I think it is 2000 funded and rest unfunded.

Vaidyanathan said, “So we have Rs 2,000 funded exposure and Rs 1,244 crore of non-funded exposure. And if we imagine the worst case, let’s say 100 percent loss, even if you take a full Rs 2,000 crore, our capital adequacy will be 14.6 percent. So, we have a pretty focussed balance sheet and we will deal with this issue.”

Now, as regards to the obligation, if the non-funded exposure is revocable then no obligation to honor but if irrevocable then yes. But then I guess this could be a bank guarantee to the Government. But if so, what’s the implication of the telecom relief package by Govt in terms of returning bank guarantees? Any view welcome!!

Bank guarantees are owed to the government and are revocable by the govt. Govt had started returning the guarantees to VI and Bharti Airtel in Nov/Dec…it’s seems likely that majority of the BG will be returned back to the telecoms per the relief package, in which case IDFC non-funded exposure also reduces significantly.

I honestly feel we should rest the VI issue on this page. It is done and dusted, VI paid 1500 cr + 170 cr (interest as well) . They will pay 500 crore this mid Jan. Non funded is subjected to Dot and GOI.

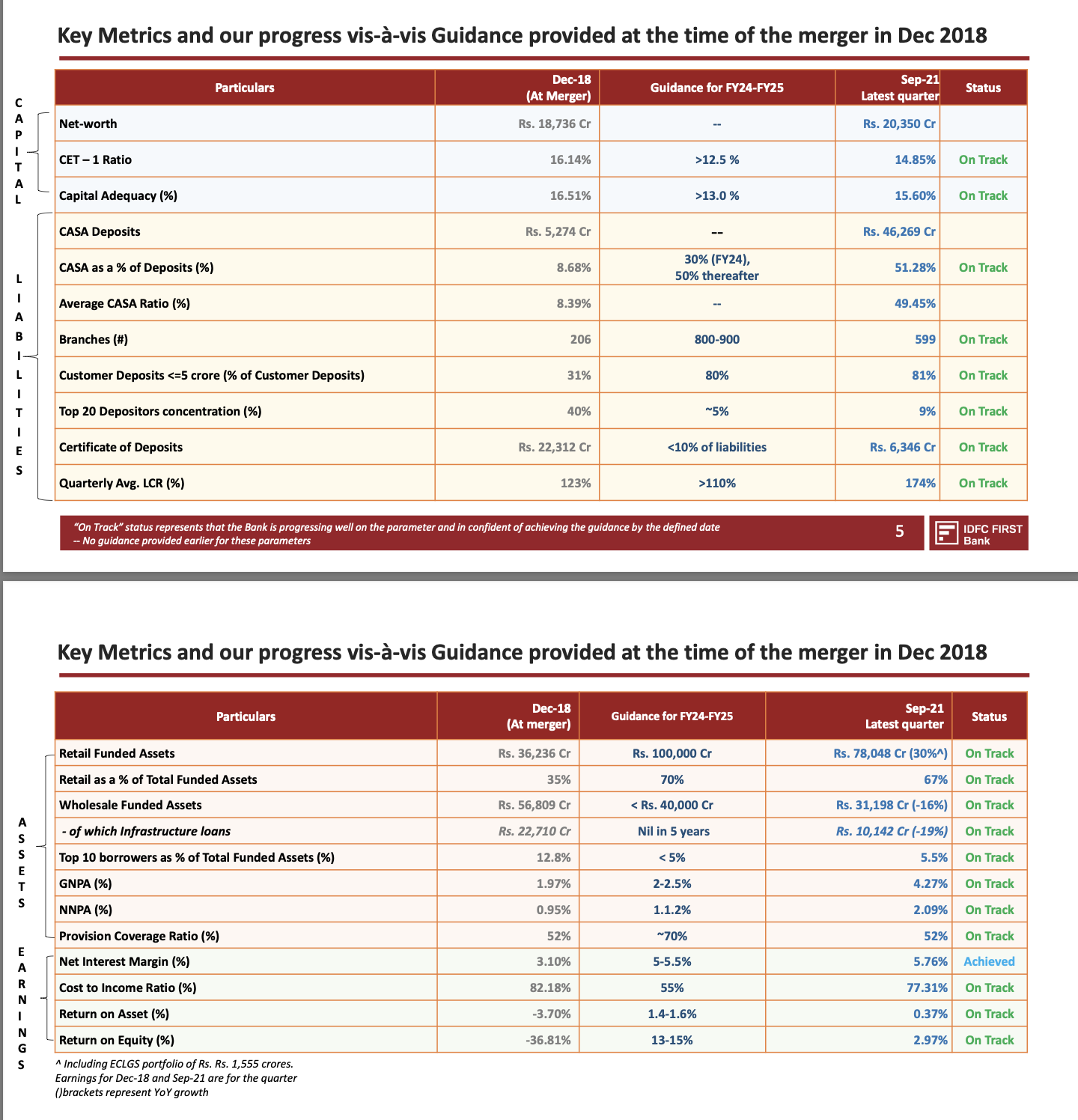

May be we should focus on how retail loan segment is shaping up for the bank. ( NPA, recoveries…etc)

I think AU Small Finance has actually declared much better numbers. The total advances have grown 10% qoq as opposed to 4% for IDFCB. This is in the festive quarter, with minimal covid impact. I understand the retail growth and infra de growth but at the end of the day we’re buying the entire book. 6k crore of de growth still to come, the numbers this quarter seem distinctly average to me considering the industry standard.

Using qoq since covid makes that the best barometer for growth.

Explosive growth can also end up being a cause for concern. We should try to understand the granularity of where the growth comes from. In lending, higher growth is NOT always better. growth is front ended, or seen. Npas are back ended or unseen.

In idfc first case most of the growth is coming from home loans so overall portfolio risk is going lower. In fact, their mfi segment is slower growing than entire book.

If you look at retail segment, growth for idfc first has also been 10% qoq on 78k cr loan book, 7k cr growth. But what i would also look at is where that 7kcr is coming from. In idfc first case, quality of growth is incrementally getting better. That is what investors might be missing.

IDFC was listed in 2015 at 65 rupees, in 2022 it is trading at 49 with huge equity base which bars it to raise QIP capital also. This is one of major underperformer at street where Index rose from 20K to 63K in 7 years and this leggard is still trading at pathatic levels. Untill merger with IDFC is completed this will be in dark and road ahead for IDFC investors is dark as well.

There is a problem with being too much into mortgage. Housing finance interest spreads are not too much. Being a bank they have to be as competitive as any other bank. If they have to work like a HFC, then they have to look for different set of borrowers to get a higher spread. What stops HDFC bank from going into home loans only given that they underwrite better than most? DCB bank always tried to be heavy on mortgage backed securities and what has it achieved? Share value destruction. Everything needs to be balance. Infact I can only see NIMs of IDFC first bank stabilizing or going down from here

i would urge you to read this thread thoroughly. This exact question has been discussed at least 3-4 times & beaten to death.

" what stops X from doing Y" is not the best way to understand the problem. A better framing is: “why do we have this entire spectrum of lenders who operate at all sort of price points from 7% to 25% ROI?”. You will find the answer on this thread & others too!

Reg home loans: NIMs is one way to look at it: two other important ways need to be considered:

Since it is safest form of lending, NPAs are very low & loss of capital even lower.

Operating costs are very low.

For these reasons Housing finance (for HFCs, & banks like IDFC) is a very remunerative proposition.

Another advantage of Home loans is that it stays for a very long period of time and thus contributes to the profits of the bank for over 10-20 years. Secondly, in one of the recent interviews of a Kotak top management I heard that home loans help build long term relationships with customers. Hence, the bank can continuosly gain wallet share from a mortgage borrower by selling more products. So, even if the NIMs are low, it helps in the long term. I consider this to be customer acquisition cost. While fintechs spend money for customer acquisition, atleast IDFC makes money.

There is one more reason now to justify in housing loans. It is the overall real estate uptick and booming house constructions. There is enough evidence to prove that housing as a sector is in for a long demand driven trajectory. If a bank is not tapping that, they are missing a huge avenue to deploy the funds.

Reg home loans: NIMs is one way to look at it: two other important ways need to be considered:

Since it is safest form of lending, NPAs are very low & loss of capital even lower. Operating costs are very low.

In that case one should really buy one of the efficiently managed retail focussed HFC

" what stops X from doing Y" is not the best way to understand the problem. A better framing is: “why do we have this entire spectrum of lenders who operate at all sort of price points from 7% to 25% ROI?”. You will find the answer on this thread & others too!

There seems to be no end to bankers trying different things and blowing up. Same thing could have been said for a Yes bank or RBL bank. Lending is easy but lending that balances growth, asset quality requires calibration on both the levels.

I agree with a lot of what’s been said. Home loans have many advantages and the growth there is good to see, but this positive needs to be balanced with growth of the overall book, NIM, asset quality and profitability.

I still think the bank will get where it wants to be, the question is how long it will take. Every investment has to have a time frame in mind, since every passing year substantially reduces the CAGR even if the co. does get there eventually. When the merger was announced, Morgan Stanley had said the turnaround will take at least 2 years (pre Covid) and a lot of us on this forum had dismissed them. Important that this thread remains an objective discussion.

On this question, the 6k cr of de growth yet to come along with possible Omicron provisions don’t bode well.

HFCs by default carry higher risk since they don’t compete in the same segment as banks do. For eg: a CoF of under 6% for IDFC FB and gradually lowering allows it to offer housing loans starting from 6.5%. This is not the same as HFCs which have to rely on debt raised from financial institutions. Further, because HFCs do not have CASA, asset liability mismatch (ALM) mismatch is a huge issue for them since if liquidity dries up tomorrow as it happened in the post ILFS era for many NBFCs, then they can default on their liability side. A bank rarely sees CASA withdrawal unless the bank is collapsing.

Don’t know about RBL but surely the troubles of Yes didn’t stem from its housing loan portfolio but more from its corporate loan portfolio right?

You are right …YES bank is in this situation,because of Mr Kapoor lending policy to corporate. He used to give loans to the organizations where other banks denied them. If the organization X needs 100 crores Yes gives them 80C and still charges interest for 100C ( because X was unable to get money from other banks they used to agree) …

You misunderstood. I was replying to @sahil_vi’s why do we have this entire spectrum of lenders who operate at all sort of price points from 7% to 25% ROI?”

Just operating in different ROIs and ignoring the basics doesnt get one great results. They try and do things that finally proves that it doesnt work. By that time they would have caused all the damage. The point is not about YES bank or RBL bank. It is not about retail or corporate lending. They were mere examples. At some point these guys would have said: "oh HDFC and Kotak wont lend to some corporates. we will operate and show what can be done ". But we know the end result.

Also I mentioned, “an efficiently managed retail focussed HFC”. GRUH finance was able to show it. They didnt have CASA. i know people will now start saying they had HDFC bank backing etc CanFinHomes is still doing very well. Banks have their own customers and they cant and wont really lend to some set of customers where as the HFCs can do. Why do you think in the last 2-3 years there are many HFCs, NBFCs that are doing co-orignation with banks. Why cant the bank go and lend to those customers directly. The banks want only customers with good credit and where risk is less on their balance sheets.The flip side they cant get good credit spreads. They will takes these risky customers with their co-origination