Our MD & CEO, V Vaidyanathan, speaks to Zee Business on Q2FY22 results

Our MD & CEO, V Vaidyanathan, speaks to CNBC TV18 on Q2FY22 results

Someone had asked what was the Mumbai toll roads that had been declared NPA in Q1, read a research note from Ashika Inst securities that mentions that its IRB (EXTRACT BELOW)-

IRB just raised Rs 5,000cr funding too which is another positive development, with most of funds being used for debt repayment- IRB Infra to raise Rs 5,347 crore from GIC & Spain’s Cintra; deleveraging & growth capital deal drivers

Assuming quarterly profit of approximately ~500 cr for FY23 and an ROE of ~ 7%, the P/B can be around 2.2 (current Axis Bank P/B with similar RoE). Assuming quarterly profit of ~ 800 cr for FY 24 with an ROE of ~ 13%, the P/B can be around 3.2 (current ICICI P/B with similar RoE).

Upside: the entire financial space is rerated and current valuations of other banks don’t reflect future valuations IDFCFB may get.

Downside: Bank may not be able to deliver on above numbers, although I have roughly tried to stay within guidance.

That translates to returns of around 50% annually for the next two years at least from CMP. Good to know our expectations for comparison with other opportunities.

Disclaimer: These are extremely rough, back of the envelope calculations - to be taken with a pinch of salt.

Except that IDFC FB should also grow its loanbook significantly over the next few quarters and then credit card biz will give it a lot of fee income (one reason for higher multiples of big banks). I expect steady compounding to happen in IDFC FB if they are able to maintain their guidance.

Next quarter is extremely crucial for the bank as Vodafone payments are due by then. All eyes on equity infusion in Voda.

Is the Vodafone loan only left with one last payment to close the loan? If yes then how much is the payment outstanding and what will happen if vodafone didn’t honor the payment (assuming it’s only the last payment)?

All growth in loan book, higher fee, lower cost of funds etc eventually translate into profit and we’ve seen that the market only rewards profits. Not just for IDFCFB but all banks. And the profits I’ve estimated are already factoring in a lot of growth from current levels. Unless the growth is much higher (doubtful IMO), the ~50% returns projection should hold.

ICICI Direct has put out a note. Have tempered their expectations on credit growth (14% from 18%) and also on NII for FY23 (13% growth from FY22)

And VI is in talks with SBI for new loans. Will that be used to pay down existing loans or used for tech deployment? Pretty sure, SBI will put a man on the board to monitor how the money is being spent.

What is the confidence level that Vodafone payment will happen? Want to see any opinion from members in this group .

Looks like, VI might ask IDFCFB to take equity for the loan given, so that they can avoid the interest payments. Wouldn’t it be good if they offer a discount on the market price?

IDFCB has not given a loan to Voda; they had bought NCDs which are due between Dec and Jan. What Voda is discussing with SBI is loans recast. NCDs cannot be converted into loans or equity.

That’s even better. Good to hear that they NCDs. Definitely re-rating can happen

Yes and if Vodafone doesn’t pay on time IDFCB can drag Vodafone to bankruptcy court if it wants or even have them declared as defaulters, this is why in the Annual Report and in recent media interactions VV has mentioned law of the land when asked about Vodafone. IMO Vodafone will pay back all Ncds on time.

VI has applied to DOT for deferring the spectrum+ payments of Q2, Q3, Q4 to apr-may 22. Considering that the most likely reason for previous communications minister’s departure was, for allowing VI to reach imminent bankruptcy, it is now almost certain that DOT would make sure that VI not only survives but survives well on a sustainable basis. The GOI has the maximum financial stake of 1.6 lakh crores revenue in VI and the Govt will not allow that money to sink as it is well within the capability of DOT and MOF to protect it.

Similarly, PSBs will also make sure that VI gets the desired restructuring. The private banks have relatively very small stake and should be able to exit by Jan 22. The new communication minister informed on the ‘Times Now’ platform that he will come out with further reforms to strengthen the industry.

So IMHO the anxiety for VI exposure is over for IDFCF and situation would be crystal clear by 31 Dec. The brilliant minds of this forum would do better if they shift focus onto other aspects of IDFCF functioning.

If that happens, worst is behind for IDFCFB. CASA, Creditcard, Homeloan, Retiring Infra loan, Toll Road Provision Recovery, Reverse merger with IDFC to get some growth capital. All is well. The interest Rate up regime is also favourable for banks. It is going to be tailwind only.

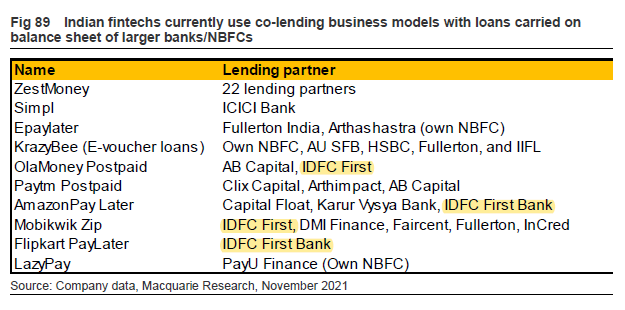

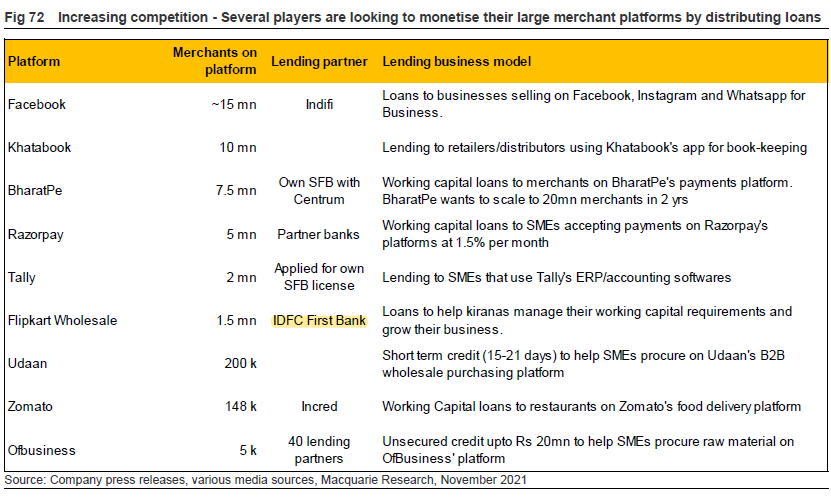

Was reading Macquarie’s IC report on PayTM and they discuss fintechs and its amazing how many partnerships IDFCB already has in this space.

They have one with CRED too. All loans on CRED’s platform are essentially loans by IDFC FB. Goes to show that if banks transform into omni channel fintech payment system of sorts - it’ll push out fintechs out of the game pretty bad - but this will require a holistic change in thinking