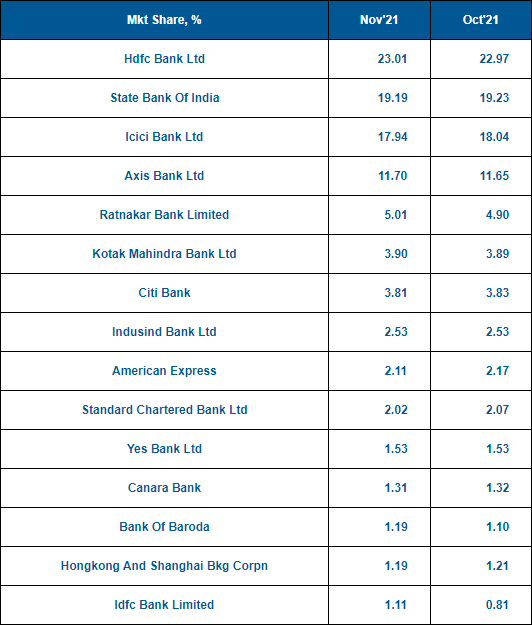

Guys who think idfc will gain a significant market share in credit card markets i think otherwise .I have 2 credit cards 1 axis and idfc ,i hardly use my idfc card due to the poor reward rate and there are no merchant offers or no cost emi schemes on the card either ,I would not even issued it if it was not life time free .

I am also a idfc bank customer and there are 3 reason i am invested ,

1)lowest banking charges be it the best intrest rates ,zero charges for unlimited imps,low atm fees provided you can maintain 25k minimum balance.

2)The best feature for me is the 3in1 account linked with zerodha where i can send any amount to my demat in an instant with one click ,this is best feature for me or anyone else who uses zerodha to invest in equities,we all know how important few minutes are when your favorite stock crashes.

3)There customer service is also class apart ,miles ahead of axis or even hdfc,industry leading response time and you can even call them at 1 am in the night and they will answer you phone.This is what modern banking should be why have tons of branches and pay rent when you can do all the work from phone banking

beg to disagree.

I am also using metal credit card (ONE) issued from IDFC. Rewards are good and best part is they give point for every rupee spend which is not the case with any of the banks’ CC. redemption is super cool. transaction approval is new age other than OTP thing (you have to slide a pop on ur mobile screen to approve it else its declined). hopefully, if they market well these little things, they can gain market share overall quantity wise.

plus there are 'multiply rewards" thing every month. yes, they have less offers than other banks and that should be fine because ultimately in these offers, someone has to burn their pocket.

Check with them once and you will appreciate some of all of these facts.

axis ace

2% cash back any transaction offline or online

5% on any utilities bill payment through google pay (electricity,dth,water bill)

4 % on swiggy and zomato

idfc first select (all cards have same reward ratio)

.75% on offline spends

1.5% on online spends

2.5 % on every spend after you spend 20000 in a month

biggest disadvantage on ifdc is it doesn’t give rewards on any insurance be it car or life insurance which makes your rewards zero.Just like you ,i only use my card for absolute necessities and these expenses are inevitable and form a major chunk for me making the card useless for me,it might be useful for someone but i can be assured that 90% user will save more money using other bank credit card.

To buy 500 shares of idfc with your credit card rewards only assuming you get 2.5% back on all transactions highly unlikely you would need to spend 10 lakhs if your buying price is 50rs per share.

with that kind of spending look into hdfc imperia ,it will be free for you plus you will get almost close to 1 % back on all spends ,not including the amazing 10 to 33% discounts on amazon ,flipkart and flight tickets,plus many many extra benefits.

marketing wise this is brilliant but it does not show the accurate picture and a credit user will figure this out ,they do offer the lowest interest rates true but that will only be given to people with good cibil score who don’t default on payment and those who do will be charged the same as other companies maybe a little lower .

Lets not make this thread a credit discussion group ,you can pm if you want to ask something about credit cards (i am not an expert though).I think for idfc to gain market share, they need to differentiate the rewards on the cheapest and the most expensive card and come up with more offers to get the market share and launch brand specific credit cards and partner with more brand channels to offer discounts and no cost emi.They are the new kid in the block so we just need to give them some time.

New kid on the block yes.

Another headwind, the outbreak of Omicron and lockdowns caused thereof, will aggravate npa, while making growth sluggish, due to lessened economic activity.

We should hope for an average quarter, and no major bad news. Best case.

For the same reasons, unsecured lending is looking grim, currently. However, IDFCFIRST is a wise lender, with VV at the helms we can count on his experience.

Their books are diversified and they function strictly on CIBIL scores (much like Bajaj Fin).

VVs overall strategy is to start accounts small, and based on their paying patterns, increase the loan amount. This has worked well for him during Capital First days.

And fresh accounts are started based on strong credit score.

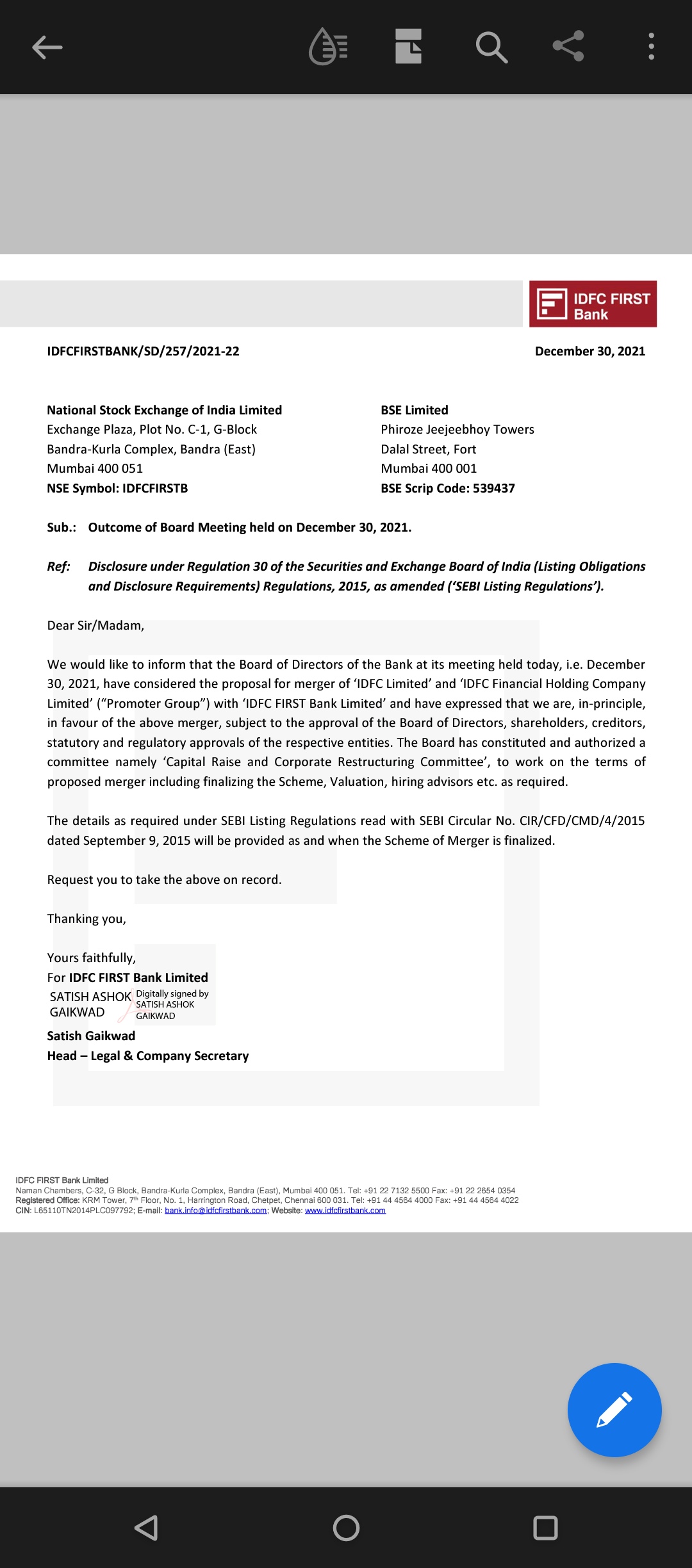

Should secure growth capital for idfc bank while securing value unlocking for idfc shareholders. Will be interesting to see what the swap ratio is and by how much it increases book value for the bank.

More important than the swap ratio / relative valuations is who heads the merged entity? Does VV remain at the top or will Anil Singhvi command the reigns? I’m a little sceptical now.

Benefit or not to IDFC FB shareholders can only be ascertained post the swap ratio is released. If IDFC has all assets on book - it does bring in an additional billion dollars of capital? If not billion dollars, whatever would be the liquid assets?

I feel IDFC Ltd investors will benefit in this reverse merger. They will get a slightly favourable swap ratio, and in return the bank is only happy to get the capital, for which they’d otherwise would have to dilute equity by preferential allotment in the open market.

I trust VV to not let IDFC shortchange IDFC FB shareholders. So whatever the swap ratio should benefit given LT objectives of the bank i.e. growth capital at a higher valuation (not the paltry 50 odd right now). Atleast the valuation at which last cap raise occured.

Do note that the committee has been named as ‘Capital Raise and Corporate Restructuring’ Committee. So one thing is clear:

With two different boards heading the 2 companies, the merger is not going to be a cakewalk for IDFC Ltd like it will be for similar companies like Ujjivan and Equitas.

The proceeds of the AMC biz will first be ploughed back to the bank in the form of a capital raise. Capital Raise will happen at an opportune time(not before Dec-22 is my guess) when IDFC First Bank’s growth and PAT numbers may lead to a re rating to atleast a price of Rs 70-80/share or even higher.

If shares are first allotted to IDFC Ltd at say 70/share or higher and then reverse merged with IDFC First Bank at a 10-15% holdco discount, then it will be a win-win situation for both the companies.

How does IDFC First Bank win?

Gets to raise fresh capital for growth at say Rs 70-75/Share (or even higher). Even QIP investors will be happy since the new capital raise is coming at a decent premium to the last QIP price of 57.3.

Reverse merger at a 10-15% holdco discount means that IDFC First Bank gets the entire fresh growth capital without diluting any equity( on the flip side some shares will also get extinguished). This is any bank’s dream: Fresh Growth Capital that comes along with equity extinguishment.

How does IDFC Ltd?

Finally the entire holdco structure will be collapsed and shareholders will see value unlocking.

Price of IDFC Ltd can trade at a 25-40% premium to IDFC First Bank(Depending on what holdco discount the market assumes for the merger).

Lastly, right now it is just the intent of the two boards that has been made public. To first sell the AMC biz and dissolve the complex structure is atleast going to take 7-10 months and negotiations between the two boards can take another 2-3 months in my view

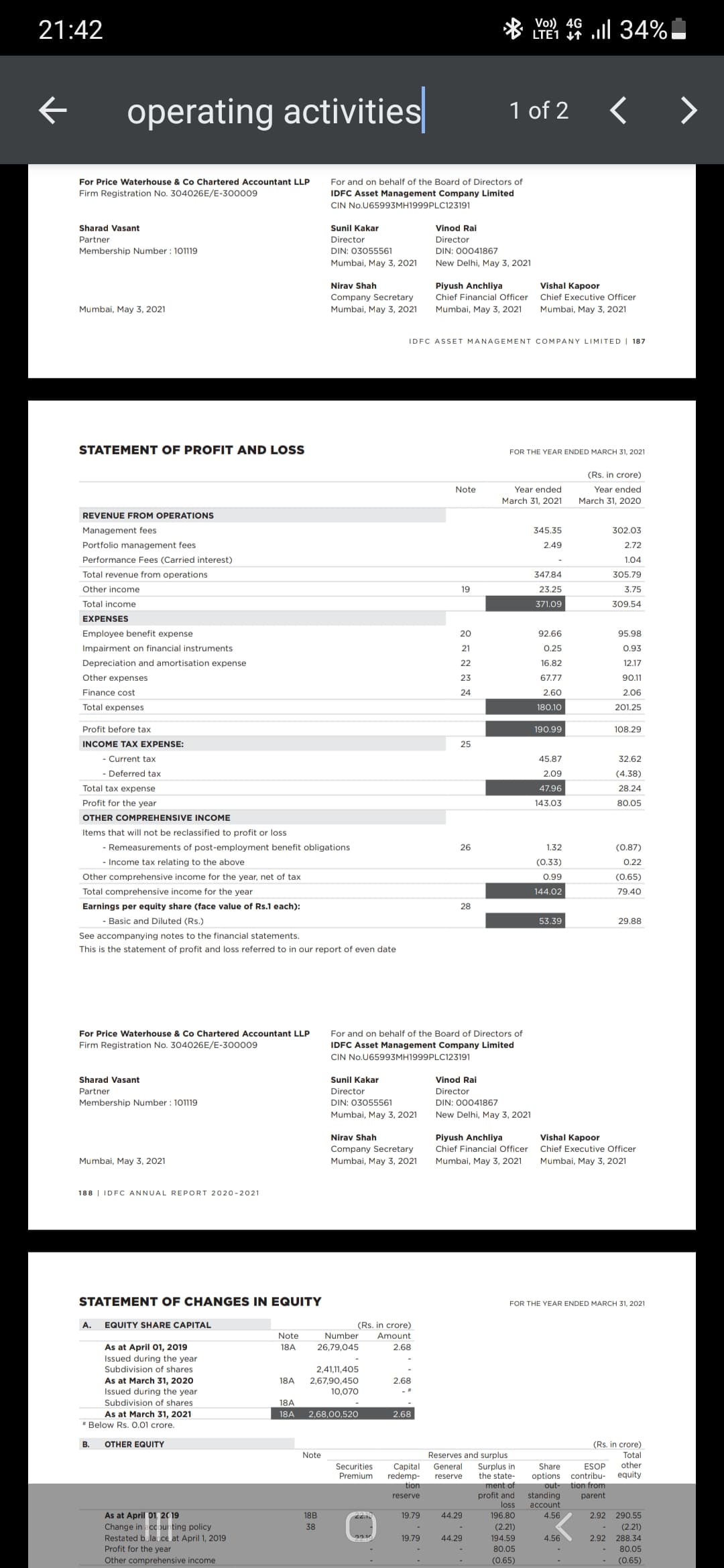

For 144Cr of profit, one would best get 10x.

The buying party would then get 10% return on investment.

From what I read, IDFC AMC is a cash and a debt fund for most part, with expense ratio as low as 0.10% for some schemes, and growth in AUM has been unimpressive. So, there is a low possibility of getting a higher multiple of earrings than 10x.