Yes, idfcfirst is underpriced. Plainly speaking, it’s not a stretch of imagination to see that quarterly PPOP(pre provisioning Operating profit) will be to the tune of 1000Cr. Post Tax 800Cr. Annualized 3200Cr. Will most likely be more.

With 621Cr equity shares, this comes to EPS of 5.2

So, essentially at CMP, the stock is trading at 10PE

That’s mispriced, but only for people who believe VV can deliver.

While your thought process is right , but calculation of EPS is never done at PPOP level but at net income level post provisioning . However if VV can sustain his 2-1-2 formula he explained @ AGM ( 2 % GNPA , 1% NPA & 2% credit cost ) then it will consistently compound with healthy ~ 6% NIM

DOT has already granted 4 years moratorium for spectrum dues. VI and Airtel have availed it. So there is zero possibility of DOT encashing the BG of Rs 1244 for next 4 years. That makes the BG risk free and the approx 3% BG annual charges become risk free income to the banks. Common wisdom would dictate that DOT and VI take steps to remove this free gift to the concerned banks.

I think we can lay the VI story to rest on this forum. Exposure has come down dramatically and it’s quite clear that the rest will be repaid since the company isn’t going into insolvency. Beyond that, all plans for capex, growth etc. are quite irrelevant to IDFCB since they don’t own any equity.

Short question, IMO is when can the bank now increase the profitability and ROE. With industry leading NIM of 6%, average profitability should also translate to high ROE and valuations.

VV had said the jaw will start widening in FY23, that remains the key monitorable along with growth in credit book. Both at average levels should see serious upside from current price.

Apparently, in BNPL side of story is not looking good. Atleast, in other companies, many of them.

I think for next couple of quarters its important that we see a very controlled NPA situation in this bank, for the general public and institutions to start looking positively.

Yes, ROE will get into double digits only post FY23 when cost to income ratio improves which is now beaten due to opening of new branches.

For now, I feel the bank is positioned well, business wise and stock price wise.

I had a question re IDFC. I know the AMC business is housed under different entity. But I wanted to understand if IDFC FB ever plans to get into the insurance business? My understanding of banking is that if you can basically underwrite well and keep the credit losses under control, the fee income will take you places and that in the case of banks is credit cards (IDFC FB is ramping it up), MFs (not under IDFC FB purview for now, maybe after reverse merger) and insurance (not sure of the status here?)

Also, key monitorable for me is loan growth from now on. At the end of Q2, IDFC FB was sitting on excess liquidity and they have another 1600crs add into as a result of VI repayments. Toll road issue is also just a non-issue, for most part of it.

IDFC FB today is sitting on lots of liquidity. January update should be interesting for the entire Q3 loan growth etc.

This is because they have more deposits than they can lend out currently. The credit off take in the entire system is low and most banks are sitting on excess liquidity.

The 1600 cr is shareholders capital, the excess liquidity is excess deposits ie liabilities.

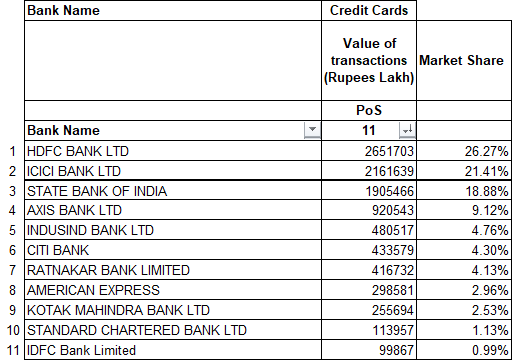

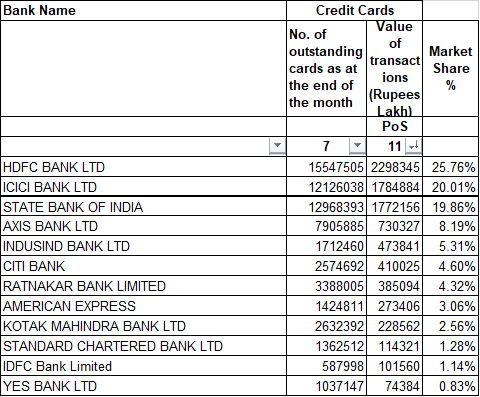

Yes, I track the market share based on the value of POS transactions every month rather than outstanding cards as some guys like Canara Bank / Yes Bank have a lot of dud cards outstanding and that doesnt reflect the true picture. On that basis IDFCF is already the 11th largest player and will prob be in the Top 10 before the end of the year as this is based on Oct data.

The IDFC First Bank Share has improved to 1.1% by Nov end. Hopefully in next few months it would be at position 9 (given Citi business would merge with Axis or Kotak)

I have a feeling that RBL like cases will strength the importance of having a very good corporate governance and transparent management play in any organisation, including banks.

With continued good corporate governance and transparent management at IDFCFB (in my view), hope the conviction will keep getting strengthened.

I think the value of transactions should be in lacs. Good job otherwise. The level of datacrunching would have required some time. Also would be interesting to know who’s the 4th highest incremental card issuer? SBI, HDFC, ICICI, Axis / IndusInd? W