IDFCB has launched their private banking offering

Is the banks’s higher number of issued shares (compared to other banks) coming its way of growing shareholder’s investment (or will come it’s way in future)? What do you all think bout it ?

I have heard this in many analysts mentioning that the number of outstanding shared has got almost doubled in past few years.

IDFC First Bank Revises Interest Rates On FD & RD: Now Get Up To 6% Returns

When ROE for the bank is higher than the loan book growth, the bank doesn’t need additional external capital. As per the commentary from the management and my understanding, the bank would again need capital at the start of 2023. We can be comfortable once ROE> 15% i.e atleast 3000 cr PAT per year. Until then the bank will keep diluting equity.

Also, the valuation at which the bank raises funds is important. If the bank raises equity at 2bv or 3bv, the final BV would increase. If they raise it like they did in March/April 2020, the book value would go down. So, once the bank starts to deliver on PAT numbers, the stock price would get re rated and it can raise fresh equity at good valuations.

So, I think situation would improve as IDFCFB starts to deliver numbers as per management guidance.

I believe, last equity Dilution happened Because of NPA. Otherwise, as per the management, their goal is to switch the lending book from wholesale to retail.

Now, the management is expecting a sharp decline in NPA since covid is history, infact, Telecom and toll road NPAs are likely to be reversed.

So, IMO, there won’t be Dilution anytime soon.

Not able to recollect all the figures correctly but i think …total funded + guarantee exposure to idea is around 3200 cr. And bank has only provided 450 cr. Some TV channels report they have provided around 50% which is wrong. I think they have provided earlier around 800+ crs but reversed half amount of it and utilized for covid provision.

India’s first-ever standalone metal debit card's launch announced Looks like an interesting offering!

Good article by Ken

This might give some relief -

Telecom Department Starts Returning Bank Guarantees To Bharti Airtel, Vodafone India (cnbctv18.com)

Hi @sahil_vi,

In case if you are any one in this topic knows if Vi does not pay last installment (of funded exposure which is due in Dec 2021) to the IDFC First then do IDFC has to provide for full loan taken or it will be equal to just last installment ?

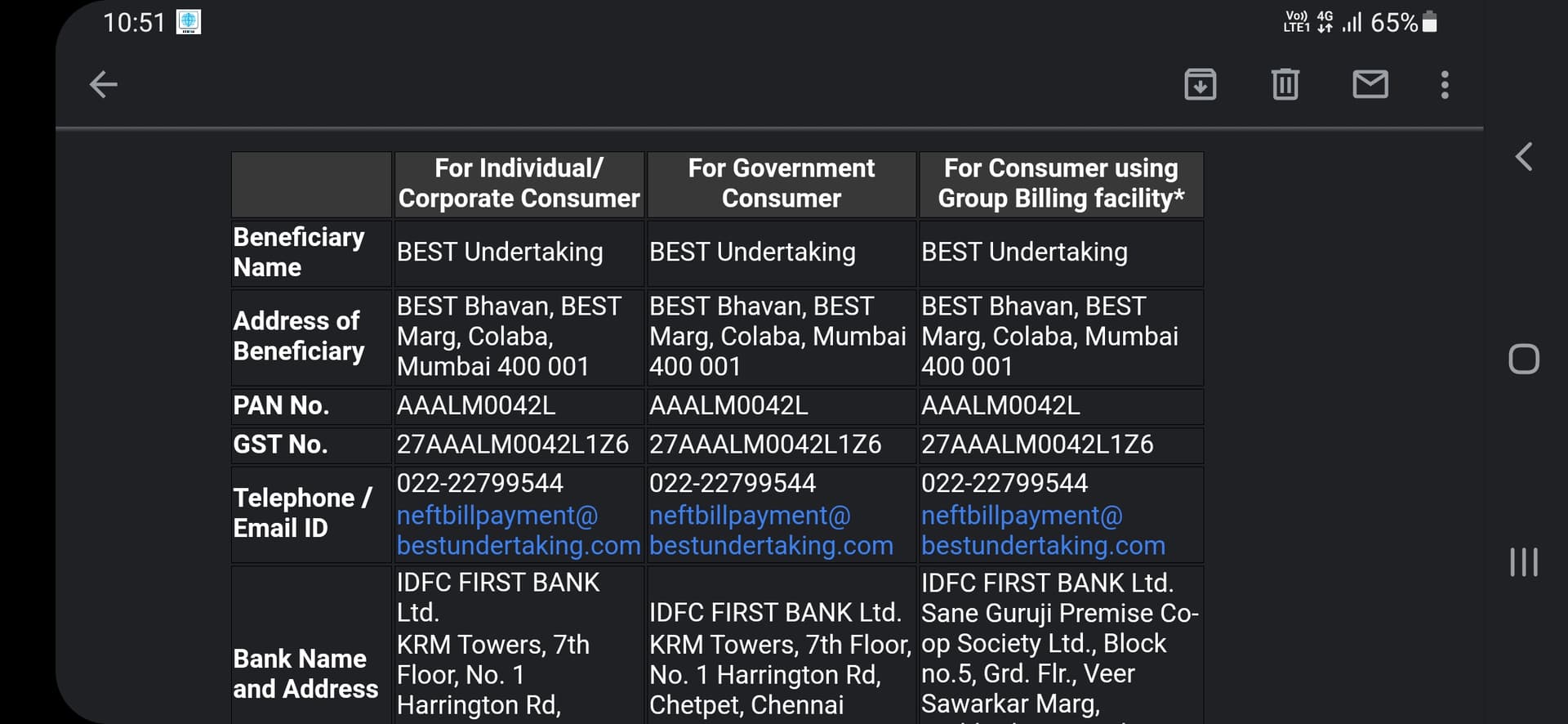

Looks like Mumbai’s civic body BEST is using IDFCFB for payments.

It isn’t a loan. It’s a Non Convertible Debenture (NCD) that Vi issued. The way NCDs work is that they are (in most cases) fully redeemed only upon maturity. So Vi isn’t due to make any payments before the maturity date (early Jan 2022).

So if Vi defaults, the loss would be 100%.

Good news but doesn’t clear clouds over IDFC FB yet. Main thing is the funded exposure of 2000crs.

All signals so far in the telecom sector thus far have been positive though. Tariff increase, likely withdrawal of one time spectrum charge litigation.

Let’s see how things pan out.

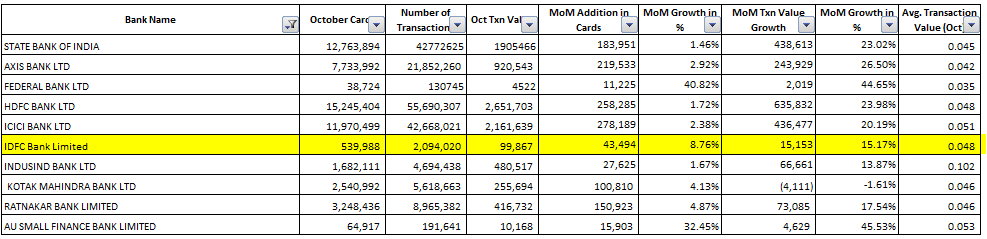

In the meantime, card growth data. Good growth in card addition. I guess the big spenders are still not onboard (most corporates have tie ups with HDFC for bank a/c opening) since the txn value growth lags the biggies.

Intresting twit

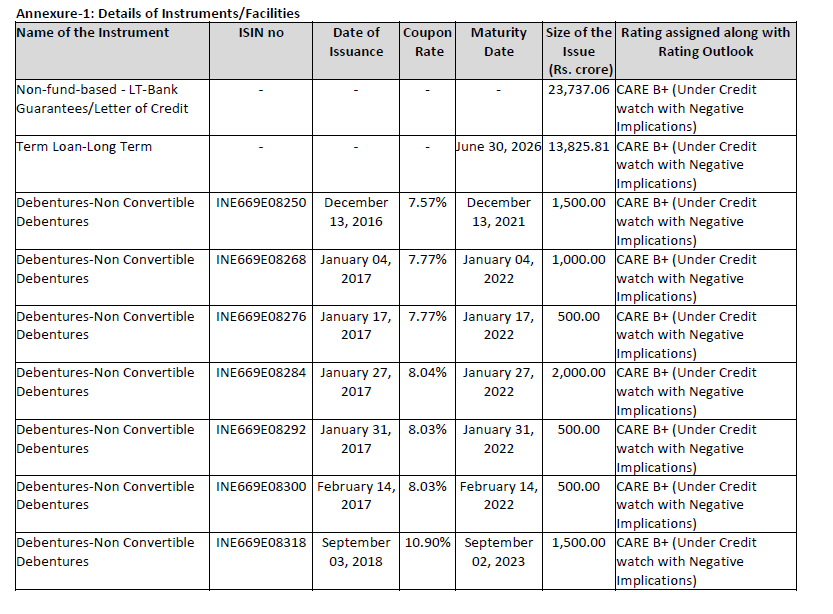

Looks like we can finally lay to rest the Vodafone issue. There is only one NCD due for repayment in December 2021 and IDFCB had confirmed they own it (not clear how much). Expecting the provisions made to be released over Q3/Q4-

Edit- Added below outstanding NCD’S-

Excellent news. Hope the bank makes an official announcement to the exchanges if they recieve the payment as its material information that is important for shareholders to know about.

Expect a disclosure in January since I believe the 2k crs NCDs due on Jan 27 are the ones that IDFC has subscribed to.

Their presentation mentions Dec /Jan so they definately are getting some repayment in December otherwise they wouldn’t have mentioned it. Maybe they have 1000cr exposure to both NCDs or something.