Four years back with half the AUM they had been offered 2500cr which was refused, so I think your estimate is way off the mark. This is a low capital intensity business that generates 30-50% ROEs and is growing at 40% YOY. Also they have 500cr of free cash on the books and like the L&T transaction that will be separate.

3 Likes

Is IDFC AMC part of IDFC First bank?

What is the relation between the two?

From what I understand there is no link

I agree on both counts.

The Equity is 378 Cr, so yes a net profit of 144 Cr would generate nice double digit RoE.

And

The Balance Sheet is 488 Cr.

Furthermore, their management fees, the main source of income is up 20%. That’s a decent clip.

It would be very very nice if the group could get Rs.5000-ish on their hands. Cuz the bank is leveraged 7.5x and an organic infusion of 5000 Cr would mean they could open doors for another 35000Cr of liquidity as and when they want.

2 Likes

5000cr infusion at say 60+ per share will also increase the book value per share of the bank substantially other than providing growth capital for the next few years.

4 Likes

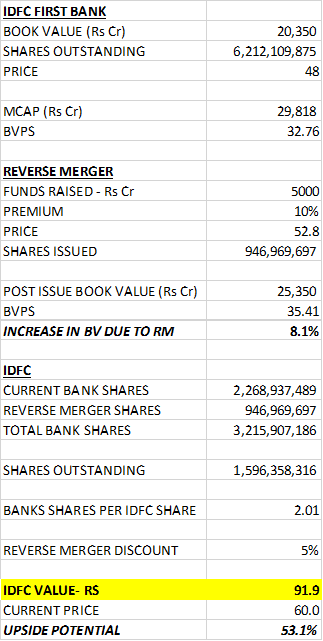

Some calculations below to better frame the discussion, assuming additional shares are issued at a 10% premium and the reverse merger happens at a 5% discount-

IDFC Bank BV will go up by around 8% if 5,000cr of shares are issued at a 10% premium to the current price.

IDFC fair value is around Rs 92 taking into account additional shares that will be issued and a 5% discount.

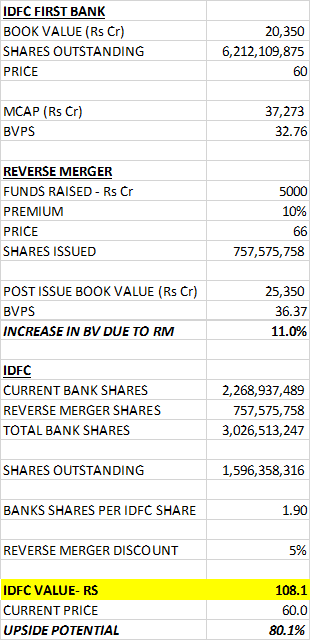

If we take into account the fact that the reverse merger will take atleast 9 months and assume the Bank is trading at Rs 60 by that time then the numbers look like this-

6 Likes

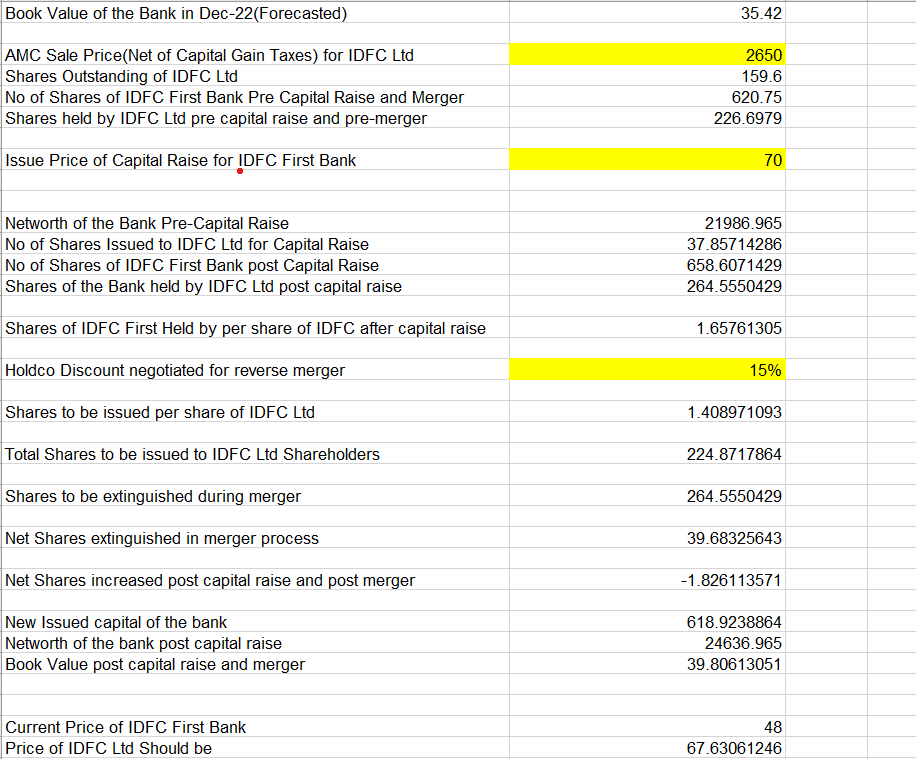

My Calculations are as below: (Assumption is that the entire sale proceeds(net of taxes) from the AMC biz will be ploughed back into the bank).

There are only 3 variables here: AMC Sale Proceeds(net of taxes), issue price for capital raise and holdco discount for reverse merger.

In my view( as shown above), the fair value of IDFC Ltd, if IDFC First is at 48 comes to 67.5. Given the fact that the merger is 1 year away plus a whole lot of egos may be involved in the process(which may derail it), IDFC ltd may trade at a 25-30% premium to IDFC First Bank and slowly move to 40% as the merger probability increases.

9 Likes

No. idfc amc is part of IDFC limited. Its the holding company of the IDFC first bank

2 Likes

Why the merger intent is declared at this moment? As per me, VV is confident of good set of growth and profit numbers in New Year. That will increase the current market price of bank share and will be major factor for deciding swap ratio.

2 Likes

L&T Mutual fund is being sold to HSBC. The deal is at about ~4% of AUMs. Hence IDFC AMC also might get sold at similar valuations

1 Like

Numbers look good.Retail loan growth would be higher it appears.

Given the season for NPA and blow offs like RBL, Bank of Baroda one feels cautious and wants to see NPA. Wants to ensure provisioning doesnt spike given that the bank in is almost entirely retail focused. That’s where the pain is.

1 Like

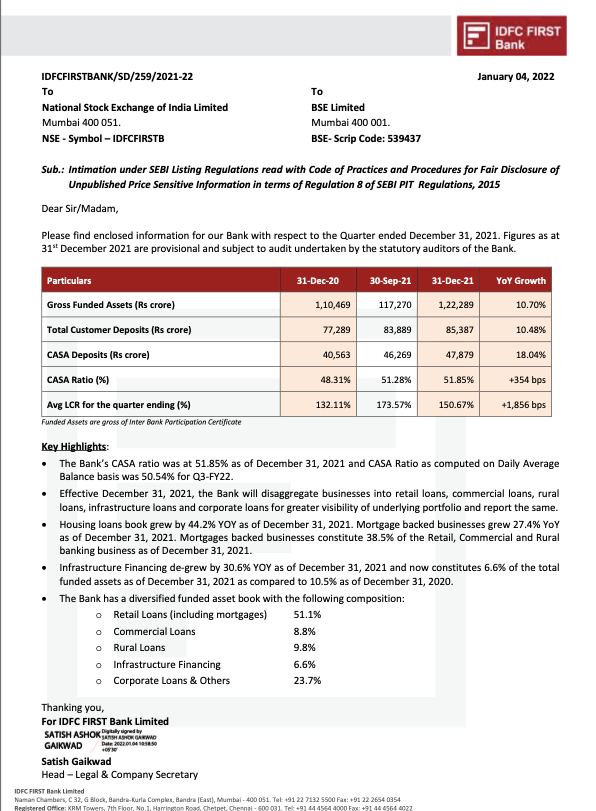

Very good quarterly update from IDFC First Bank.

After breaking down the numbers, it looks like retail loans have grown 9.2% QoQ(42% annualized). Infra loans have come down to 8050 crs in Dec '21 from 10140 crs in Sep '21. Seems like VI exposure(infra account) has come down by 1500 crs in the quarter.

Execution by VV is spot on in terms of guidance on growth and retailisation.

2 Likes

1.)Infrastructure loans came down to 8071 cr (6.6%)from 10,142 cr in Sep 2021.

2.)Despite this the total funded assets went up 4.28% QOQ.

3.) Bank is making efforts to bring down LCR although the deposits and CASA have increased marginally. This is due to increase in loan book size and also low cost deposits replacing the legacy high cost borrowings. We have to check the impact on Net interest Income and NIMs when the results are out.

4.) I would have been happier had the deposits decreased.

We have to watch out for Asset quality & provision, operating expenses when the actual results are out.

1 Like

Have a question. When a bank talks about non-funded exposure like for e.g. IDFC first bank used to say about a 2000Cr non-funded exposure to Vi. what exactly it means? 1500Cr disbursed is funded and 2000cr is committed but not disbursed. But that 2000cr is not an obligation right? Can a bank decide not to disburse at any time? How does it really work? Any pointers with an example ?

1 Like

Retail loans upto 85,000cr, was 66,000cr in Q3FY21. Means YOY growth is 29%! Amazing numbers and 7,000cr growth in a single quarter with huge growth in mortgage and housing loans.

9 Likes

I think the way the Business update is presented is very confusing for someone who does not track this company very closely.

It is evident in the market reaction over the past two days.

AU Bank has done similar numbers and look at how they presented it and the market reaction for the same.

We should highlight YOY Retail growth Advance,Corporate growth Advance numbers along with Overall book numbers.

The way its presented as 10%YOY is what market thinks we have grown where as our core area Retail has seen much higher.

11 Likes

LCR for the quarter improved by 18.56 percentage. Can anyone explain what will be effect of this on profit of bank.

The banks which are having > 4 % market share pay a lot in calling customers on a regular interval and they also give regular mail for credit cards. Until and unless customers issues a card/ requests DND/or block their calls.

Hdfc and icici is most regular in calling

Puls they have have tie-ups with a big corporations like

amazon > issues icici amazon pay credit card

Flipkart > Axis Bank Bus credit card

Puls these banks have an advantage on getting a share from salaried customers.

The three main banks are hdfc, icici and sbin many companies in India gives only three option for telling a bank for salary credit

That explains their market share

On the other hand, IDFC bank is the least interested bank for issuing credit cards:sweat_smile:

I have an account in it you will never get mail/call for a credit card until and unless to raise a request same for Kotak

2 Likes