Brilliant analysis and equally brilliant counter points by @valueinvesting101.

The above 2 posts comprehensively cover the relevant facts and leave only the room for final judgement of an investor on to invest in this or not. The variables to the problem have been effectively defined.

I also agree that @harsh_visharia model uses a very optimistic growth rate. Discount brokers have made the industry extremely competitive for full-service brokers.

As per mgmt concall , thr assessment is correct that demand for full-service brokers will always be there vis-a-vis discount brokers. However, that demand will not garner explosive growth as expected. In fact, growing fast can be counter-productive as it might lead to opening fake, dubious demat accounts, flexing the margin rules ( which, btw, the management does not do. they sacrifice growth to precisely avoid leverage risk - this was specifically mentioned in Jun results con-call)

Valuation : -

On a relative basis, this stock is cheap when compared to other listed brokers. Keeping aside the real estate value which the co will be demerging\selling off, this should be valued on earnings multiple basis. How much shd be paid for a slow-growth, high ROE earnings which will be distributed throughout ur investment tenure.

For disclosure, I bought the co. whn the mkt cap was only the real estate valuation and got the entire business for free ( I posted on this link at that time, check above :-)) Nd being a cheap value seeker, I didn’t averaged up or anything and continue to hold that position which at the time of allocation was 3-4% of the portfolio.

Mr. Arindam Chanda has resigned as the Chief Executive Officer, Key Managerial Personnel of the Company w.e.f. close of business hours on December 22, 2020 due to personal reasons.

Stock closed at Rs. 43 on Dec 22, 2020 after declaration by IIFL that they will repurchasing shares from open market worth 90 cr.

As per data at https://www.nseindia.com/get-quotes/equity?symbol=IIFLSEC, free float market cap is only around 620 cr. As per disclosure by the company promoter, they will not be selling any shares. Fairfax India, other large shareholder is unlikely to sell share, as their fair value estimates are around Rs. 84 as per Fairfax India’s annual report. Voting for buyback proposal indicating support for the buyback indicating majority of the shareholders supporting buyback at this price.

Given that this thread belonged to IIFL Holdings which had started trading as IIFL Finance after the restructuring, lets continue discussions about IIFL Finance in this thread.

There was a good initiating post in a locked thread. I am adding the link to that post for convenience.

Also following is an initiating coverage report from HDFC Securities

As per reports the company is planning to sell a minority stake in its subsidiary, affordable housing financier IIFL Home Finance, as it looks to unlock value.

I request @Worldlywiseinvestors to add his inputs in this thread given that he is invested in the company.

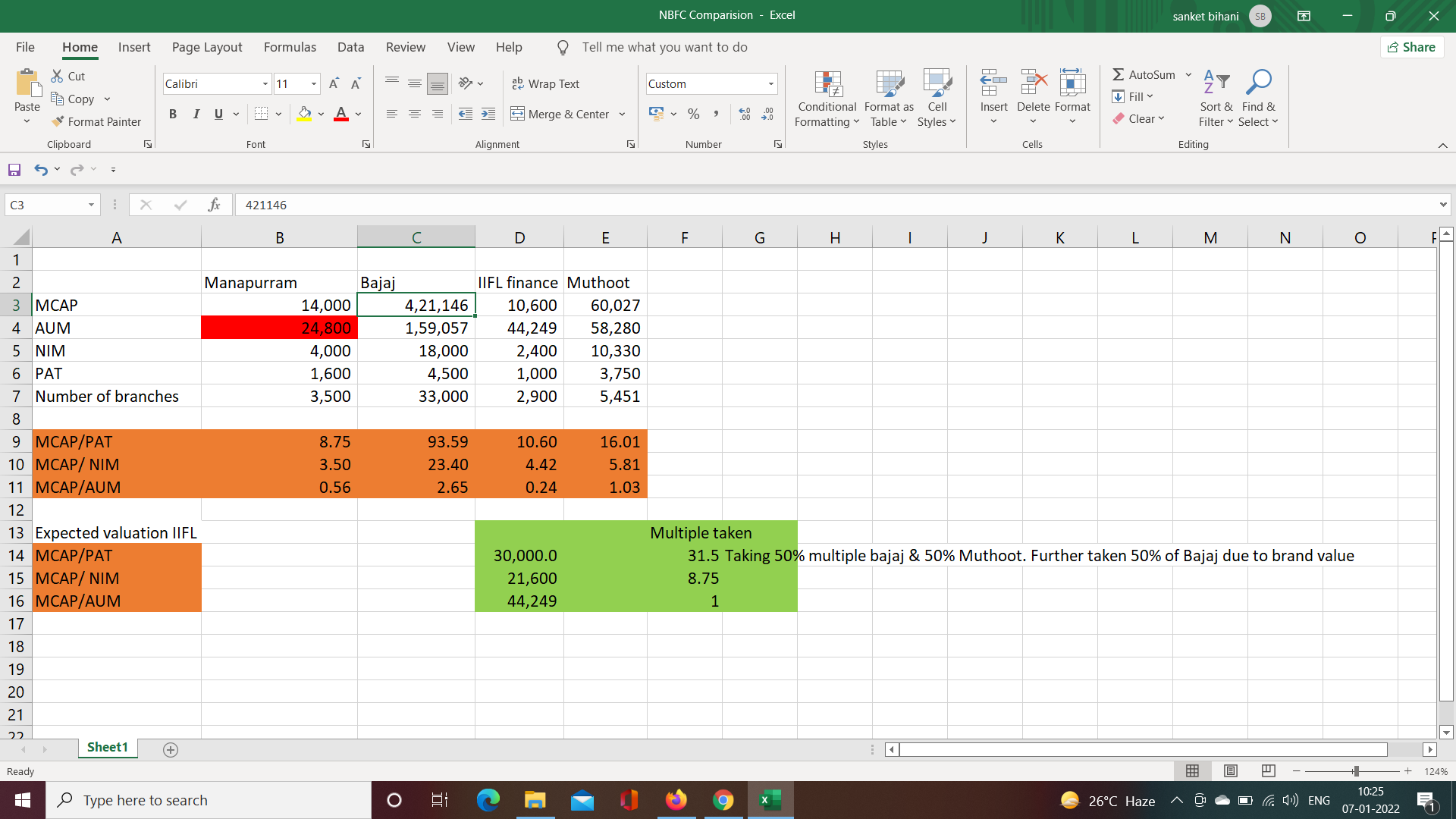

Is this high level valuation appropriate as it shows IIFL is quite undervalued.

Thesis: I tried doing relative valuation comparison for listed NBFC to see value potential of IIFL finance. Have taken a mix of bajaj finance & muthoot multiple as they have diversified portfolio and further 50% discount due to brand valuation for franchise. Still looks undervalued compared to its market cap.

Yes Sanket. You make a very valid point. The scrip seems to be highly undervalued. Unable to get around as to why? Is there something the market knows that we are unable to see ? Or this is a case of "diamonds in the dust "

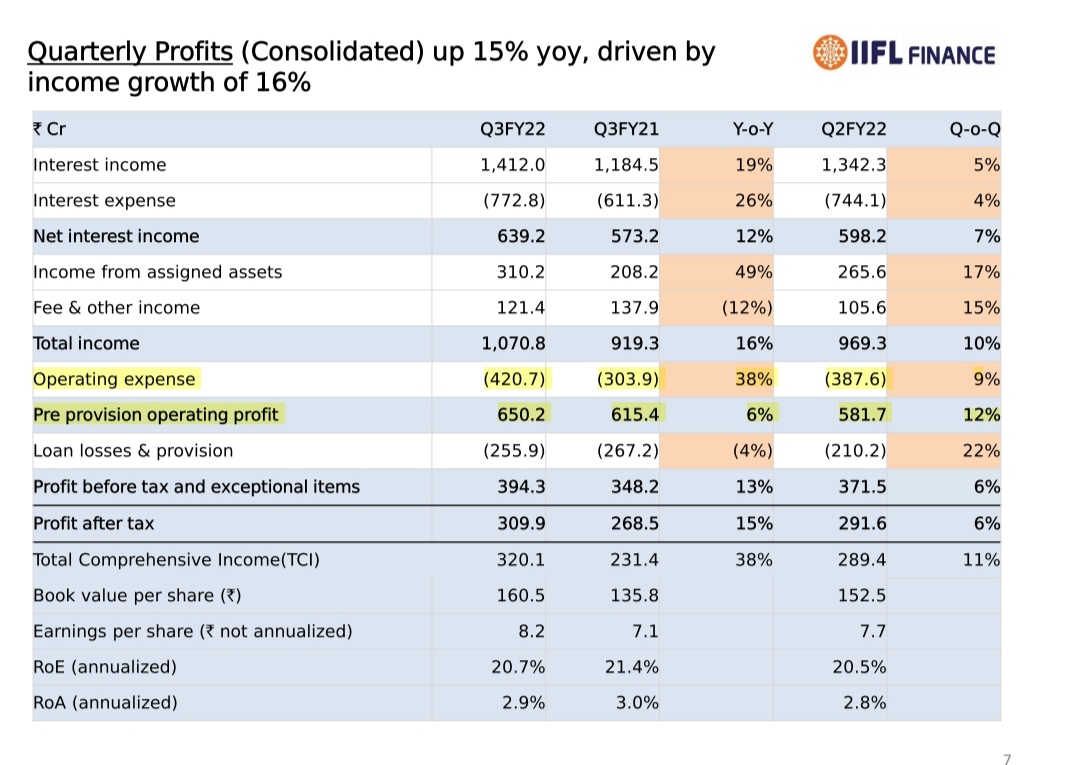

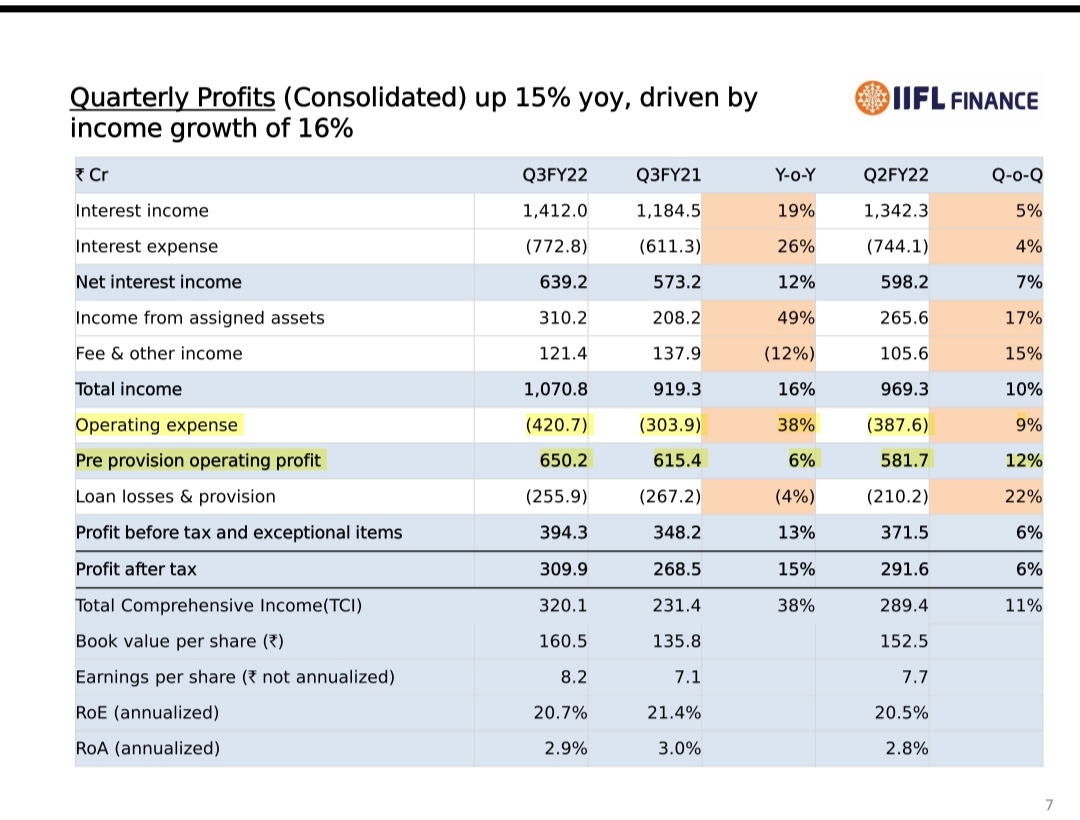

Q3 results are out. Decent result.

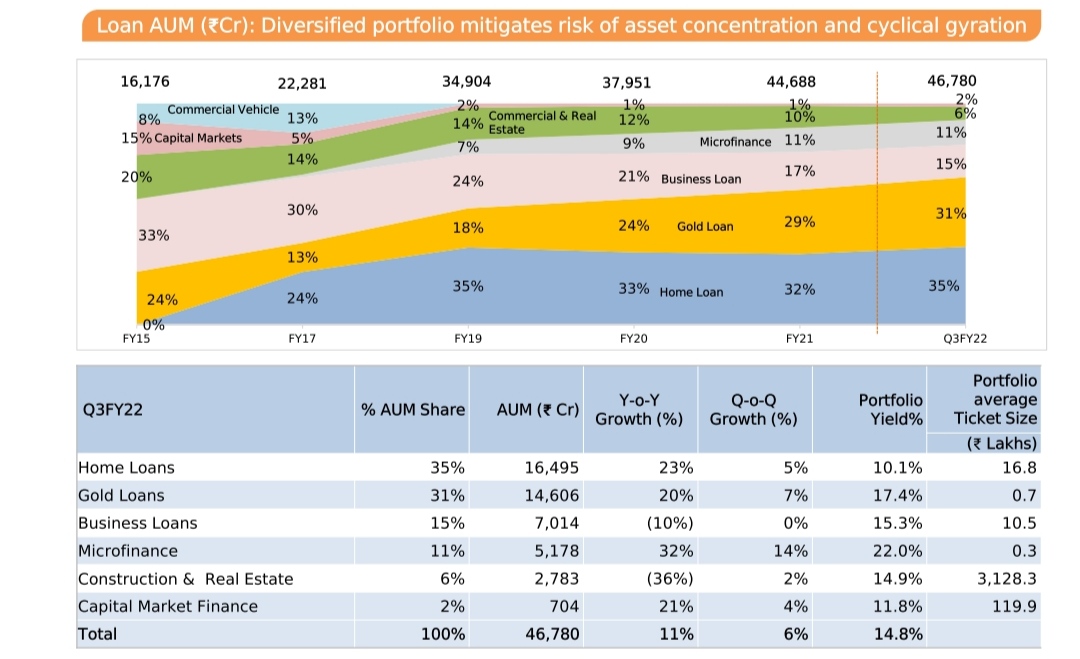

AUM increased from 44249 cr to 46780 cr compared to q2fy22

GNPA/NNPA: 2.8/1.5 compared to 2.3/1.1 in Q2.

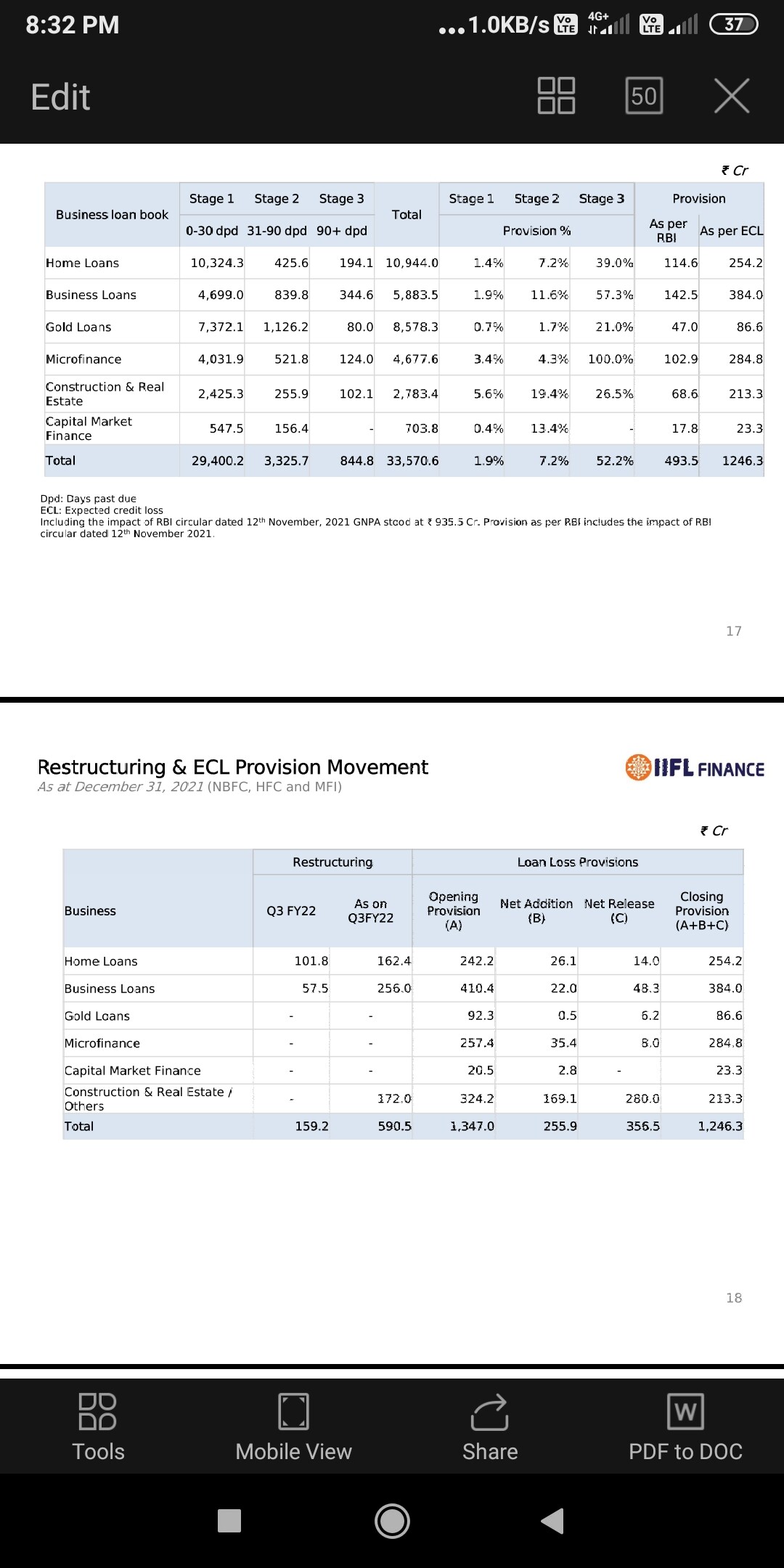

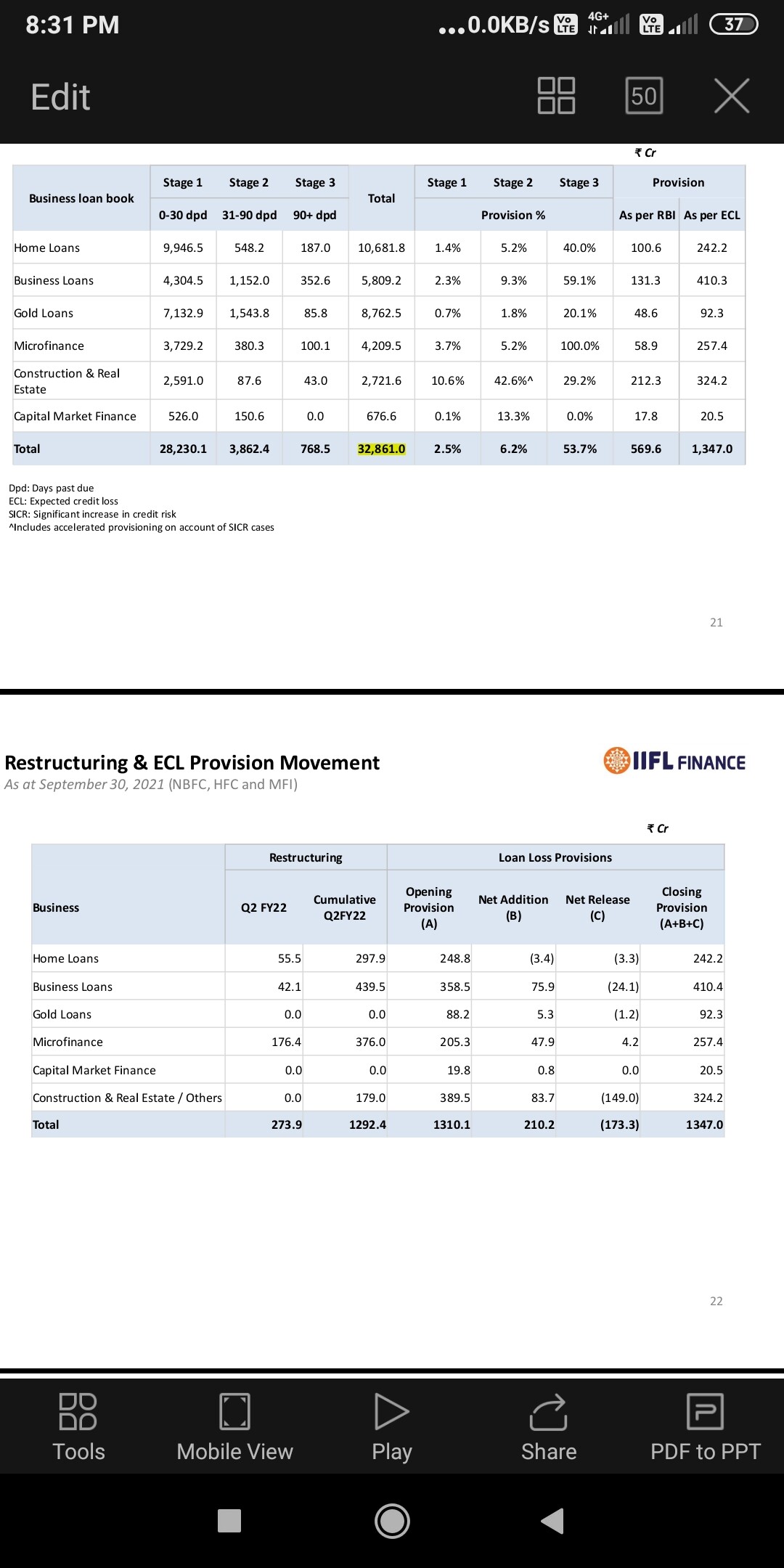

More digging into asset quality: previous quarter GNPA/NNPA was 1017/486 cr and there was cumulative 1292 cr as restructured loans which was possible source of future NPA. In Q3 GNPA/NNPA is 1309/700 cr and cumulative restructured loan is 592 cr. So 300 cr fresh addition to GNPA from those restructured loans. Now going forward the asset quality will not deteriorate more since cumulative restructured loan is low now. Provisions are also low compared to q2.

Operating leverage is kicking in Cost to income ratio is decreased to 39.3% from 40% previous quarter. How ever this should not be compared with Q2 Fy21 because the company is expanding it’s operations. That’s why I’ve compared it with previous quarter

Good pre provisioning operating profit (PPOP) insipte of increased operating expense (due to new branches).

PPOP/AUM is 5.2% compared to 5.0 in Q2. For similar reason as Cost to income ratio I’ve compared it with previous quarter.

Key things to monitor: Asset quality going forward, how much slippage will happen from the remaining 592 cr restructured loans. The growth plans are good. So we can expect decent safe returns if the asset quality remains same, which is possible easily since this 3rd wave is very mild.

Senior member: Is my understanding of the cumulative restructured loans is correct?

I believe when it comes to lending the AUM growth is not a problem because there are plenty of people to take the loan. So growth can happen easily. How conservatively they are lending that matters which is reflected in the asset quality. They are in micro finance, home loan, business loan where there are plenty of scope to grow the aum. They have increased the gold loan AUM by 20% that’s impressive because of the competitiveness of the gold loan market. I’m happy with the loan growth they have shown as I’m against growth at the cost of asset quality.

Disbursement in quarter is flattish because of pent up demand in Q1.

YoY December was ATH in home loan last 1-1.5 years

Growth guidance for next 12 months: around 25%

Average interest has got slight pressure: on portfolio there is 60 basis points decline.

Incremental yield might have fallen by 1%

Falling of yield is because of competitive pressure from banks

But management says that this happens in this industry and they have witness this earlier.

In gold loan you start with low interest rate and if the customer doesn’t pay on time then interest goes up over period of time.

Some players have already withdrawn the low interest rate but the new stabilization of interest rate will be lower than previous standard.

Home loans:

60-65% are salaried customers seeking home loans and first time home buyers. (Blue collared customers)

Yields at 9-9.5%

LTV at 75 to 78%

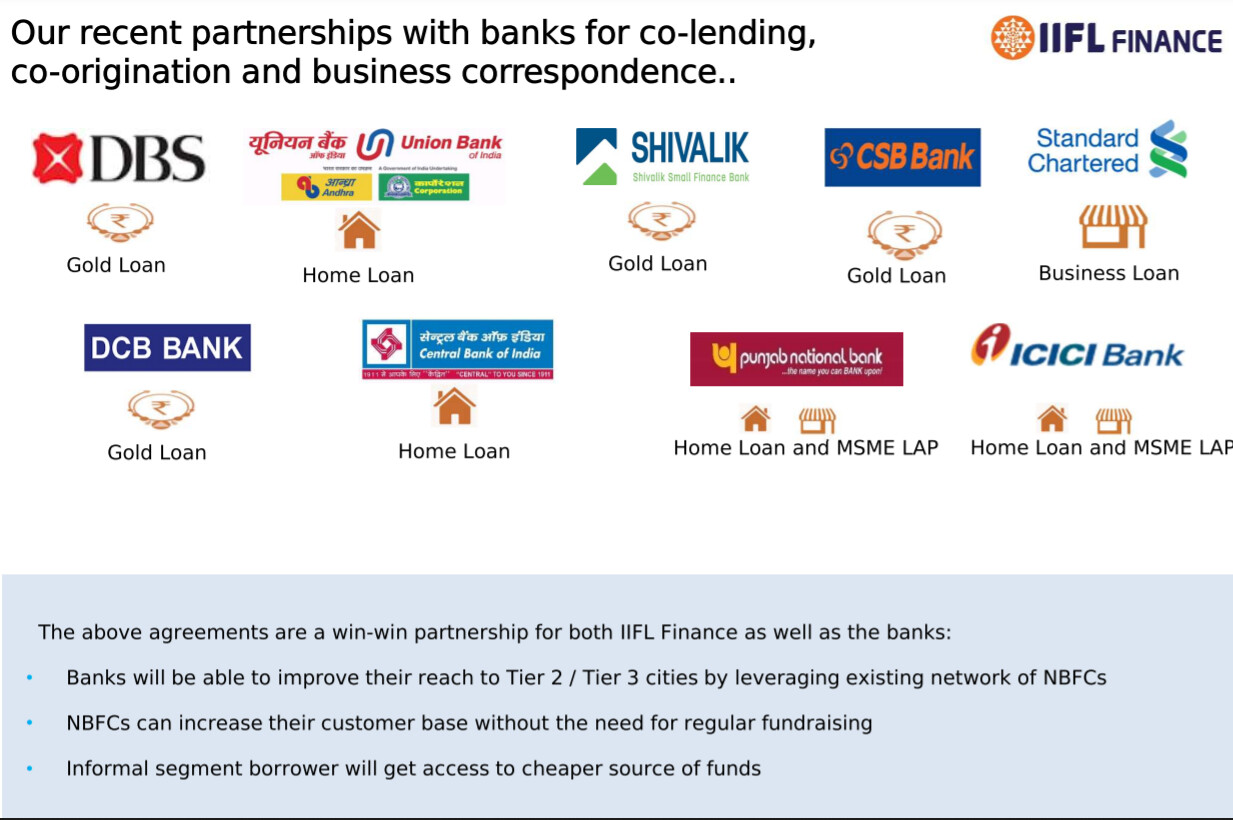

Co-lending

850cr disbursement for co-lending with banks so far with home loans. (only 20% will be on company’s balance sheet)

Half of the total disbursement of loan should be from co-lending model is their internal target

Interest rate remains same in this model.

Eg: Charging 10% interest to customer on Rs.100 that is Rs.10

For that Rs.100 principal amount Rs.80 was provided by bank and if the deal with bank is set at 8% interest then Rs.6.4 (that is 8% of that 80% principal amount) will be paid to bank.

Remaining Rs.1.6(that is extra 2% interest of that 80% principal amount) + Rs.2(10% of the Rs.20 principal amount which IIFL gave from its own books) will be retained by IIFL. Total Rs.3.6 earned out Rs.100 loan.

Rs.1.6 will be shown as Assignment income and Rs.2 as interest income.

I have a view that this gold loan portion is at risk, not just IIFL, for whole industry. Every gold loan players have higher loan book than precovid and now banks do have very higher amount of gold loan.

If economy revives(may be in a year or after 10 years) and banks started giving more loans to SMEs, won’t there be degrowth in this segment. I have seen similar kind of questions to manapuram/muthoot management, their reply is once economy back to normal, banks will go back to their traditional business and reduce this space. And they say running a gold loan business is not easy, but banks are doing fairly well now(except 90% LTV flop show, but they can do the same with 75%)

What if banks, didn’t vacate this space? Will there be any longevity for NBFC gold loan companies

In my opinion, the main competition is the unorganized sector which holds around 60-65% market share.

As you have mentioned, when things start looking good the banks would shift to better yield products and the reason being as Gold loan is not yield attractive for banks plus comes with a lot of operational cost.

But Banks stay or not, the market is quite big and the next growth depends on the execution of players. If they keep expanding to areas where Banks can’t but taking away market share from moneylenders then they will win.

Further, also keep in mind IIFL is also partnering with banks for gold lending.

Muthoot management is also telling the same thing. If everybody starts doing gold loan the market will expand. It’s not like taking market share away from one another. The gold loan AUM growth looks similar for IIFL and Muthoot. Q-o-Q basis it was slow for Q2FY22. Now for IIFL this gold loan growth is quite good. Let’s hope Muthoot will also have good AUM growth in this quarter.

Their PCR is 133% from 175% in Q2. But I guess it will increase again once the things normalise and their NPAs reduce. The restructured loans is the main source of NPAs in my opinion. So once all the restructured loans start to pay we’ll have to wait. We don’t know when the first payment for these loans are due.