@sameernics from which website did you get this data? (the image)? could you pls tell the name or share its link ?

2 Likes

One of the recent interviews of top management of IGI.

1 Like

How is the Rupee Vest platform relevant to the IGI thread?

1 Like

@sameernics posted an image displaying mutual funds buying more of IGIL. He did not mention the website name.

@garade asked Sameer which website the image is from.

@GrowthValueInvester replied posting the website link.

Had the stock page link been posted, instead of the homepage link, it would have been clearer.

3 Likes

You’re right, but most of the buying was done through passive funds so we’ll have to consider that while evaluating.

Disc: Invested.

1 Like

the stock IPO’d only recently right ? and it’s a part of an index already? which index is it ?

A double-edged sword kind of situation for IGIL

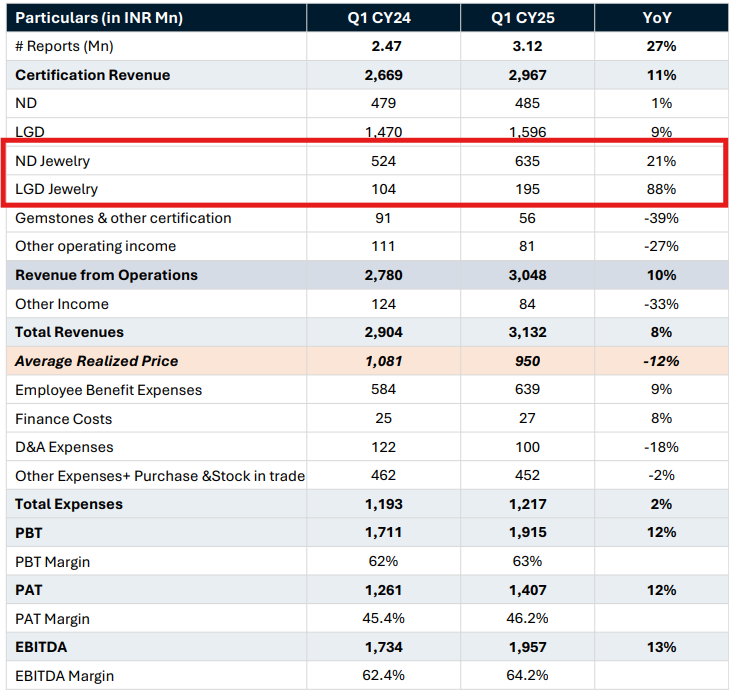

In order to increase certification revenue, company is focusing more on jewellery segment, which has stunted ARP(average revenue per report ) compared to other segments. contribution of ND&LGD jewellery to revenue increased from 23.5% to 28% yoy, so the question is how much can they stretch this exposure. ND&LGD jewelry’s growing influence on revenue leads to 1) moderation in ARP which is bane 2) jewellery segement is volume driven, which is boon. If the volume growth is not maintained it will have Amplified adverse impact on topline growth.

2 Likes

This time, the management during the con call sounded more positive with the business momentum and future outlook. The management has guided 15-20% revenue growth on consolidated and standalone basis for CY 25. The margins are expected to be sustained between 57-64%. The volume and revenue will be driven by ensuring right mix across the portfolio. The bulk of revenues will be generated from India. 60% of revenues are not impacted by US tariffs. The company is adding more capacity by way of gemmologists and infrastructure to cater to increasing demand. The strategic decisions taken are helping their European subsidiaries to perform well, which was evident in their consolidated numbers. The management reiterated there is no much seasonality factor in their business, so next quarter will be similar to gone by quarter numbers.

Below screenshot is from their press release.

3 Likes

All the discussion about IGI is based on views how consumer preference will be in the future(along with change in cost of manufacturing LGDs). I think, all agree that cost will decrease. Has anyone given an estimate for where this decrease will end? As for consumer preferences, we can only make some assumptions. I think it will be highly dependent on economic cycles. What if cheaper diamonds means more consumption and entry into hitherto untouched markets? There are a lot of things that we don’t know the answer to. I suspect the management doesn’t either. I have a dozen questions and I can not write all of these here. As such, next few quarters will make a few things clear to us.

Disc :Invested a small amount in the IPO. Bough some more in the volatility. No transaction in last 30 days.

3 Likes

Can someone provide a quick summary of the article, as I don’t have access to it?

One thing is clear: this will likely remain a business with a maximum growth potential of 15-20%. However, considering the high profit margins, what price-to-earnings (PE) ratio might the market assign? It seems unlikely that the stock will return to the days when it traded above ₹600.

D: Invested

3 Likes

The article states that tariff impact will lead to higher cost of diamonds in US, lower demand and impacting IGI volumes.

in this thread considerable amount of discussion has happened on the relevance of certification providers (the likes of IGI) going ahead with rapid propagation of LGDs and ever declining price trend for LGDs. Just trying to add to the mix - with part subjective and part data backed view.

-

On Natural Diamonds Certification business: Rather than being a threat to certification business, spread of LGDs should be seen as counter force to drive certification for Natural diamonds. To avoid adulteration and ensuring authenticity, certification will be even more relevant and sought after, as LGDs gain currency.

- At industry level, total ND volume is of ~26 mtc). the penetration of certification for natural diamonds is ~65%.

- At a sub-segment level, 50% volume is less than 0.5 carat natural Dimond. This sub-segment has certification rate of 50%. So, at a segment level (natural diamond) and sub-segment level ( less than 0.5 carat) we can see better need of certification for authenticity.

-

On LGD side, I think we need to understand few points:

- Position of certification vendor in the LGD/LGD studded jewellery value-chain – Certification players like IGI is relevant even in the midstream process where jewellery manufacturer buys LGD from grower/polisher. Unfortunately, all LGD are not homogeneous though being grown in labs (if that’s the base premise of the argument against need for certification of LGDs). Therefore, the 4Cs (cut, Carat, Color, Clarity) differs and are equally relevant from B2B buyer perspective. Downstream jewellery manufacturer would be interested to know what he is paying for (say between IF to I3 on clarity or D to Z colour grading).

- On the B2C side of the trade value-chain, one needs to look at it objectively from end market perspective. India accounts for 35% of LGD production globally. The USA leads the consumption of LGD-studded jewellery with more than ~80% of the market demand in terms of estimated volume. Now, looking at it from a US like end-market perspective where organized retail format is more prevalent, certification will still be relevant from 4C and ESG perspective - more so if the certification cost is say <$20 for an studded piece costing $1200 - $1500 (1% - 2% of total value).

While going through different reports, was glad to notice that they have been pretty agile (infact ahead of curve, most of the time) towards tech adoption, customer orientation, product/service innovation etc. May be that is the essence of the duopoly position that they enjoy today:

- IGI was the first among our global peers to issue certification reports for laboratory-grown diamonds globally in CY2005 (way back in 2005)!!

- In 2018, IGI introduced the Dcheck System that enables us to differentiate between laboratory-grown diamonds and natural diamonds in loose as well as in mounted condition,

- Heart and Arrow certification: One of the crucial add-on services is the cut analysis for Hearts and Arrows. Round-cut diamonds tend to exhibit hearts and arrows when examined from the pavilion and the crown of the diamond, respectively. However, a diamond can have a top grading in cut and clarity – but not exhibit Hearts and arrows. This is why Hearts and Arrows is tested independently and is considered a sign of superior craftsmanship. IGI Belgium was one of the earliest among its global peers to introduce the “Hearts & Arrows” diamond reports to the consumer market in 1998.

- In 2021, started including details on post-growth treatment of laboratory-grown diamonds in our certifications, which enable customers to identify whether the laboratory-grown diamonds is “as grown” or has been subject to any post-growth treatments which alter its color.

- In 2021, our Company launched in-factory laboratory set-ups for laboratory-grown diamond growers in India to deliver on-site certification services to our customers. As of September 30, 2024, IGI has 12 in-factory laboratory set-ups located in India. Additionally, adding up mobile labs.

- To further strengthen its brand equity and the credibility and marketability of the certification, IGI has been doing co-branded reports, partnering with a brand or retailer. A portion of the certification fees from manufacturers is paid as commission to the brand or retailer.

From business model perspective, pretty killer business (if one can zoom out and away from macro picture or perceived growth issues etc.): Low Opex, low Capex (has been <3% except for 2023 where they were setting up Surat facility). Lean working capital (service nature of business), Consol EBIDTA north of 55%. Almost duopoly market globally.

Disc: No investment (this may change though)

Tarun

17 Likes

This is exactly what I meant here.

+1 on this.

I visited Westside store yesterday.

Visited Westside SoBo store yesterday.

1 Carat ring was available for just Rs. 17k. (On 10 Gm Silver Base)

Why would anyone want (& need) to go for a certificate for an item of this price?

As long as the retailer/brand enjoys customers’ trust, I will sell easily without certification. The same is reflected with your experience also.

1 Like

I think the point few missing here is, IGI’s revenues are largely driven from B2B side. As long as B2B demand stays, IGI will continue to grow.

Will this change in the future, that is something we need to watch out for.

6 Likes

Is this positive to IGI ? FTA with UK to benefit Indian textiles, leather, toys, gems and jewellery

2 Likes

Where do we get this kind of information , please can you share the source Mr.Manan_Madlani