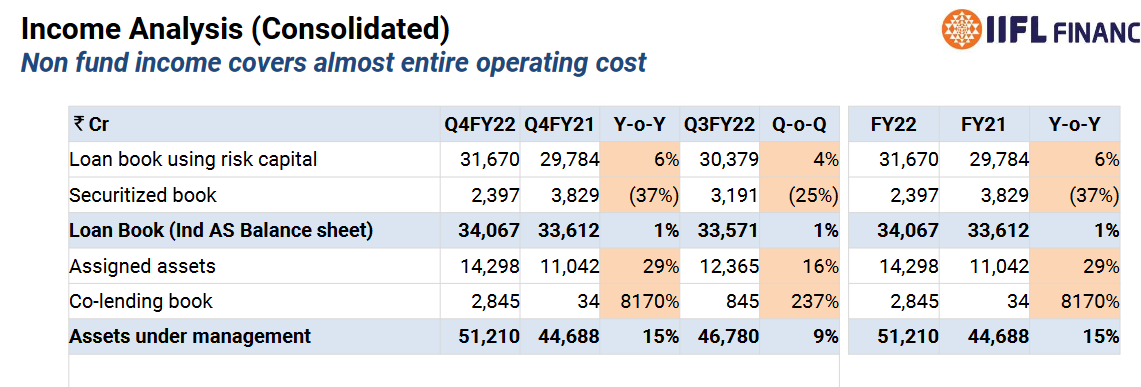

Their total loan book is around 51000 cr.

Total stage 3 loans ( including deemed NPAs ) / total loans works out to be - 1074 cr / 51000 cr = 2.2 %

Total stage 2 loans / total loans works out to be - 1859 cr / 51000 cr = 3.6 %

Am I missing anything ???

Kindly correct me if I am mis-reading the data.

Also, the total loans in Stage 1 ( overdue by 0-30 days ) are aprox 31000 cr on a loan book of 51000 cr.

Is this normal ???

Or… Is this at par or roughly in range with Industry averages???

Some thoughts on the same shall be really helpful.

Regards,

Ranvir Dehal

If that was the case they would have shown 51,000cr of loans in the table. 34,000cr are the loans on their own balance sheet, the rest are off-balance sheet and co-lending arrangements. This is clearly shown on slide 5 which you can see below-

For the assigned assets and the co-lending book we don’t have the NPA figures. So you need to be very careful when you are looking at the NPA figures they report, they are far lower than the actual numbers.

Went through the presentation - https://www.bseindia.com/xml-data/corpfiling/AttachLive/4fd3dd38-cba4-49dc-924c-4a24c4827190.pdf

A couple of points worth analysing:

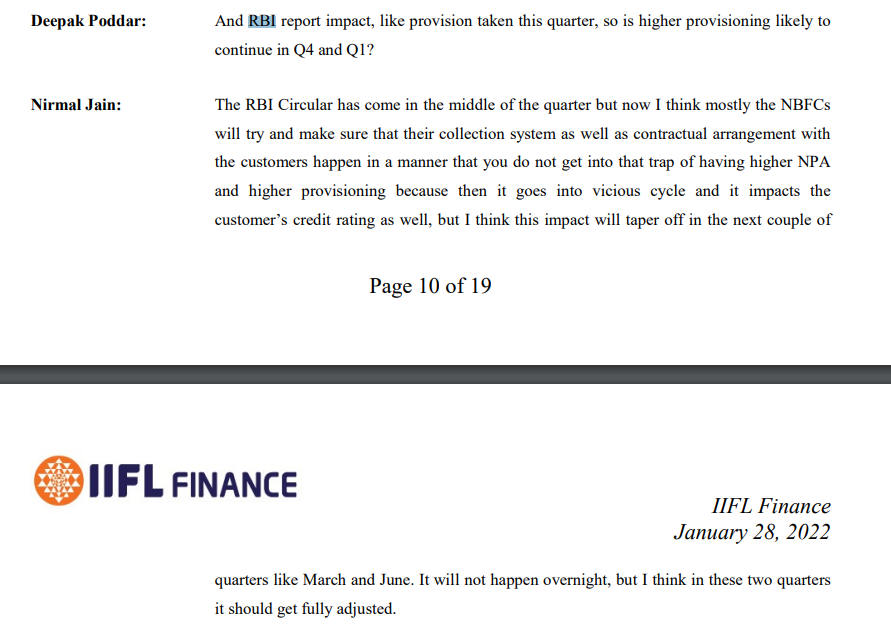

1. GNPA/NNPA has increased to 3.15%/1.83% from 2.8%/1.5% last quarter - There could be two sources of this increase in NPA.

a.) First is the lingering effect of changed RBI norms. In the last concall Mr. Jain had mentioned that due to the modified norms, contractual discussions with customers have to be modified to ensure they don’t get classified as NPA which make take 1-2 quarters to smooth out.

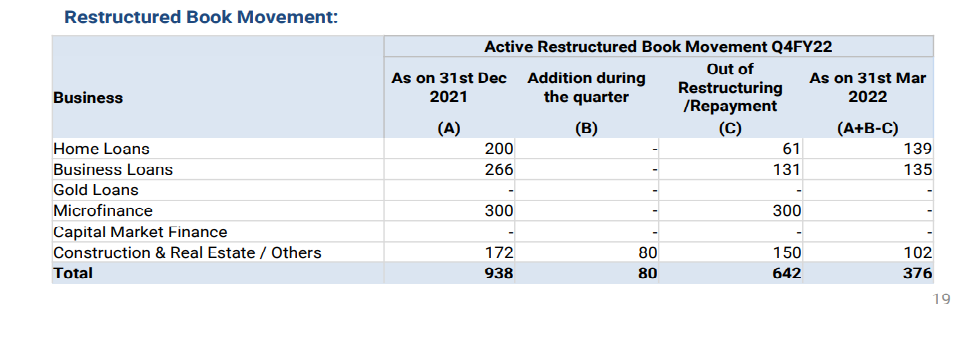

b.) Second is NPAs generated from the re-structured book. The re-structured book has moved down by a good INR 562 Cr, its possible some of them have been classified as NPA.

The GNPA slippage has been highest for the Home Loans category. Home loans and MFI GNPAs have increased QoQ whereas Gold Loan and Business Loan GNPAs have either remained same or contracted QoQ.

Since GNPA/NNPA is in a downtrend due to the start of a new credit cycle, this is a red flag in my opinion and needs close monitoring. I hope this question is asked and answered in the investor concall.

2. Gold loans yields on the entire AUM have fallen by 110bps from last quarter to this quarter. Till Dec '21, Goal loan portfolio yield was 17.4%. This indicates heavy competition in the gold loan space, a well known fact in the market. Results of Muthoot and Manappuram are to be tracked to gauge how IIFL’s gold loan portfolio has done wrt market.

Also Cost to income ratio has increased by 160 bps once again Q-o-Q. Hope this % starts consolidating now. Overall results seem good but asset quality has to be monitored very closely.