IGI India A Global Leader in Diamond Certification

1. Industry Overview

- Sector: Gemmology and Certification Services

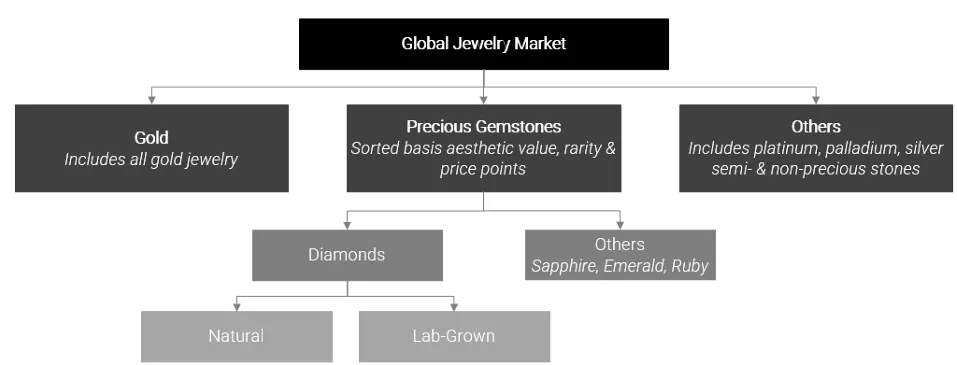

Global Jewellery Market

The total size of the global jewelry market as of 2024, INR 26,600 billion equivalent to approximately USD 320 billion. China, India, and USA Is leading consumer market

Men’s Jewelry Market: Men’s jewelry made up 10% of the global jewelry market in 2023, worth about INR 2,900 billion (USD 35 billion). Common items include cufflinks, gold chains, necklaces, and rings. This market is expected to grow by 8% each year, reaching INR 4,100 billion (USD 50 billion) by 2028.

New Technology in Jewelry: The jewelry industry is using modern technology to improve how jewelry is made and sold:

- Computer design tools help create detailed jewelry designs

- Laser machines make precise engravings

- 3D printers can make complex jewelry pieces

- Virtual try-on features let shoppers see how jewelry looks on them when shopping online

Consumption of Jewellery by Top Countries

Indian Jewellery Market Size

India’s Jewellery Market Overview

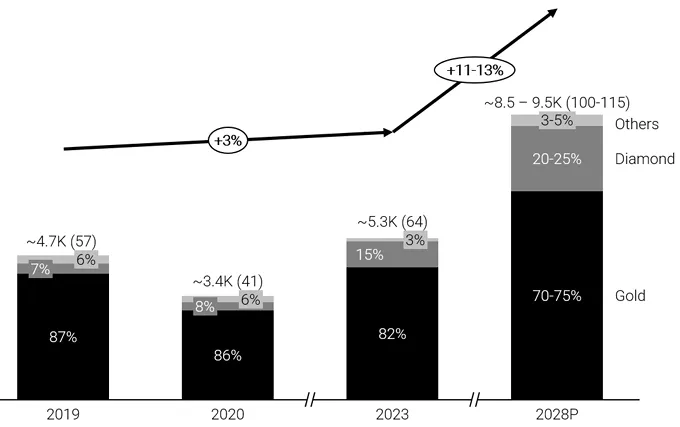

The Indian jewellery market reached INR 5,300 billion (USD 64 billion) in FY 2023. During the COVID lockdowns, jewellery store traffic declined significantly as weddings—the primary driver of jewellery demand in India—were postponed. This led to fewer celebratory and gift purchases, causing the market to contract by approximately 28% to INR 3,400 billion (USD 41 billion) in FY 2020. The market subsequently rebounded after the pandemic, fuelled by pent-up consumer demand, and grew at a 16% CAGR to reach INR 5,300 billion (USD 64 billion) in FY 2023.

Gold dominates India’s jewellery market with an 82% share (INR 4,300 billion) in FY 2023, down from 87% in FY 2019, and is expected to decline to 70-75% by FY 2028. Diamond-studded jewellery has grown from 7% in FY 2019 to 15% (INR 780 billion) in FY 2023, with projected 20% CAGR through FY 2028. The major growth for this fast growth of diamond-studded jewellery.

- Rising discretionary incomes: Growing middle-class disposable income drives jewelry purchases as both fashion items and investments.

- Young urban consumers: Jewelry buying extends beyond traditional occasions, with younger buyers following global trends and purchasing diamonds for daily wear.

- Working women shoppers: Financially independent women are key decision-makers in jewelry purchases, driving demand for both everyday and special occasion pieces.

- Western fashion influence: Growing preference for diamond-studded jewelry (~18% market share in 2023, expected 25-30% by 2028) reflects changing style preferences and increased luxury consumption.

2. Diamond Market

Diamonds come in 2 types: natural and lab-grown (LGDs). Both share identical physical, chemical, and optical properties, including brilliance, fire, and durability. The key difference is origin - natural diamonds form over millions of years underground, while LGDs are created in labs within weeks.

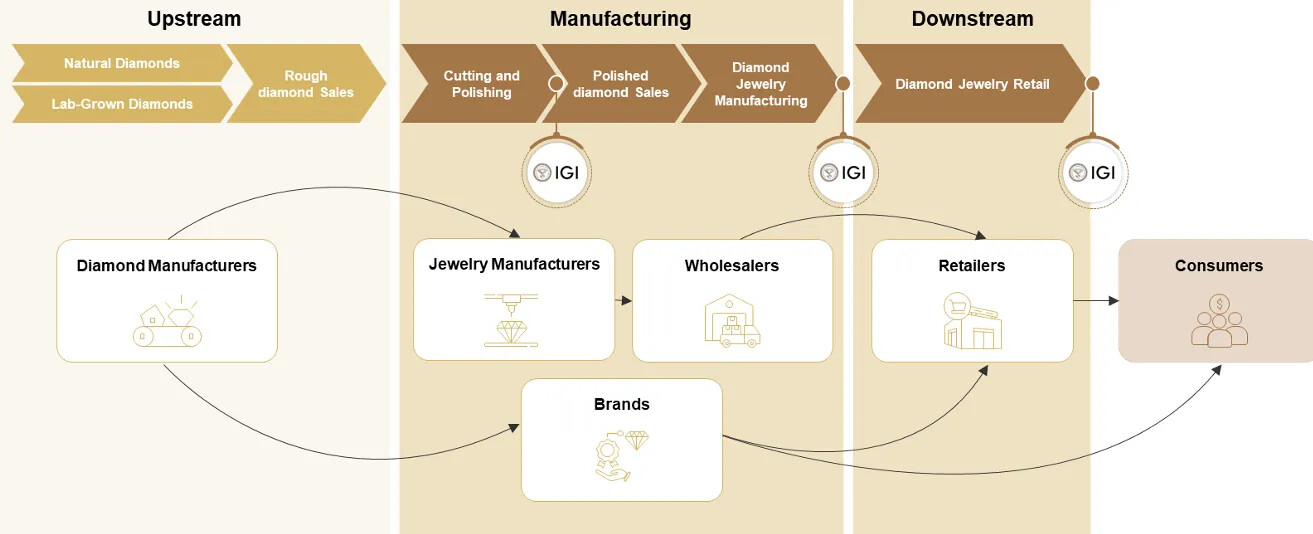

Natural diamonds (NDs) follow a value chain with three major stages from exploration to retail, involving multiple stakeholders.

Value chain of Natural Diamond-studded Jewelry

The process from rough diamond to polished diamond How diamonds are made Link https://www.igi.org/consumer-education/learn-today/natural-diamonds/

- Upstream

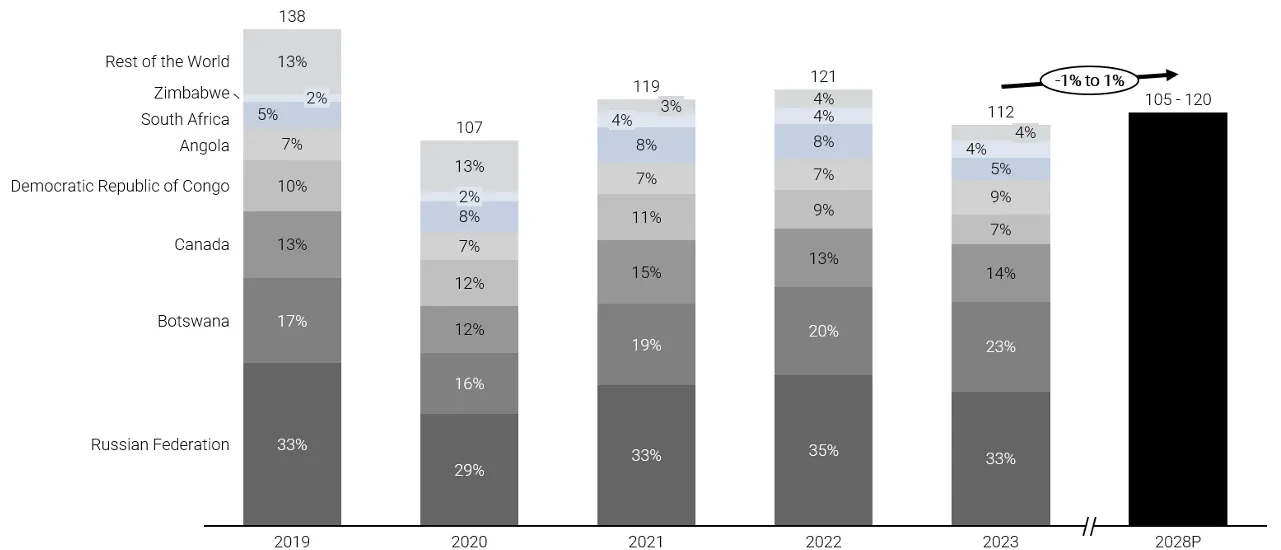

The upstream stage begins with diamond exploration and mine development. Companies search for viable diamond deposits through geological surveys, drilling, and feasibility studies. Once identified, they invest in infrastructure and equipment to establish mining operations. As of 2023, global industrial diamond reserves were approximately 1,700 million carats according to the US Geological Survey. Russia, Botswana, and Canada Hold 68% of total natural diamond mining in FY 2022.

Global Natural Rough Diamond Production

Gems as Rough

- Midstream

Diamond cutting involves a meticulous process. Rough diamonds are analyzed for their characteristics to determine the optimal cutting plan. Advanced technology aids in creating precise digital blueprints. Skilled lapidaries then cut and polish the diamonds to maximize their beauty and value. Approximately half of the rough diamonds are used for industrial purposes, while the other half is used for jewelry. The cutting and polishing process results in a significant weight loss of around 50%.

- Total Rough Diamond Production: This is the starting point, The total amount of rough diamonds mined.

- Industrial Rough Diamonds: About half of the rough diamonds are not suitable for jewelry. These are used for industrial purposes like cutting tools and drilling bits.

- Jewelry-grade Rough Diamonds: The other half is considered good enough for jewelry.

- Waste (Cutting & Polishing): When cutting and polishing rough diamonds, a lot of material is lost as waste. This is shown as a significant reduction in the amount of diamonds.

- Total Polished Diamonds: The final result is the total number of polished diamonds that can be used for jewelry. This is much smaller than the original amount of rough diamonds due to the waste generated during the cutting and polishing process.

Gems as POLISHED then these are sold to consumers

Polished diamonds are checked and certified by expert labs. They look at things like color, clarity, cut, size, and whether the diamond is natural or lab-made. This certification happens before diamonds are sold.

- Downstream

Retail sales are the next step in the diamond value chain, where jewelry retailers sell to customers worldwide. The market is highly diverse, with many different store formats. Since the pandemic, online shopping has become a popular choice for buying diamonds because it offers a wide variety and more options. While the USA is the biggest market for diamonds, demand in Asia is growing faster. - The US is the biggest buyer of natural diamonds, accounting for over half of all diamond purchases. China and India are the next largest markets, but they are less organized than the US market. In the US, most diamonds are sold through well-known brands and stores, while in China and India, a larger portion is sold through less formal channels.

- China, India, and the US are the biggest buyers of diamond jewelry in the world, together making up about 77% of the total market. The US is the biggest buyer, spending around 57 billion US dollars on diamond jewelry. Both China and India have seen a big increase in diamond jewelry purchases, growing at a rate of over 20% per year. China now spends around 13.5 billion US dollars and India spends around 9 billion US dollars on diamond jewelry.

Natural Diamond Jewelry - Market Structure

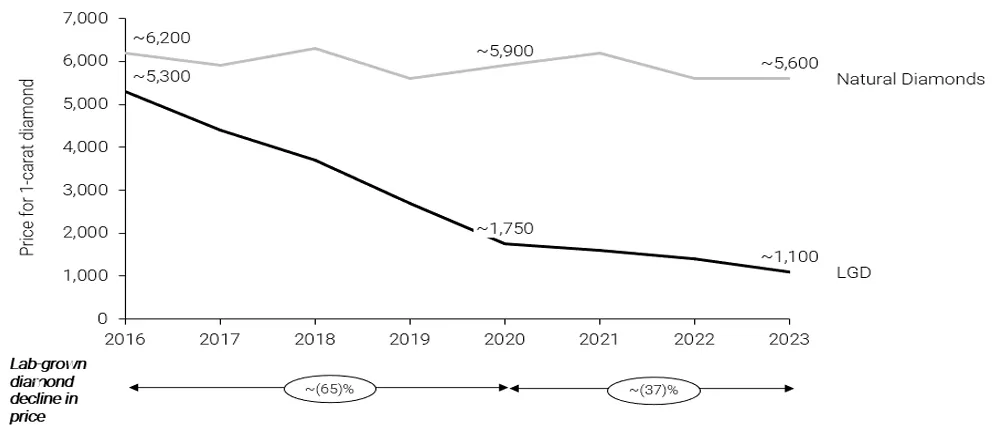

Pricing of LGD vs Natural Diamonds

India is not only a major consumer of diamond jewelry but also plays a pivotal role in the global value chain for both natural and lab-grown diamonds. In FY 2022, India ranked as the sixth-largest exporter of jewelry and loose stones.

India’s Role in Lab-Grown Diamonds

- India is the second-largest producer of rough lab-grown diamonds contributing ~35% of global LGD production in FY 2023.

- Top Exporter India ranked first in LGD exports in FY 2022, with a 29% global export share.

- Skilled Labor: A large pool of highly skilled artisans, leveraging generational expertise in cutting, polishing, and jewelry-making, at competitive costs.

- World-Class Infrastructure: Specialized hubs like Surat, Mumbai, and Jaipur, equipped with advanced technology, support efficient diamond processing.

- The Indian government is actively supporting the diamond industry. They’ve built a large diamond trading center in Surat called the Surat Diamond Bourse. They’ve also introduced new rules to make it easier to trade rough diamonds in India. Additionally, the government is investing in research on lab-grown diamonds and has reduced taxes on importing materials and certifying diamonds. These measures aim to boost the diamond industry, create jobs.

Core Business & Market Overview IGI India’s Leading Role in Diamond Certification and Grading

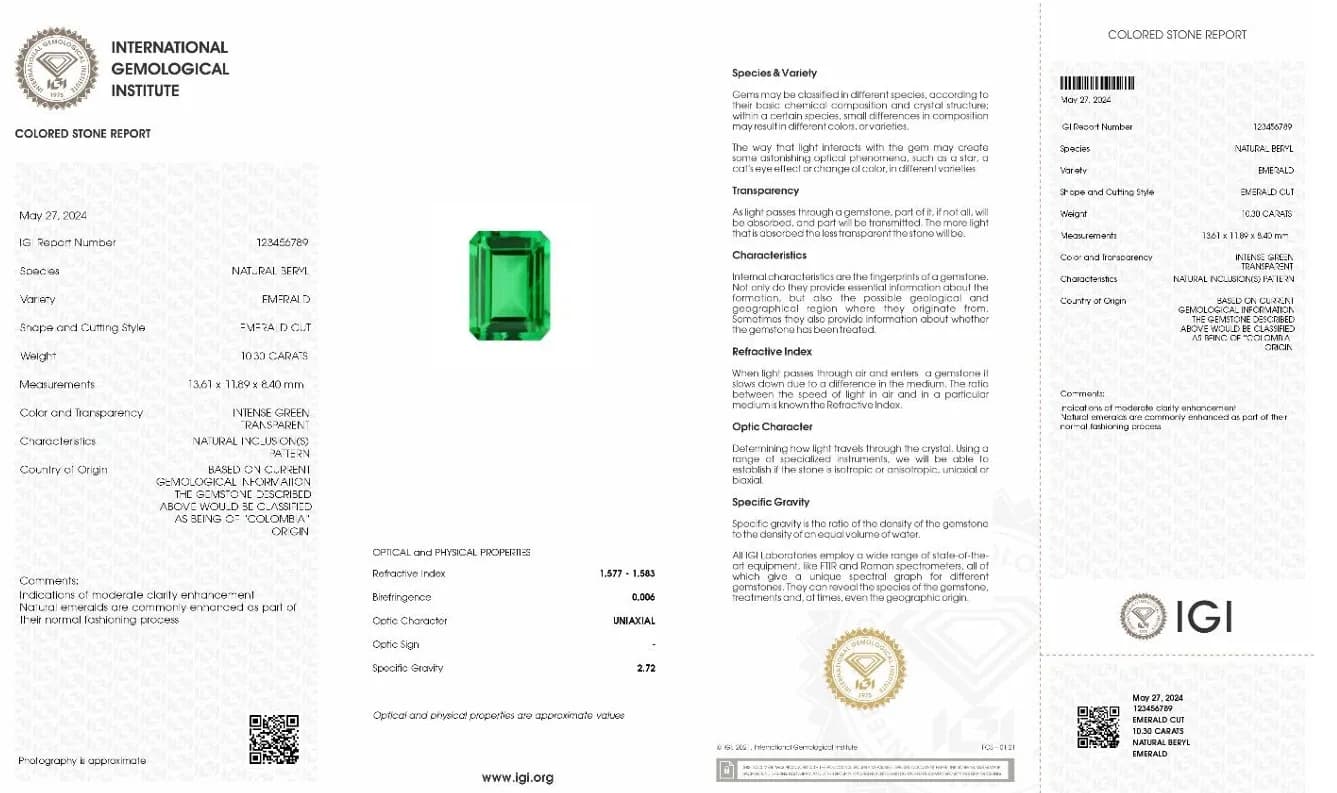

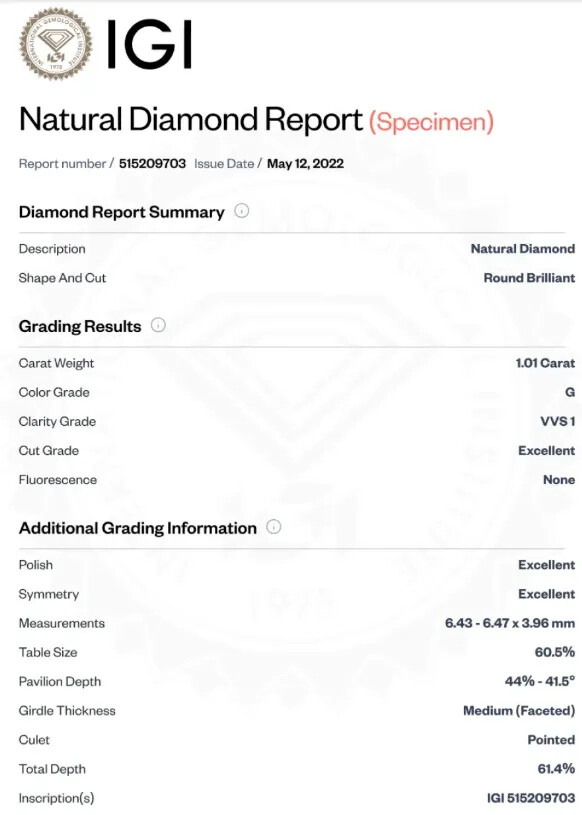

Diamond certification involves a detailed process by independent labs, assessing key factors such as weight, color, clarity, cut, and fluorescence. The 4Cs (Carat Weight, Color, Clarity, and Cut) provide objective grading standards. Certification includes additional tests like laser inscription and origin identification.

Example of Color Grading Scale used for Diamond Certification

- D-F: Colorless - These diamonds are extremely rare and valuable, with no visible color.

- G-J: Near Colorless - These diamonds may show a slight hint of color, but it is usually invisible to the untrained eye. They offer good value.

- K-M: Faint Yellow - These diamonds show a faint yellow or brownish hue, and their color may be noticeable to the naked eye.

- N-R: Light Yellow - Noticeable yellow or brown tones are visible in these diamonds.

- S-Z: Very Light Yellow to Yellow - These diamonds have strong color and are the least valuable.

The Grading Process Link - https://www.igi.org/grading-process/

Cut Grading

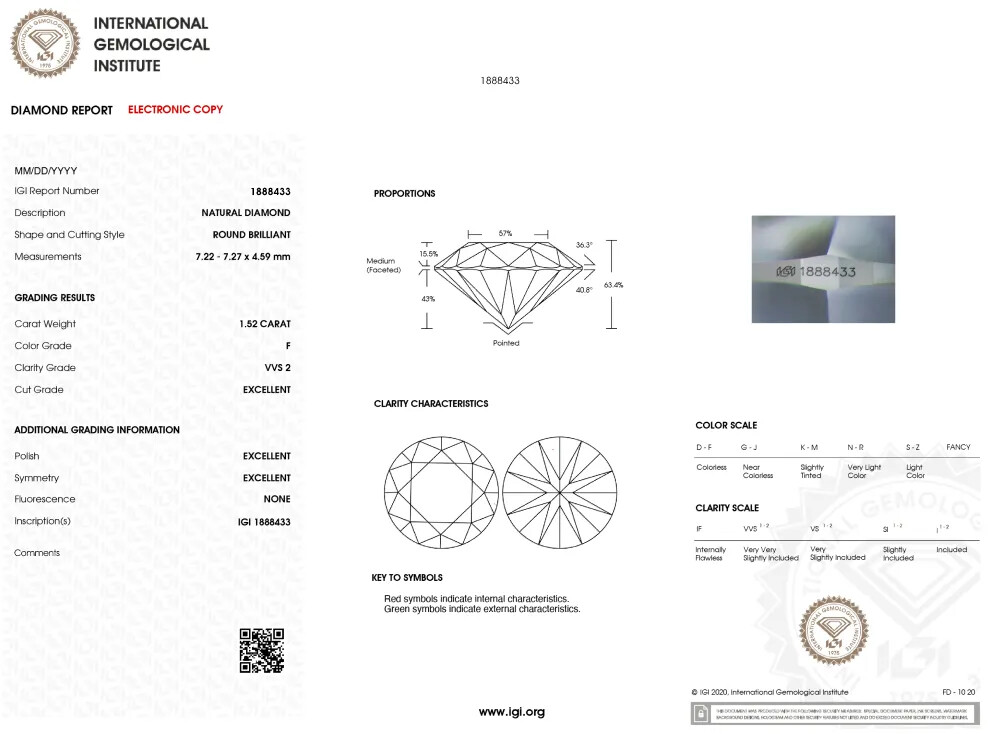

Certification Reports

- A diamond certification report is an official document detailing a diamond’s quality based on standardized grading systems.

- The report includes the diamond’s carat weight, color grade, clarity grade, cut grade, and fluorescence, along with diagrams and laser inscriptions for identification.

- It provides buyers with confidence in the diamond’s authenticity and quality, and is crucial for pricing and resale value.

Click here To see Report’s By IGI

In 2023, around 33 million carats of diamonds were produced globally, with natural diamonds mostly smaller in size, while lab-grown diamonds (LGDs) are produced in larger sizes. Certification penetration is higher for LGDs (~70%) compared to natural diamonds (~65%).

IGI holds a significant global market share in certification, with 42% of studded jewelry certifications and 33% overall. The certification market studded jewelry valued at INR 46-54 billion in 2023, expected to grow at a CAGR of 9-13% till 2028, with LGD certification growing the fastest at ~22%. India remains a key hub for certification, contributing 60-70% of global certifications in 2023.

Drivers for Growth of Loose Stones and Studded Jewelry Certification

- Increasing Consumer Awareness Education campaigns, media coverage, and industry partnerships have raised awareness about certification.

- Surge in Lab-Grown Diamond (LGD) 70% of LGDs are certified globally in 2023, and the demand for LGDs is expected to drive certification rates to 85% by 2028.

- Smaller Diamonds Certification is expanding due to the increasing risk of adulteration and the need for authenticity.

- Growth of the Second-Hand Diamond With the rise of pre-owned jewelry sales, certification assures provenance and quality, making it essential for vintage and rare pieces.

Competitive Advantage of the Certification Market

The loose stones and studded jewelry certification market is dominated by a few players, including IGI, GIA, and HRD Antwerp, due to high barriers to entry such as reputation, high set-up costs, and specialized expertise.

- Leading players partnerships with retailers, this strengthening their market position.

- Certification from recognized bodies like ISO ensures quality and independence.

IGI’s Position

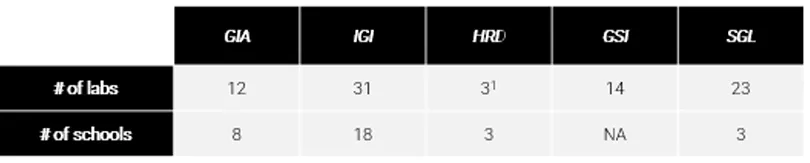

Competitor Lab & schools

Global Company’s in the Diamond Certification Industry

- International Gemological Institute (IGI)

- Gemological Institute of America (GIA)

- Gemological Science International (GSI)

- Hoge Raad Voor Diamant (HRD)

- Solitaire Gemmological Laboratories (SGL)

The core services offered by IGI and its peers include grading for natural diamonds, lab-grown diamonds, and coloured stones, based on the 4Cs (cut, clarity, color, and carat weight). IGI provides additional services such as laser inscriptions, origin reports, quality audits, and damage analysis.

3. Business Overview

- Core Operations: Certification and accreditation services for diamonds (natural and lab-grown), studded jewelry, and colored stones. This highlights that your primary expertise lies in evaluating and authenticating the quality and characteristics of these precious items.

- Competitive Advantages:

- Established global brand presence.

- Technological edge in gem certification.

- International Gemmological Institute (IGI) is a leading global provider of certification and accreditation services for diamonds, colored gemstones, and jewelry.

- Diamond Certification

- Colored Gemstone Certification like rubies, sapphires, and emeralds.

- Jewelry Certification

- Laboratory-Grown Diamond Certification

- Educational Programs

Revenue Sources

- Certification/Accreditation Services Main revenue source.

- Education: Revenue generated through IGI Schools of Gemology, indicating a focus on training and knowledge dissemination within the gemological field.

- Traded Goods: Revenue from selling Dcheck System equipment, suggesting a technological aspect to your business that provides tools or solutions for your customers.

Diamond Reports

- Report offer specialized reports tailored to the type of diamond

- Natural Diamond Report

- Laboratory Grown Diamond Report

- Report provide crucial information for assessing a diamond’s value

- Origin: Clearly identifies whether the diamond is natural or lab-grown.

- 4Cs: Documents all aspects of the diamond’s 4Cs (carat, cut, color, clarity), which are the globally recognized standards for evaluating diamond quality.

Grading and Reporting Processes

1. Fancy-Shaped Diamond Grading

- Polish and Symmetry Grading

- Proportions Qualifications

- Shape-Specific Requirements

2. Jewelry Reports

- Details of mounted stones (e.g., shape, measurements, 4Cs for diamonds, or gemological details for colored stones).

- Precious metal content and purity stamps.

- High-quality photos showing craftsmanship and mounting details.

3. Co-Branded Reports

- Certification fees are shared with the collaborating brand/retailer as commissions.

Customer Segments

- Upstream Market

- Customers: Lab-grown diamond growers and natural diamond wholesalers.

- Purpose: Certification of polished diamonds before selling to jewelry manufacturers or retailers.

- Manufacturing Market

- Customers: Jewelry manufacturers and brands.

- Purpose: Certification of diamond or colored stone jewelry before retail sales.

- Downstream Market

- Customers: End-consumers, either directly (walk-ins) or indirectly through retailers.

- Purpose: B2C jewelry certification services upon request.

Notable Customers and Achievements

- Clients: Includes diamond growers like Kira Diam, jewelry firms such as Morellato, and international luxury brands.

- Significant Milestone

4. Financial Highlights

Financial Performance Comparison (₹ In Million)

| Metric | 3 Months Ended March 31, 2024 | Year Ended December 31, 2023 | Year Ended December 31, 2022 | Year Ended December 31, 2021 | CAGR (FY2021-FY2023) |

|---|---|---|---|---|---|

| Revenue | 2,780.38 | 8,980.14 | 6,385.28 | 4,909.94 | 32.32% |

| EBITDA | 1,734.37 | 4,960.02 | 4,501.18 | 3,351.82 | 36.76% |

| EBITDA Margin | 62.38% | 55.23% | 70.49% | 68.27% | 3.36% |

| PBT | 1,710.89 | 4,554.31 | 4,437.78 | 3,293.61 | 37.11% |

| PBT Margin | 61.53% | 50.72% | 69.50% | 67.08% | 3.62% |

| PAT | 1,260.76 | 3,308.48 | 3,247.38 | 2,417.58 | 37.59% |

| PAT Margin | 45.34% | 36.84% | 50.86% | 47.03% | 3.98% |

My take on Financial Performance

- Strong Revenue Growth company has consistently demonstrated strong revenue growth over the years, driven by increased demand for its services.

- Improved Profitability company has significantly improved its profitability margins, indicating efficient operations and cost control.

- Company maintains a healthy financial position with positive net working capital and a strong balance sheet.

Segmental Revenue Breakdown

| Revenue Source | Three-Month Period Ended March 31, 2024 | % of Total Revenue (Q1 2024) | Calendar Year 2023 | FY 2023 | Calendar Year 2022 | FY 2022 | Calendar Year 2021 | FY 2021 | CAGR (CY2021-CY2023) |

|---|---|---|---|---|---|---|---|---|---|

| Certification Services | 99.05% | 6,206.82 | 97.21% | 4,777.44 | 97.30% | 3,574.30 | 98.01% | 31.78% | |

| Natural Diamonds | 393.49 | 18.82% | 1,224.16 | 19.45% | 1,221.39 | 25.23% | 1,183.51 | 32.45% | 1.70% |

| Laboratory Grown Diamonds | 1,260.41 | 60.28% | 3,338.66 | 53.03% | 2,049.88 | 42.35% | 1,286.73 | 35.28% | 61.08% |

| Studded Jewelry & Colored Stones | 417.36 | 19.95% | 1,644.00 | 25.75% | 1,506.17 | 31.12% | 1,104.06 | 30.27% | 22.03% |

| Education | 11.83 | 0.57% | 53.59 | 0.84% | 38.73 | 0.79% | 24.71 | 0.68% | 47.28% |

| Others | 7.98 | 0.38% | 124.87 | 1.95% | 93.77 | 1.91% | 47.90 | 1.31% | 61.46% |

| Total Revenue from Operations | 2,091.07 | 100.00% | 6,385.28 | 100.00% | 4,909.94 | 100.00% | 3,646.91 | 100.00% | 32.32% |

5. Key Risks and Data Overview

- Dependence on Global Gemstone Market Demand

- IGIL’s business depends on the continuous demand for gemological certification services, which is influenced by fluctuations in the global demand for gemstones and jewelry.

- Impact of Economic Downturns

- Economic slowdowns or downturns can negatively affect the demand for luxury goods, including certified gemstones and jewelry, leading to reduced business volumes.

- Competition from Unorganized Sector

- The unorganized gem certification sector may offer lower-cost alternatives, which could challenge IGIL’s market share, especially in price-sensitive markets.

- Changes in Regulatory Environment

- Any changes in government regulations or policies affecting the gemological certification industry or financial regulations could negatively impact the business.

- Technological Risk

- IGIL relies on advanced technology for gemological testing and certification. Any disruptions, technological failures, or inability to keep up with innovation could hinder its ability to compete.

- Dependence on Key Management

- The loss of key management personnel, including the CEO or CFO, could disrupt operations and hinder the company’s strategic plans.

| Revenue from Top Customers | March 31, 2024 | FY 2023 | FY 2022 | FY 2021 |

|---|---|---|---|---|

| Top 10 | ₹1,023.66 (48.95%) | ₹2,597.92 (40.69%) | ₹1,666.23 (33.94%) | ₹861.88 (23.63%) |

| Top 15 | ₹1,155.27 (55.25%) | ₹2,966.52 (46.46%) | ₹1,914.06 (38.98%) | ₹1,058.01 (29.01%) |

Revenue of Certification Business (in millions ₹)

| Region | Q1 2024 | 2023 | 2022 | 2021 |

|---|---|---|---|---|

| Gujarat | 1,099.62 (53.09%) | 2,849.51 (45.91%) | 1,942.76 (40.67%) | 1,145.43 (32.05%) |

| Maharashtra | 807.04 (38.96%) | 2,688.99 (43.32%) | 2,227.82 (46.63%) | 1,959.38 (54.82%) |

| Rest of India | 160.98 (7.77%) | 645.05 (10.39%) | 605.62 (12.68%) | 469.49 (13.14%) |

| Total | 2,071.26 | 6,206.82 | 4,777.44 | 3,574.30 |

Key observations from the data

- Gujarat and Maharashtra consistently account for over 90% of the total revenue

- Total revenue has shown growth year over year

6. Management and Governance

-

Key Personnel:

- Managing Director & CEO: Tehmasp Nariman Printer

- CFO: Easwar Subramanian Iyer

- Company Secretary: Hardik Desai

-

Board Composition: The Board currently consists of six directors: one Executive Director, three Non-Executive (Nominee) Directors, and two Independent Directors.

-

Board Size: The company’s Articles of Association stipulate a minimum of three and a maximum of fifteen directors.

- Bimal Tanna: Chairman and Independent Director. He is a chartered accountant with extensive experience, having worked with PricewaterhouseCoopers (PwC) for over two decades.

- Tehmasp Nariman Printer: Managing Director and Chief Executive Officer. He has been with the company for over 25 years and possesses deep expertise in the diamond industry. He holds a physics degree and a certificate in strategic management.

- Mukesh Mehta: Non-Executive (Nominee) Director. He is a chartered accountant and chartered financial analyst with over 18 years of experience in private equity.

- Prateek Roongta: Non-Executive (Nominee) Director. He is a chartered accountant and company secretary with over 23 years of experience in portfolio management. He holds a commerce degree and a postgraduate diploma in management.

- Tejas Naphade: Non-Executive (Nominee) Director. He has a background in electrical engineering and business administration, with degrees from the Indian Institute of Technology, Bombay, and Stanford University. He has around eight years of experience in private equity.

- Sangeeta Tanwani: Independent Director. She is the CEO of Pantaloons, a division of Aditya Birla Fashion & Retail Limited. She has a background in pharmaceuticals and business administration, with experience across several multinational companies.