Don’t know what to make of this holding structure. IIFL MF scheme Focus Equity owns >5% IIFL holdings in its fund and this is one of the top ten holding along with highest allocation among all schemes owning it. This is unethical if not illegal. Earlier ICICI pru bailed out ICICI Sec IPO. It goes out of my watchlist now.

IIFL Focussed Equity Fund buying a mere 0.06% equity of IIFL Holdings is neither illegal nor unethical.

ICICI Pru case is very different. There, the fund bailed out a clearly overpriced and failing IPO of a group company at the expense of it’s unit holders. That was both illegal and unethical, as determined by SEBI.

In the case of IIFL MF, it purchased IIFL shares from the secondary market and its meagre 0.06% ownership cannot influence the share price of IIFL Holdings in any way. Hence, clearly it has been purchased on the merits of the investment and not to bail out or influence the price of the parent company, unlike ICICI Pru MF.

IIFL Focussed Equity Fund is merely one of the 24 MF schemes that own IIFL Holdings, including several 4 & 5 star rated schemes, who also purchased it from the secondary market on its investment merit.

well, my point was that this scheme is not plain vanila as such. This is supposed to be a concentrated fund and out of which the manager allocates >5% to its own parent to make it top 10 holding. This is also not a large AUM in which they have allocate to the parent equity when IIFL is not part of any major index (Nifty/Sensex). Anyone will conclude that there is a large discretion involved when they could certainly find investment of similar potential.

IIFL is not part of any major index (Nifty/Sensex).

IIFL Focussed Equity Fund, being a multi cap fund, is free to invest across market caps and is under no obligation to restrict itself to Nifty/Sensex stocks. In fact, as on 30-Jun-2018, only about 35% of it’s portfolio is invested in Nifty Stocks. Nearly 50% is in mid and small cap stocks.

The question of unethical behaviour arises only when the purchase of their parent’s shares have benefited the parent in any way (as was the case with ICICI Pru MF). Here, I don’t understand how purchase and holding of a mere 0.06% equity (Rs 12 cr out of Rs 20,000 cr mcap) from secondary market has benefited IIFL Holdings. In fact, several 4 & 5 star MFs hold much bigger amount (For eg, L&T Hybrid Equity, a 4 star fund, holds 10 times more shares of IIFL Holdings than IIFL MF.

I disagree. Always avoid conflict of interest.

Chanda Kochar would not have gotten into trouble if that rule was followed

We would not be discussing this, if not for such potential dubious behaviour of ICICI Securities. Even after that incident, justifying related company holding is futile.

IIFL Holdings Ltd

Highlights Of Q2 FY19 and H1 FY19 Results

Financials

- Net profit grew by 29 % to 301 Cr compare to last year same quarter

- Net profit after minority grew by 30 % to 230 Cr compare to last year same quarter

- ROE stood at 16.4 % for the quarter

- ROA stood at 2 % for the quarter

-

NBFC Business

- AUM grew 40% YOY and 8% QOQ to Rs36,373 Cr

- PAT grew by 70 % YOY to 161 Cr.

- Tier-1 CAR stands at 15.5% & total CAR at 18.7% . Primary drivers of AUM growth are small ticket home loans which grew by 59% YOY, small ticket MSME loans which grew by 113% YOY and Micro-finance loans which grew by 259% YOY.

- In the quarter company had done asset sale of 1492 Cr compare to 2400 Cr in previous quarter so the volumes are slightly lower. The upfront gain booked in the current quarter was completely offset by reversal of gains in the previous quarter.

Key Highlights

- Company has added 208 branches for its NBFC business includes majorly the large number of branches of microfinance - 135 branches, and also quite a few for other product loan.

- Company focus is on retail lending and SME where company ticker price is just about Rs 5 lakhs , small ticket size home loans where ticket size is 20-22 lakhs and micro finance loan and gold loans.

- There is a bit of fall in interest margin since last quarter and one can see that as the liquidity profile of liability changes, there can be some more pressure on NIM but company is geared up to make sure that company have the right product mix and company save on its operating cost and thereby make up for it. Last quarter NIM is also impacted because quarter before last company had a securitization gain coming in. Going forward there will be some impact on NIM but that will be easily be made up over a period of time by product mix as well as having a tighter control on cost

- In terms of liquidity company had repaid Rs 4000 Cr of CPs as a group. Some new CPs that company have contracted are for three months or longer so they basically cross over December. Besides the CPs, Rs700cr of NCD which sell due for payment and all the debentures or bonds have been paid in time and in total company paid about Rs5000cr of debt of short term and long term in the month of October.

-

Wealth Business

- The velocity of the flow of funds, the new money is about Rs5,000cr which has been a similar number for last several quarters and that shows the fundamental robustness and stability of the business.

- On overall AUM of 1,40,000 Cr total market loss on the base itself is just about Rs1,500cr in the last quarter which is just about 1% on an aggregate basis.

-

Securities Business

- Investment business was impacted last quarter and there may be more impact in this quarter because company investment banking revenue is mostly from ECM and which depends a lot on IPOs and QIPs. At least at this point in time it looks like that many issues might have been deferred, and this quarter may be a tough one, but more importantly, the other two segments of securities business which are: retail equities and financial product distribution, and institutional business, are becoming less volatile because the dependence on foreign capital or FPIs or FIIs has reduced.

- Company have been gearing retail investors towards mutual fund rather than direct equity and this trend will continue which will make the business more robust and stable from a longer term perspective.

-

Corporate Reorganization

- Demerger are on track, most of the important approvals like RBI, SEBI etc have already been received. NCLT has convened a shareholders’ meeting on 12th December. Once shareholders under the supervision of NCLT approve it than most of the other things are procedural which is basically submit the approved scheme to NCLT and then obviously the process of getting it listed through Exchanges. Company expect this to be done in the last quarter of this financial year which is as per the schedule.

- Company recorded good growth in Gold and CV loan

- Growth in n LAP and Capital Market loans was moderate

- In Home loans company focus was mainly on small ticket loans to the salaried and self-employed section. The fastest growing segment in home loans is the affordable home segment of Swaraj Loans with average ticket size of Rs13lakhs. Swaraj Loans accounted for 22% of company home loan disbursements in Q2FY19 and 14% of closing home loan AUM.

- Within construction & real-estate Finance, the mix continues to change towards construction finance for small ticket housing projects. As on 30th September 2018. Company had over 7,300 approved housing projects, nearly up by 1.5x from 5,000 approved projects a year back. All company construction finance loans and 50% of home loans were made through these approved projects

- Retail loans including consumer loans and small business finance constitutes about 85% of company loan book. Large proportion of loans are compliant with RBI’s priority sector lending norms. About 50% of company home loan , 56% of LAP, 87% of CV, 42% of SME and nearly all of MFI loans are PSL compliant. In aggregate, nearly 46% of company loans are PSL compliant. The large share of retail and PSL compliant loans are of significant value in the current environment where company can sell down these loans to raise long-term resources. The share of loan sold down currently stands at 15% of current AUM and company Endeavour is to take this up to over 20% in the next few quarters. Company have been selling down both PSL & NPSL loans in 6 product categories including home loan, LAP, SME, CV, gold and micro finance.

- Average cost of borrowing rose by 10bps QoQ and 20bps YoY to 8.7%. Incrementally borrowing costs have risen by 75-100bps due to the liquidity crunch.

- In a rising interest rate scenario, company is in a position n to commensurately reprice our loans. 46% of loans are on a floating rate basis. In the last four month company have raised its home loan rate by 90-100 bps, LAP , Construction Finance, CV, Gold and SME loans by 150bps and capital market loans by 200bps.

- Company NIMS was at 6.8%, contraction of about 50bps QoQ and about 75bps YoY, primarily due to upfront gain of Rs40cr booked on direct assignment portfolio in the previous quarter.

- Medium and high yielding assets currently constitute 52% of AUM. These include micro finance loans, MSME loans, gold, CV and construction finance. The other half of AUM consists of relatively low yielding assets including home loan, LAP and capital market loans. 90% of company AUM comprises of loans that are secured and about 10% of loans are unsecured.

- Company will continue to add branches in HFC, gold and micro finance business and total numbers of NBFC branches have grown by 52%YoY to 1,755. Consolidated GNPAs and NNPAs recognized as per RBI’s prudential norms and provisioned as per the Expected Credit Loss (ECL) method prescribed in IND AS stood at 2.2% and 1% of loan respectively. As a result of implementation of the ECL provisioning under IND AS provision coverage on Stage-III assets stood at 53% and on standard assets at 191bps. ROA was 1.9% and ROE was 16.7%.

- Liquidity Scenario :- Company have positive ALM mismatch across all buckets. On the asset side, company loan book has a relatively short maturity pattern with 28% of loans having maturity of <6 months and 40 % of loans having maturity of <12 months. Company funding is well mixed ncluding 18% from NCDs, 5% from subordinate debt, 35% from bank term loan and NHB refinance 16% from off balance sheet borrowings & 24% from commercial paper. During the month of October company was able to contract new CPs and repay old ones. In October company have repaid and prepaid CPs worth 4725 Cr , also company repaid NCDs worth Rs795cr. Company have liquid investments of Rs2,400cr and undrawn credit lines of Rs1,535cr as on 31st October

- On Digitization company have continued focus on digitization encompassing every aspect of customer loan journey. Of the total 8.18 lakhs loans disbursed in Q2FY19, 99% were on-boarded digitally. Company have focused on backend process digitization through multiple innovations as well as partnerships, helping company to achieve process efficiencies. With 162,000 mobile app downloads in Q2FY19 and 4.4 lakhs cumulative downloads, “IIFL Loans Mobile App” is growing steadily, fulfilling account management and servicing needs of company customers. Consequent to the change in policy regarding usage of Aadhaar company have moved to non-Aadhar based KYC processes across business.

- On Analytics company continue to drive the use of credit codes and automated decisioning across products and strengthened risk mitigation by developing and deploying behavioural score cards for purpose of providing repeat funding of existing customers Company have retrospectively deployed advanced analytics in CV business. Company have tightened its credit approval thresholds in regions company anticipate greater on-boarding risk. There is continued focus on cross-sell and win-back which are analytically driven gold loan win-back generating strong volumes for both gold business as well as group-wide products. Analytics triggers are also being used by Fraud Control Unit (FCU) to eliminate fraud applications in pre-disbursal stage as well as for initiative proactive action in post-disbursal stage

- Wealth Management business

- Wealth PAT computed as per IND AS was at Rs100cr. Asset under advice management and distribution have grown 3%QoQ and 23%YoY to reach Rs1.45 trillion. IIFL Wealth raised equity capital of Rs746cr in June 2018 through a private placement to six institutional investors. Out of this amount company had allotted shares worth Rs652cr and the same forms part of net worth as on 30th June 2018. Allotment of the balance Rs94cr worth of shares was completed in August 2018. Company have 10 bankers during the quarter, taking the number of bankers to 358, to further drive the growth momentum. Company now have presence in 24 locatios and 9 geographies. Company offer range of products and services to participate in a larger share of the client wallet. This includes financial product distribution, advisory, brokerage, asset management, credit solutions and estate planning Company raised net new money of Rs5,171cr in Q2FY19 versus average quarterly run rate of around Rs6,000cr last year. AIF assets have grown 53%YoY to Rs13,676cr. IIFL Wealth Finance which offers loan against securities and margin funding to high net worth clientele, grew its loan book 28%YoY and 10%QoQ to Rs6,191cr. Average lending rate for this book is around 10.5%.

- Capital markets are largely comprises of retail broking, institutional broking and investment banking businesses grew its net profit by 23%YoY. During the quarter company daily cash turnover was up 9%YoY to Rs1,334cr versus 19%YoY growth in the exchange cash turnover. Company daily average total turnover, including F&O was up 59% YoY to Rs21,070cr. Company NSE market share in the cash segment around 3.7 % and in total around 1.9 %.

- Company is continuously enhancing its offerings on digital and mobile platform for retail customers in brokering business.

- Company mobile app “IIFL Markets” has had over 2.1mn downloads. Presently, about 44% of retail broking “IIFL Markets” has had over 2.1mn downloads. Presently, about 44% of retail broking customer made through mobile app. Company completed 4 transactions in investing banking.

Q&A

- On liquidity side company is having 7000-8000 Cr of maturity redemption in November so how company look on it , is it through bank lines, what additional cost do company see over the 75-100 bps cost increase ?

- There do not have 7500 Cr maturity in November. If it is CP then it is a total different thing but company have got Rs 4000 Cr liquidity of which 2500 Cr of cash and 1500 Cr of undrawn bank line. Beside that company have 2000 Cr of securitization which is at advance stage and it will conclude in this week only. So that meets company total requirement of November.

- What outlook does company give on growth overall ?

- Company focus segments will be continue. In a quarter or next company core business of gold loan, small ticket home loan or SME should come back to normal. If interest rates will go up then that can impact the demand itself which is difficult to figure out at this point in time whether interest would go up in a permanent way or will stabilize again back to the normal level. Except that whole economy is doing well and company do not see any let down in growth.

- On GNPA number, there is sharp rise of about 18-20 $ jump on QOQ basis so what was the reason for that ?

- There are two things: GNPA real estate and CVs. In commercial vehicles company recognize on a 90 day basis. Many a time’s truck drivers do not have a culture in terms of availability also and even one installment miss becomes basically GNPA. That is one problem that company is dealing with and grappling to sort it out. Other than that, the real estate sector has lumpy loans. So, company also give GNPA of each product category separately. Other that this two other business remain stable.

- In Real estate book, How many accounts are under problem and which geographies ?

- Company has adequate collateral which is clean and company can recover its money. So company book is fairly diversified, it is not really focused on one geography and in terms of borrower segment also, it is not really a concentrated exposure. But sector is in stress more from the cash flow and not from the point of view of value or the quality of collateral. So over a period of time company will recover its money.

- What is the reason for stress in real estate ?

- Main problem is very high priced luxury segment of Mumbai, maybe followed by some other areas in Gurgaon, if they are premium properties. But as far as affordable is concerned, the small ticket home loans or the builders are building either in the suburbs of large cities or small cities. There things have been stable and moving at least till now. In terms of Industry company exposure is limited . The builder and developer segment is not even 10 %.

- So ultimately the stress in high priced, high value segment because, sales are slow; therefore cash flow is slow and that is causing a concern.

- After SEBI changing commission of upfront and tier-1 now how is the business of wealth management going on and what is the outlook there ?

- Broad impact is on the retro session and commissions has not really changed. From a yield perspective in mutual funds there will be a greater migration towards direct plans as compared to broker plans. The mutual fund part of the business is going to transition to an advisory business over the next 12-18-months, The small variations or the little changes in yield are a function, a little bit more of asset class investments, for example, in the last quarter, and investments are more fixed income biased as compared to equity. That causes a little bit of variation in yields over QoQ basis as opposed to any large change in mutual fund commissions

- In mutual funds now company have 65bps yield so how will it be settle down and what is the trend ?

- Retention will be continue to be in the region of round about 75-80bps, which will be a function of combination of fee-based income as well as fund based income. The fee-based income on a consolidated basis will hover around 55-60bps and the fund-based income will add another 15-20bps going forward.

- In Zero to six month bucket is about Rs8,700cr. Does that include any prepayments in the business here?

- It will be based on the historical trend. So company had take the past data of the foreclosures and prepayment and also the normal payments and then based on that company work out percentage for each product category and there also company will keep updating as trend change.

- The 4,700 Cr of CP that company had repaid is that the entire repayment or there has been like some rollovers also and company is able to prospectively get some rollovers in the market?

- There have been some rollovers as well as some pre-payments. Upto 9th November whatever has mentioned company have already prepaid. Many of the mutual funds are reluctant to take the money back early but when there is liquidity then it is a bit of negative carry. That comprises both, the normal repayments as well as prepayments. Some of that have been rolled over as well.

- Is the unused 5,000cr of liquidity in terms of bank lines and securitization, everything put together this is at group level or for individual ?

- This is only at IIFL finance level. Rs4,000cr liquidity as at 31st October and Rs5,000cr is referring to 30th September, Rs2,500cr will be the cash and Rs1500cr will be unused lines, this is over and above at IIFL Wealth Finance.

- On the real estate side, company average ticket size is about Rs11cr so what would be the highest on the peak side, what kind of lenders company would lend and brief on geographies s and kind of apartments these developers are selling?

- Rs11cr is the average size, but on the higher side it can go up to Rs150-200cr also. So, this is diversified and spread all over the country. So, most of it is to the affordable segment where the apartments are of lower value.

- Will be there any stress for the larger ticket size developers ?

- Yes, so there are one or two cases in the last quarter that have gone into the NPA bucket on which company is working on but in all cases company have adequate collateral which has a value. In case of recover company can recover then company can liquidate the collateral or maybe force-sell the collateral. Company is fully covered but there is stress in the system that impacted the real estate sector more than anything else.

- What will be the AUM target and the margin trajectory from the NBFC point of view?

- There are two parameters; one is liquidity and the other is interest rate. So, unless company is fixed on interest rate, it is very difficult to rework the growth numbers because that is something that will impact home loan business more which is very significant. Almost half of company business s is coming from mortgages. There, it is relatively interest-sensitive because people will defer their home buying, if the interest rate goes double-digit, there is lot of resistance. So company will have to wait and watch how the November month goes in terms of liquidity and how the whole sector and industry recovers from this.

- How is the mutual fund industry behaving post September 20th, are the lines with mutual funds open or they are still figuring out as to how they should go forward?

- There are two types of mutual funds. One of them is still figuring out and some of them have started doing business back in a slightly higher yield. AUM is getting concentrated more in the larger mutual funds. On AUM basis some of the larger mutual funds maybe at a level higher than what they were prior with the prices, some smaller funds are getting decimated completely

- In Wealth Finance business in current liability situation how is the risk management practices in that particular segment ? Give clarification on Ashapura stake ?

- In case of Ashapura company had exposure through NBFC as well as through margin funding. Now, what happened to this company was very unexpected and unusual but the company had a business which had a good track record and a brand and there are people who are willing to take over the company also. So, company have not taken over the shares but there was a pledge created on that because of the large amount, the pledge got reported and being illiquid are a much larger cover. So, it appears to be very significant part of the company. But the family and key people in the company are working on a transition of ownership along with management. So company will not have any loss there. Company have about 32%-33% of the company’s equity for cover and company exposure is about 40 Cr from both these put together.

- So, on the Wealth Finance side company loan book is fairly conservative, company work on 50 % margin and typically most of the book is funded back to wealth clients against their portfolios. In India , clients do not borrow to invest , they borrow against the investment portfolios for temporary liquidity needs. Over last 10 years company had never seen a situation even once since 2008 where company had to incur a single rupee of loss as of now. Even in the current stress over the last 30-45 days company have not really encountered a situation where even on a marginal case of not being able to recover money. So, there is really no need for looking at any kind of provisions on loan against shares book on the asset wealth finance book.

- What will be the mutual fund in the overall AUM and what is ballpark effect on the yield that will get to see once the SEBI rules on trade commission are implemented?

- Company ballpark AUM of mutual funds would be in the region of round about Rs50,000cr, which is broken up into two segments: one is mutual funds, which should go under the broker plan and second mutual funds, should go under the direct plan. There has been a function, what is called an RIA which is the Registered Investment Advisor. Under the broker plan, it will be in the region of Rs28,000-30,000cr, RIA would be another Rs20,000-22,000cr. Typically on the RIA company do not get any commission. Company work on advisory fee basis from the client. On the Rs28,000 cr, company retro session on a trial basis because company discontinued upfront for more than a year on mutual funds, in the region of about Rs135-140cr a year which is round about Rs35cr a quarter which makes up about 14-15% of overall net revenues. This may come down by round about 5-6%. So, effectively 14% of revenue will be down by round about 5%. So, there has been impact of round about 0.8% of revenues because of the SEBI change in TER commission laws.

- In six month bucket there is cumulative outflow of Rs 12,339 Cr does it means that there is redemption of borrowing or are these the redemptions of company borrowings plus the disbursements that company need to make ?

- This is a static liquidity, so these are the redemptions of borrowings and the committed payout.

- Why there is no assignment income seen in 2nd quarter ?

- New IND AS accounting standards have come to effect from this financial year and company is trying to understand and getting stable in terms of how the accounting will take place. So when the last year accounts were re-cast based on those company provisions were created for every quarter separately. This year 1st quarter company had an assignment of 40 Cr of Income was there upfront which is booked. But in hindsight company realized that maybe this was a little aggressive booking on the income because there are some prepayments that have happened and the actual accrual may vary from quarter-to-quarter, eventually it may be little lesser than this. Out of that there was some reversal this quarter and whatever new assignments company have done . Company had reversal this quarter of almost about Rs14cr which more or less matches with the income on the new assignment. So that is why there is QOQ fall in IND AS accounting profit for IIFL Finance.

- On the fund mobilization side on the IIFL Wealth business, how should company really be thinking about it in terms of the AUA growth going forward ?

- About 20% growth in corpus YoY approximately with the (+/-5%) variation , So, effectively this year Rs20,000cr-25,000cr of net asset flow into the business is essentially the guidance number which effectively translates to about Rs5000cr6000cr of corpus on QoQ basis, stripped out for the mark-to-market impact on the portfolio.

- Going forward which products will drive the growth momentum ?

- From a portfolio allocation perspective, it is kind of a diversified portfolio with a broader mix between fixed income and equity. At current time nearly 54%-55% of the assets would be in equity at equity constituents, 45%-odd would be broken up into fixed income. Within fixed income, most of it would be in AA+ to AAA kind of categories through mutual funds or direct holdings. On the equity side, again, it will be a combination on mutual funds alternative investment funds PMSs and little bit of direct equity. So, it is a fairly diversified portfolio. There is no change in it. Clients will continue to spread their allocation between all these instruments. On an asset allocation basis if markets continue the way they have been for the last 30-45 days you might see roundabout a 5% shift from equity to debt, but that is about it. So company expect it to be in the region of 45% to 60% in fixed income and 45%-55% in equity going forward. From an instrument perspective, not many radical changes, obviously, on the high net worth side alternates has an alternate investment funds, have a bigger share of new flows as compared to equity funds. So, that is the only kind of new trend company have seen over the last 12-18 months, but barring that really it is the same old instruments.

- On the AIF side and PMS side will the risk of realizations going down given the fact that mutual fund TERs have come down as well?

- Alternate e investment funds and PMSs fees have been much more competitive than mutual funds for the larger ticket sizes. So, contrary to typical perception for clients who put in Rs5cr-Rs10cr cheque into alternative investment funds and PMSs, unlike a mutual fund have a tiered fee share of management fee structure. So, some other client is putting in Rs5cr-Rs10cr, even today before the reduction of TER of mutual funds because client was able to get a management fee share class, which was nearly 50-70bps cheaper than a regular share class in mutual funds and possibly 25bps cheaper to what could get in a direct plan in a mutual fund. So, PMS and AIF in that sense have already been fairly competitive. In case direct plan fees in mutual funds come down even more, right now on an average direct plans 125bps. In case direct plan fee structures come even lower on the mutual funds, then company see some 25bps reduction in fees in PMS or AIF, but otherwise company do not really see it, because that change has happened practically over the last two years for all large clients.

- Does the stress will continue in premium segment developer inventory due to lower off take ? Does the price also coming down due to this stress ?

- it will continue for some time. So best scenario will be time correction with the prices remain static where value of interest of money becomes cheaper. So in High price segment the area is Parel, Worli area, lot of constructions that has happened there, it can continue for some time.

- Prices are already coming down So if a client have money and if he go with the cheque than he can have discounts.

- When company will acquire the shares than who will buy it ?

- Company will just pledge it and sell in market and company will never acquire the shares.

- On wealth management what is the mix of equity in net new money this quarter? And on the fixed income side, that company have raised the money. Is it coming in liquid instruments which are like very low yield or is it coming in any other structures company would have fixed income ?

- In gross flows fixed income is a large portion this quarter, 70% would be the breakup of fixed income in the gross flows. Approximately, gross flows 65% to 70% has found its way into fixed income and related instruments, 30%-odd in equity on the gross flow side.

- In terms of fixed income, is money coming on extremely low yield liquid kind of instruments or is it any other structures that company may have ?

- No, it has been a combination, so most of the money in the last 30-days specifically has come into fixed maturity plans. So, fixed maturity plans obviously have a lot flavor, but typically a three or three-and-a-half years SDL kind of FMPs. So, typically low risk FMPs is something which has got in a lot of attraction. Company also closed large private equity fund which was essentially a private equity fund of professional entrepreneur, so really where the fund owns a majority of the business, so that fund closed around Rs1000-odd Cr, so large part of that collection happened in the last quarter. That also in a sense is immune to market levels and the fund is more or less sitting in cash right now because company enter the business pretty much at face value

- What is the reason behind operating expense in IIFL finance going up QOQ and YOY at much faster pace compare to the net interest income or even the total income ?

- Number of branches and people have grown up significantly . Number of employee are 85 % up YOY because the microfinance, the new business that company have taken over , company also building strength in housing finance and gold loan, but going ahead it should taper off, the pace of growth will slow down for sure, but last year number of people that company had added is very large number. So primary reasons are branches and employees.

- On wealth side what is the outlook going forward in terms of ROE will it go up to 25 % and what are the levers that will push that number higher ?

- In wealth company raised capital last quarter and that is what has depressed ROE of wealth and thereby for the group. So as company start using this capital more effectively over the next few quarters, then company will see TOE moving up to the target level.

- What can be steady ROE for the wealth business ?

- Steady state ROE for the wealth business should be around the 25%-27% region. Company was having acquisition in mind over the last three to four months which was the part of the reason for raising a bit of the capital, and secondly company wanted to reduce dependence on CPs, so that essentiality led company to raise a bit of capital in the second quarter of the calendar year and over the next 12-odd-months company had charted out on next growth path. The third utilization of the capital is essentially to act as a sponsor for alternative investment funds, that business is growing fast company have nearly got $3 billion, Rs20,000cr of capital commitment in that business. Company end up putting 1%-1.5% of sponsored money as own capital contribution. So, these three things essentially are where the capital will get utilized and as the business scales up, the ROE should move up.

- In last three-four years consistently company have been around 20s in terms of ROE. In next 12-18 month company will back to 20-25 % ROE number.

- In IIFL finance what was the reason for loan loss provisioning coming down ?

- Yes, because the last year provisioning was abnormally higher for the new accounting IND AS in which company have to consider expected credit loss on each and every item. So, relatively it is appearing low because last year is extraordinarily high.

- On expected growth going forward how do company see its AUM and the net interest income going forward ?

- Historically company have given guidance of 20-25 %. So there is no change in that. Company will grow 20-25 % on topline and if company can manage the business efficiently and improve the margins, then 25%30% on the bottom line

- On the IIFL wealth consolidated results in the footnote, company have mentioned that in Q2 FY19 company had a lower weight-age of offshore subsidiaries in the PPT. So, is it like the offshore subsidiaries are also slowing down for a particular reason?

- This is about the tax as there was very high tax evidence in Q2, that company has provided for dividend distribution tax on the dividend received from overseas subsidiary.

- There are three basic impacts because of the tax calculation:

- Company have done a dividend done out from offshore subsidiary to India so there is an incremental 15% impact on the dividend, it obviously help to save on the cash flow of the dividend distribution tax.

- NBFC business was taxable at 25% last year because of the business company acquired last to last year, therefore the revenue was less than Rs250cr, so that business is back to 34% in terms of tax.

- The offshore business contribution to profit is not in the same percentage terms as it was over the last two years. The domestic business is much larger than the offshore business which is having a small impact on the tax rate, but the larger impact on the tax rate is on account of the dividend distribution tax and the NBFC moving from 25% to 34%.

- This dividend distribution tax can be completely offset against the Rs5/share dividend that wealth will pay, because this is a wealth subsidiary but on number on YOY basis then the tax provision has gone up significantly because of that.

- What percentage of lending book has exclusive charge and what percentage would be on pari passu?

- Almost company entire book is exclusive, company primary charge has to be the first charge and exclusive charge. All the collateral that company have is by its internal policy , there has to be exception for pari passu but almost entirely or predominant part of collateral is exclusive not pari passu.

IFL Finance: IIFL Securities has allotted 1 share of IIFL Securities for every 1 share IIFL Finance and

IIFL Wealth Mang has allotted 1 share of IIFL Wealth Management for every 7 shares of IIFL Finance on June 06, 2019.

I do not see either IIFL Securities & IIFL Wealth Management listed in NSE/BSE. When can we expect them to list?

This should take few more weeks

Nyone tracking\holding its demerged cos. ?

IIFL Finance and IIFL securities seem to be value buys now.

Buyback is very likely to get approved as insider hold more than 50% shares. Fairfax India which holds nearly 26% of IIFL securities valued cost their stake around Rs. 84 after demerger. Immediately after demerger around September there was decent buying from insider around price of Rs. 25 and then again in Nov 2019.

I am surprise to see hardly any price movement in the stock but may be it will start moving after buyback is approved and actually executed. As per NSE website free float is only 530 cr. so buyback of 90 cr. likely to have impact on the price.

Hello, i am Harsh Visharia.

as we know the entities have demerged from IIFL holdings into 3 different companies,

IIFL security, IIFL finance and IIFL wealth management.

I would like to share my research on IIFL security here and would like to get some feedback on it.

Also as the promoters are common, so investors holding IIFL finance and IIFL wealth management could also read the promoter analysis part.

(I had posted this article on my blog on 11th November, 2020

Link here: IIFL securities stock investment idea: 10x in 10 years ~ Shareholder Awareness Program )

(I am writing its content here and in the end would also add onto the recent developments)

(This might take some good 10-15 minutes to read the whole post, here we go)

IIFL securities: 10x in 10 years

Flow of the article

Explaining the flow

Introduction

About the business

Demerger

Brokerage business

Land bank they have

AAA (advisor anytime anywhere)

Other business IIFL markets etc.

Financials & Ratios

Valuations (using DCF) and multiples like P/E and P/B.

Promoter and Management analysis (very important)

So let’s begin:

Introduction

I searched on internet regarding IIFL securities, but there aren’t many articles which can interest an investor.

Even the valuepickr forum has threads about the old IIFL holdings but not of the demerged entities.

Today I want to present fundamental analysis of a FinTech stock which has potential to become 10x in 10 years,

Its IIFL securities.

About the business

Demerger

First of all let me provide details of demerger of IIFL holdings

Record date for demerger 31st may 2019

Demerger ratio

For every 7 shares of IIFL holdings.

Investors will get

7 shares in IIFL finance

7 shares in IIFL securities

1 share in IIFL wealth

Brokerage business

Let’s talk about the brokerage business

IIFL securities is a traditional brokerage house in India has 2, 52,498 active clients as on the date (source: chittorgarh)

It has more than 2500 branches as on date.

(50-60 owned and rest are of sub brokers)

As any other traditional brokerage house it faces competition from discount brokers.

Once IIFL holding promoted 5 paisa (now demerged) it has 6 lac active clients and 3rd largest discount broker after Zerodha and upstox.

Because of conflicting nature of both IIFL Securities and 5 paisa they demerged but the management had an idea that there is a huge market potential for discount broker and hence started the 5 paisa venture.

However coming back to IIIFL securities

The brokerage business will be the cash cow for the company, it will grow but not as fast as the discount brokers, if you look at the historical income statements of IIFL securities you’ll see cyclicality in it, as it’s the nature of the markets.

To counter this cyclicality they ventured into NBFC business of wealth management and disbursing loans, through IIFL wealth and IIFL finance, but they are now demerged entities, now they came up with the idea of AAA to counter cyclicality of markets. (More on that further)

Pros: long established brand value and reputation in the industry.

They are expensive but fully service oriented with branches, research & advisors, RM’s, this also makes them profitable.

Cons: they have tough competition from discount brokers,

They are not banking related brokerage firm.

Coming to the land bank that IIFL security holds.

IIFL securities holds substantial real estate in terms of office space which it rents out to its associate companies and earns rent.

Its earning through rental income is approximately 55 crores annually

(As stated by management in recent con-call)

Buts its profitability is not good as major chunk goes into the finance cost.

They hold around 6, 34,459 square feet spread across multiple locations from Ahmedabad to Mumbai to Pune. They are carrying it at book value of roughly about 300 Crores and the market value is close to about 700 (source link : concall of Q2 FY21)

Also the management plans to unlock value through sale of its real estate, but they have to make debt payments against it as well.

However in future they could post exceptional gains when they sell some of their real estates.

Let’s see what AAA is about in short.

AAA (Advisory anytime anywhere)

I had seen many advertisements on TV but didn’t paid much attention to it at first.

After doing a little bit of research I understood that this is the ‘FinTech’ start-up kind of venture.

After all what PayTM has is a software which makes it convenient for users to transfer cash to each other.

Similarly what AAA is: a technological software which makes it extremely convenient for distributors to carry on business!

Its competitors are NJ India, and Funds India wealth advisor.

They also provide software to distributors to provide convenience in carrying out business and in turn take a share in profits earned by distributor who uses their software.

Let’s see what the management had projected and said regarding this venture.

R. Venkatraman :AAA is a tab based order entry risk management back office for independent financial advisors, including sub brokers, so this is one tool in which you can not only do stock broking, but also buy mutual funds, buy insurance, debt products and it has all encompassing comprehensive solution. ~concall 18th, May 2020

On the Concall in May2020 they said they have roughly 1000 sub brokers using AAA.

In this article we can see that Nirmal Jain chairman of IIFL said that

“Currently we are targeting tier II and tier III cities, soon to make it multi-lingual with Gujarati and Hindi in the coming months. We have invested nearly Rs. 100 crore and aspire to sell 100,000 tablets in 2019 across more than 1000 IIFL centres. We are betting on Jio’s growing network across India” (source link: BFSI Economic times)

I am very excited because the growth potential from this venture is tremendous.

This venture has the potential to add more sub brokers in turn aiding the growth of traditional brokerage business as well as growing its income from financial product distribution (FDP) as well.

Other business of IIFL securities:

Security broking currently contributes 67% of income.

Advisory income and distribution of financial products (FPD) contributes towards 13% of total income.

Other than that its real estate business contributes to its revenue

and also the investment banking business which undertakes IPO’s, FPO’s, QIP’s, rights issues, share buyback, advisory and M&A also contributes to its revenue.

Let move to next part that is Financials and Ratio’s

As the demerger happened around May 2019 we don’t separately have annual report for the company prior to FY2020’s

We will take the help of the investor presentation to check its performance.

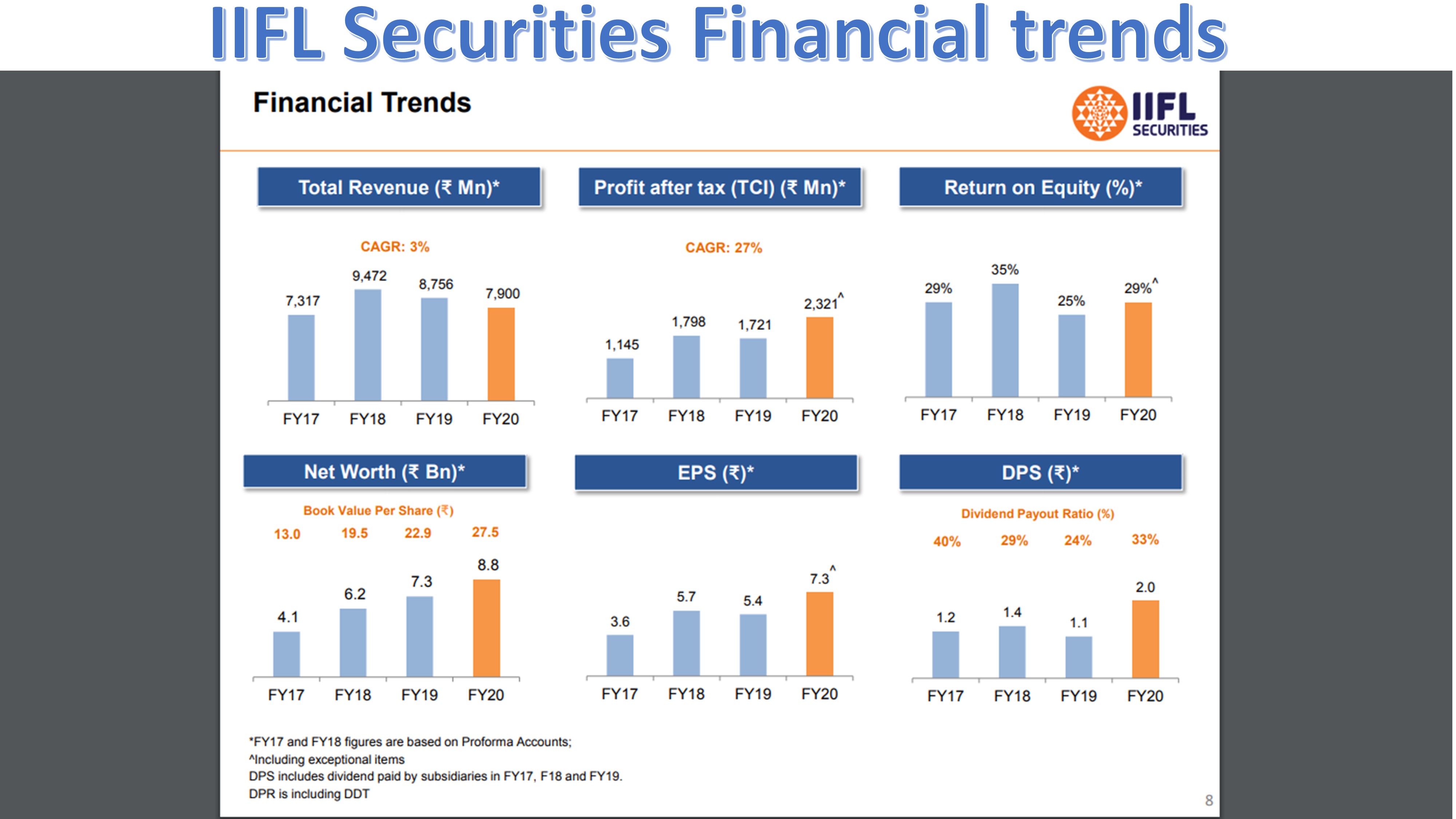

Here is the picture.

Here all the basic metrics such as growth of net worth, earnings per share and dividend per share is given.

And also the return on equity (ROE) is given which shows a consistent figure of more than 20 percentage.

ROE reflects quality of earnings: ability of company’s business to generate super normal profits. This is the reason why most High ROE companies trade at high P/E multiples

(But our IIFL securities is trading at single digit P/E multiple)

Let’s move onto Valuations part.

Let’s compare the IIFL securities with Motilal Oswal and ICICI securities. (As on 6/11/20)

stocks----------------stock price ----- market cap----- P/E ratio ----P/B ratio ------ROE %

ICICI securities------ 454.15 ------14632.49---------19.21---------10.06--------------52.37

Motilal Oswal---------- 560.60------8169.59-------------32.77-------2.79 --------------8.51

IIFL securities---------38.70--------1236.89--------------6.40--------1.52--------------23.73

As seen compared to peers it’s one of the cheapest stocks available,

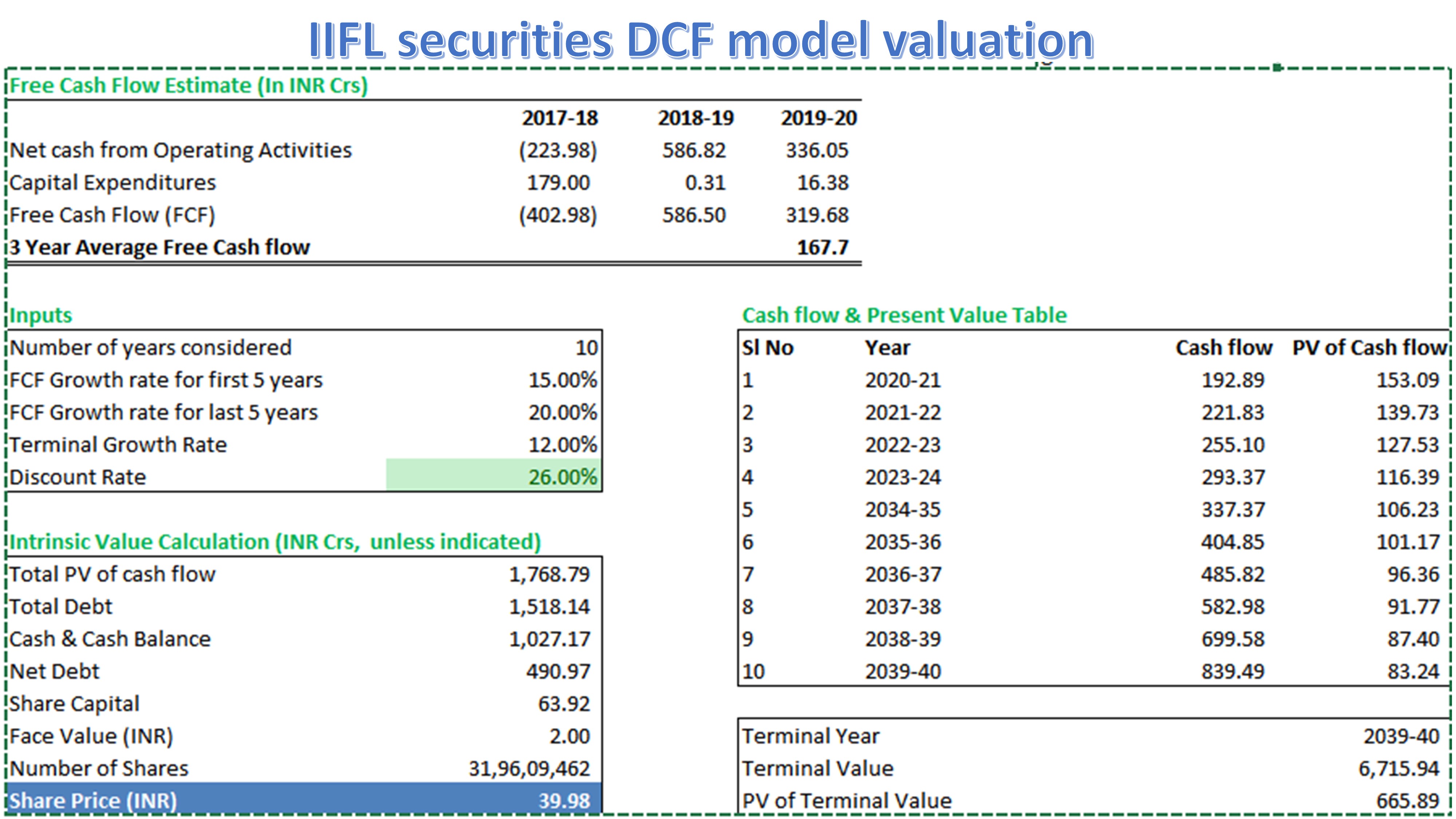

Let’s do the DFC (discounted cash flow) valuations of the stock

(Now obviously you could take different rates and the fair value would be higher or lower, that’s why I have given all my figures and assumptions here)

In the picture you can see what assumptions we have taken, and according to this the fair value as of today comes in the range of 39.98 to 50.37 rupees, for the current year FY 21.

And because the discounting rate is 26%, we can calculate fair value after 10 years which comes in the range of 403.22 to 508.06 rupees.

In this manner I assume the stock to grow 10x in 10 years from the current levels.

Moving on to the next part

Promoters and management

I believe that however good the business and valuations look prima facie,

It’s the management which matters the most.

Unfortunately it’s not simple task to do analysis of management also this process is very time consuming,

So even my analysis could get updated with the passage of time.

So Moving on:

IIFL was promoted by Nirmal Jain (aged 53 as on 2020)

The promoters currently hold 29.8% shares

Fairflax currently holds 35.4% (they intend to be passive financial investor)

During 1999 they decided to offer equity research free of cost to public.

During 2000 IIFL launched 5 paisa per trade scheme for its online retail customers. Retail customers needed to pay just 0.05% instead of 1%-1.5% levied by other brokers. This helped IIFL gain a lot of retail customers and also started a price war in the brokerage industry.

We’re talking about the year 2000. It was his vision at that time and those disruptive tactics have worked well for IIFL group.

(Source link : for 1999 and 2000 year disruptions)

Years later his original concept of discount broking got converted into 5 paisa company and are at no. 7 with 6,31,514 clients.

Later as the company grew they ventured out of only brokerage business and started wealth management as well as disbursement of loans such as housing, car loans, gold loans, they also became distributor of financial products and started their own Mutual fund AMC.

Fairflax promoted by an India Prem wasta, who resides in Canada is known as Warren Buffet of Canada, he says that he invests in well managed companies with integrity and always takes a long term view of his investments.

Fairflax owns investment all over the world in India it also owns majority of Indian company Thomas cooks.

Fairflax become the client of IIFL, later an investor holding 9% stake in 2011 and later they went on to acquire more stake through open offer, raising their stake to 35% in 2017.

Being a financial investor larger than promoters gives investor a confidence that yes they have interest in wellbeing of the company and will monitor the working and operations of the company closely.

Originally in 2005 they came up with an IPO giving shares @ 74 rupees

They did a split (5:1) in 2008 now let’s take the price of IIFL holdings in 2019 as 450 rupees.

This means the shares have multiplied your wealth by 30 times in 14 years that comes to around 27.62% CAGR returns.

(That’s not even counting dividends)

From the above study it’s clear that management has right intention and right vision to move ahead, there is big shareholder named Fairflax to scrutinize everything and make sure that the level of corporate governance remains high.

It’s certain that I don’t need to worry about the intention of the management now even if company fails then it shall be business failure,

And as we have studied they have their new FinTech product ‘AAA’ ready, also the management is innovative and disruptive which will certainly ensure survival of business.

Nirmal Jain has worked well and certainly created wealth for shareholders, but the real question is:

Will this innovation and growth sustain? after all he is growing old. (His age 53 years)

Well at least for the next 10 years he would be capable to actively handle and contribute towards the company so let’s not worry for the next 10 years

One more study I would like to present is :

On 13th march 2018 IIFL holdings made a high of 874 Rupees

And if we compare same demerged shares their value is

IIFL sec (38.60 Rs)

- IIFL finance (84.75 Rs)

- IIFL wealth (908.75 *(1/7) Rs = 129.82 Rs)

=253.17 rupees

This comes to around 253.17 Rs which is 71.03 % discount from its peak, while the business & profits have only grown since March 2018.

This according to me is value investing in real terms.

Conclusion:

From what we have studied I conclude that

-

We don’t need to worry about the intention and integrity of management, they seem to have good track record and background.

-

The company is innovating constantly, which is essential for survival, also the venturing into FinTech space through ‘AAA’ seems promising, so business prospects looks bright.

-

Very good financial performance and ratios, as mentioned constant high ROE which was above 20% and a good Dividend pay-out ratio.

-

It is such a brand and well known B2C business which every reader must have at least heard off, thus establishing brand value and reputation of this company.

You will find many such fantastic companies but the main point to focus is valuation.

All other such quality companies will be trading at high valuations BUT IIFL securities is trading at a P/E multiple of just around 7.

With a combination of

Good management+ bright business prospects+ cheap valuations

One should definitely not ignore investment opportunity in IIFL securities.

I would repeat this thing again

IIFL security could be a multibagger, it has potential to become 10x in 10 years.

Scrip code: 542773 market cap: 1236.89 crores

Stock price 38.70 eps: 6.05 rupees

(Disclaimer: I hold small quantity, and would like to read your views, questions on this research so comment down below, what do you think?)

this is what was written in blog article now coming to Recent developments

So after writing this post IIFL securities also announced a Buyback of 90 crores from open market for 5.21% outstanding equity shares at price not exceeding 54 rupees.

This in my opinion is positive sign that management recognises the undervaluation of Stock and is ACTING to improve it value,

(Also in the recent ongoing IPO of M/S Bector foods one of the merchant banker handling the issue is IIFL securities)

Now the share price has gone up to rupees 47.25 and market cap is 1511.70 crores, but it’s still within fair value price range as I mentioned in my DCF calculations.

Notes:

-

Do your own research before taking investment decision.

-

I would like feedback and comments on my research.

-

and I still own the same small quantity of stock (only in IIFL security)

Thanks for the detailed write up @harsh_visharia. I believe your free cash flow estimates are very high. I believe free cash flow estimates are missing maintenance and growth capex required by this business.

IIFL securities has broking (retail & institutional), investment banking, asset management and financial product distribution businesses.

IIFL full service broking business model is definitely challenged world over by discount brokerages. Given the rise of cheaper alternatives, value proposition of IIFL securities full service model is questionable. Brokerage research tend to be a tool to attract investment banking and institutional broking business. I wonder if they start charging separately for research how much revenue and profitability that business will bring. Europe already had introduced such regulation (MIFID) and see it being introduced in India in next year. Running sell side research operation is expensive and its utility to bring in additional revenue and hence profitability is questionable. It is not apparent in the consolidated financial of IIFL securities but there are hardly any profitable equity research or specialized/trade publication businesses world over.

IIFL investment banking seem to be sub scale businesses. They will need to invest heavily and compete with much bigger player to be relevant. It might be okay business but will remain only fringe player in the IB league table for foreseeable future. Here they will be competing with foreign MNC as well as large deposit banks in India. IIFL expertise might be middle market ECM but even then IB employees will be making money but return of the investment banking are questionable. Again not enough standalone investment banking businesses in India to compare but similar businesses are struggling globally. With similar industry dynamics and similar foreign players, I don’t see how outcome will be different in the Indian Market. Would company prefer to higher IIFL securities as their investment banker over Morgan Stanley, GS, JPM, BoFA, Axis, Kotak, HDFC Bank, ICICI Bank?

Asset management business has minuscule AUM of 3000 cr. and mostly loss making at this point. It will be relevant (profitable) only if they can break into top 5-7 players which seems almost impossible except through inorganic growth. I believe we will rise of passive investment in India in next 10-15 years and active MF industry will shrink dramatically.

Financial product distribution business could be very high ROE and margin business but not clear competitive advantage of IIFL over other players in this market. Banks, finch startups, product originators’s own distribution channels, digital only insurance players and possibly telecom players such as Jio, Airtel leave very less room for financial product distribution for IIFL. Fintech start up platforms are raising billions $$ and ready to burn that money to gain market share. IIFL securities seem to be going in other direction with share repurchase plan using existing assets.

Valuation for cheap for this business especially considering real estate holdings. It seems there is less debt liability for these real estate assets and hence they would probably have value of around 500 cr. It remains to be seen after tax value realized from these holdings.

Insiders purchase after demerger last year in Sept and then again in November indicated bottom. Upcoming buyback signals undervalued stock as per mgmt. It is most likely to provide bounce to around ~55.

IIFL had published cost basis for demerger and that indicated price of the IIFL securities around ~80-90/share.